HDFC Bank Share Price: Closing Analysis

Market Brief: Global Financial Landscape

**Friday, February 27, 2026**

Global equity markets are navigating a period of heightened volatility as the final trading session of February closes. Investor sentiment is currently caught between resilient corporate earnings and significant geopolitical uncertainty. High-growth sectors, particularly those tied to emerging technologies, have faced sharp corrections, while traditional defensive sectors show relative stability.

North American Indices

Wall Street experienced a split performance in its most recent sessions. The **S&P 500** declined **0.54%** to settle at **6,908.86**, while the tech-heavy **Nasdaq Composite** saw a more pronounced drop of **1.18%**, closing at **22,878.38**. This downward pressure was largely driven by a major sell-off in the semiconductor space; despite beating revenue estimates, industry leader Nvidia fell over **5%**, marking its worst day since early 2025.

In contrast, the **Dow Jones Industrial Average** managed a marginal gain of **0.03%**, closing at **49,499.20**. Investors are increasingly rotating capital toward cyclical industries, with financials and industrials outperforming as the broader tech rally cools. The yield on the **10-year Treasury** note eased slightly to **4.03%**, reflecting a cautious move toward safer assets.

Asia-Pacific and Emerging Markets

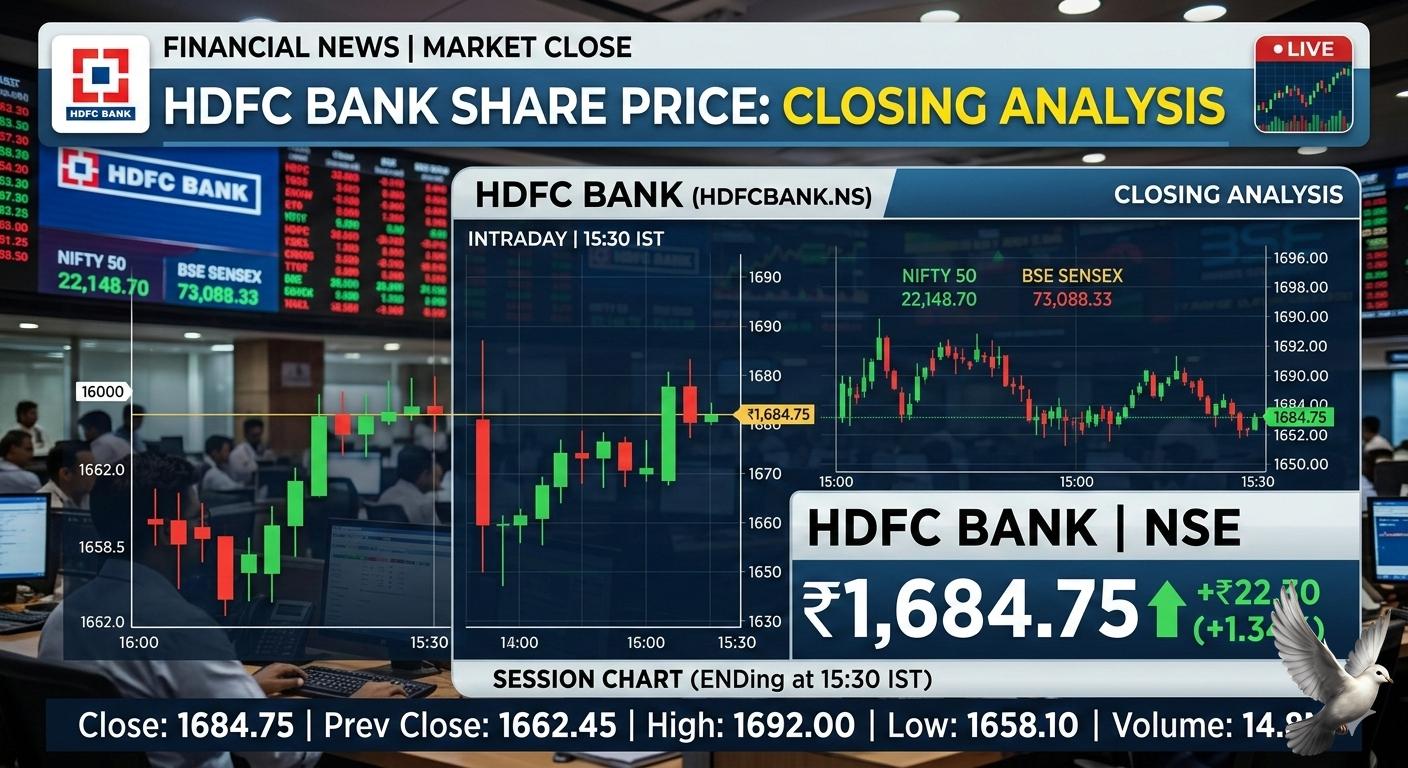

Indian markets witnessed a sharp downturn today. The **BSE Sensex** plummeted **961 points** (down **1.17%**), while the **NSE Nifty 50** dropped **311 points** to close below the **25,200** mark. This correction comes despite the government revising its **GDP growth forecast** for the current fiscal year to **7.6%**, following a rebasing of the economic framework to better capture digital economy gains.

Across the region, the **Nikkei 225** slid **0.6%**, and South Korea’s **Kospi** declined **1.1%**. Market participants are closely monitoring U.S.-Iran nuclear negotiations in Geneva, as any diplomatic breakthrough or breakdown directly impacts regional risk appetite and energy costs.

Commodities and Energy

Crude oil prices remain sensitive to the stalling of diplomatic talks in the Middle East. **Brent crude** is trading near **$71.19 per barrel**, while U.S. **West Texas Intermediate (WTI)** rose to **$65.62**. While geopolitical tensions provide a floor for prices, gains are capped by expectations that **OPEC+** may resume production increases in April, potentially adding **137,000 barrels per day** to global supply.

Gold continues to serve as a primary hedge against uncertainty. Spot gold prices remained steady near **$5,168 per ounce**, holding significant gains after recently breaching the psychological **$5,000** threshold.

Monetary Policy Outlook

Central banks are largely adopting a "wait and watch" stance. The **Reserve Bank of India** recently maintained its repo rate at **5.25%**, signaling a neutral stance as it monitors the impact of previous cuts. Globally, the focus remains on the **U.S. Federal Reserve**, with upcoming Producer Price Index (**PPI**) data expected to influence the trajectory of interest rate decisions for the second quarter of 2026.