Bullish News

Collection

Aditya Infotech Shares Rise 7.3% After Promoters Sell 5.3% Stake

Major institutional movements have reshaped the shareholding structure of Aditya Infotech Limited, the parent company of surveillance giant CP PLUS. In a significant bulk deal executed on BSE, promoters offloaded a 5.3% stake in the company. The Hari Khemka Business Family Trust and Dixon Technologies (India) together sold 62.6 lakh shares. The transaction was valued at approximately ₹920.8 crore, with shares changing hands at a fixed price of ₹1,470 per share. Market response to the move was notably positive. Following the transaction, Aditya Infotech shares rallied 7.3%, closing at ₹1,574.6 on the day of the trade. This uptick suggests strong investor confidence despite the promoter exit. Institutional appetite for the stock remains high. The shares were picked up by a consortium of heavyweights, including Motilal Oswal Mutual Fund, Kotak Mahindra Mutual Fund, Axis Mutual Fund, and HDFC Life Insurance. The company’s recent financial performance reinforces this institutional interest. Aditya Infotech reported a stellar Q3 FY26, with revenue climbing 37.3% to ₹1,139.1 crore. Even more striking was the bottom-line growth, as net profit surged 138.8% year-on-year to reach ₹96 crore. Growth is being driven by a 28.4% dominant market share in the Indian surveillance sector. The brand is pivoting heavily toward AI-integrated IP cameras, which now contribute 87% of total revenue. To sustain this momentum, the company is investing ₹500 million to expand its annual production capacity from 24 million to 30 million units. The broader sector continues to benefit from the "Make in India" push and smart city initiatives. The Indian surveillance market is projected to reach a valuation of $3.70 billion by 2025, maintaining a double-digit growth rate through 2033. For Dixon Technologies, the sale represents a strategic divestment of a portion of its 6.2% holding. Meanwhile, the Khemka family maintains a controlling interest in the firm, which has delivered returns of over 133% since its listing. The stock currently trades with a 52-week high of ₹1,745.10 and a low of ₹1,015. Technical indicators show the price holding steady above its 50-day moving average of ₹1,489, supported by rising net cash flows and consistent operational excellence.

Pandey: Indian Stock Market Presents Opportunities for Scale and Growth

India’s equity ecosystem is undergoing a structural shift toward greater transparency and resilience, aimed at securing long-term institutional capital. Market leadership remains focused on building an investable landscape that balances rapid growth with global governance standards. Current market data as of late February 2026 reflects a stabilizing trend after a period of high volatility. The Nifty 50 has recently hovered around the 25,482 level, while the BSE Sensex trades near 82,276. These figures represent a consolidation phase as the market processes global macroeconomic shifts and domestic earnings reports. The foreign investment landscape is showing signs of professional maturity. Foreign Portfolio Investor (FPI) assets have surged over recent cycles, reaching approximately ₹71 lakh crore. While FPIs have recently been net sellers in the secondary market, they remain active participants in primary offerings, signaling continued faith in India's long-term corporate pipeline. Domestic Institutional Investors (DIIs) have emerged as the market’s primary stabilizing force. In recent sessions, DIIs have consistently counterbalanced foreign outflows, with net buying frequently exceeding ₹3,100 crore in a single day. This domestic liquidity cushion has reduced the market's historical dependence on overseas sentiment. Regulatory reforms are accelerating to keep pace with this scale. SEBI has announced a comprehensive review of Portfolio Management Services (PMS) regulations, expected to be finalized by mid-2026. This overhaul aims to rationalize the framework for high-net-worth investors and institutional mandates, ensuring the rules remain adaptable to current market dynamics. Sector performance remains varied but growth-oriented. Recent winners include the automotive and metal sectors, driven by domestic demand and favorable global trade expectations. Conversely, the IT sector has faced headwinds due to shifting global technology spending, though recent sessions show a modest recovery as enterprise demand stabilizes. The rupee currently trades around 90.89 per US dollar. While the currency has faced pressure from global dollar strength, India’s record foreign exchange reserves and manageable external balances continue to provide a safety net against sharp depreciation. Looking ahead, the market is transitioning from a period of high exuberance to one of disciplined growth. With corporate balance sheets at their healthiest in a decade and a steady rise in retail participation via systematic investment plans, the infrastructure for a transparent and investable market is now firmly in place. [Market update for Indian investors](https://www.youtube.com/watch?v=VNZ2Z81uPhg) This video provides a deep dive into the recent SEBI board meetings and regulatory updates that are shaping the future of Indian equity markets. http://googleusercontent.com/youtube_content/0

SEBI Increases Oversight of Brokerage Dealing Rooms

Market Brief: Enhanced Surveillance in Brokerage Dealing Rooms India’s market regulator, SEBI, has significantly escalated its oversight of stockbroker operations under the newly implemented **SEBI (Stock Brokers) Regulations, 2026**. This updated framework, which became effective in early **January 2026**, replaces decades-old rules with a modernized mandate focused on preventing market abuse. The primary target is front-running, where brokerage employees use confidential information about large impending trades to profit personally. Under the new regime, brokers must establish an "institutional mechanism" specifically designed to detect and report such fraudulent practices. Tightening the Perimeter Regulatory focus has shifted from simple record-keeping to proactive prevention. Stockbrokers are now required to maintain all trading records and internal communications for a minimum of **8 years**, an increase from the previous 5-year requirement. This longer archival period ensures that investigators can trace complex trade patterns over a broader timeline. The 2026 regulations also introduce a residency requirement for management. Every brokerage must have at least one designated director residing in India for at least **182 days** per year. This ensures that a senior executive is directly accountable to local authorities for any compliance failures or ethical breaches. Tech-Driven Surveillance The oversight of dealing rooms has become increasingly data-centric. Brokers are now mandated to implement automated surveillance systems that flag suspicious activities to exchanges within **48 hours**. This is particularly critical for "Qualified Stock Brokers" (QSBs), who handle high volumes and are subject to even more stringent governance and technical capacity standards. Recent enforcement actions underscore the regulator's zero-tolerance policy. In **January 2026**, SEBI barred **12 entities** from the securities market for a period of **5 years** following a front-running investigation. The case resulted in the disgorgement of **₹1.07 crore** in illegal gains, plus **12% annual interest** and additional penalties totaling **₹90 lakh**. Institutional Accountability The regulator is looking closely at how trades are initiated for high-net-worth individuals and institutional clients. New rules prohibit brokers from operating unauthorized investment schemes or accepting cash from clients, aiming to close loopholes used for mule accounts and shadow trading. Compliance officers are now personally responsible for segregating client funds and ensuring that trading terminals are used only by authorized staff at approved locations. These measures collectively aim to protect market integrity as India’s trading volumes continue to reach record highs.

Metal Sector Gains 7% with Projected Upside of 25%

Market Brief: Metals Sector Momentum The metals sector emerged as a primary market driver on February 25, 2026, with the Nifty Metal index climbing **3%** in intraday trade. This rally followed a broader trend that saw metal stocks surge over **7%** during mid-week sessions. Investor sentiment has been bolstered by a landmark U.S. Supreme Court ruling on February 20, 2026. This decision effectively curbed the executive branch's authority to impose broad "reciprocal duties" under the IEEPA. Consequently, market analysts, including those from Morgan Stanley, expect average U.S. levies on Chinese imports to drop from **32%** to approximately **24%**. This reduction in trade friction has significantly eased global "peak uncertainty." Commodity Price Trends Base metals are reacting sharply to the reopening of Chinese markets post-Lunar New Year. Benchmark copper prices on the London Metal Exchange (LME) jumped **2.8%** to trade near **$13,228** per metric ton. Aluminum followed with a **1%** gain, reaching **$3,118.50** per metric ton. In the domestic market, silver prices surged **4%** to **$90.6**, providing a dual benefit to companies with exposure to both industrial demand and safe-haven investment. Steel prices also advanced **1.3%**, supported by domestic safeguard duties that have curtailed Chinese dumping and protected local margins. Stock Performance and Valuations Leading players in the sector have recorded substantial gains as capital rotates out of the IT sector into cyclical commodities. * **Vedanta Limited**: Shares rose **5%** to reach **₹732.35**. Global brokerages have upgraded the stock, with revised target prices suggesting an upside of up to **₹840**. * **Tata Steel**: Hit a new 52-week high of **₹216.35** on February 25. The company reported a **49.8%** year-on-year increase in quarterly Profit After Tax, reaching **₹2,787.42 crore**. * **Lloyds Metals & Energy**: Jumped **7.5%** following fresh "Buy" ratings from major brokerages, with technical targets set as high as **₹1,600**. * **National Aluminium (NALCO)**: Gained between **3%** and **5%** in recent sessions, fueled by the spike in global aluminum benchmarks. Outlook and Growth Drivers Analysts maintain a "buy on dips" stance, forecasting a potential near-term upside of **15%** to **25%** for the sector. The long-term trajectory for the Nifty Metal index targets the **15,000** level, provided it sustains its current breakout above the **12,400** resistance zone. Domestic demand remains a primary catalyst, specifically driven by infrastructure spending and the "green steel" policies introduced in the 2026 Union Budget. Furthermore, the rising adoption of electric vehicles and renewable energy infrastructure is expected to keep supply-demand balances tight for copper and aluminum through 2027. The sector's resilience is further evidenced by a **11%** year-to-date surge in the Nifty Metal index, significantly outperforming the broader Nifty 50, which fell **2.5%** in the same period. This divergence highlights a clear shift in institutional positioning toward commodity-linked equities.

IT Stocks Rise After Five-Day Decline Amid Analyst Cautions on Market Sustainability

Market Brief: Indian IT Sector Turbulence The Indian IT sector is navigating its most volatile period in over two decades. The **Nifty IT Index** has plunged **21%** in February 2026, marking its steepest monthly decline since the 2008 global financial crisis. On February 25, the index staged a modest recovery of **1.57%** to close at **30,526.35**, yet analysts maintain a cautious outlook as structural risks intensify. AI Disruption and Market Erosion Investor sentiment shifted sharply following the launch of advanced automation tools by US-based firms like Anthropic. Tools such as **Claude Code**, which can modernize legacy systems like COBOL, have raised fears regarding the future of traditional managed services. This technological shift has contributed to a **$68.6 billion** wipeout in market capitalization for the top 10 IT constituents in February alone. Major industry players are seeing significant valuation adjustments. **Infosys** has declined **21%** year-to-date, while **TCS** and **Wipro** have seen drops of **19%** and **24%**, respectively. Brokerages like Jefferies have responded by cutting price targets by as much as **33%**, citing a necessary pivot from labor-intensive models to AI-driven consulting. Divergent Growth and Employment While the broader sector faces pressure, **Nasscom** projects total technology revenue to reach **$315 billion** in FY26. However, growth has slowed to a modest **6.1%**. A significant trend is the plateauing of employment; the industry added only **135,000** net jobs this year, signaling a decoupling of revenue growth from headcount as AI-driven efficiency gains take hold. Currently, AI-related revenues account for approximately **$10–12 billion** of the total pie. Major firms are reporting varying degrees of AI integration, with **TCS** leading at an annualized run rate of **$1.8 billion**, followed by **Infosys** at **5.5%** of its total revenue. Technical and Derivative Outlook The technical structure for the sector remains bearish. Analysts have identified a **"Death Cross"** on weekly charts—a negative crossover of key moving averages—indicating that the previous "buy on dips" strategy has transitioned to "sell on rise." Immediate support for the Nifty IT is pegged near **29,960**, with a deeper floor at **28,800**. Derivative data shows significant call writing at the **25,800** and **26,000** strikes for the Nifty 50, suggesting a ceiling for any near-term relief rallies. Short covering was the primary driver for Wednesday's bounce, but a sustained reversal is unlikely without a stabilization of the Nasdaq and clearer long-term growth visibility.

Indian Credit Card Spending Decreased in January Following December Peak

The Indian credit card market entered February 2026 showing signs of structural consolidation and a shift toward high-value transactions. While overall spending moderated after a year-end surge, the industry reached a significant milestone with active cards in force climbing to **116.6 million**. **Spending Momentum and Market Shift** Monthly credit card spending stood at **Rs 1.99 lakh crore** in January 2026, marking an **8.1%** increase compared to the previous year. Although this represents a **2.7%** sequential decline from the December peak of nearly **Rs 2.05 lakh crore**, the drop is largely attributed to seasonal normalization following the festive cycle. A critical trend is the widening gap between card volume and spending value. The top five legacy banks now command **85.6%** of total transaction value, up from **81.2%** at the start of the fiscal year. This indicates that while mid-sized banks and fintech players continue to issue cards, consumers are increasingly using primary accounts from major lenders for high-ticket e-commerce, travel, and luxury purchases. **Dominant Players and Performance** HDFC Bank maintains its market leadership with a **22%** share of active cards and a **28.4%** share of total spending value. SBI Card follows closely, capturing **19%** of the card base and **24.7%** of spending value. Together, these two institutions control nearly half of the entire credit card market. Other major participants include ICICI Bank with a **16%** spending share and Axis Bank at **14%**. Notably, average spending per card has adjusted to approximately **Rs 17,700**, reflecting a move toward smaller, more frequent digital transactions. **Regulatory and Product Evolution** The landscape is being reshaped by new Reserve Bank of India (RBI) regulations effective early 2026. These updates mandate stricter two-factor authentication for all digital payments and require banks to provide fortnightly reporting to credit bureaus to improve data accuracy. The rise of UPI-linked credit cards remains a primary growth driver. RuPay-based credit transactions now account for roughly **38%** of total card transaction volume. This integration has moved credit usage beyond large purchases into everyday categories like groceries and local dining, effectively displacing traditional debit card usage at point-of-sale terminals. **Strategic Tightening** Lenders have adopted a more cautious approach to risk management. There is a visible tightening of underwriting standards and a widespread "devaluation" of reward programs. Many banks have introduced spending thresholds for lounge access and capped reward points on specific categories like utility bills and government payments. These measures aim to curb rising delinquencies and manage the high cost of premium card benefits in a maturing market. [Understanding Indian Credit Card Trends](https://www.youtube.com/watch?v=a_G-Q8VhXI4) This video provides a detailed breakdown of the latest RBI data and explains how spending patterns are shifting in the current economic climate. http://googleusercontent.com/youtube_content/0

IIFL Finance to Raise Up to $750 Million Through External Borrowings and Bonds

IIFL Finance is entering the final stages of a major capital expansion, targeting a raise of **$500 million to $750 million** through external commercial borrowings and dollar bonds this March. This strategic move, backed by Fairfax, aims to significantly diversify the lender's resource base and reduce its dependence on domestic bank funding. The fundraising is structured as a mix of dollar-denominated loans and foreign currency social bonds. These instruments are gaining traction as the company looks to fuel its business growth and capitalize on the latest regulatory relaxations. **Regulatory Tailwinds and Market Demand** The timing of this move coincides with the Reserve Bank of India’s landmark reforms introduced on **February 16, 2026**. Under the new framework, the borrowing limit for eligible entities has been increased from **$750 million to $1 billion**. Furthermore, the central bank has removed the all-in-cost ceiling, allowing borrowing rates to align naturally with global market conditions. Investor appetite for the company's debt remains high. A recent **2,000 crore INR** retail bond issue, launched on **February 17, 2026**, was oversubscribed within hours of opening. Domestic institutional demand also stays robust, with the company currently in the process of raising an additional **1,000 crore INR** through private placements. **Operational Recovery and Growth** IIFL Finance has shown a strong operational rebound following a challenging 2025. Key highlights include: - Total Assets Under Management (AUM) recovered to approximately **98,336 crore INR**. - Gold loan AUM surged by **189% year-on-year**, reaching **43,432 crore INR**. - Home loan portfolios remain stable at **31,893 crore INR**, reflecting a **5% annual growth**. The lender is currently engaging with a broad spectrum of global financial institutions, including prominent banks from **Singapore and Taiwan**. Existing lenders such as Deutsche Bank and Mizuho Bank have historically participated in the company's debt issues, underscoring its international credit standing. **Market Performance and Credit Stability** The company's stock is currently trading near the **503 INR** level, maintaining a market capitalization of approximately **21,385 crore INR**. While the broader financial sector has faced some volatility, IIFL has shown relative resilience, supported by a "Buy" rating from major analysts and a price target as high as **720 INR**. Credit ratings remain steady, with instruments assigned **AA/Stable by CRISIL** and **AA+/Stable by Brickwork Ratings**. These ratings reflect a low credit risk profile and high safety for debt servicing. The proceeds from the upcoming March issuance are earmarked for onward lending and the refinancing of existing high-cost debt. This shift toward international markets is expected to optimize the company's finance costs and provide the necessary capital cushion for its projected 2026 growth cycle.

Yes Bank-BookMyForex Data Breach Impacts 5,000 Users with Rs 2.5 Crore Loss

Yes Bank has reported a significant security incident involving its multi-currency prepaid forex cards, uncovering a series of unauthorized transactions originating from Latin America. The breach, detected on **February 24, 2026**, primarily targeted cards issued in partnership with the digital forex platform **BookMyForex**. Incident Details Unauthorized transactions totaling **Rs 2.55 crore** were approved during a five-hour window between **3:30 AM and 8:30 AM IST**. The fraudulent activity was traced to **15 merchants** based in a Latin American country where two-factor authentication for e-commerce is not mandatory. Fraud-monitoring systems flagged an unusual spike in transaction declines across specific bank identification numbers, allowing the bank to block **688 additional attempts**. This swift intervention prevented further potential losses estimated at **Rs 90 lakh**. Customer Impact and Response Approximately **5,000 customers** have been affected by the breach. Yes Bank has since restricted e-commerce transactions originating from the high-risk region to prevent recurring issues. The bank is currently working with BookMyForex to initiate chargebacks, aiming to recover the funds and ensure impacted users are protected from financial loss. BookMyForex has clarified that its own servers and systems remained secure throughout the incident. Market Performance The news coincided with a period of high trading volume for Yes Bank shares. On **February 25, 2026**, the stock closed at **Rs 20.79** on the NSE, marking a daily decline of **2.22%**. Despite this short-term volatility, the bank’s broader financial health remains resilient. Recent **Q3 FY26** results highlighted a **55.4%** year-on-year jump in net profit, reaching **Rs 952 crore**. Sector Outlook Cybersecurity remains a critical focus for the Indian banking sector in **2026**. With global cybercrime damages projected to reach **$10.5 trillion** this year, the Reserve Bank of India (RBI) has reinforced mandates for real-time threat reporting and enhanced third-party risk management. Yes Bank’s recent inclusion in the **NIFTY BANK Index** and its improved **S&P Global ESG score of 79** reflect ongoing efforts to build a more stable and transparent institutional framework amid evolving digital threats.

Key Factors Influencing Thursday's Stock Market Performance

Indian equity benchmarks settled with minor gains on Wednesday, recovering partially from a sharp sell-off in the previous session. The **Nifty 50** advanced **57.70 points** or **0.23%** to close at **25,482.35**, while the **S&P BSE Sensex** added **50.15 points** or **0.06%** to end at **82,276.07**. The session was characterized by high volatility, as early morning gains of over **700 points** on the Sensex were largely erased by afternoon profit-booking. Market sentiment remains cautious as investors prepare for the release of third-quarter GDP data on February 27, with growth projected at **8.1%**. The **Nifty Metal** index led the recovery, surging **2.70%** on the back of strong performances from major players. The **Nifty Auto** and **Nifty Pharma** indices also outperformed the broader market, each gaining **1.85%**. The automotive sector continues to show domestic resilience, with the sectoral index nearing its record high of **29,179.10**. Buying interest in the IT sector provided additional support, with the **Nifty IT** index rising **1.57%** as value buying emerged following recent concerns regarding automation and project timelines. Upside remained capped by weakness in heavyweights and selective selling in other sectors. The **Nifty PSU Bank** index fell **0.39%**, while **FMCG** and **Realty** also traded in the red, declining **0.25%** and **0.19%** respectively. Foreign Institutional Investors (FIIs) have shown mixed activity, recording a net sell-off of **102.53 crore** in the most recent session, while Domestic Institutional Investors (DIIs) provided a cushion with net purchases worth **3,161.20 crore**. Volatility showed signs of cooling as the **India VIX** dropped **4.68%** to settle at **13.49**. Despite this stabilization, the market breadth remained negative, indicating a defensive stance among participants. In the currency and commodity markets, the Indian rupee strengthened slightly to **90.88** against the US dollar. **MCX Gold** for April delivery rose **0.71%** to reach **161,110**, reflecting a continued preference for safe-haven assets amid global macroeconomic shifts.

Circle Shares Rise 20% Following Better-Than-Expected Revenue and Stablecoin Growth

Circle Internet Group (NYSE: CRCL) delivered a massive earnings beat on Wednesday, February 25, 2026, reporting fourth-quarter revenue and reserve income of 770 million dollars. This performance surpassed Wall Street consensus estimates of 747 million dollars, marking a 77% year-over-year surge. Following the announcement, Circle’s shares jumped more than 20% in early trading, reaching nearly 74 dollars. The rally reflects investor confidence in the company’s ability to monetize its reserves as its flagship stablecoin, USDC, gains massive market traction. **Key Financial Highlights** The quarterly net income for Q4 reached 133 million dollars, or 43 cents per share. This was a significant jump from the 4 million dollars recorded in the same period last year and far exceeded analyst expectations of 16 cents per share. Full-year 2025 revenue reached 2.7 billion dollars, up 64% from the prior year. While the company reported an annual net loss of 70 million dollars, this was primarily due to one-time stock-based compensation costs of 424 million dollars triggered by its 2025 IPO. Operating performance remains strong, with adjusted EBITDA for the quarter hitting 167 million dollars, a 412% increase compared to 2024. **USDC Market Expansion** The growth was fueled by a 72% increase in USDC circulation, which ended the year at 75.3 billion dollars. On-chain transaction volume for USDC reached a record 11.9 trillion dollars in Q4, representing a 247% increase. This surge highlights the token's growing utility for institutional payments and digital finance. Circle’s euro-denominated token, EURC, also saw explosive growth, with circulation rising 284% to 310 million euros. **Strategic Outlook and Regulatory Moves** The company is benefiting from a more favorable regulatory environment following the passage of the GENIUS Act in 2025, which established a federal framework for stablecoins. Circle recently received conditional approval to establish a national trust bank, a move that would place its reserves under the direct oversight of the OCC. Management has issued bullish guidance for 2026, targeting a 40% compound annual growth rate for USDC circulation. The company is also diversifying its revenue streams through its new "Arc" infrastructure platform, which has already processed over 166 million transactions during its institutional testnet phase. **Market Context** Despite today's 20% surge, Circle’s stock continues to navigate high volatility, remaining below its 2025 highs. However, the company’s position as a regulated leader in the 300 billion dollar stablecoin market is strengthening as it captures a larger share of global transaction volumes and institutional partnerships.

Short-Term Trading Outlook for Central Bank of India and Colgate-Palmolive

Market Overview The Nifty 50 concluded the session on February 25, 2026, with a modest gain of **57.85 points**, closing at **25,482.50**. Despite an intraday surge of over **700 points** following easing global tariff concerns, heavy profit booking in market heavyweights trimmed the final gains to **0.23%**. The index continues to trade in a volatile sideways pattern, hovering near its critical **200-day Simple Moving Average (SMA)**, which currently sits around the **14,125** level for the Nifty 200, while the Nifty 50 remains caught in a tight consolidation zone between **25,350** and **25,900**. Sector Performance The **Auto sector** emerged as a primary driver of the recovery, with the Nifty Auto index rising **1.85%**. **Bajaj Auto** led the charge, jumping **2.74%** to settle at **10,098.50**. The ancillary space also saw significant momentum, with **Bosch Ltd** gaining **3.62%** to reach **36,610.00**. The **IT sector** staged a strategic rebound after recent sharp declines. **HCL Technologies** climbed **2.74%** to **1,375.90**, while **TCS** advanced **2.14%** to close at **2,629.00**. This recovery was viewed as value buying following a period of sector-wide pressure. Conversely, the **PSU Bank** and **Energy** sectors faced headwinds. **State Bank of India** fell **1.93%** to **1,199.30**, and **Reliance Industries** dropped **2.23%** to **1,400.80**, acting as the main drags on the frontline indices. Technical Outlook & Recommendations Market volatility, measured by the **India VIX**, cooled by nearly **5%** to settle at **13.49**, suggesting a temporary stabilization in sentiment. Analysts are currently highlighting selective opportunities in the banking and FMCG spaces. **Central Bank of India** is maintaining a bullish bias, trading at approximately **40.20**. The stock is currently priced at **0.92 times** its book value and has shown a significant **31.23%** quarterly profit variance. Technical indicators place its first major resistance at **40.30**, with a long-term target potential extending toward **55.00** according to some brokerage projections. **Colgate-Palmolive (India)** is also under the spotlight as a bullish contender in the FMCG segment. The stock ended the session near **2,270.40**. While it remains below its 200-day moving average, a sharp **16.18%** surge in Open Interest suggests fresh capital entry and a building conviction for a directional breakout. Consensus targets for the stock average around **2,431.43**, representing a potential upside of approximately **7%**. Investors are now shifting focus toward the upcoming **GDP data** release on February 27, which is expected to dictate the next major move for the benchmark indices.

US Equities Rise Ahead of Nvidia Earnings Results

US equity markets opened in positive territory on Wednesday as investors shook off earlier volatility to focus on a high-stakes earnings report from the world’s leading AI chipmaker. The S&P 500 climbed 0.5% in early trading, recovering losses from a turbulent start to the week. The Nasdaq Composite led the gains with a 1.0% jump, while the Dow Jones Industrial Average edged up by 69 points, or 0.1%. Nvidia remains the primary engine for market sentiment. The stock rose 1.7% ahead of its fourth-quarter results, with analysts projecting a massive 70% surge in profit to approximately 37.52 billion dollars. Investment in AI infrastructure shows no signs of slowing down. Major "hyperscalers" including Microsoft, Google, Meta, and Amazon are estimated to hit 600 billion dollars in capital expenditure for 2026, much of which is directed toward Nvidia's hardware. Beyond the chip sector, other tech players are showing strength. AMD shares added 1% following news of a multi-year agreement with Meta to deploy 6 gigawatts of processing power for its data centers. Trade policy continues to be a point of intense focus. While earlier fears of aggressive tariffs on Canada and Mexico weighed on sentiment, recent legal rulings have temporarily shifted the outlook. The U.S. Supreme Court recently invalidated certain unilateral tariff measures, leading to a pivot in strategy. The administration has since implemented a 10% blanket tariff on most imports under different legal authorities, though key goods like pharmaceuticals and critical minerals remain exempt. Market volatility is also being fueled by a split in performance across different sectors. While tech and AI-related stocks are driving the indices higher, more than half of the stocks in the S&P 500 actually traded lower in the early session. Sectors sensitive to trade and consumer spending are facing pressure. Industrial and consumer discretionary stocks have lagged as investors weigh the impact of new trade surcharges and a visible slowdown in the pace of US hiring. The CBOE Volatility Index, often called the market's "fear gauge," recently ticked up by over 4%, reflecting the high stakes of this week's corporate and economic data. Traders are pricing in a potential 6% swing for Nvidia following its announcement, a move that could dictate the direction of global markets for the remainder of the week. Solid underlying business investment continues to support US growth despite a slight slowdown in GDP. The focus remains on whether corporate earnings can justify current valuations amid the evolving trade and regulatory landscape.

IRFC OFS Under-Subscribed; Government to Skip Greenshoe Option

Market Brief: IRFC Offer for Sale Update The Government of India has officially decided to skip the oversubscription option for the **Indian Railway Finance Corporation (IRFC)** Offer for Sale (OFS). This decision follows a lukewarm response on the opening day of the issue, which was reserved for non-retail investors. The government originally planned a base offer of **2%** equity, with a "green shoe" or oversubscription option for an additional **2%**. By skipping this option, the total divestment is now capped at the base size of **26.13 crore shares**. Subscription and Pricing Data Non-retail bidding on February 25, 2026, saw a subscription of **95%** for the institutional portion. This left an undersubscription of approximately **1.18 crore shares** at the close of the first day. The floor price for the offer was set at **₹104** per share. At this level, the initial base offer is valued at roughly **₹2,718 crore**, significantly lower than the **₹5,436 crore** target that would have been reached had the full **4%** stake been sold. Stock Market Impact Following the announcement, IRFC shares faced significant downward pressure on the exchanges. The stock closed at **₹104.43** on the NSE, marking a sharp decline of **4.6%** in a single session. The current trading price is hovering just above the OFS floor price. This move has pushed the stock to a new **52-week low**, reflecting a persistent "supply overhang" as the market absorbs the additional equity. Sector Performance and Outlook The broader railway sector is currently navigating a period of high volatility despite robust government backing. * **Capex Allocation:** The Union Budget for FY25-26 has earmarked a record **₹2,62,200 crore** for railway capital expenditure. * **Infrastructure Targets:** Ongoing projects aim to expand the network by **307 km** by 2030, with a focus on freight capacity and electrification. * **Market Sentiment:** Peer companies like RVNL and Texmaco Rail have also seen price corrections recently, attributed to margin compression and high valuations despite strong order books. Shareholding and Regulatory Goals As of December 2025, the government held an **86.36%** stake in IRFC. The primary objective of this OFS is to move closer to the SEBI-mandated **75%** limit for public shareholding in listed entities. Despite the current market cooling, IRFC reported a record profit after tax of **₹1,802 crore** for the quarter ended December 2025, representing an **11%** year-on-year growth. Net interest margins also saw an improvement of **8%** during the same period. The retail portion of the OFS opens on February 26, 2026, allowing individual investors to bid for the remaining shares at the established floor price.

HSBC India Pre-tax Profit Rises 11% Driven by Corporate and Institutional Segments

HSBC India has solidified its position as a primary engine of growth for the global banking giant, reporting an 11% increase in profit before tax to $1.9 billion for the 2025 calendar year. This performance elevates India to the bank’s second-largest profit contributor in Asia, trailing only Hong Kong and surpassing mainland China, where earnings were impacted by significant one-off charges. The surge was anchored by the Corporate and Institutional Banking (CIB) segment, which contributed $1.5 billion to the total pre-tax profit. This vertical benefited from a 60% year-on-year increase in equity capital market issuances and strong momentum in cross-border transaction banking. Corporate lending across Asia, including India, grew by $7 billion, reflecting the bank's success in capturing supply chain shifts and multinational client business. Wealth management and personal banking also showed resilience, with the bank expanding its footprint to four new cities and launching international wealth solutions in GIFT City. Despite a global headcount reduction, HSBC expanded its India workforce to 47,423 employees, making it the bank's largest staff base worldwide. Customer accounts in the country grew to $28.73 billion, up from $27.20 billion the previous year. On a global scale, HSBC reported a pre-tax profit of $29.91 billion for 2025. While this exceeded market expectations, it represented a 7% decline from the $32.3 billion recorded in 2024. The drop was largely attributed to $4.9 billion in one-off charges, including a $2.1 billion write-down related to its stake in China’s Bank of Communications. The bank is currently undergoing a strategic pivot to become a simpler, more agile institution. Key highlights of this transformation include: - Achieving $1.5 billion in annualized cost savings six months ahead of schedule. - Announcing 11 business or market exits to optimize the global portfolio. - Raising the return on tangible equity target to 17% or better through 2028. - Initiating a new share buyback program of up to $2 billion. In the broader Indian banking landscape, structural trends remain favorable. Domestic credit expanded 11.19% to reach $2.27 trillion by mid-2025, while gross non-performing assets across the sector fell to a historic low of 2.31%. This healthy macro environment, combined with the RBI's shift toward a neutral monetary stance and interest rate cuts in mid-2025, has provided a robust backdrop for foreign lenders to scale their operations.

Zerodha’s Nithin Kamath Advocates for Loan Against Shares to Refinance High-Interest Debt

Zerodha Capital has scaled its Loan Against Shares (LAS) business to cross the **Rs 500 crore** mark. CEO Nithin Kamath describes this segment as a strategic tool for investors to settle high-interest liabilities, such as credit card debt or personal loans, without liquidating their long-term portfolios. The lending unit offers structured interest rates starting at **10.00%** per annum for loan amounts above **Rs 5 crore**. For smaller requirements between **Rs 25,000** and **Rs 50 lakh**, the rate is set at **11.00%**. These rates remain significantly lower than traditional unsecured credit options. Investors can borrow up to **Rs 10 crore** against a wide list of approved stocks and mutual funds. The process is fully digital, typically seeing funds credited within **one working day**. The model uses a standard Loan-to-Value (LTV) ratio of **50%**, requiring a collateral buffer to manage market volatility. Kamath has recently highlighted the importance of transparency regarding hidden costs in the broader brokerage industry. He specifically pointed to Depository Participant (DP) charges, which are often overlooked by retail participants because they do not appear on standard contract notes. At Zerodha, DP charges are fixed at **Rs 15.34** (inclusive of GST) per scrip, per day for male account holders. Female primary holders receive a slight discount, with the total coming to **Rs 15.05**. These fees apply only on the sell side for delivery-based trades and are debited directly from the ledger. The market environment is shifting due to new regulatory mandates effective **April 1, 2026**. These rules will standardize collateral requirements for market intermediaries. While these changes may increase costs for many brokers, Zerodha expects no impact on its client fee structure as the firm operates as a self-clearing member with zero external financing. Regulatory changes have also targeted speculative trading. Following the Union Budget 2026, the Securities Transaction Tax (STT) on futures has risen to **0.05%**, while options have seen an increase to **0.15%**. These adjustments make secured lending products like LAS a more stable alternative for maintaining liquidity compared to high-frequency speculative trading.

Indian Debt Capital Market Participants Seek Enhanced Funding Regulatory Flexibility

India’s corporate bond market is undergoing a significant transformation, with outstanding issuances reaching approximately 53.6 trillion INR as of early 2025. Despite a robust 12% annual growth rate over the last decade, the market remains heavily concentrated among top-rated issuers. Current data shows that while fundraising through bonds is increasingly competitive with bank credit, secondary market liquidity continues to be a bottleneck. Recent 10-year benchmark government bond yields have stabilized around 6.67%, providing a reference for corporate pricing. However, corporate bonds typically command a spread of 0.8% to 1% over sovereign debt to attract investors. Merchant bankers are now pushing for a strategic shift in regulatory policy. They have formally requested that the Securities and Exchange Board of India (SEBI) allow borrowing against corporate bonds. This move is designed to boost underwriting capacity, allowing intermediaries to manage risks more effectively during periods of weak debt demand. The industry is also advocating for an anonymous bond-trading platform. Proponents argue that such a platform would mirror the efficiency of equity markets, facilitating better price discovery and deeper liquidity. Currently, much of the trading is handled through private placements or specialized request-for-quote platforms, which can limit the participation of smaller players and retail investors. To further broaden the ecosystem, bankers are seeking access to more diverse funding sources. This comes at a time when retail participation is rising, aided by SEBI’s decision to reduce the minimum face value of privately placed bonds to 10,000 INR. Total fresh issuances are projected to hit 11 trillion INR in the coming fiscal year, underscoring the urgency for improved liquidity mechanisms. While SEBI recently introduced a voluntary "liquidity window" to help investors exit holdings, early adoption by issuers has been slow due to complex compliance requirements. Merchant bankers believe that enabling repo transactions—where bonds can be used as collateral for short-term loans—is the missing link needed to give market makers the flexibility to provide continuous buy and sell quotes. Strengthening these structural components is seen as essential for India to reach its goal of a 100 trillion INR bond market by 2030. Success will depend on whether regulators can balance the need for tighter oversight with the flexibility required for intermediaries to maintain a vibrant, liquid secondary market.

India Long-End Bonds Supported by Investor Demand While Benchmark Yields Remain Steady Ahead of Supply

Market Brief: India Debt Performance India's longer-duration government bonds recorded gains on Wednesday, underpinned by sustained interest from long-term institutional investors. Insurance companies and pension funds continue to absorb longer-dated paper, driven by a stable domestic inflation outlook and a favorable interest rate environment. The benchmark **10-year** bond yield settled slightly higher at **6.69%**, compared to the previous close of **6.68%**. Yields saw early downward pressure during the session, touching intraday lows of **6.67%**, but ultimately flattened as traders balanced healthy demand against an upcoming supply of central government debt. Primary Market Dynamics The market successfully absorbed a higher-than-expected supply from state governments this week. On Tuesday, Indian states raised **46,100 crore** through the weekly State Development Loans (SDL) auction. This amount exceeded the planned notified value of **44,550 crore**, signaling deep liquidity and a strong appetite for sovereign-backed debt despite the increased volume. Attention is now shifting toward the central government’s scheduled auction on Friday. The Reserve Bank of India is set to offer **32,000 crore** of the **10-year** benchmark security. This issuance is a critical component of the government’s borrowing program and will serve as a definitive test for market pricing. Economic and Policy Context Market sentiment remains supported by the Reserve Bank of India’s steady policy stance. In its February 2026 meeting, the Monetary Policy Committee maintained the repo rate at **5.25%** and retained a neutral stance. This follows a cycle where the central bank cut rates by a cumulative **125 basis points** through 2025 to support growth. Inflationary pressures are currently viewed as manageable. The headline CPI for January was reported at **2.75%**, staying well within the central bank's tolerance band. Projections for the first half of the next fiscal year suggest inflation will hover between **4.0%** and **4.2%**, providing a predictable backdrop for fixed-income participants. Global and Currency Factors Domestic yields are also navigating global volatility. The **U.S. 10-year** Treasury yield rose to **4.06%** on Wednesday as markets reacted to new global tariff structures. While global yields rose, the Indian rupee remained resilient, trading near **90.88** against the U.S. dollar. In the secondary market, the yield curve continues to benefit from a recent debt-switch operation. The government recently bought back **755 billion** of near-term maturities and issued securities maturing in **2040**, a move that has effectively reduced immediate redemption pressures and encouraged investment in longer durations.

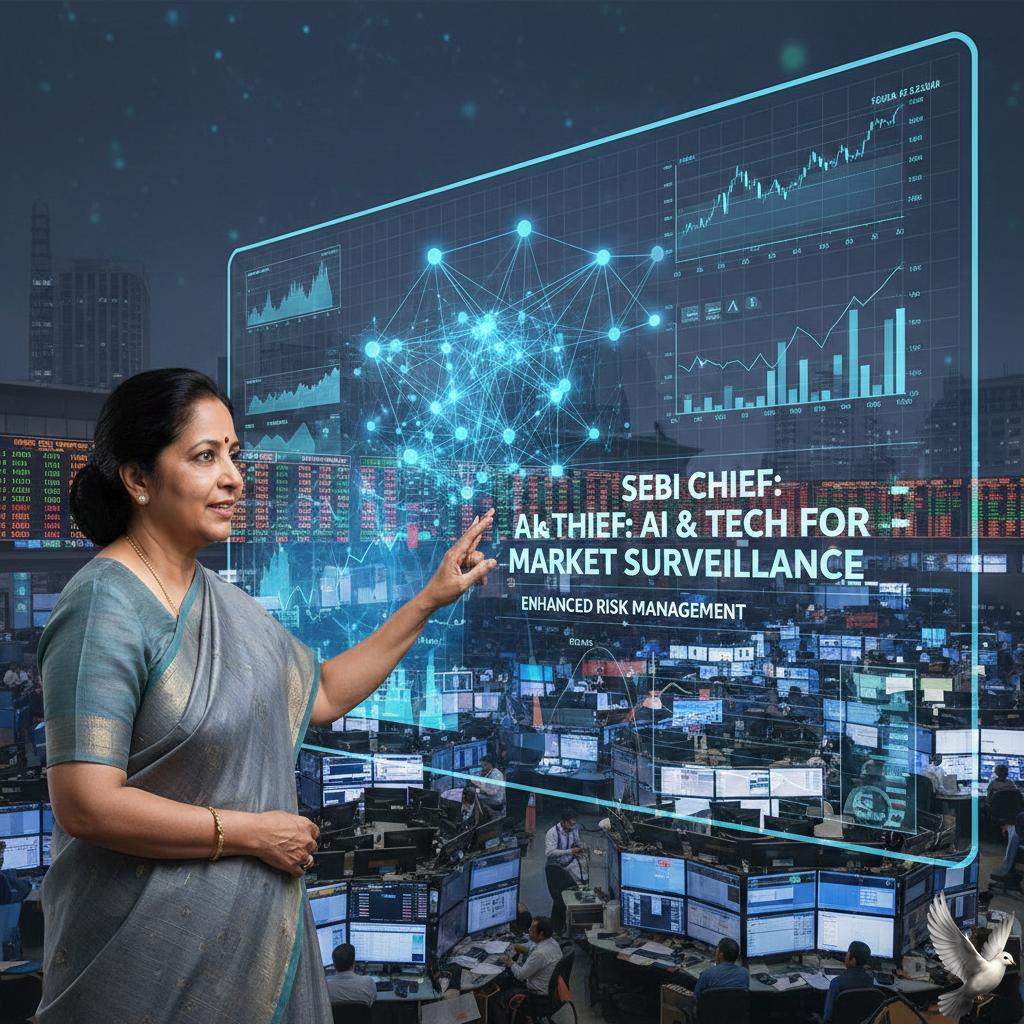

Sebi Chief: AI and Tech to Enhance Market Surveillance and Risk Management

Market Brief: SEBI Directs AI Push for Market Integrity The Securities and Exchange Board of India (SEBI) is accelerating the integration of Artificial Intelligence to transform market oversight. Chairman Tuhin Kanta Pandey recently confirmed that AI is now a core component of the regulator's enforcement architecture. The strategy focuses on three pillars: strengthening real-time surveillance, improving risk management, and enhancing transparency across the financial ecosystem. Strategic AI Deployment SEBI is currently deploying AI tools to monitor financial influencers, or "finfluencers," to ensure compliance with investment advice regulations. The technology is also being used to scan market advertisements and detect patterns of insider trading in real time. Beyond misconduct, AI is performing audits of cyber security frameworks to proactively identify systemic vulnerabilities. Market Context and Performance As of February 25, 2026, the Indian equity benchmarks showed marginal gains following a period of high volatility. The **Sensex** settled at **82,276.07**, gaining **50.15 points**, while the **Nifty 50** closed at **25,482.35**, up **57.70 points**. Market sentiment has been influenced by global factors, including a **10%** universal tariff implementation in the U.S. and concerns over AI-driven disruption in the IT sector. Sectoral Trends and Growth Growth in the Portfolio Management Services (PMS) industry highlights the need for advanced oversight. Assets under management in the PMS sector rose to **₹10.5 lakh crore** as of January 2026, representing a compound annual growth rate of approximately **17%**. The number of PMS clients has climbed to **2.15 lakh**, marking a nearly **50%** increase since 2022. While technology leads the recovery, sectoral performance remains mixed. The **Nifty Metal** index recently outperformed the broader market, whereas **PSU Banks** and **Realty** sectors have faced downward pressure. Regulatory Evolution The transition toward "SupTech" (Supervisory Technology) is designed to keep pace with an economy where market capitalization has grown fourfold over the last decade to over **₹470 trillion**. India's market cap as a share of GDP has risen from **81%** in 2015 to **138%** today. To manage this scale, SEBI has formed a high-level working group to develop a technology roadmap for Market Infrastructure Institutions, targeting both 5-year and 10-year strategic goals. The shift represents a move from static rules to dynamic, anticipatory supervision. The regulator aims to ensure that as the market attracts more institutional capital, the quality of governance and disclosure remains world-class.

US Stock Futures Edge Higher Ahead of Nvidia Earnings

U.S. stock index futures pushed higher on Wednesday morning as the market worked to recover from earlier volatility. Investors are currently recalibrating their positions in the artificial intelligence sector while navigating renewed uncertainty surrounding global trade policies. Technology shares are leading the upward momentum. The Nasdaq 100 rose 0.94% in recent trading, while the S&P 500 gained 0.48% to reach approximately 6,922.83. The Dow Jones Industrial Average also trended upward, rising 0.22% to 49,280.34. Nvidia remains the primary focus of the global AI trade. The company is expected to report its fiscal fourth-quarter results today, with analysts anticipating a massive 68% jump in revenue to roughly $65.9 billion. Adjusted earnings are projected to rise 72% to $1.53 per share. Market sentiment received a boost following a 10% global import tariff implementation, which was lower than the 15% to 25% previously feared. However, uncertainty remains as the administration suggests these rates could still be adjusted. Trading activity shows a clear shift toward AI infrastructure. Major software and chip stocks are rebounding as investors look for confirmation that heavy capital expenditures in data centers will continue to drive growth through 2026. The VIX volatility index has retreated to 18.68, a drop of 4.45%, signaling a temporary easing of investor anxiety. Despite this, technical levels remain critical, with the S&P 500 holding between the 6,800 and 7,000 range as participants await the next major catalyst. Key metrics to watch include Nvidia’s gross margins, which are targeted at 75%. This figure will serve as a definitive indicator of pricing power in the semiconductor industry and will likely dictate the direction of tech indices in the coming sessions.

Copper Reaches Two-Week High Following Reversal of US Tariffs

Copper prices have surged to a fresh two-week peak, trading near **$13,195** per metric ton on the London Metal Exchange (LME) as of February 25, 2026. This recovery follows a volatile period where the metal retreated from its January all-time high of **$14,527**. The primary driver for this bullish momentum is a significant shift in trade policy. Market sentiment has brightened following a U.S. Supreme Court ruling that struck down sweeping reciprocal tariffs. This legal development has eased fears of a localized supply glut in the U.S. and improved the outlook for global trade flow. Demand is currently anchored by the return of Chinese industrial buyers. Following the Lunar New Year holiday, the Yangshan copper premium—a key indicator of Chinese import appetite—jumped **60%** to reach **$53** per ton. This signals an immediate need for physical material despite a seasonal rise in local inventories. The "AI Metals Frenzy" continues to redefine the long-term floor for copper. New data suggests a single hyperscale AI data center can require up to **50,000 tons** of copper, which is nearly ten times the requirement of conventional facilities. This structural demand is competing with the needs of the global energy transition. Supply-side constraints remain a persistent concern. Mine production growth for 2026 has been revised downward to **2.2%** from previous estimates of **2.8%**. Declining ore grades in major producing regions like Chile are forcing miners to process more material for lower yields, supporting the case for sustained high prices. While global exchange stocks have reached their highest levels since early 2025, exceeding **243,000 tonnes** on the LME, the market is viewing this as a temporary buffer rather than a sign of oversupply. Analysts maintain a constructive outlook, with price targets for the second quarter focusing on the **$13,500** to **$14,000** range. Traders are now closely watching U.S. manufacturing data and upcoming earnings from major technology firms to gauge the pace of infrastructure spending. Copper’s role as an economic barometer remains intact, with its current trajectory reflecting a mix of industrial recovery and strategic stockpiling.