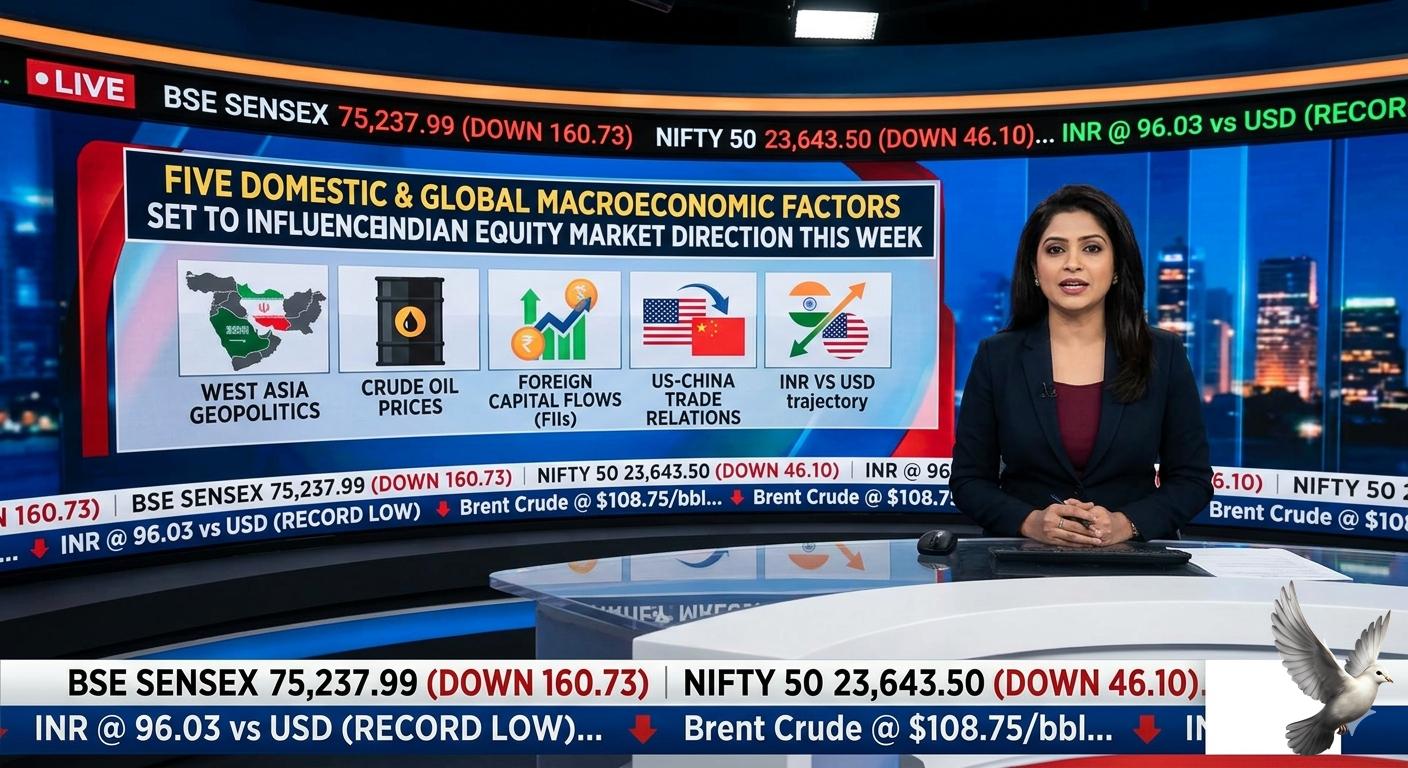

Five Domestic and Global Macroeconomic Factors Set to Influence Indian Equity Market Direction This Week

Indian equity benchmarks concluded a volatile trading week with notable losses, reversing prior recovery attempts as major global and domestic macroeconomic pressures converged. Over the course of the week, the BSE Sensex fell by approximately **2,000 points**, while the NSE Nifty 50 recorded a weekly drop of roughly **2%**.

On the final trading session of the week, early gains driven by a selective rally in information technology and pharmaceutical stocks were entirely erased by late-afternoon selling in financial and metal counters. The Nifty 50 slipped **46.10 points**, or **0.19%**, to settle at **23,643.50**, while the BSE Sensex declined by **160.73 points**, or **0.21%**, to close at **75,237.99**.

A primary trigger forcing defensive positioning across Dalal Street is the ongoing depreciation of the local currency. The Indian rupee fell to a fresh historic low, weakening past the psychological threshold to touch **96.03** against the US dollar. Currency depreciation continues to amplify fiscal concerns regarding imported cost inflation, directly impacting corporate margins.

The pressure on the local currency is closely linked to escalating global energy costs. Driven by direct supply risk anxieties surrounding the US-Iran geopolitical friction and the ongoing closure of the Strait of Hormuz, global oil benchmarks surged by approximately **5%** over the week. Brent crude futures jumped past **$107 per barrel**, while closing the week trading towards **$109 per barrel**.

This steep energy appreciation prompted state-run oil marketing companies to implement a fresh fuel price hike, raising both petrol and diesel prices by **₹3 per litre** nationwide. The sudden tariff revision, the first major fuel price increase in nearly four years, has immediately revived broader consumer inflation concerns across domestic retail and logistics ecosystems.

Market sentiment is expected to remain guarded and highly reactive to headline updates moving into the upcoming sessions. Trading direction will be heavily dictated by five primary factors: developments in the West Asia conflict, international crude pricing structures, foreign institutional capital flows, international trade discussions between the United States and China, and the trajectory of the rupee against a strengthening US dollar.