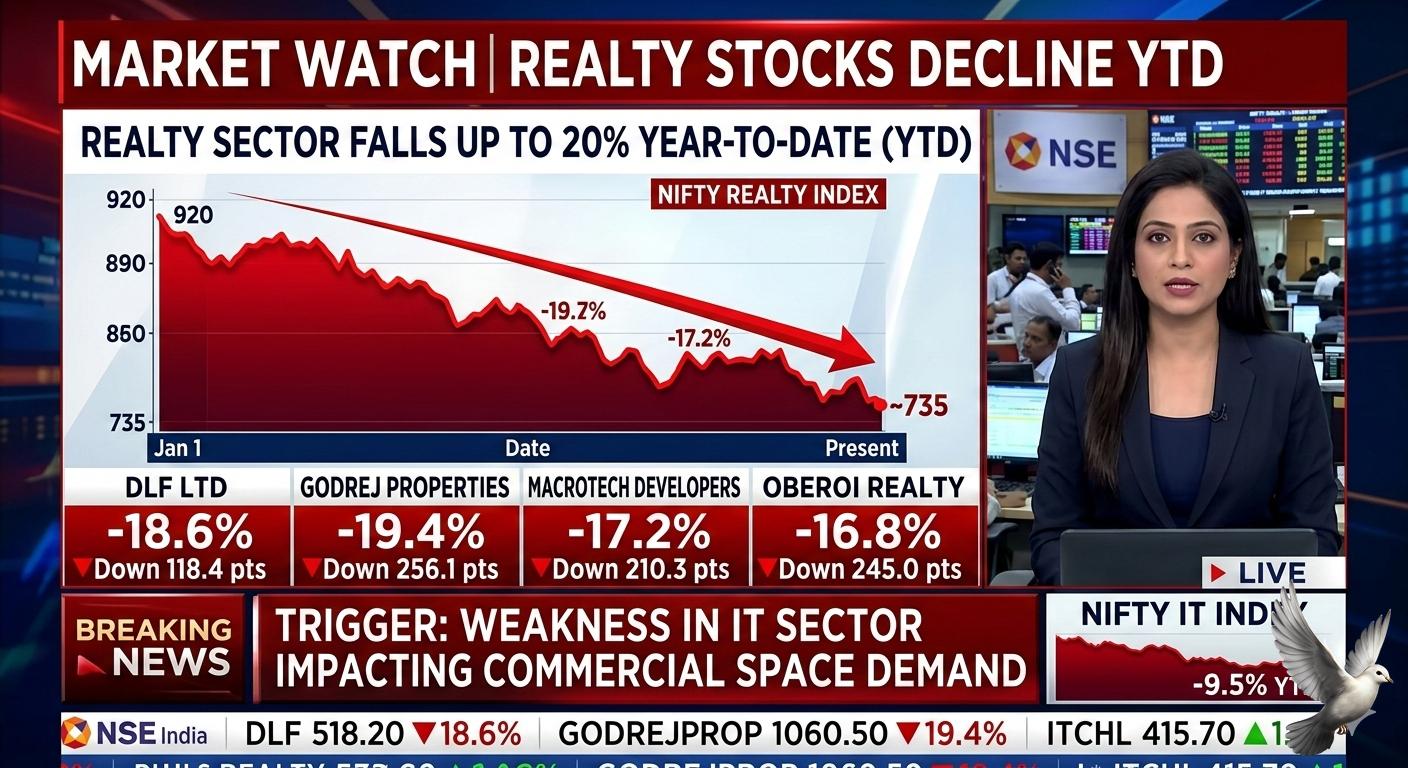

Realty Stocks Decline up to 20% Year-to-Date Amid IT Sector Weakness

Indian real estate stocks have faced a significant correction in early 2026, with the Nifty Realty index dropping nearly 12% year-to-date and falling over 26% from its previous all-time highs. This downturn has pushed the sector into official bear market territory, driven primarily by a "rub-off effect" from global technology volatility and local concerns over artificial intelligence.

Investors are increasingly wary that AI-led disruption could fundamentally alter the employment landscape in India’s software industry. Because residential absorption and Grade A office leasing in hubs like Bengaluru are tied to IT services and Global Capability Centers, the prospect of slower hiring has dampened market sentiment. Sector experts note that if AI-driven efficiency gains translate into workforce reduction, the spillover into housing upgrades and commercial expansion could be substantial.

The impact is most visible among developers with heavy exposure to South Indian tech corridors. Brigade Enterprises has seen the steepest decline, with shares falling more than 20% this year. Other major players including Prestige Estates and Sobha Limited have recorded losses ranging from 1% to 11%. Even national heavyweights like DLF and Godrej Properties have retreated by as much as 12% as the narrative of an IT slowdown gains momentum.

Beyond the tech narrative, the sector is grappling with valuation and operational hurdles. Many real estate stocks saw their prices double over the last 18 months, leading to a phase of profit-booking as valuations outpaced fundamentals. Recent operational data has also added pressure; Oberoi Realty reported a 56% year-on-year decline in pre-sales, while other developers faced inventory shortages and administrative bottlenecks that delayed new project launches.

Despite these headwinds, the broader real estate market shows signs of a K-shaped recovery. While the mid-segment faces caution due to shifting job security, the luxury segment remains resilient. Sales for homes priced above 4 crore rose nearly 28% last year, and institutional investment reached a historic high of 25,375 crore in the third quarter of 2025. This suggests that while stock prices are correcting, physical demand for premium assets and data centers continues to attract significant capital.

Policy shifts are providing a localized floor for the industry. The Reserve Bank of India recently cut the repo rate by 25 basis points to 6.25%, the first reduction since 2020. This move, combined with the Union Budget’s focus on increasing middle-class spending power through tax cuts, is expected to support demand in the affordable and mid-tier housing segments in the long term.

The current market environment is characterized by a transition from a broad-based rally to a period of selective consolidation. Analysts view the AI threat as a near-term overhang that may delay purchase decisions and increase financial caution among buyers. However, the structural drivers of Indian real estate—including rapid urbanization and the consolidation of the market toward organized, large-scale developers—remain intact as the industry adapts to a new technological and economic reality.