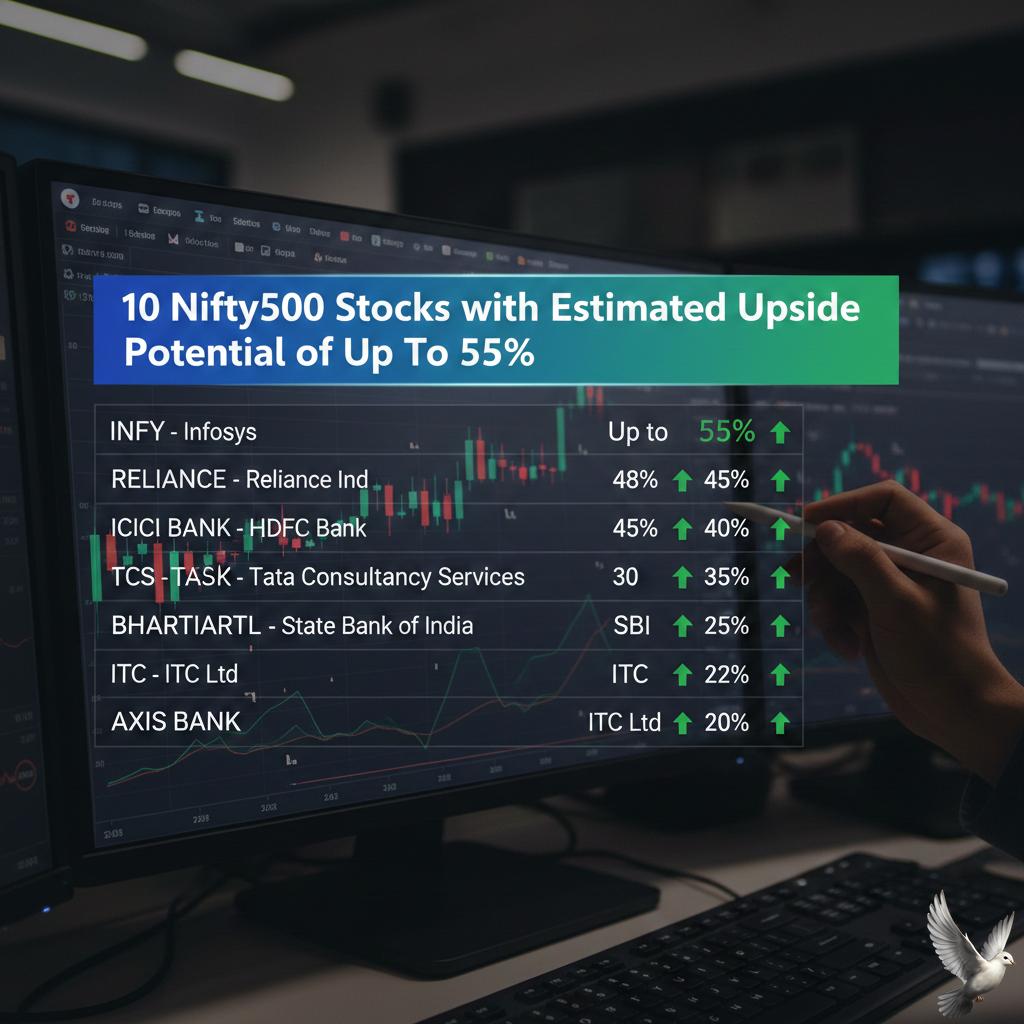

10 Nifty500 Stocks with Estimated Upside Potential of Up to 55%

The Indian equity markets are currently navigating a period of significant volatility, characterized by sharp sectoral shifts and evolving analyst sentiment across the Nifty 500. Recent data indicates a "bloodbath" on Dalal Street, with the Nifty 50 falling below the 25,500 mark. This downward pressure is largely attributed to heavy sell-offs in the IT sector, where global concerns regarding artificial intelligence disruption have dampened investor confidence.

Market indices reflect this turbulence clearly. As of mid-February 2026, the Sensex has plunged over 1,000 points to settle near 82,595, while the Nifty 50 closed at 25,471.10, representing a 1.30% daily decline. The broader Nifty 500 has not been immune, though select pockets of resilience exist. Specifically, while the IT index tumbled 5%, the Financial Services and Consumer Durables sectors have managed to edge up, providing a fragile buffer against the wider market slump.

Analyst consensus from Trendlyne suggests that strategic opportunities remain within the Nifty 500 for those looking beyond current volatility. Ten specific stocks have been identified based on sequential earnings growth and multi-analyst coverage. These companies are projected to offer upside potential ranging from 40% to 55% over the next 12 months.

In the banking and financial space, State Bank of India (SBI) continues to hit near 52-week highs, recently trading at 1,198.60. Other notable performers include Bajaj Finance, which gained 2.57% to reach 1,024.75, and Shriram Finance, which holds steady at 1,065.80 despite broader selling pressure. Eicher Motors has also shown strength, rising 1.54% to 8,065.00, positioned just 0.67% away from its 52-week peak.

Corporate earnings for the Nifty 500 show a nuanced recovery. While revenue growth has been modest at approximately 5.7% year-on-year, aggregate profit (PAT) for the Nifty 500 excluding the top 50 companies grew by a strong 20.7%. This indicates that mid-cap and small-cap constituents are currently driving profit momentum more effectively than their large-cap counterparts.

Sector-wise, the Financials, Materials, and Industrials segments are expected to contribute nearly 62% of incremental earnings over the next two years. However, caution remains the dominant theme. The Earnings Revision Indicator (ERI) has dipped into negative territory for most sectors, reflecting more analyst downgrades than upgrades in the immediate term. Investors are closely monitoring the 25,400 support level for the Nifty, which remains a critical psychological and technical baseline for the current market structure.