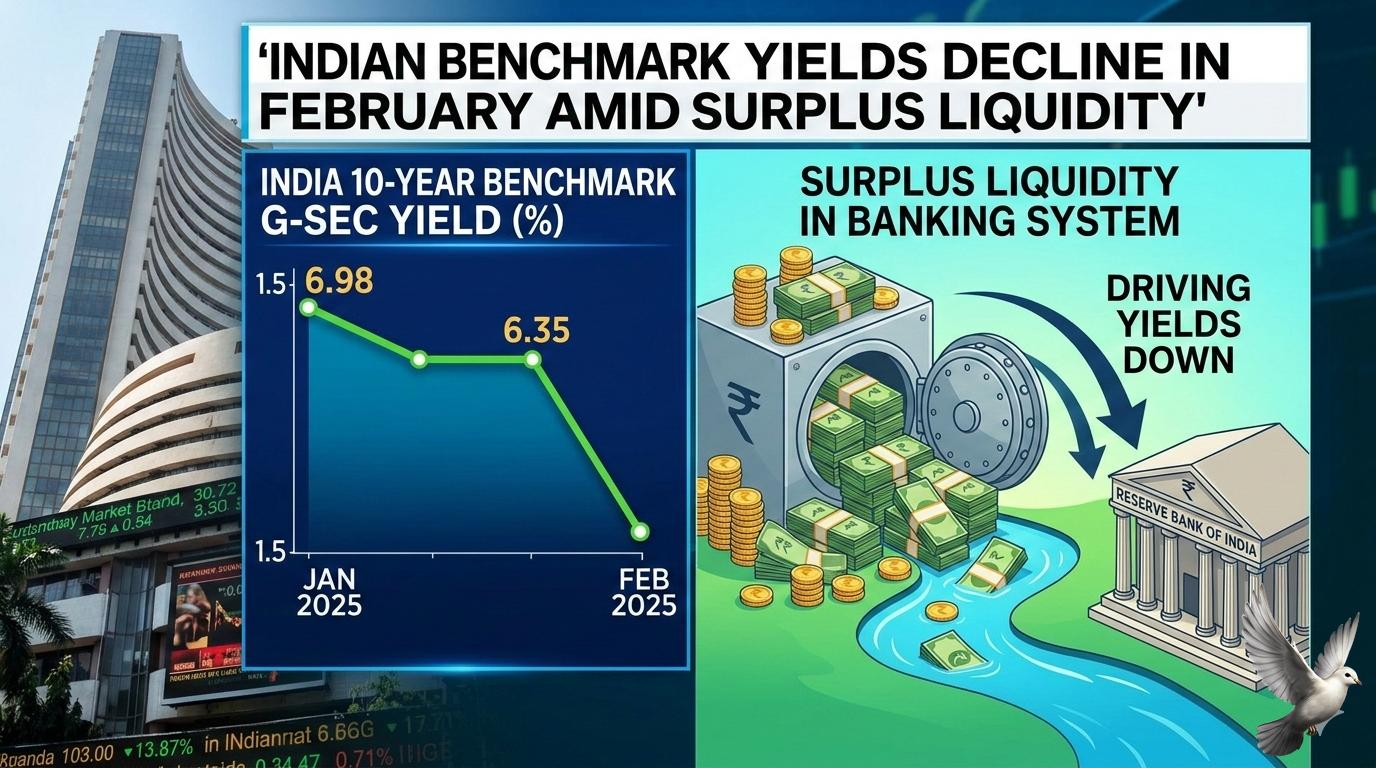

Indian Benchmark Yields Decline in February Amid Surplus Liquidity

The Indian government bond market is navigating a complex period of shifting yields and liquidity adjustments as of late February 2026. While benchmark rates have shown signs of softening, the broader market is reacting to heavy supply pressures and a cautious central bank stance.

The 10-year benchmark bond yield is currently hovering around the 6.68% to 6.70% range. This follows a volatile month where yields initially spiked to 6.73% after the Reserve Bank of India (RBI) maintained a neutral policy stance. Recent auctions have seen stronger demand, particularly for state government debt, helping to pull the benchmark down from its monthly highs.

Banking system liquidity has emerged as a critical support pillar. The RBI has been exceptionally active, purchasing approximately 47% of the government's total bond issuances so far in the current fiscal year. These Open Market Operations (OMOs) have injected over 6.39 trillion rupees into the system, maintaining a surplus of nearly 3 trillion rupees and preventing a sharper rise in borrowing costs.

Despite this surplus, the yield curve is steepening. This is driven by a divergence between short-term rates, which are stabilizing due to high liquidity, and long-term yields, which face pressure from upcoming supply. The government has announced a record gross borrowing target of 17.2 trillion rupees for the next fiscal year (FY27), a figure that exceeded many market projections and continues to weigh on investor sentiment.

The RBI's Monetary Policy Committee recently held the repo rate steady at 5.25%. While inflation remains within the comfort zone at approximately 4%, the central bank’s decision to maintain a "prolonged pause" has dampened hopes for immediate rate cuts. This has shifted investor focus toward short-term instruments, while ultra-long bonds—specifically 30-year and 40-year papers—continue to see sustained interest from insurance and pension funds.

Credit-to-deposit dynamics remain a structural challenge for the banking sector. With credit growth at 14.6% outpacing deposit growth at 12.5%, many banks are seeing their liquidity coverage ratios shrink. This has forced increased reliance on certificates of deposit (CDs), which have seen their rates climb above 7.30%, reflecting persistent funding competition despite the overall system surplus.

Market participants expect the 10-year benchmark to remain within a range of 6.65% to 6.80% in the near term. The primary focus remains on how the market will absorb the final auctions of the current fiscal year and the transition into the heavy borrowing schedule of April.