European Oil and Gas Index Reaches Record High Above 2007 Peak

**EUROPEAN ENERGY BRIEF**

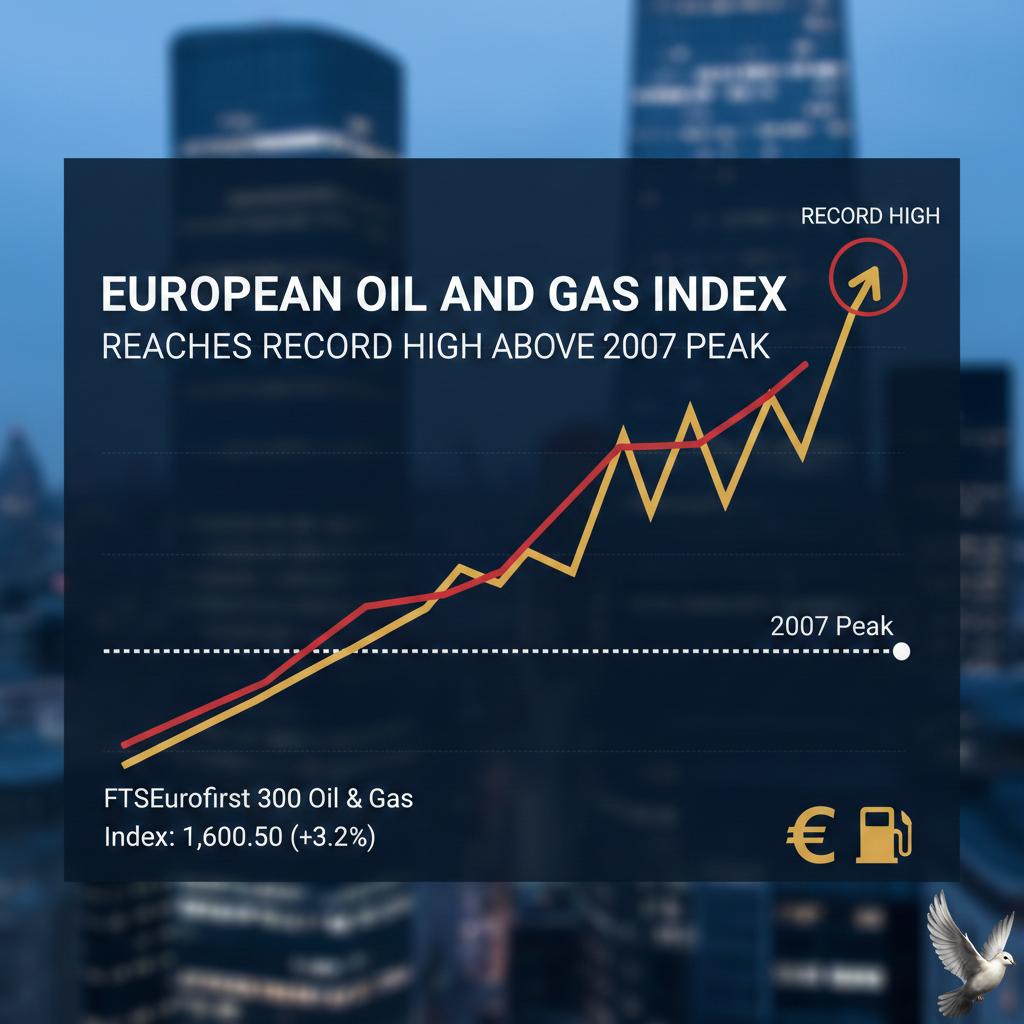

European oil and gas equities have reached a historic milestone. The STOXX Europe 600 Oil & Gas index recently hit a record high of **470.16**, officially eclipsing its previous peak set nearly two decades ago in 2007.

**MARKET PERFORMANCE**

The sector has shown remarkable strength with a **28.8%** increase over the past year. Short-term momentum remains aggressive, with the index gaining more than **12.4%** in the last month alone. Major players like Shell and BP continue to dominate the index weight, contributing to a total five-year return of approximately **89.6%**.

**OIL PRICE DYNAMICS**

This rally is closely tied to volatile crude markets. Brent crude is currently trading around **$71.28** per barrel, while West Texas Intermediate (WTI) holds at **$65.72**. Despite a slight daily softening of **0.6%**, prices remain elevated compared to late-2025 levels due to persistent geopolitical friction in the Middle East.

**SUPPLY AND DEMAND OUTLOOK**

Market analysts are watching a complex supply-demand tug-of-war. Global oil production is forecast to rise by **2.4 million** barrels per day in 2026, reaching a total of **108.6 million** barrels. However, demand growth is slowing to roughly **850,000** barrels per day as major economies transition toward electrification.

**NATURAL GAS STABILITY**

In the natural gas sector, European storage levels remain healthy at approximately **83%**. This buffer has helped stabilize TTF gas prices, which are expected to average **€30/MWh** through 2026. While household gas prices saw sharp year-on-year increases in 13 EU countries, industrial supply is beginning to ease as new LNG capacity from North America and Qatar enters the market.

**STRATEGIC RESERVES**

Emergency oil stocks in the EU currently sit at **108.6 million** tonnes. While this is an increase of **7.3%** from the 2022 lows, commercial stocks have tightened to **45.7 million** tonnes as of mid-2025. This lean inventory environment continues to provide a price floor for energy stocks despite broader economic uncertainties.

**FUTURE PROJECTIONS**

Investors are balancing record-breaking stock performance against a projected supply surplus for late 2026. While the "risk premium" from current geopolitical tensions keeps prices high today, financial institutions anticipate a gradual decline in Brent prices toward the **$50–$60** range by year-end as global inventories build by an average of **3.1 million** barrels per day.