**AI Spending Dampens Stock Buybacks for Major Tech Companies**

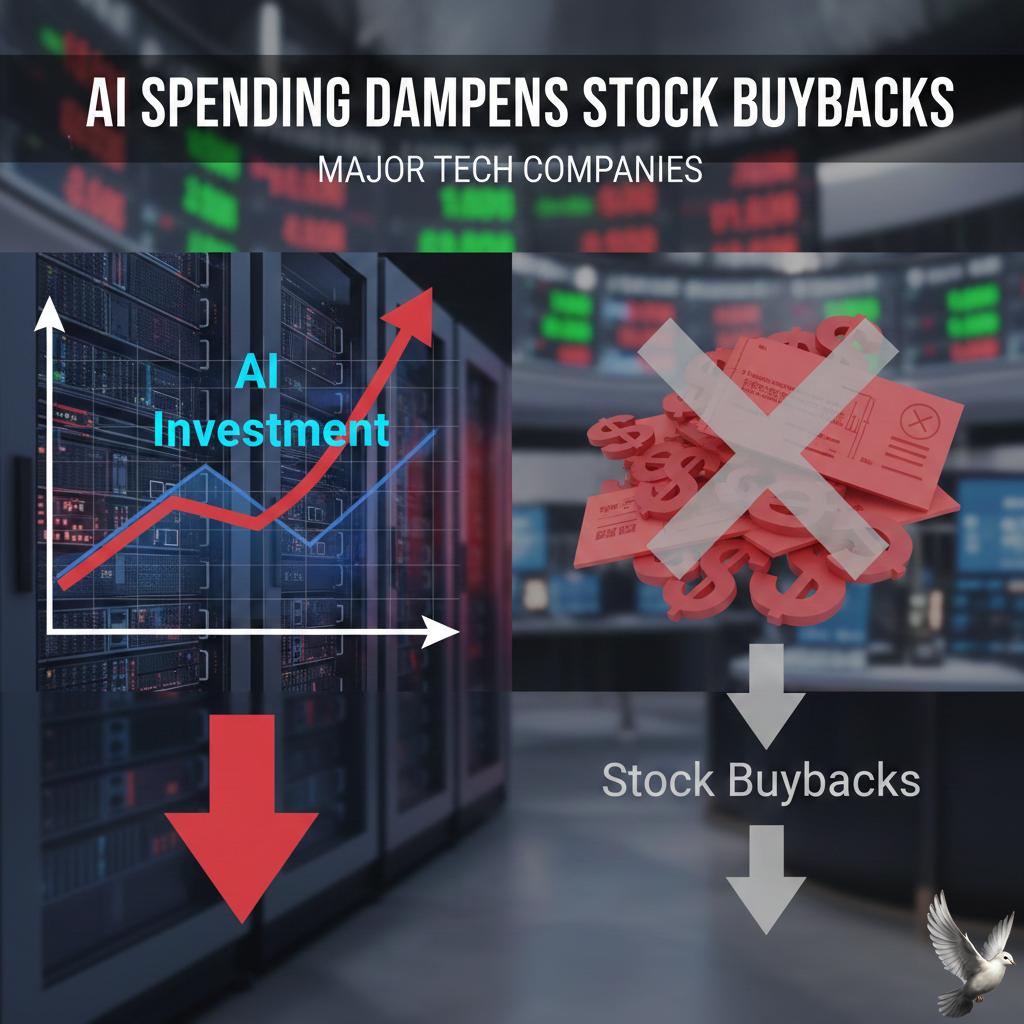

Major technology corporations are undergoing a structural shift in capital allocation, prioritizing massive infrastructure investments over traditional shareholder returns. As of February 2026, the industry's four largest hyperscalers—Alphabet, Amazon, Meta, and Microsoft—have signaled a collective capital expenditure (CapEx) package of approximately **$650 billion** for the current year.

This surge represents a **60% increase** from the **$410 billion** spent in 2025. This pivot is largely funded by a significant retreat from stock buybacks. Combined share repurchases for the top tech firms fell to **$12.6 billion** in the final quarter of 2025, marking a **74% decline** from the peak of **$48 billion** seen in 2021.

Strategic Infrastructure Spending

The primary driver of this expenditure is the race to build AI data centers, procure advanced chips, and secure power-hungry computing clusters. Amazon has disclosed plans to spend nearly **$200 billion** this year, with a heavy focus on its cloud unit, AWS. Alphabet’s projected spend is expected to exceed **$50 billion** to support its Gemini ecosystem, while Microsoft is on pace to surpass **$140 billion** in annual spending to double its data center footprint.

* **Hyperscaler Total:** **$650 billion** (Projected 2026)

* **Sector Growth:** **165%** increase in CapEx since 2024

* **Market Sentiment:** **$900 billion** in collective market cap lost following recent earnings reports as investors weigh spending against immediate returns.

Market Volatility and Divergence

While the broader market remains cautious, a clear divergence has emerged between companies providing the infrastructure and those developing consumer software. Nvidia remains a primary beneficiary, with analysts expecting quarterly revenues of roughly **$65.5 billion** due to its **80% market share** in AI accelerators.

In contrast, software-heavy firms face increased scrutiny. The S&P 500 software and services index recently saw a **10% decline** in a single week, as investors voiced concerns over the timeline for AI monetization. Despite the "AI headache" for some, Meta has found a silver lining, reporting growth in AI-driven advertising revenue that helped its stock initially resist the broader sector sell-off.

The Long-Term Outlook

This transition suggests that Big Tech is evolving from a high-margin software business into a capital-heavy "AI utility." While reduced buybacks have removed a historical stabilizing force for stock prices—leading to higher volatility—tech leaders maintain that these investments are essential. The current build-out is being compared to the industrial revolution, with infrastructure spending now equating to roughly **0.8% of global GDP**.