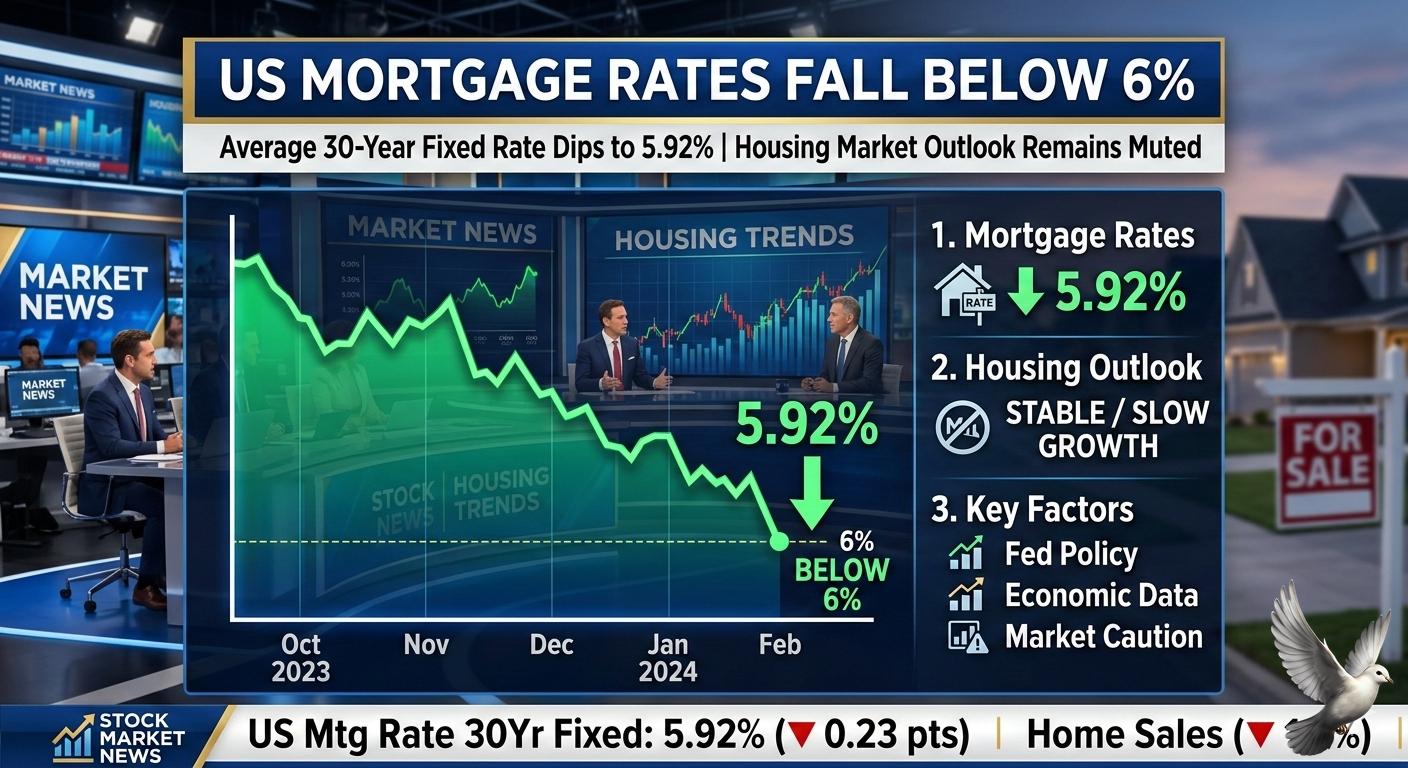

US Mortgage Rates Fall Below 6% Amid Muted Housing Market Outlook

US 30-year fixed mortgage rates have officially dropped below the 6% threshold for the first time in three and a half years. As of February 26, 2026, the benchmark rate averaged 5.98%, a notable decline from 6.01% the previous week and significantly lower than the 6.76% recorded a year ago.

This shift marks the lowest borrowing cost for American homebuyers since September 2022. The 15-year fixed mortgage rate followed a different path, rising slightly to 5.44% this week. These movements are closely tracking the 10-year Treasury yield, which currently sits near 4.00% as investors move toward safer bond assets amid broader market volatility.

Market analysts view the sub-6% rate as a critical psychological milestone. While the dip provides a boost to purchasing power, the housing market remains in a state of transition. Recent data shows existing home sales dropped 8.4% in January, reaching an annualized pace of under 4 million units—the slowest in over two years.

Supply constraints continue to dominate the narrative. Total housing inventory sits at approximately 1.22 million units, and while this is an improvement over 2025, it remains below pre-pandemic norms. The median sales price for existing homes is currently $396,800, reflecting a 1.1% year-over-year increase despite the high-rate environment of the past year.

Affordability remains a challenge for many, as nearly 69% of existing homeowners hold mortgages with rates at or below 5%. This "lock-in effect" disincentivizes selling, keeping supply tight. However, experts anticipate that if rates remain under 6%, the upcoming spring season could see a significant increase in both listings and buyer activity.

Refinancing activity is already responding to the rate drop. Mortgage applications for refinancing have surged, with some indices showing a 130% increase compared to the same period last year. For a standard $400,000 home with a 20% down payment, the current rate environment translates to roughly $2,268 in annual savings compared to 2025 figures.

The Federal Reserve is scheduled to meet in mid-March to discuss further interest rate policy. Current market sentiment suggests that while volatility persists, the combination of cooling inflation and government initiatives, such as the recent $200 billion mortgage-backed securities purchase order, may help sustain these lower rate levels through the first half of the year.