Indian Stock Market Declines as Rising US-Iran Tensions Lift Oil Prices

Market Brief: India’s Response to Rising Geopolitical Stress

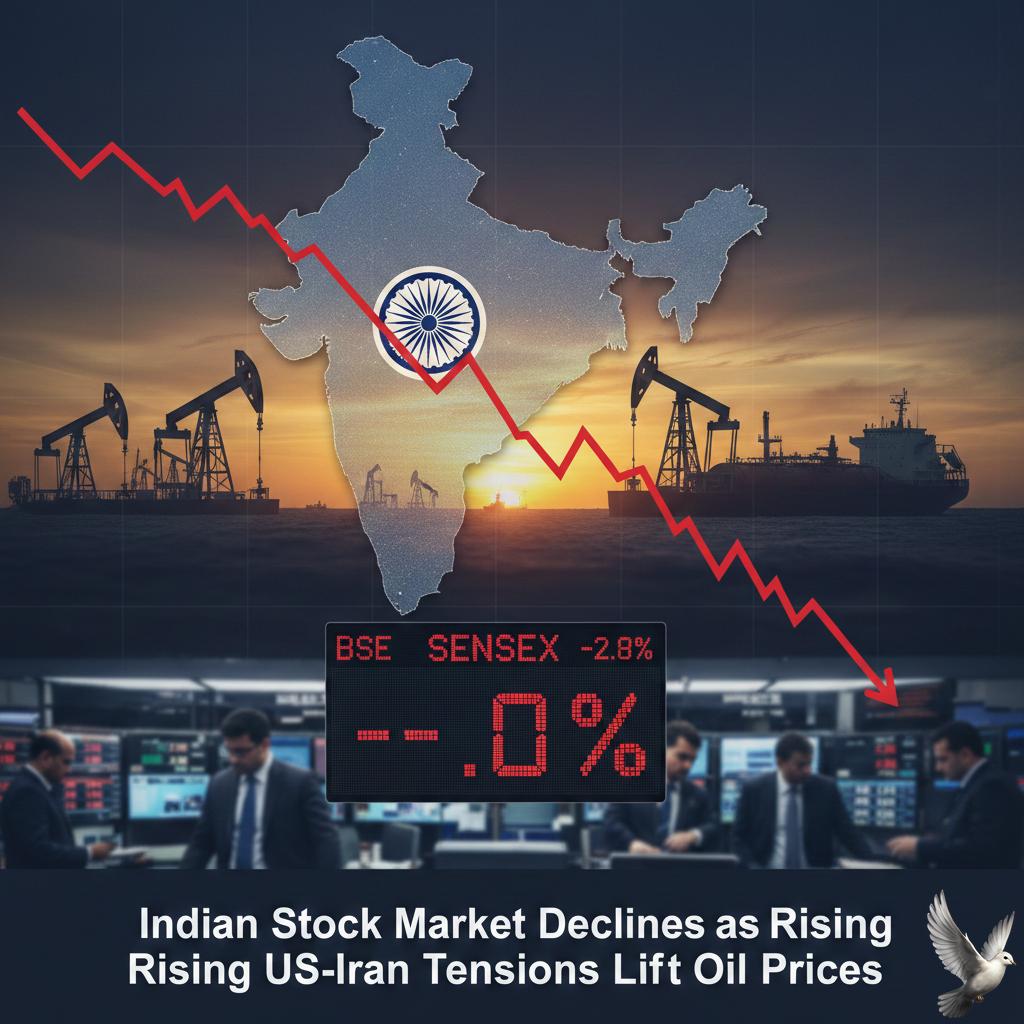

Indian equity markets faced a wave of heavy selling as the week drew to a close. The benchmark **BSE Sensex plummeted 1,236 points**, representing a **1.48% decline**, to settle at **82,498.14**.

Simultaneously, the **NSE Nifty 50** shed **1.41%**, sliding below the psychological support level of 25,500 to end the session at **25,454.35**.

The downturn was triggered by a sudden escalation in military rhetoric between the United States and Iran. Market nerves were rattled by reports of a possible military strike and the deployment of aircraft carriers to the Persian Gulf.

Energy and Commodity Pressure

The geopolitical standoff had an immediate impact on the energy sector. **Brent crude oil** futures climbed nearly **2%**, trading at **$71.66 per barrel**. This marks its highest level in six months.

US West Texas Intermediate (WTI) followed suit, settling at **$66.43**. Analysts warn that a total disruption of Iranian exports or any interference with the **Strait of Hormuz**—where **20% of global oil** passes—could push prices toward **$100**.

As a major net importer of oil, India is particularly sensitive to these shifts. Higher crude prices translate directly into concerns over widening trade deficits and increased domestic inflation.

Currency and Volatility

The **Indian Rupee (INR)** faced downward pressure as the US Dollar strengthened on safe-haven demand. The exchange rate moved toward **91.04 against the USD**, reflecting the broader exit from emerging market assets.

Market volatility spiked significantly during the session. The **India VIX surged over 10%** to reach **13.46**, indicating heightened investor anxiety and expectations of further short-term turbulence.

Nearly every sector ended the day in the red. Banking, metal, and auto stocks were among the hardest hit, with the **Nifty Bank** index dropping **1.32%** to close at **60,739.55**.

Outlook and Investor Sentiment

Despite the sharp one-day crash, some resilience was noted earlier in the week due to consistent domestic institutional inflows. However, the current environment is dominated by a "sell-on-rallies" sentiment.

Investors are now closely monitoring the **10-day deadline** mentioned by US leadership regarding nuclear negotiations. Further escalation in the Middle East is expected to keep the **war premium** on oil high, maintaining pressure on Indian fiscal stability and corporate margins.