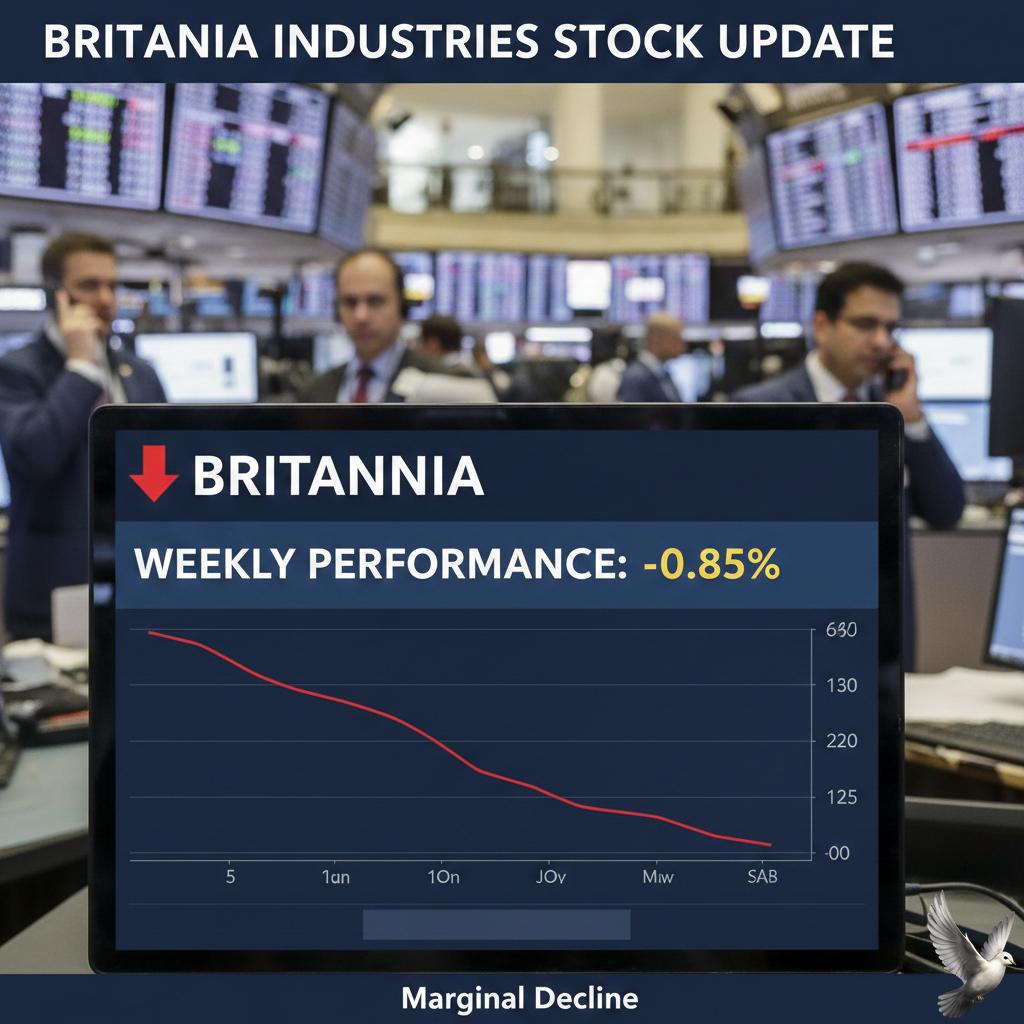

Britannia Industries Stock Update: Weekly Performance Records Marginal Decline

NVIDIA Market Brief: February 2026

The global semiconductor industry is entering a historic "giga cycle," with annual sales projected to reach **$1 trillion** in 2026. This surge is driven almost entirely by the transition from AI model training to large-scale inference, creating an unprecedented demand for high-performance computing infrastructure.

NVIDIA remains the dominant force in this landscape, commanding an estimated **85% to 90%** market share of the AI accelerator sector. The company’s financial performance continues to break records, with Q3 fiscal 2026 revenue hitting **$57 billion**, a **62%** increase year-over-year.

Data Center and AI Infrastructure

The Data Center division remains the primary growth engine, contributing **$51.2 billion** in the most recent quarter—up **66%** from the previous year. This growth is fueled by the massive rollout of the Blackwell architecture.

CEO Jensen Huang has noted that Blackwell demand is "off the charts," with cloud GPUs effectively sold out across major providers. The upcoming **Rubin architecture**, scheduled for the second half of 2026, is expected to further increase average selling prices and maintain technical leadership.

Key Financial Indicators

* **Stock Price:** Trading near **$185.41**, with market expectations targeting a move above **$200** following the February 25 earnings report.

* **Gross Margins:** Stable at **73.6%**, with a target to reach the mid-70% range by year-end.

* **Shareholder Returns:** NVIDIA has returned **$37 billion** to shareholders in the first nine months of fiscal 2026 through buybacks and dividends.

* **Q4 Guidance:** Revenue for the final quarter is projected to reach **$65 billion**.

Emerging Verticals and Competition

Beyond traditional data centers, NVIDIA is aggressively expanding into Physical AI and Robotics. The **GR00T project** for humanoid robots and the **BioNeMo platform** for drug discovery are positioned as the next trillion-dollar opportunities. Automotive revenue has also seen a significant uptick, rising **32%** to **$592 million** as autonomous driving platforms enter full production.

Competition is intensifying as hyperscalers like Google and Amazon develop custom internal silicon to reduce reliance on external vendors. Companies like **Broadcom** are gaining traction in the custom ASIC market, while **AMD** maintains a **7% to 8%** share with its MI350 series.

Supply Chain and Market Risks

The industry faces a paradox of soaring demand and systemic supply risks. Memory revenues are expected to hit **$551.6 billion** in 2026, driven by a "supercycle" in High-Bandwidth Memory (HBM). However, persistent supply-demand imbalances are projected to trigger price spikes of up to **50%** by mid-2026, potentially impacting the production timelines of next-generation AI factories.