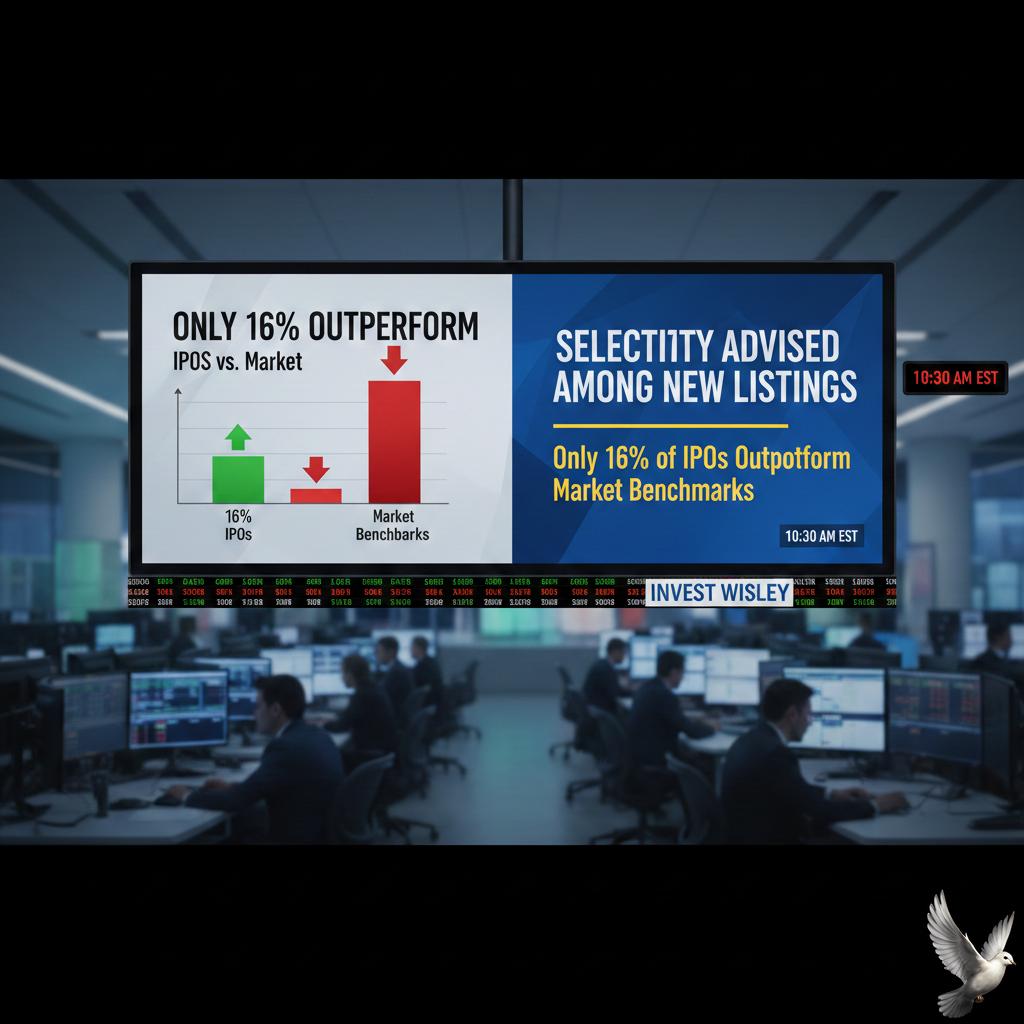

Only 16% of IPOs Outperform Market Benchmarks; Selectivity Advised Among New Listings

The Indian primary market is navigating a pivotal phase in early 2026. After a historic 2025 where 102 companies raised a record **₹1.75 lakh crore**, the momentum has transitioned into a massive but cautious pipeline. Currently, over 190 companies are in the queue, seeking to raise more than **₹2.5 lakh crore**. Despite this volume, the actual launch activity in January and February has been muted as issuers wait for secondary market stability.

While the "IPO boom" headline remains attractive, long-term wealth creation data suggests a starkly different reality. Recent analysis reveals that only **16%** of IPOs have managed to outperform the broader market returns over the long term. Furthermore, approximately **50%** of the small-cap universe is currently trading nearly **40%** below their all-time highs. This underscores a significant gap between listing-day euphoria and sustainable shareholder value.

Institutional dynamics are providing a unique floor to the current market. Foreign Institutional Investor (FII) ownership has seen periods of selling, with recent net outflows reaching **₹7,395 crore** on specific volatile days in February. However, Domestic Institutional Investors (DIIs) have acted as a consistent shock absorber, frequently recording net buys exceeding **₹5,500 crore** to stabilize the indices.

Sectoral performance is diverging based on fundamental recovery rather than speculative heat. The IT sector is positioned for a sharp recovery in 2026, with spending in India projected to reach **$176.3 billion**, a **10.6%** increase from the previous year. This growth is largely driven by AI-centric contracts, which now form nearly **74%** of all new deals for major Indian tech firms.

Consumption remains a key theme, though valuations in mid and small-cap segments continue to trigger red flags. The Nifty Smallcap index has faced recent pressure, dropping over **3%** year-to-date, compared to a milder **1.4%** decline in the Nifty 50. This correction is viewed by many as a necessary cooling phase following the multi-year rally that stretched valuation multiples.

For the remainder of 2026, the focus is shifting from "liquidity-driven" to "earnings-driven" listings. Marquee names in fintech, consumer tech, and infrastructure are expected to headline the next wave of offerings. Investors are increasingly prioritizing companies with clear profitability pathways and transparent governance over those relying solely on future growth projections.

Patience remains the primary tool for navigating this landscape. With the Nifty 50 hovering around the **25,700** level and the India VIX declining to **12.67**, the current environment favors a selective approach. Wealth creation is increasingly concentrated in quality issues that can survive the transition from primary market hype to secondary market reality.