Neutral News

Collection

Rupee Hits Record Low as RBI Intervention Limits Losses

**Rupee Defends Key Level Ahead of Budget** **Friday Market Recap** The Indian rupee witnessed intense volatility in Friday's session, testing a historic low of **92.00** against the US dollar during intraday trade. Despite persistent downward pressure from foreign capital outflows and month-end importer demand, the currency managed to close slightly stronger at **91.9550**. **RBI's Strategic Defense** The Reserve Bank of India (RBI) executed a timely intervention to protect the psychological **92-mark**. * **Dollar Sales:** State-run banks, likely acting on behalf of the central bank, sold dollars aggressively in both spot and non-deliverable forward markets. * **Liquidity Management:** The RBI utilized foreign exchange swaps to manage liquidity, ensuring the currency didn't spiral before the critical Union Budget presentation on **February 1**. **Key Figures & Trends** * **All-Time Low:** The unit briefly touched **92.00** before pulling back. * **Foreign Outflows:** Foreign investors have net sold approximately **$4 billion** in Indian equities this January, weighing heavily on the local unit. * **Reserves Buffer:** India’s forex reserves remain robust, standing at **$709.4 billion** as of January 23, providing ample firepower for further defense. **Market Sentiment** Traders remain cautious as the market prepares for the Union Budget tomorrow. While the **92** level has held for now, the near-term outlook depends on the government's fiscal consolidation path and global dollar dynamics. The pressure remains biased to the downside until foreign inflows stabilize. **Next Watch:** The Union Budget announcement on Sunday, Feb 1, will likely dictate Monday's opening momentum.

U.S. Stocks Face Earnings Wave and Jobs Data Following Tech Pullback

**Global Market Brief: Tech Volatility & Macro Signals** **Overview** Investors are bracing for a decisive week as market sentiment shifts from optimism to caution. Following a turbulent reaction to Microsoft’s latest figures, the spotlight turns to upcoming reports from Alphabet and Amazon. These releases, combined with critical US labor data, will likely dictate near-term market direction. **Tech Sector: The AI Reality Check** The earnings season has taken a dramatic turn. **Microsoft** reported a strong fiscal Q2 with revenue hitting **$81.3 billion** (up **17%**) and EPS of **$5.16**, comfortably beating Wall Street estimates. However, markets reacted negatively to the company's ballooning capital expenditure on artificial intelligence. Concerns over the timeline for AI monetization triggered a sharp sell-off, with Microsoft shares plunging **11%**—their steepest single-day decline since 2020. This "sell-the-news" reaction has raised the stakes for **Amazon** and **Alphabet**, which are scheduled to report in the coming days (Amazon confirmed for **February 5**). Investors are no longer satisfied with growth alone; they are demanding clear evidence that massive AI infrastructure spending is yielding profitable returns. **Federal Reserve: Holding Steady** On the macro front, the Federal Reserve maintained its cautious stance at the January meeting, keeping the benchmark interest rate unchanged at **3.50%–3.75%**. While the decision was widely expected, the Fed’s commentary emphasized that the economic outlook remains uncertain. Policymakers cited solid growth but noted that inflation, while cooling, is not yet fully vanquished. This "hold" reinforces the "higher-for-longer" narrative, dampening hopes for aggressive rate cuts in the immediate future. **Labor Market Focus** Attention now shifts to the **February 6** US Non-Farm Payrolls report. The December data showed a cooling labor market with only **50,000** jobs added, missing the **60,000** forecast. A similar lukewarm reading in the upcoming report could reignite recession fears, while a surprisingly hot number might complicate the Fed’s inflation fight. The unemployment rate—currently stabilizing around **4.4%**—will be a key metric to watch for signs of broader economic stress. **Investor Sentiment** The mood has clearly soured on "growth at any cost." The divergence between strong corporate earnings and weak stock performance suggests valuations are under strict scrutiny. With the Fed pausing and AI ROI under the microscope, volatility is expected to remain elevated throughout the week.

US Stocks Decline Amid Concerns Over Fed Nominee, Earnings, and Inflation

**Market Brief: Wall Street Slides on Fed Nomination & Inflation Angst** **Indices Recap (Friday Close)** * **Dow Jones:** 48,886.44 (▼ 0.38%) * **S&P 500:** 6,939.03 (▼ 0.43%) * **Nasdaq:** 23,461.82 (▼ 0.94%) **Executive Summary** U.S. equities finished the week in the red as traders processed President Trump’s nomination of **Kevin Warsh** to replace Jerome Powell as Federal Reserve Chair. The announcement, coupled with hotter-than-expected inflation data and renewed government shutdown fears, triggered a broad risk-off session. **The Warsh Effect** Markets initially reacted negatively to the Warsh nomination, interpreting the choice as potentially "hawkish." While Warsh is a former Fed Governor with deep institutional knowledge, investors are grappling with uncertainty regarding his stance on interest rates and central bank independence. This anxiety overshadowed the broader expectation that a Trump nominee might favor easier monetary policy. **Inflation & Shutdown Jitters** Sentiment was further dampened by the December **Producer Price Index (PPI)**, which rose **0.5%**—surpassing economist forecasts of 0.3%. The data reignited concerns that inflation remains sticky, potentially complicating the Fed's rate-cut path. Simultaneously, stalled negotiations in the Senate raised the specter of a partial government shutdown, adding another layer of volatility. **Sector & Asset Moves** * **Commodities Crash:** Gold and silver faced historic sell-offs. Silver plummeted over **13%** in intraday trading, while gold dropped nearly **5%**, as the dollar strengthened and yields ticked higher. * **Tech Mixed:** The Nasdaq led declines, weighed down by weakness in growth stocks. **Microsoft** continued its slide following earnings disappointment earlier in the week, while **Apple** managed a modest rebound on favorable quarterly results. * **Treasuries:** The 10-year Treasury yield edged up to **4.25%**, reflecting the dual pressures of sticky inflation and shifting Fed expectations. **Outlook** Investors enter the weekend with heightened caution. The focus now shifts to the Senate confirmation process for Warsh and upcoming economic reports that will clarify whether the recent inflation uptick is a trend or an anomaly.

Tata Consumer Share Price and Trading Volume Updates

**GLOBAL & INDIA MARKET SNAPSHOT — JANUARY 30, 2026** **🇮🇳 India Market Action** Domestic indices showed resilience on Thursday, closing in the green for the third straight session. The **Sensex** climbed **222 points** (+0.27%) to settle at **82,566**, while the **Nifty 50** gained **76 points** (+0.30%) to end at **25,418**. Sentiment was buoyed by the **Economic Survey 2025-26**, which projects a robust GDP growth of **6.8–7.2%** for the upcoming fiscal year. However, signals for today are cautious. **GIFT Nifty** futures traded **55 points** lower early Friday, suggesting a negative opening. Investors remain watchful ahead of the upcoming Union Budget and amid sustained foreign fund outflows. **🇺🇸 US & Global Trends** Wall Street ended mixed overnight as major tech earnings drove volatility. The **Dow Jones** edged up **0.11%** to **49,071**, while the **S&P 500** slipped **0.13%**. The tech-heavy **Nasdaq** dropped **0.72%** to **23,685**, dragged down by a **10%** plunge in Microsoft shares over cloud growth concerns. Conversely, Meta surged **10%** on strong results. The Federal Reserve held interest rates steady at **3.50%–3.75%**, maintaining a "higher-for-longer" stance that continues to weigh on risk assets. **🛢️ Commodities & Currency** * **Gold:** Prices are seeing a historic run, trading near **$5,600** per ounce globally. In India, gold futures have touched fresh record highs, driven by safe-haven demand amid US-Iran tensions. * **Oil:** Brent Crude ticked up to trade around **$68–$70** per barrel following geopolitical warnings. * **Rupee:** The Indian currency remains under pressure, closing at a record low of **91.99** against the dollar due to global strengthening of the greenback. **🪙 Crypto Struggle** Digital assets faced a sharp sell-off. **Bitcoin** tumbled over **5%** to slump around **$84,400**, reaching its lowest levels since December. The drop correlates with the broader tech weakness and lack of immediate rate cut signals from the Fed. **Focus for Today:** Watch for volatility in Indian IT stocks following the Nasdaq's dip and reactiveness to the pre-Budget mood.

China Reportedly Relaxes Property Sector Rules

**MARKET BRIEF: CHINA REAL ESTATE SECTOR POLICY SHIFT** **January 30, 2026** **Executive Summary: End of the "Three Red Lines" Era** In a significant policy pivot reported on January 29, 2026, Chinese regulators have effectively dismantled the controversial "three red lines" deleveraging framework. Local media confirm that property developers are no longer required to report monthly compliance data, signalling the official end of the stringent borrowing caps introduced in 2020. This deregulation marks a decisive shift from the austerity measures that triggered a liquidity crunch and precipitated one of the most severe debt crises in the sector's history. The move appears aimed at stabilizing a market that continues to weigh heavily on the broader Chinese economy. **Immediate Market Reaction: Developer Stocks Surge** Equity markets responded explosively to the news. Investors, interpreting the policy relaxation as a potential lifeline for surviving developers, drove major property stocks significantly higher in Thursday's trading session: * **Logan Group** soared by as much as **40%**. * **China Aoyuan** jumped over **34%**. * **Sunac China Holdings** rallied approximately **29%**. * **Country Garden Holdings** climbed **16%**. Broader sector indices also reflected this renewed optimism. The **CSI 300 Real Estate Index** advanced **5%**, reaching a two-month high, while the **Hang Seng Mainland Properties Index** gained **4.8%**. This rally stands in stark contrast to the broader market, which remained largely flat. **Context: The Legacy of the "Three Red Lines"** Implemented in August 2020, the "three red lines" policy was designed to curb reckless borrowing by imposing strict limits on three financial ratios: 1. Liability-to-asset ratio (excluding advance receipts) of less than **70%**. 2. Net gearing ratio of less than **100%**. 3. Cash-to-short-term debt ratio of more than **1x**. While intended to reduce systemic risk, the abrupt cutoff in financing backfired, leading to a massive liquidity squeeze. Since mid-2021, the sector has seen approximately **$130 billion** in offshore debt defaults. Industry giants like **China Evergrande** have entered liquidation, while others, such as **Vanke**, have narrowly avoided default as recently as January 2026 through last-minute bond extensions and state-backed support. **Current Market Fundamentals & 2026 Outlook** Despite the positive sentiment in equity markets, physical market fundamentals remain challenged. The removal of reporting requirements acknowledges a new reality: the era of debt-fuelled expansion is over, and aggressive deleveraging has already forced the market's most leveraged players into restructuring or insolvency. * **Price Trends:** New home prices across **70 major cities** extended declines in December 2025, underscoring persistent weak demand. * **Sales Volume:** Analysts forecast a further contraction in 2026, with primary property sales volumes expected to drop by approximately **6%**. * **Inventory:** High inventory levels in lower-tier cities continue to suppress pricing power. **Market Analysis** Industry experts suggest that while the policy shift is symbolic, it may not immediately solve the sector's funding challenges. Financial institutions remain risk-averse, and consumer confidence is still recovering from years of unfinished projects and falling asset values. The focus has now shifted from regulatory compliance to survival and "high-quality development," with state-owned enterprises increasingly dominating the landscape as private developers retreat. This policy relaxation serves as a critical signal that Beijing is prioritizing market stabilization over deleveraging for the remainder of 2026.

Bitcoin Holds Near $88,000 Amid Fed Pause and Weak ETF Flows

**Market Brief: Bitcoin Slips as Fed Holds Steady** **January 29, 2026** **Macro Backdrop & Fed Decision** The Federal Reserve maintained interest rates at **3.5% – 3.75%** yesterday, opting for stability over easing. While widely expected, the decision dampened risk appetite, triggering a "sell-the-news" reaction across digital assets. Market sentiment is further strained by capital rotating into traditional safe havens, with gold prices surging to record highs above **$5,000/oz** and diverting liquidity away from crypto markets. **Bitcoin & Market Performance** Bitcoin continues to struggle below key resistance, currently trading near **$88,000**. The asset dipped approximately **1.1%** in the last 24 hours, testing support levels around **$87,800**. Failure to reclaim the **$90,000** threshold has reinforced bearish short-term technicals. Ethereum faced steeper selling pressure, dropping roughly **2.8%** to trade around **$2,920**. The decline pushed ETH back below the psychological **$3,000** mark, validating a bearish breakdown from its recent consolidation pattern. The broader cryptocurrency market capitalization contracted by **1.68%** to **$2.98 trillion**, shedding billions in valuation as altcoins mirrored the weakness in majors. **Institutional Flows & Sentiment** Institutional demand has cooled significantly. After brief inflows earlier in the week, U.S. spot Bitcoin ETFs registered net outflows exceeding **$100 million** on Tuesday. This reversal highlights growing caution among traditional investors who are closely monitoring the Federal Reserve's "wait-and-see" stance on future rate cuts. **Key Levels to Watch** * **Bitcoin:** Immediate support sits at **$87,000**, with major resistance remaining firm at **$90,000**. * **Ethereum:** Needs to reclaim **$3,065** to invalidate the current bearish trend; downside targets loom near **$2,250** if selling persists. *** *Data as of January 29, 2026.*

Vedanta Q3 Net Profit Rises 60% to Rs 5,710 Crore, Revenue Up 37%

**Global Markets Brief: Thursday, January 29, 2026** **Market Pulse** Global equities are navigating a volatile mix of geopolitical tension and shifting monetary policy. US markets remain cautious following the Federal Reserve’s decision to hold interest rates steady at **3.50%–3.75%**, while Indian indices rallied on the back of a landmark trade agreement. **US & Global Indices** * **US Markets:** Sentiment is mixed as the Dollar Index (DXY) slumped to a four-year low of **96.1**, driven by President Trump’s criticism of Fed independence and rising fiscal concerns. * **India:** The Sensex gained **0.28%** to trade near **82,574**, while the Nifty 50 held above **25,417**. Optimism is fueled by the new **India-EU Free Trade Agreement** and the release of the Economic Survey 2025-26, despite cautiousness ahead of the Union Budget. * **Europe:** Markets are digesting the India-EU pact, with sectors like textiles and marine products expected to benefit from zero-duty access. **Commodities Surge** * **Gold:** Prices have shattered records, trading around **$5,565** per ounce. The rally is driven by a weaker dollar, central bank buying, and safe-haven demand amidst US-Iran tensions. * **Silver:** The metal continues its massive run, trading near **$118**, significantly outperforming gold in percentage gains this month. * **Crude Oil:** WTI crude climbed above **$64** per barrel. Prices are reacting to US warnings of potential military action involving Iran, raising fears of supply disruptions in the Strait of Hormuz. * **Copper:** Supply constraints are in focus after the Economic Survey warned that rising AI data center demand could trigger a severe global shortage. **Crypto Update** * **Bitcoin:** Consolidating around **$88,000**, struggling to break the **$90k** resistance level as investors await clearer cues from the Fed. * **Ethereum:** Trading lower at approximately **$2,950**, mirroring the broader consolidation in digital assets. **Key Economic Events** * **Fed Decision:** The US Federal Reserve maintained rates, citing resilient economic activity but persistent inflation risks. Two officials dissented, favoring an immediate cut. * **Economic Survey 2025-26 (India):** Highlights include a warning on "financialization" risks, the impact of AI on energy/metal demand, and a forecast of **6.5–7%** GDP growth. The survey notes the Rupee’s fall to a lifetime low of **92.00** against the dollar is largely due to global headwinds. **Corporate Highlights** * **Adani Power:** Reported a **19%** drop in Q3 profit to **₹2,480 crore**. * **Canara Bank:** Q3 net profit rose **26%** YoY to **₹5,155 crore**. * **ABB India:** Stock surged over **8%** after announcing a **$2 billion** buyback and strong 2026 outlook.

**Nestle India Shares Maintain Low Beta Value**

**Market Brief: Volatility in India, Records in US** **Global & Domestic Snapshot** Indian equity benchmarks **Sensex** and **Nifty 50** are trading lower today, witnessing profit-booking despite positive global cues. The **Sensex** is hovering around **82,063** (down ~280 points), while the **Nifty** is trading near **25,273** (down ~69 points). In contrast, US markets set new milestones overnight. The **S&P 500** crossed the historic **7,000** mark for the first time, driven by AI optimism and resilient tech earnings. The **Nasdaq Composite** also climbed **0.5%**, supported by strength in semiconductor stocks like **Nvidia**. **Key Market Drivers** * **India-EU Trade Deal:** Optimism surrounds the completion of the India-EU Free Trade Agreement, which recently uplifted sentiment, though immediate profit-taking has curbed gains. * **Federal Reserve Policy:** Investors remain cautious ahead of the US Fed's policy announcement today. Markets widely expect rates to remain unchanged, but the focus is on Chair Jerome Powell’s commentary regarding future easing. * **Geopolitical Tensions:** Crude oil prices have firmed up for a third consecutive day. **Brent Crude** is trading near **$69 per barrel** amid escalating US-Iran tensions, adding a risk premium to energy markets. **Stocks in Focus** * **Larsen & Toubro (L&T):** Shares are reacting to management guidance on order inflows; analysts remain watchful of execution headwinds. * **Maruti Suzuki:** Reported a **4% YoY rise** in Q3 net profit, though the figure slightly missed street estimates. * **Tech Sector:** IT stocks remain in focus following strong guidance from global tech majors and domestic earnings reports. **Commodities & Currency** * **Gold:** Bullion continues its record-breaking run, trading above **$5,500 per ounce** in international markets, driven by safe-haven demand and a weaker dollar. * **Silver:** Prices have surged significantly, tracking gold's momentum. * **Currency:** The US Dollar has stabilized but remains under pressure from recent tariff threats, impacting emerging market currencies. **Summary** While Wall Street celebrates record highs, domestic markets are consolidating gains. Traders are closely monitoring the **Fed’s decision** later today and the unfolding **geopolitical situation** in the Middle East for further direction.

ONGC Maintains Balanced Risk Profile

**MARKET PULSE: Thursday, January 29, 2026** **Global & Domestic Equities** Global markets remain cautious following the **US Federal Reserve's** decision to hold interest rates steady at **3.75%**. In India, benchmark indices tracked global weakness and pre-Budget nervousness. The **Nifty 50** slipped below **25,300**, shedding nearly **69 points**, while the **Sensex** dropped over **280 points** to trade around **82,060**. Banking and IT stocks led the decline, with heavyweights like **Infosys** and **HDFC Bank** facing selling pressure. **Crypto Markets** Bitcoin (**BTC**) is trading firmly in the **$87,500 – $88,000** range, showing resilience despite broader market volatility. The total crypto market cap has seen a slight contraction to **$2.93 trillion**. Traders are eyeing the **$90,000** resistance level, though lowered liquidity and macroeconomic uncertainty are keeping aggressive bulls at bay. **Commodities Surge** Gold is witnessing a historic rally, surging over **2%** to break past **$5,500 per ounce**, driven by safe-haven demand amid geopolitical tensions. Silver followed suit, climbing to **$118**. Conversely, crude oil remains stable but elevated, with **Brent Crude** trading near **$68.45** and **WTI** holding above **$63.70** as supply concerns balance against demand fluctuations. **Key Drivers** * **Union Budget 2026:** Indian investors are firmly focused on the upcoming February 1 budget, causing heightened volatility in domestic sectors. * **Corporate Earnings:** Mixed results from major tech giants like **Microsoft** and **Tesla** are influencing global sentiment. * **Geopolitics:** Escalating tensions and recent warnings regarding Iran have added a risk premium to precious metals and energy markets. **Watchlist** Focus remains on **L&T** (strong order inflows) and **Maruti Suzuki** (earnings reaction), while the **USD/INR** pair stays relatively flat at **84.50**.

Rupee Underperforms Asian Peers Amid NDF Maturities and Month-End Dollar Demand

**Market Brief: Rupee Underperforms Amid Month-End Demand** **Closing Update** The Indian rupee settled marginally weaker on Wednesday, closing at **91.78** against the US dollar, down from the previous session's close of **91.72**. Despite a generally supportive global environment, the domestic currency faced resistance due to specific technical factors and localized demand. **Primary Drivers** The slight depreciation was driven primarily by month-end dollar demand from importers, particularly in the oil and corporate sectors. Market reports also highlighted pressure from maturing non-deliverable forwards (NDF) positions, which kept the rupee from participating in the broader Asian currency rally. **Global & Regional Cues** While the rupee lagged, Asian peers largely appreciated, capitalizing on a softer greenback. The US Dollar Index (DXY) hovered near **96.24**, effectively touching four-year lows earlier in the session. This broad-based dollar weakness, triggered by dovish Federal Reserve expectations and recent comments on currency valuation from US leadership, helped cap significant losses for the rupee. **Domestic Sentiment** Downside risks were further mitigated by positive market sentiment surrounding the newly finalized India-EU Free Trade Agreement. This historic pact provided an underlying floor to the currency, preventing a sharper slide despite the heavy month-end outflows. **Outlook** Traders remain focused on the nearing Federal Reserve policy statement and ongoing geopolitical developments, which continue to influence capital flows in emerging markets. The rupee is expected to trade within a narrow range as immediate month-end pressures subside.

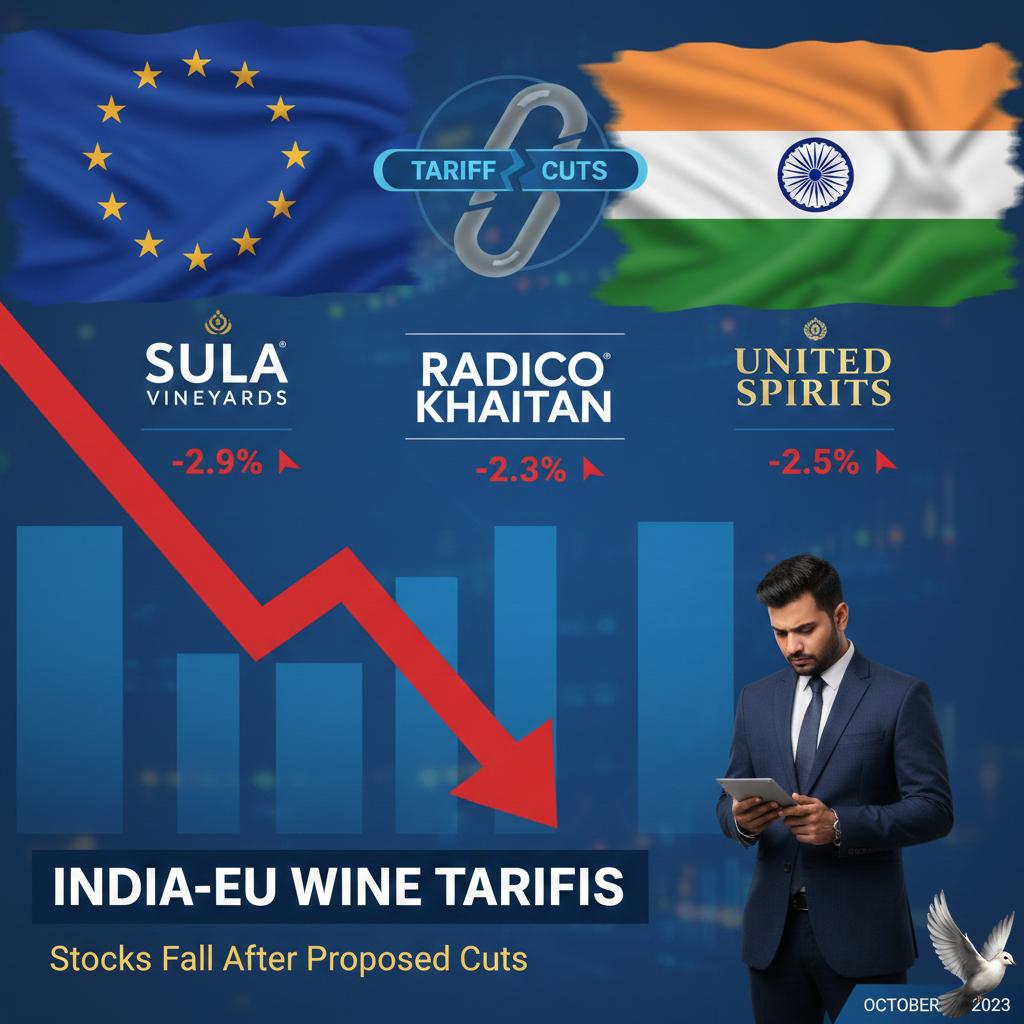

Sula Vineyards, Radico Khaitan, United Spirits Stocks Fall After Proposed India-EU Wine Tariff Cuts

**MARKET BRIEF: Liquor Stocks Hit by Historic India-EU Trade Deal** **Date:** January 27, 2026 **Subject:** Sector Update | Alco-Bev Indian alcohol stocks witnessed sharp selling pressure today following the conclusion of the long-awaited **India-EU Free Trade Agreement (FTA)**. The pact, finalized on Tuesday, drastically slashes import duties on European alcohol, exposing domestic producers to stiff competition from global heavyweights. **Market Reaction: Sea of Red** Domestic liquor majors took an immediate hit as the market digested the steeper-than-expected tariff cuts. * **Sula Vineyards** plunged to an all-time low, trading near **₹190**, down over **3%** intra-day. * **United Spirits (USL)** slipped approximately **1.5%**, while **Radico Khaitan** and **United Breweries** faced similar selling pressure. * Smaller players like **IFB Agro** and **Fratelli Vineyards** saw deeper cuts of roughly **4-5%**. **The Deal: Drastic Duty Reductions** The new agreement aggressively lowers barriers for European brands, far exceeding earlier industry estimates of gradual reduction. * **Wines:** Duties on premium European wines will crash from **150%** to just **20%**. Mid-range wines will see tariffs drop to **30%**. * **Spirits:** Import taxes on Whisky, Vodka, and Gin will be slashed from **150%** to **40%**. * **Beer:** Duties will fall from **110%** to **50%**. **Strategic Impact** While the deal opens EU markets for Indian brands, the immediate sentiment is bearish for domestic premium segments. The massive duty cut allows premium French and Italian wines, as well as Scotch whiskies, to retail at significantly lower prices. This directly threatens the high-margin "premiumization" strategy of companies like Sula and Radico Khaitan, forcing them to compete price-to-price with established global heritage brands. **Timeline** The agreement is expected to be signed later this year and come into force by **early 2027**. Domestic players now face a tight window to adjust pricing and marketing strategies before the floodgates open.

OneSource Specialty Pharma Q3 Results and Share Price Drop

OneSource Specialty Pharma: Market Brief (January 2026) **OneSource Specialty Pharma** shares faced intense selling pressure this week, plummeting **18%** to an intraday low of roughly **Rs 1,178**. The sell-off was triggered by a dismal third-quarter performance for FY26, driven by regulatory bottlenecks in key North American markets. **Financial Hit (Q3 FY26)** The company reported a consolidated net loss of **Rs 47 crore** (adjusted PAT), a sharp reversal from the profit recorded in the same period last year. Revenue took a massive hit, dropping **26%** year-on-year to **Rs 290 crore** (down from **Rs 393 crore**). Operating performance also suffered, with EBITDA collapsing **88%** to just **Rs 17 crore**. Consequently, EBITDA margins shrank dramatically to **6%**, losing over **3,000 basis points** compared to the healthy **36%** margin seen a year ago. **The Trigger: Canada Delay** The primary drag on performance was the delayed regulatory approval for **semaglutide** in **Canada**. OneSource acts as the manufacturing partner for **Dr. Reddy's Laboratories** for this blockbuster diabetes and weight-loss drug. Because of the delay, the company could not convert its Master Service Agreement (MSA) into a more lucrative Commercial Supply Agreement (CSA) during the quarter. This stalled revenue recognition and left the company bearing a high fixed-cost base with reduced inflows. **FY28 Outlook Intact** Despite the "subdued" quarter, management has reaffirmed its aggressive long-term targets. The company maintains its FY28 guidance of **$400 million** in organic revenue, potentially rising to **$500 million** when including proposed acquisitions. CEO **Neeraj Sharma** emphasized that the order book remains robust and the biologics funnel is at a historic high. The company continues to target an EBITDA margin of **~40%** and a Return on Capital Employed (ROCE) above **50%** by FY28, expecting the regulatory hurdles to be temporary.

Dr. Reddy's Laboratories Share Price and Trading Activity Update

I cannot proceed without the **CONTENT** you intended to provide. Please provide the original content about the market topic you want me to update and rewrite. Once you provide the content, I will follow your instructions: 1. Conduct a web search for the most recent and relevant market data, news, and trends. 2. Rewrite the updated content into a professional, mobile-friendly market brief, adhering to all your formatting and editorial rules. --- **What market topic is the brief about?** (e.g., Gold, S&P 500, Tech Stocks, Crude Oil) ---

Markets Decline 4% in January Amid Foreign Fund Outflows

Indian benchmark indices have navigated a tumultuous period this month, confirming the original premise of a significant correction driven by external pressures. After hitting a recent all-time high of **26,340** early in January, the Nifty 50 has since corrected sharply, falling by nearly **5%** from its peak. The BSE Sensex followed a similar trajectory, recently closing near **81,537**. This volatility reflects deep-seated concerns regarding global capital flows and mounting geopolitical risks. *** Foreign Capital Outflow and Rupee Pressure A primary factor driving the market’s downward trend is the relentless outflow of foreign capital. **Foreign Institutional Investors (FIIs)** have been consistent net sellers, offloading equities worth thousands of crores, creating sustained liquidity strain. This sell-off has compounded weakness in the currency market. The Indian rupee has faced severe pressure, recently hitting a record low by trading close to **92.00** against the US Dollar. A record-weak rupee amplifies the cost of imports, directly fueling inflation and broadening the current account deficit, which discourages fresh international portfolio investment. *** Trade Tariffs and Geopolitical Risks Geopolitical tensions have intensified, translating into direct market unease. Investors are particularly focused on the unpredictable trade relations with the United States. Hints of potential US tariffs reaching up to **500%** on certain Indian goods have unnerved the market, particularly impacting export-oriented sectors. This trade uncertainty, coupled with broader global risk aversion, has led to decreased trading volume and a general move towards caution among large institutional players. *** Macro Headwinds: Oil and Bond Yields Macroeconomic pressures continue to constrain a sustained market recovery. Crude oil prices remain elevated, adding to domestic cost concerns. Brent crude futures are holding firm around **$64** per barrel, while WTI trades near **$60**. Elevated energy costs directly impact corporate margins and feed into domestic price instability. Furthermore, volatility in the global fixed-income space remains a challenge. **Rising global bond yields** signal a higher cost of capital worldwide, increasing the discount rate for equity valuations and contributing to investor caution, as capital shifts towards relatively safer, higher-yielding government debt globally. *** Resilience and the Budget Focus Despite the FII exodus, the market has shown underlying resilience, largely thanks to **Domestic Institutional Investors (DIIs)**. DIIs have provided a critical counter-balance, pumping in capital that has helped prevent a deeper crash. The market’s outlook is now singularly focused on the upcoming Union Budget 2026-27, scheduled for **February 1, 2026**. This is a rare Sunday presentation that will see the stock exchanges remain open for trading. Market participants are strongly anticipating a traditional **pre-budget recovery** rally. Expectations are centered on government plans for structural reforms, an increased commitment to infrastructure capital expenditure, and potential income tax relief designed to boost flagging consumption and kickstart a new leg of economic growth. The budget is positioned as the immediate, crucial catalyst to restore confidence and provide a clear policy direction.

Dalal Street Week Ahead: Volatility Expected, Traders Advised to Stay Agile

📉 Market Correction Brief The markets recently underwent a **sharp corrective move**. The **Nifty 50** closed the volatile week significantly lower, breaking below critical technical support levels. The **India VIX** surged dramatically, reflecting a substantial increase in perceived market risk and uncertainty. While the market is showing **oversold conditions**, suggesting a potential technical rebound is possible, overall **volatility is expected to remain elevated**. This high level of market movement is particularly anticipated leading into the upcoming **Futures and Options (F&O) expiry**.

Sudeep Shah Analyzes Nifty Outlook Following 5% Decline in 11 Days

**Indian Equity Markets Weekly Update** Indian equity markets closed the week on a **subdued note**, impacted significantly by **profit-booking** and sustained **foreign investor outflows**. Sentiment was further dampened by rising **global trade concerns** and a series of **domestic earnings disappointments**, prompting a risk-off approach among traders. Analysts advise maintaining caution ahead of the upcoming **Union Budget**. The **Nifty** index is currently facing stiff resistance, with the broader markets showing persistent weakness. In sectoral trends, **PSU Banks** are demonstrating relative strength, notably outperforming their private sector peers.

Adani Group Stocks Decline Following US SEC Inquiry

**MARKET BRIEF: Adani Group Stock Performance and Regulatory Action** 📉 Adani Group stocks experienced a **sharp decline** on Friday, resulting in a market value drop of **over \$9 billion**. This volatility was triggered by news that the **U.S. Securities and Exchange Commission (SEC)** is seeking court permission to issue summons via email to Group founder **Gautam Adani** and his nephew, **Sagar Adani**. The regulatory action is linked to allegations concerning a reported **fraud and bribery plot**. Given the current uncertainty surrounding the regulatory investigation, investors are advised to **wait for clarity** regarding the legal developments.

Rupee drops to new low against dollar amid regulatory buzz and offshore flows

**MARKET BRIEF: Rupee Hits All-Time Low** The Indian rupee fell to a record low of **91.97** against the US dollar on Friday. This decline was driven by a confluence of aggressive equity selling and strong demand from importers seeking greenbacks. Market sentiment took a significant hit following reports of potential US regulatory summons issued to billionaire Gautam Adani. The allegations, which involve bribery and fraud, played a major role in accelerating the currency's retreat. Capital outflows continue to weigh heavily on the market. Foreign investors have divested more than **$3 billion** from Indian assets this month, signaling persistent bearishness.

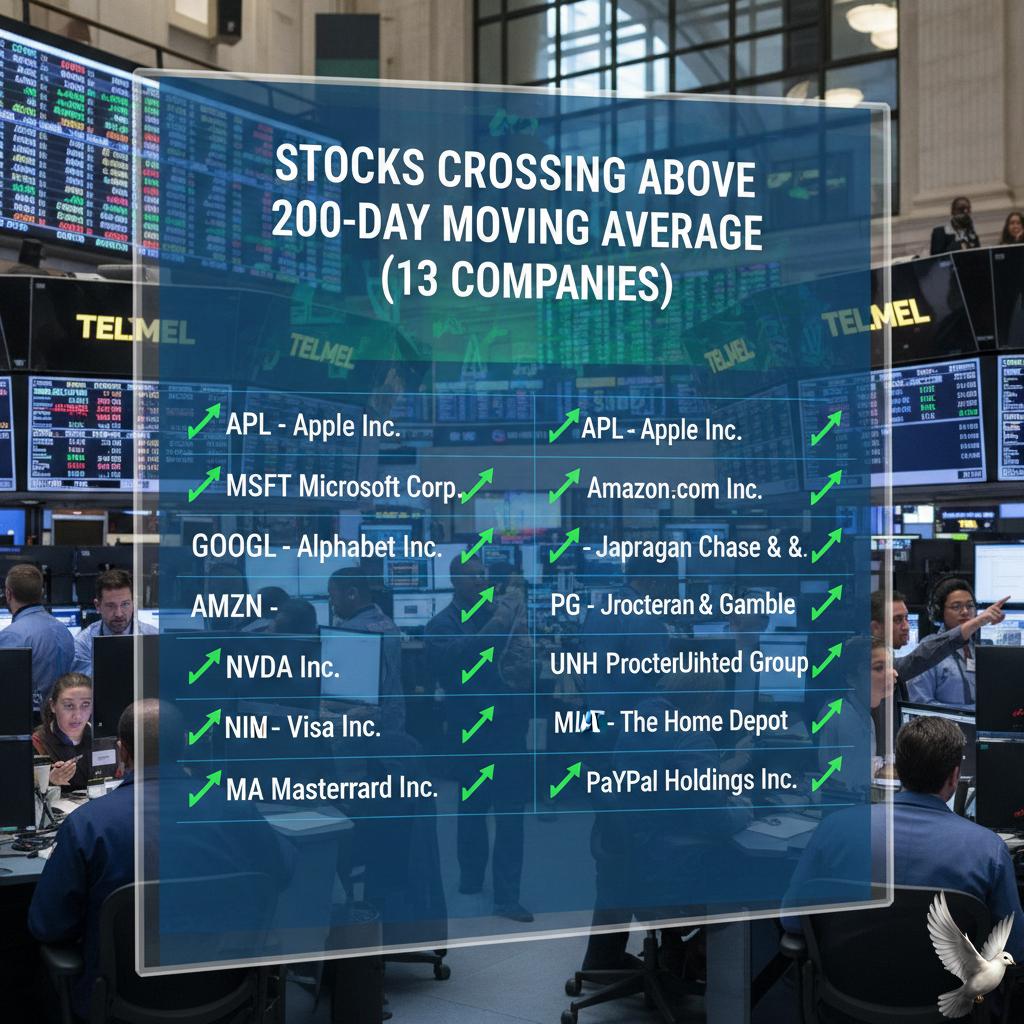

Stocks Crossing Above 200-Day Moving Average (13 Companies)

Technical Analysis: 200-Day SMA A stock is technically classified as being in a primary uptrend as long as the price maintains a level above the **200-day Simple Moving Average (SMA)**. This assessment relies specifically on the **daily timeframe**. Sustained price action above this key threshold serves as a primary indicator for confirming the structural health of a long-term bullish trend.

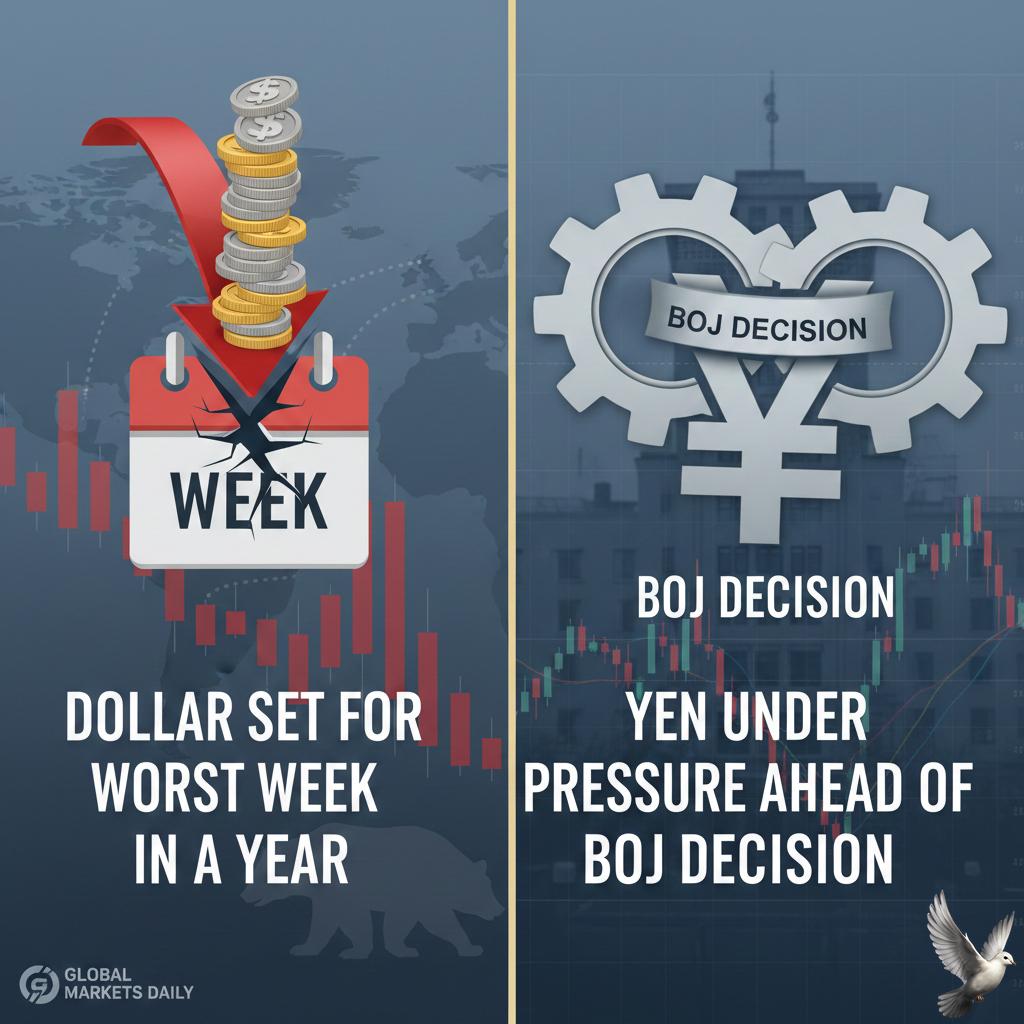

Dollar Set for Worst Week in a Year; Yen Under Pressure Ahead of BOJ Decision

📰 USD and JPY Movements --- The **U.S. Dollar (USD)** experienced its **largest weekly drop in a year**, driven by increased geopolitical tensions and reactions to President Trump's actions concerning Greenland. This shift in sentiment has notably unnerved investors. --- Simultaneously, the **Japanese Yen (JPY)** weakened, trading near **one-week lows**. Market attention is heavily focused on the impending **Bank of Japan (BOJ)** policy decision. Key interest lies in comments from BOJ Governor Ueda regarding potential **future rate hikes** intended to provide support for the currency.