Bullish News

Collection

Ascendas Firstspace acquires 9 lakh sq ft industrial warehousing space in Gujarat for Rs 275 crore

**Ahmedabad Industrial Market Brief** CapitaLand-backed Ascendas Firstspace has finalized a strategic acquisition of 900,000 square feet of Grade-A warehousing and industrial space in Bawla, Ahmedabad. The transaction, valued at approximately 275 crore, was executed through a forward purchase agreement with the Gujarat-based Crystal Group. This deal marks the formal entry of Ascendas Firstspace into the Gujarat market. The project is slated for a phased development and handover over the next 18 months, ensuring that capital deployment remains closely aligned with construction progress and high governance standards. **Strategic Location and Connectivity** The Bawla micro-market is situated along National Highway 48, making it a critical node for logistics. Its location provides seamless connectivity to the Ahmedabad city center and serves as a vital link between the industrial corridors of Gujarat, Maharashtra, and Rajasthan. The region has seen a surge in demand from third-party logistics (3PL) providers, e-commerce giants, and manufacturing firms. This acquisition addresses the growing need for institutional-grade facilities as occupiers increasingly prioritize operational efficiency and modern infrastructure. **Ahmedabad Market Trends** The Ahmedabad industrial and logistics sector showed strong momentum throughout 2025. Total annual absorption reached 2.2 million square feet, while new supply additions stood at 3.1 million square feet. This increase in supply pushed the overall vacancy rate slightly higher to 14.2%, compared to 12.1% in the previous year. Rental values in the Changodar-Bawla cluster have remained resilient, posting a 5% year-on-year increase. Industrial land prices in the area have followed a similar upward trajectory, appreciating by 4% to 5% as prime land becomes increasingly scarce. **National Sector Performance** The broader Indian warehousing market continues to transition toward Grade-A assets, which now account for 62% of total transaction volumes nationwide. Manufacturing has overtaken third-party logistics as the primary driver of demand, contributing 48% of all leasing activity in early 2025. Average Grade-A rents across India's top eight markets range between 55 and 85 per square foot per month. Despite a slight recalibration in total absorption compared to the record highs of 2024, the sector remains a magnet for institutional investment, with over 10,000 crore in private equity entering the market in the last year. **Economic Outlook** India’s manufacturing momentum is reflected in the Purchasing Managers' Index (PMI), which peaked at 58.4 in mid-2025. Coupled with record GST collections and a stable inflation forecast of 3.7% for the upcoming fiscal year, the industrial real estate sector is well-positioned for sustained growth. Institutional investors continue to favor forward purchase structures like the one seen in the Bawla deal to secure scale and predictable yields in high-growth corridors.

Adani Ports Completes $495 Million Bond Buyback Including $196.94 Million in Early Tenders

Adani Ports and Special Economic Zone (APSEZ) has provided an update on its substantial capital management exercise, announcing the early results of its offshore bond buyback program. As of the early tender deadline on February 24, 2026, the company received valid tenders totaling $196.94 million. This figure represents approximately 40% of the maximum $495.1 million acceptance limit set for the repurchase. The participation rate varied significantly between the two targeted note series. The 3.10% Senior Notes due 2031 saw a stronger response with $95.36 million tendered, reaching 63.6% of its sub-limit. In contrast, the 4.0% Senior Notes due 2027 saw $101.58 million tendered, or 29.4% of its specific limit. The company is scheduled to proceed with early settlement on February 27, 2026. While early participation was lower than the total ceiling, the broader offer remains open until the final expiration date of March 11, 2026. APSEZ maintains the flexibility to adjust final acceptance amounts based on market conditions and its ongoing strategy to optimize its debt maturity profile. Complementing this international debt reduction, the company successfully raised 1,000 crore INR through the private placement of non-convertible debentures (NCDs) on February 23, 2026. These 5-year rated and secured notes will be listed on the BSE Wholesale Debt Market, providing long-term domestic funding to support the firm’s liquidity and expansion goals. Market performance for APSEZ remains resilient despite broader volatility. As of February 25, 2026, the stock closed at approximately 1,529 INR. The company’s market capitalization stands at roughly 3.52 trillion INR. Financial indicators remain robust, with a Return on Equity (ROE) of 18.8% and a trailing 12-month revenue growth of approximately 30%. Operationally, the firm continues to expand its global footprint, recently signing a strategic agreement with NMDC and Brazil’s Vale to develop iron ore facilities. APSEZ has also raised its FY26 EBITDA guidance to 22,800 crore INR, reflecting a positive outlook on cargo volume growth across its portfolio of 15 ports. Investors are monitoring the March 11 deadline closely, as the final buyback volume will signal the company's progress in reducing foreign currency debt and lowering future interest obligations. This multi-pronged financial strategy highlights a shift toward domestic capital markets while proactively managing high-value offshore liabilities.

Robert Arnott on the Inverse Relationship Between Investor Comfort and Profitability

Market Brief: Contrarian Strategy in a High-Value Era Real investment opportunity often thrives in the gap between market noise and fundamental data. As of February 2026, the S&P 500 is trading at a forward P/E ratio of **21.5**, significantly higher than the 10-year average of **18.8**. This suggests a landscape where optimism is high, making the search for value increasingly complex. Navigating this environment requires looking beyond comfort zones. While the broader indices remain resilient, sector performance reveals deep fragmentation. Software stocks, for instance, have plummeted **20%** year-to-date, hit by skepticism over the immediate returns of certain technology cycles. For the disciplined investor, such pessimistic sentiment often marks a potential entry point where valuations finally align with long-term reality. Key Performance Indicators Global markets are currently processing a shift from momentum-driven gains to earnings-driven performance. The S&P 500 closed recently near **6,890**, while in India, the Nifty 50 hovers around **25,482**. Despite these elevated levels, institutional selling has been noted, with foreign investors recording outflows of approximately **638 crore** in specific weekly sessions. Valuation remains the primary anchor for long-term success. Currently, **18 out of 20** major valuation metrics for the S&P 500 are considered statistically expensive. History shows that in years of double-digit earnings growth—projected at **14.4%** for 2026—multiple compression occurs **66%** of the time. This means stock prices may not rise as quickly as profits, demanding a more selective approach. Sentiment and Volatility Volatility, measured by the VIX, remains stable yet sensitive at around **13.5 to 14.4**. This range indicates a "low-hiring, low-firing" economic backdrop, where the U.S. Federal Reserve maintains rates between **3.5% and 3.75%**. In India, the RBI has signaled a prolonged pause on rates, keeping the repo rate steady while inflation is projected to settle near **2.1%** for the fiscal year. True profitability involves acting on these hard figures rather than popular narratives. While the "crowd" focuses on the next growth surge, contrarian opportunities are emerging in undervalued segments like European banks, which have seen massive gains over a five-year horizon, or the resurgence of metal and pharma sectors during recent sessions of high volatility. Successful investing in 2026 is defined by the ability to tolerate the discomfort of a "K-shaped" recovery. While specific megacaps dominate the headlines, the broader market's health is found in the rotation toward mid-sized companies and value-oriented assets. By prioritizing data over sentiment, investors can capitalize on the mispricing that uncertainty inevitably creates.

Poll Suggests Stable Outlook for Indian Equities Amid Geopolitical Factors

Indian equity markets are navigating a period of strategic consolidation as February 2026 comes to a close. While analysts have adjusted their short-term expectations, the broader outlook for mid-year remains focused on new record highs for benchmark indices. The NSE Nifty 50 recently stabilized around the **25,500** to **25,800** range, while the BSE Sensex has been trading between **82,600** and **83,700**. These levels reflect a recovery from volatility earlier in the year, supported by a significant shift in institutional participation. Institutional Flows and Market Drivers A notable trend this month is the return of Foreign Institutional Investors (FIIs) as net buyers, a reversal from the record outflows seen throughout 2025. On February 18, 2026, the Nifty 50 closed at **25,819.35**, bolstered by this renewed foreign interest and consistent support from Domestic Institutional Investors (DIIs). Domestic liquidity continues to serve as a bedrock for the market. DIIs have consistently offset foreign selling pressure, with net purchases often exceeding **₹3,000 crore** on high-volume trading days. This domestic resilience is largely powered by steady Systematic Investment Plan (SIP) inflows from retail investors. Sectoral Performance and Corporate Earnings The corporate earnings cycle for Q3 FY26 has shown a broadening recovery. Small-cap companies have emerged as the primary growth engines, posting a robust **22%** year-on-year earnings surge. This significantly outpaced large-cap growth, which stood at **14%**. * **Financials and Metals:** These sectors have led recent gains. Public sector banks and metal stocks like Tata Steel saw increases of up to **2.9%** in single sessions. * **Information Technology:** The IT index has faced headwinds, with some major names declining between **18%** and **26%** over the last month due to global tech shifts and AI-related disruption fears. * **Consumer and Manufacturing:** Auto OEMs and consumer durables are benefiting from a recovery in rural demand and recent GST rationalization. Monetary Policy and Macro Indicators The Reserve Bank of India (RBI) maintained the repo rate at **5.25%** during its February 2026 meeting. The central bank has adopted a neutral stance, supported by a benign inflation environment. Headline inflation is projected to remain near **2.1%** for the remainder of the fiscal year, well within the target comfort zone. GDP growth for FY26 is estimated at a resilient **7.4%**, positioning India as one of the fastest-growing major economies globally. Mid-Year Outlook Strategists anticipate a "business-cycle turn" as we approach the middle of 2026. While valuations for the Nifty 50 have corrected from a peak of **25x** to approximately **20x** forward earnings, the market is now moving toward a phase where returns are expected to track actual earnings growth rather than multiple expansion. The combination of a stable interest rate environment, cooling inflation, and a broadening earnings recovery suggests that the path of least resistance for the Indian benchmarks remains upward, despite the cautious tone in global markets.

Wednesday's Top Market Movers: Concord Biotech and IRFC Lead Gainers and Losers

The Indian equity markets experienced notable volatility during the February 25, 2026, session. While the **Nifty 50** managed to reclaim the **25,550** level with an intraday gain of **0.49%**, and the **Sensex** advanced over **230 points** to **82,455**, the session was defined by sharp price movements in specific mid-cap and sector-heavy stocks. High-Volume Gains and Sector Triggers **Concord Biotech** dominated market attention as its shares surged **14.39%** to close at **1,231**. This movement was supported by intense trading activity, reflecting strong investor interest in the biopharma firm's specialized fermentation-based API portfolio. **Schaeffler India** recorded a significant rally, climbing as much as **6.12%** to an intraday high of **4,334.70**. The surge followed the company's Q4 financial report, which highlighted a **32%** year-on-year increase in standalone net profit, reaching **327.96 crore**. Investors reacted positively to the firm's double-digit revenue growth and plans to increase capital expenditure in 2026. **Lloyds Metals and Energy** also saw positive momentum, trading near **1,251.80**. The company recently announced plans to increase capacity at its pellet plants in Konsari and reported a consolidated net profit of **10.47 billion** for the December quarter, underscoring strong operational performance in the metal sector. Major Decliners and Regulatory Headwinds **Waaree Energies** faced a severe sell-off, with shares plummeting as much as **15%** to settle near **2,708**. The sharp decline was triggered by the U.S. Department of Commerce's decision to impose preliminary countervailing duties of **126%** on solar imports from India. This regulatory move has raised concerns regarding the profitability of Indian solar module exporters. **Indian Railway Finance Corporation (IRFC)** shares fell by **4.46%** to close at **105**. The downward pressure came as the Indian government launched an Offer for Sale (OFS) to divest a **4%** stake in the entity. The floor price for the OFS was set at **104 per share**, aiming to raise approximately **5,430 crore**. **State Bank of India (SBI)** also traded in the red, declining nearly **1%** to **1,216.10**. Despite hitting a 52-week high of **1,234.70** in the previous session, the stock faced profit-booking as the broader banking index saw mixed results. SBI continues to maintain a dominant market cap of over **11 lakh crore** while focusing on a goal to increase its green advances to **10%** by 2030.

Union Bank of India and Five Other Financial Services Stocks Reach 52-Week Highs

Equity markets reached new heights this week as a series of positive economic reports and significant tech expansions fueled investor confidence. The Dow Jones Industrial Average climbed **370.44 points**, closing at **49,174.50**, while the tech-heavy Nasdaq Composite rose **1.1%** to finish at **22,863.68**. The S&P 500 followed suit, gaining **0.8%** to settle at **6,890.07**. Corporate growth in the artificial intelligence sector remains a primary driver for these benchmarks. Major software and workplace platforms reported gains between **2.6%** and **4.1%** following the release of new enterprise-grade integrations. While most sectors participated in the rally, health care lagged slightly, declining **0.6%**. Market volatility, as measured by the VIX, dropped by **7%** to **19.55**, reflecting a temporary easing of investor anxiety. However, the S&P 500 continues to trade at a high valuation, with its CAPE ratio exceeding **40**, a level that historically signals potential long-term cooling. Treasury Yields and Federal Reserve Outlook The yield on the US 10-year Treasury note rose to **4.06%**, rebounding from three-month lows. This shift comes as the White House began implementing a **10%** global tariff on all imports. While the rate was lower than some feared, it has led to a re-evaluation of the Federal Reserve’s path. Money markets have significantly scaled back expectations for rate cuts. The probability of a reduction by June has fallen to **50%**, and previous forecasts for a third cut by the end of **2026** have largely disappeared. Current economic indicators show an unemployment rate of **4.3%** and inflation holding at **2.4%** for the start of the year. Commodities and Energy Energy markets experienced minor fluctuations following a massive surge in US crude inventories. Stocks rose by **16 million barrels**, far exceeding the expected **1.5 million** barrel increase. Consequently, Brent futures settled at **$70.65** per barrel, while West Texas Intermediate (WTI) held at **$65.37**. Precious metals continue to serve as a primary hedge against trade uncertainty. Gold prices rose **0.5%** to **$5,175** per ounce. Institutional forecasts have grown increasingly bullish, with some major banks projecting gold to reach **$6,300** by the end of **2026** due to persistent inflation risks. Cryptocurrency Trends Bitcoin has shown signs of recovery, rallying above the **$66,000** mark. This move follows a period where its correlation with traditional stocks and gold was at its weakest since **2022**. Institutional interest remains robust, evidenced by **$258 million** in net inflows into Bitcoin ETFs during the most recent tracking period. The Coinbase Premium Index has turned positive for the first time since mid-January, suggesting that US-based buyers are returning to the market. Analysts suggest that if Bitcoin returns to its historical pattern of tracking equities during this economic expansion, there may be significant room for upward adjustment.

Vedanta to Raise Rs 3,000 Crore Through Bond Issuance

Vedanta Limited is moving to strengthen its liquidity with a planned 30 billion rupee ($329.89 million) bond sale. This move, finalized on February 25, 2026, marks the conglomerate's second major debt issuance for the current fiscal year. The company is targeting shorter-duration instruments, specifically two-year and three-year non-convertible debentures (NCDs). Market sources indicate that Vedanta has already entered discussions with institutional investors, including mutual funds, to complete the round in the first half of March. The fundraise comes on the heels of a record-breaking performance. For the December 2025 quarter, Vedanta reported a 60% surge in consolidated profit, reaching 78.07 billion rupees. Revenue climbed 19% to 458.99 billion rupees, driven by record production in its aluminium and zinc segments. Operationally, the company is maintaining strong efficiency. Its EBITDA margin expanded to 41% during the last quarter, while its net debt-to-EBITDA ratio improved from 1.40x to 1.23x. This deleveraging trend has contributed to a 77% rally in its share price over the past 12 months. The timing of this bond sale is critical as Vedanta nears its massive corporate restructuring. The group is on track to demerge into five separate listed entities—aluminium, oil and gas, power, steel, and base metals—with a target completion date of March 31, 2026. This 30 billion rupee issuance provides essential capital as the firm prepares to list its four new units by mid-May. The move aligns with a broader strategy to manage upcoming debt maturities and lower blended funding costs, which currently hover around 10%. Investor sentiment remains largely positive following the board's approval of the NCDs. On the day of the announcement, Vedanta’s stock price jumped over 5% to reach 732 rupees, bringing its total market capitalization to approximately 2.83 trillion rupees.

Bagmane REIT Seeks $3.9 Billion Valuation in India IPO

Market Brief: Bagmane REIT Public Offering Bagmane Prime Office REIT, a Bengaluru-focused commercial real estate vehicle, is preparing to launch a significant **₹4,000 crore** Initial Public Offering (IPO). This move follows the filing of a Draft Red Herring Prospectus (DRHP) and indicates strong confidence in the Indian office sector despite a subdued start to the 2026 primary market. The proposed offering is structured to raise **₹3,000 crore** through a fresh issue of units, alongside an Offer for Sale (OFS) of **₹1,000 crore** by a selling unitholder. Blackstone, which holds a minority pre-IPO stake, remains a key institutional backer. Market reports suggest the REIT is targeting an overall valuation of approximately **$3.9 billion**. Portfolio and Performance The REIT’s portfolio is concentrated in Bengaluru’s high-growth micro-markets. As of mid-2025, the assets comprised six Grade A+ business parks covering **20.3 million square feet**. The operational stability of these assets is reflected in a committed occupancy rate of **97.9%**. Key portfolio metrics include: * **Gross Asset Value (GAV):** ₹38,790 crore. * **WALE:** A weighted average lease expiry of **7.3 years**. * **Mark-to-Market Potential:** An estimated **20.3%** upside on rentals for leases expiring through 2030. * **Projected Income:** Net Operating Income (NOI) is forecast at **₹2,670 crore** for FY2027. The tenant base is notably resilient, with roughly **99%** of gross contracted rentals sourced from multinational corporations and Global Capability Centres (GCCs). Strategic Use of Funds A substantial portion of the IPO proceeds is earmarked for strategic acquisitions to expand the leasable footprint. The REIT plans to deploy **₹1,775 crore** to acquire Luxor at Bagmane Capital Tech Park and **₹1,025 crore** to secure a **93% stake** in the entity owning Bagmane Rio Business Park. Following the listing, the REIT’s financial profile is expected to remain conservative. The Loan-to-Value (LTV) ratio is projected to decline to approximately **7%**, providing significant headroom below the regulatory cap of **49%**. Sector Trends The Indian REIT market is witnessing a shift toward scale and diversification. Market capitalization for the sector surpassed **₹1.6 lakh crore** in early 2026, driven by consistent distribution yields. For Q2 FY26, listed REITs are expected to distribute approximately **₹2,331 crore** to over **3.3 lakh unitholders**. Bengaluru continues to lead office supply in the Asia-Pacific region, with **12.1 million square feet** expected to come online in 2026. This supply is being met by robust demand, particularly as corporates enforce stricter office attendance mandates and global firms continue to view India as a primary talent hub for multi-functional growth.

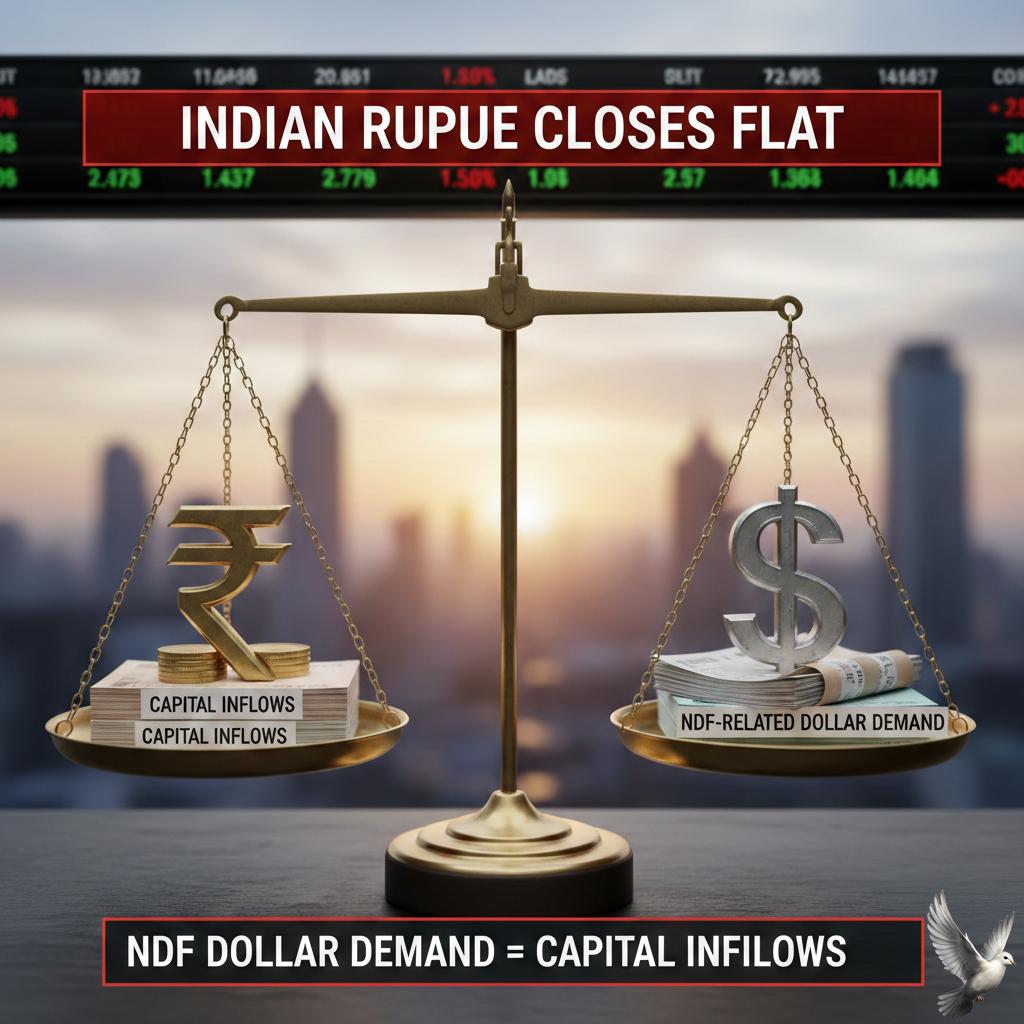

Indian Rupee Closes Flat as NDF-Related Dollar Demand Offsets Capital Inflows

Market Brief: India Markets & Rupee Performance The Indian Rupee remained virtually unchanged on February 25, 2026, closing at **90.96** against the U.S. Dollar. This follows a session of tight range-bound trading where the local unit hovered between **90.89** and **90.97**. Modest early gains were erased as a combination of rising global crude prices and maturity-linked dollar bids in the non-deliverable forward (NDF) market offset steady foreign fund inflows. The Reserve Bank of India (RBI) continues to maintain a strong presence in the currency market. Central bank intervention was visible near the **91.00** level, effectively preventing the rupee from sliding past this psychologically significant threshold. Market participants noted that the RBI’s active management in both spot and NDF markets has curtailed speculative short positions, keeping the currency stable despite global volatility. Key Market Indicators Domestic equity markets staged a notable recovery today, rebounding from previous losses. The BSE Sensex surged over **700 points** to reach an intraday high of **82,958**, while the NSE Nifty 50 reclaimed the **25,650** mark. This rally was largely driven by a **3%** bounce in the IT sector, which had recently faced a sharp correction of nearly **20%** over the past month. * **Sensex:** 82,958 (Intraday High) * **Nifty 50:** 25,650 (Level Reclaimed) * **10-Year G-Sec Yield:** 6.67% * **Brent Crude:** $71.74 per barrel Global oil benchmarks remain a primary concern for the rupee's trajectory. Brent crude futures rose above **$71**, driven by ongoing geopolitical tensions. While higher energy costs typically weigh on the rupee, recent Indo-US trade developments—including a reduction in effective tariffs on certain energy-related imports—have provided a crucial buffer for the domestic economy. Capital Flows and Monetary Policy A significant shift in investor sentiment is underway as Foreign Institutional Investors (FIIs) turned net buyers in February 2026, breaking a seven-month streak of selling. FIIs have injected approximately **₹1,370 crore** into the cash segment so far this month. Additionally, domestic institutional liquidity remains robust, with DIIs contributing over **₹3,161 crore** in recent sessions to support market depth. The monetary environment remains stable following the RBI’s decision to hold the repo rate at **5.25%** earlier this month. With headline CPI inflation projected at a benign **2.1%** for the current fiscal year and **2.75%** recorded in the latest January data, the central bank has maintained a neutral stance. This provides the RBI with the flexibility to prioritize growth, currently projected at **7.4%** for 25-26, while ensuring the rupee does not face disorderly drawdowns. Volatility remains elevated, with the India VIX rising nearly **40%** year-to-date. Traders are closely monitoring the upcoming **₹32,000-crore** government bond auction and global tariff headlines for further directional cues. For now, the combination of central bank vigilance and a resurgence in foreign buying is keeping the rupee anchored within the **90.70 to 91.20** range.

India’s Wealth Management Sector Forecast to Grow in High Teens Amid Surge in IPOs

India’s wealth management sector is undergoing a structural transformation, with the industry now positioned for high-teen growth over the next decade. This expansion is powered by a massive influx of liquidity from the primary markets and a rapidly maturing entrepreneurial ecosystem. **The IPO Wealth Engine** India's booming capital markets have become a primary driver of wealth creation. In 2025 alone, over **360 IPOs** hit the market, raising nearly **₹2 lakh crore**. A significant **₹80,000 crore** of this capital flowed directly into the hands of promoters via Offer For Sale routes. This surge in liquidity is creating a new class of "first-generation millionaires" who are recycling capital back into financial markets at record rates. **A Surging HNWI Landscape** The population of High-Net-Worth Individuals (HNWIs) in India grew by **5.6%** in 2024, reaching a total of **378,810**. Collectively, their wealth rose by **8.8%** to approximately **$1.5 trillion**. India now outpaces China in HNWI growth within the Asia-Pacific region, fueled by a strong equity market where the Sensex rose **8.2%** over the last year. **The Rise of Alternative Investments** Investment preferences are shifting away from traditional real estate and gold toward financial assets. Alternative Investment Funds (AIFs) have seen a remarkable **30% CAGR** in commitments between 2019 and 2025, reaching a total of **₹13.49 trillion**. Approximately **15%** of modern HNWI portfolios are now allocated to alternatives like private equity and private credit, with next-gen investors specifically seeking exposure to the startup ecosystem. **The Great Wealth Transfer** A significant generational shift is underway, with **50%** of Indian HNWIs expected to inherit wealth by 2030—a figure set to rise to **93%** by 2040. This younger cohort, **20%** of whom are currently under the age of 40, demands a different advisory model. Approximately **85%** of next-gen HNWIs indicate they may switch from their parents’ traditional firms in favor of digital-first, transparent, and global-facing platforms. **Digital Integration and Global Reach** While digital adoption is accelerating, human expertise remains central to the relationship. Investors are increasingly seeking holistic, institutional-grade advice rather than simple product distribution. Technology is being used to provide real-time portfolio visibility and data-backed insights, while human advisors focus on complex needs such as estate planning, tax efficiency, and global diversification. The market is moving from a product-selling era to an institutional advisory era. As domestic investors have poured over **$130 billion** into Indian companies over the last three years, the depth of the local market ensures that wealth management will remain a core pillar of India's long-term economic resilience.

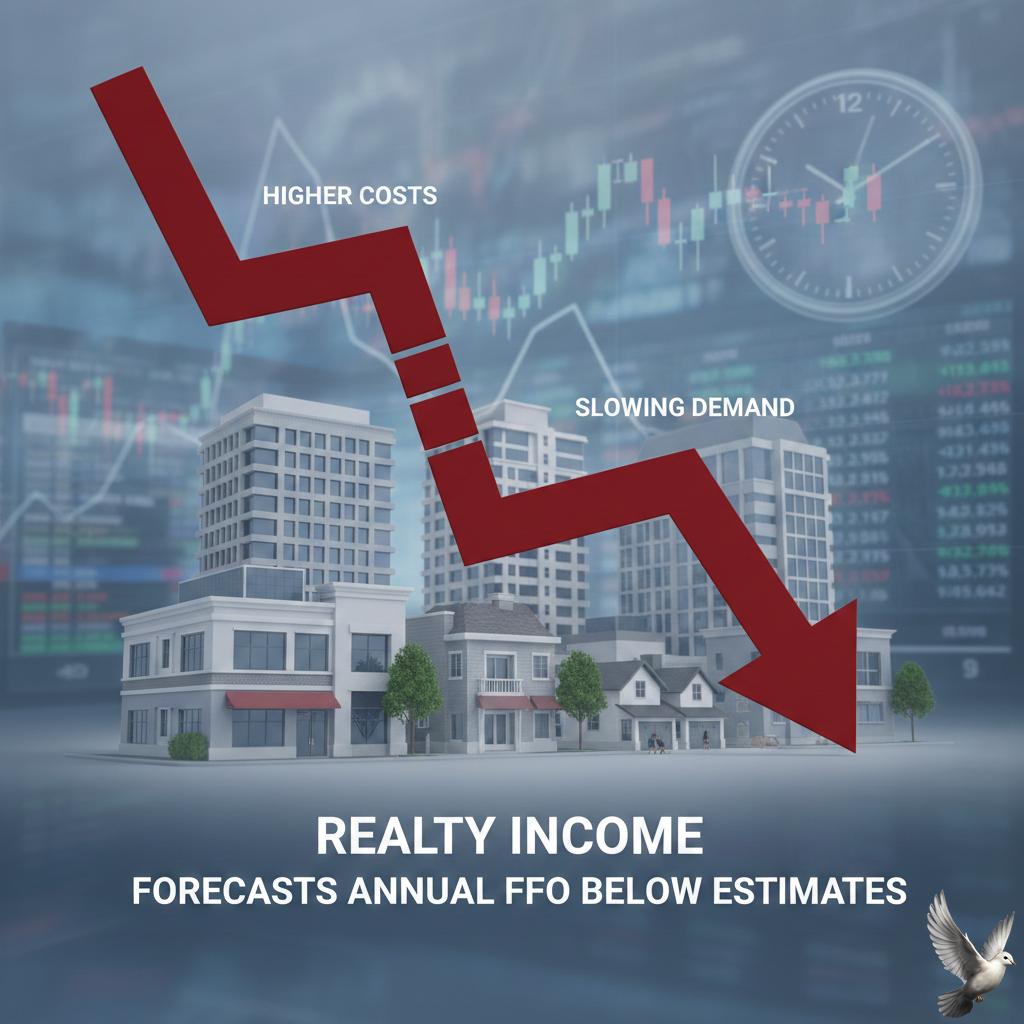

Realty Income Forecasts Annual FFO Below Estimates Amid Higher Costs and Slowing Demand

Realty Income issued its 2026 financial guidance this week, projecting annual adjusted funds from operations (AFFO) between **$4.38** and **$4.42** per share. The midpoint of **$4.40** falls slightly below the consensus Wall Street estimate of **$4.46**. Management attributed the cautious outlook to slowing tenant demand and rising property management costs. These factors are compounded by a macroeconomic environment marked by interest rate uncertainty and shifting retail trends. Operating metrics remain resilient despite the conservative forecast. The company reported a portfolio occupancy rate of **98.9%** as of late 2025. Same-store rental revenue is projected to grow between **1.0%** and **1.3%** in 2026, a slight deceleration from the **1.3%** growth seen in the prior year. The company is significantly scaling its acquisition strategy to drive future growth. Realty Income raised its 2026 investment volume guidance to **$8.0 billion**, up from **$6.3 billion** in 2025. This expansion includes a new **$1.5 billion** joint venture with GIC and an initial **$200 million** industrial investment in Mexico. Financial stability remains a priority, with the company maintaining **$4.1 billion** in liquidity. Recent capital activity includes an **$862.5 million** convertible note offering to fund the growing pipeline. The net debt to pro forma adjusted EBITDA ratio currently stands at **5.4x**. Dividend performance continues its historical trend. The company recently declared its **668th** consecutive monthly dividend. At a current share price of approximately **$66.50**, the annualized dividend yield is approximately **4.9%**. The stock has shown momentum in early 2026, rising roughly **10%** since the start of the year. While the 2026 guidance disappointed some analysts, the company's "offensive" investment stance suggests a focus on long-term scale and international diversification. Market sentiment is currently balanced, with a consensus "Hold" rating from major brokerages. Analysts have set average price targets near **$63.21**, reflecting the tension between strong portfolio quality and the rising costs of managing a global footprint of over **15,600** properties.

Indian Indices Close Flat as Banking Sector Gains Offset Broader Market Rally

Indian Equities Market Brief: February 25, 2026 Indian equity benchmarks, the **Sensex** and **Nifty 50**, demonstrated a significant intraday recovery during today’s session. The market rebounded from a sharp sell-off witnessed in the previous day, primarily supported by a surge in technology and metal stocks. Positive sentiment from global markets, particularly a tech-led rally on Wall Street, provided the necessary tailwinds for domestic indices to trade firmly in the green. By mid-session, the **S&P BSE Sensex** surged approximately **518 points**, reaching **82,744.85**. This follows a volatile start where the index had previously struggled to maintain its morning highs. The **Nifty 50** mirrored this upward trajectory, gaining **181.30 points** to trade above the **25,600** level. Market breadth remained decisively positive, with over **2,230 shares** advancing on the BSE against **1,567 declines**. The **IT sector** emerged as a primary driver of the recovery. After facing a nearly **21%** decline earlier this month due to structural concerns over technological disruption, the **Nifty IT index** climbed **2.5%** today. Major gainers included **Infosys**, **Tech Mahindra**, and **TCS**. This rebound was largely fueled by easing global fears regarding automation-led displacement in the outsourcing model. In contrast, **solar panel stocks** faced intense selling pressure, with some shares plunging by up to **14%**. This sharp decline follows the announcement of a **126% preliminary duty** imposed by the US on solar imports from India. **Waaree Energies** and **Premier Energies** both hit lower circuits of **10%** during the session. Broader market participation was healthy, with the **BSE MidCap** and **SmallCap** indices advancing **0.66%** and **0.54%** respectively. Institutional activity showed a clear divide: while **Foreign Portfolio Investors (FPIs)** remained cautious with minor net sales of **102.53 crore**, **Domestic Institutional Investors (DIIs)** provided strong support with net purchases exceeding **3,161 crore**. The **Indian Rupee** is currently trading near the **90.00** mark against the US dollar. Investors are now looking ahead to February 27, when the government is scheduled to release **Q3 FY26 GDP** figures. Early projections from the State Bank of India suggest a growth rate of approximately **8.1%**, supported by resilient domestic demand and urban consumption. On the corporate front, **Omnitech Engineering** saw strong interest in its IPO, while **Hindalco Industries** announced a **200 million dollar** investment into its subsidiary, **Novelis Inc**. These events, coupled with the ongoing **Nifty index rebalancing**, continue to drive stock-specific action across the capital goods and automotive sectors.

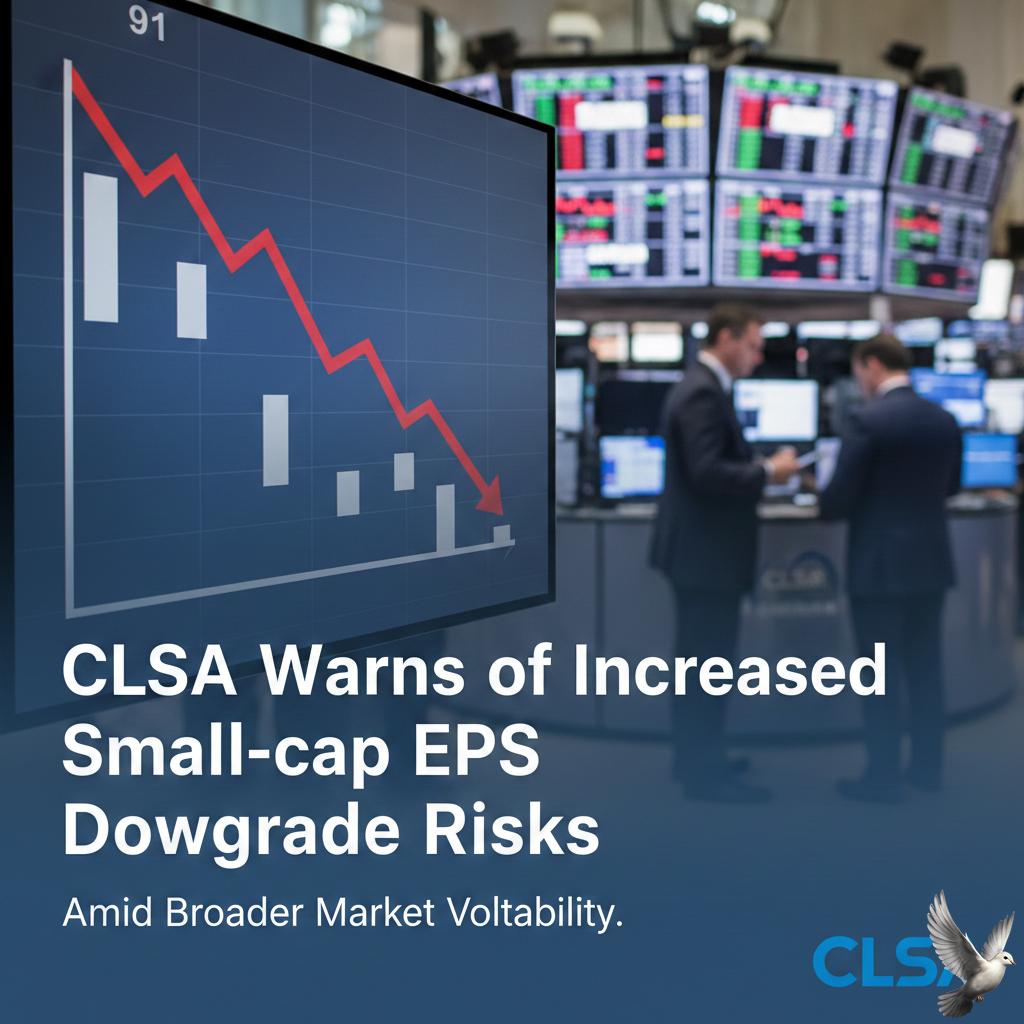

CLSA Warns of Increased Small-cap EPS Downgrade Risks Amid Broader Market Volatility

Market dynamics for early 2026 indicate a cautious shift in investment preference toward established large-cap stocks. International brokerage CLSA has reinforced its stance favoring large caps, citing more attractive relative valuations following a year of underperformance in 2025. The Nifty 50 is expected to deliver high single-digit gains in a best-case scenario for the year. This modest outlook stems from lofty valuation premiums, with the index trading at approximately 20.5x 12-month forward earnings. Analysts anticipate further earnings per share (EPS) downgrades for the small-cap segment. Small-cap valuations remain stretched due to aggressive earnings expectations that are prone to misses. In 2025, the Nifty Smallcap 100 plunged by 13.4%, signaling a correction that may persist as fundraising activities limit secondary market inflows. Sectoral performance highlights a focus on consumption, information technology, and rate-sensitive plays. Banks are projected to lead the Nifty's profit growth, with consensus forecasts exceeding 15%. Metals and telecommunications are also expected to be primary contributors to earnings momentum. Information technology remains a key area of interest. CLSA recently assigned an "Outperform" rating to Tata Consultancy Services (TCS), projecting a potential upside of 39% from current levels. The brokerage notes that while near-term sentiment is cautious due to global macro headwinds, large IT firms are well-positioned for AI-led transformation. Energy markets are shifting focus toward upstream companies. Projections suggest crude oil prices may recover toward $70 per barrel or higher throughout 2026. This trend favors companies involved in exploration and production over downstream oil marketing firms. The broader market environment is characterized by a "de-rating" phase. This means returns may lag behind actual earnings growth as valuations compress to more sustainable levels. Investors are increasingly prioritizing quality and balance sheet strength over speculative growth. Monetary policy is expected to be relatively quiet following a likely final interest rate cut by the Reserve Bank of India (RBI) early in 2026. This stability, combined with potential trade deals with the USA and EU, provides a backdrop for bottom-up stock selection rather than broad market rallies.

CLSA Sets Rs 3,593 Target Price for TCS, Citing Potential for Share Buyback and Rs 35 Dividend

Tata Consultancy Services (TCS) continues to navigate a volatile landscape as the Nifty IT index experiences its sharpest monthly decline since the 2008 financial crisis, plunging nearly 21% in February 2026. Despite this sector-wide correction, brokerage firm CLSA has reiterated an Outperform rating on the IT bellwether with a target price of 3,593 INR. The current market price of TCS stands around 2,574 INR, which reflects a 19% year-to-date decline and places the stock near its 52-week low. The brokerage’s target implies a substantial 39% upside, supported by the company’s strong cash flow and strategic pivot toward AI-native services. Dividend and Buyback Outlook TCS remains a top pick for income-focused investors, maintaining a high dividend yield of approximately 4.76%. For the upcoming Q4, analysts anticipate a potential dividend of 35 INR per share. This follows a significant Q3 payout of 57 INR, which included a special dividend of 46 INR. Furthermore, there is growing speculation regarding a potential share buyback in the coming quarters, fueled by recent tax-friendly budget changes. Operational Performance and AI Integration Financial results for Q3 FY26 showed resilient revenue growth of 5% year-on-year, reaching 67,087 crore INR. While consolidated net profit saw a 14% year-on-year dip to 10,657 crore INR, operating margins remained stable at 25.2%. A primary driver for future growth is the company's AI portfolio, which has already achieved an annualized revenue run rate of 1.8 billion USD. TCS is aggressively expanding its capabilities through partnerships with OpenAI and ServiceNow, focusing on transforming manual back-office functions into autonomous, AI-driven workflows. Sector Challenges and Risks The broader IT sector is currently facing an "AI scare trade." Concerns intensified this month after reports that advanced AI tools can now automate legacy code maintenance and legal functions, potentially threatening traditional billable-hour models. Global investors have responded by pulling over 10,956 crore INR from Indian IT stocks in early February alone. Key risks for TCS include persistent macroeconomic uncertainty in the U.S., potential tariff impacts, and currency fluctuations. Additionally, the Nifty IT index recently triggered a "Death Cross" technical pattern, suggesting that short-term sentiment remains bearish despite attractive long-term valuations. The sector is currently trading at a P/E ratio of roughly 22.1x, falling below its 10-year average.

European Equities Reach Record High as HSBC Increases Lending Targets and AI Concerns Moderate

European markets climbed to a fresh record high on Wednesday, February 25, 2026, as investor sentiment was bolstered by a powerful rebound in the banking sector and a significant cooling of fears regarding artificial intelligence. The pan-European STOXX 600 index rose 0.4% to reach 631.6 points, having touched an intraday all-time peak of 632.40 earlier in the session. This rally reflects a broader recovery in risk appetite as major indices across the continent tracked global gains. Financials led the charge following a standout performance from HSBC. Europe’s largest lender saw its shares jump after raising its profitability target to a return on tangible equity of 17% or better for the next three years. Despite a slight dip in reported annual profits to 29.9 billion dollars, the figure beat analyst expectations by approximately 1 billion dollars. The bank also signaled a strong outlook for 2026, forecasting net interest income of at least 45 billion dollars. This optimism rippled through the sector, with the UK’s FTSE 100 gaining 0.8% and the German DAX and French CAC 40 advancing roughly 0.3% each. The technology and services sectors found relief as immediate concerns over AI-driven disruption began to fade. After weeks of volatility fueled by fears that newer AI models would cannibalize traditional business models, investors have shifted toward a more balanced outlook. Market participants are increasingly viewing AI as a multi-year recalibration rather than an imminent threat to established firms. This shift was supported by recent corporate commentary suggesting that AI integration can enhance, rather than replace, core service offerings. Broader economic data also supported the upward trend. In the UK, inflation has slowed to 3.0%, the lowest level in nearly a year, fueling expectations that the Bank of England may begin cutting interest rates as early as March 2026. The market’s record-breaking performance comes despite lingering uncertainties in global trade. A recent reduction in proposed U.S. tariff levels—from 15% down to 10%—has provided additional breathing room for European exporters and cyclical stocks. Yields on the 10-year U.S. Treasury note edged up to 4.05%, while the euro remained steady against a slightly weaker dollar. Investors are now turning their attention to upcoming earnings from global tech leaders to confirm if the current momentum in the AI spending cycle can be sustained.

Prabhudas Lilladher Forecasts Nifty Reaching 28,000 by February 2027 Following Current Consolidation

Indian equity markets are navigating a strategic consolidation phase, with the Nifty 50 currently trading near the **25,450 – 25,550** range. Despite recent volatility and a modest **1.1%** dip in the previous session led by IT sector weakness, the underlying structural drivers remain robust. Domestic brokerage Prabhudas Lilladher maintains a bullish 12-month base-case target of **27,958** for the Nifty 50. This projection represents a potential upside of approximately **10%** from current levels. In a more optimistic bull-case scenario, the index is seen reaching **30,497**, implying a nearly **20%** climb. The outlook is underpinned by several critical growth catalysts: **Economic Resilience** India’s real GDP is projected to grow by **6.9%** in 2026. This momentum is supported by a historic breakthrough in trade diplomacy, including the India-EU Free Trade Agreement and a revised US trade framework. The reduction in reciprocal tariffs from **25%** to **18%** is expected to add **20 basis points** to annual growth, benefiting sectors like textiles, gems, and auto components. **Earnings and Valuations** Corporate performance continues to show strength. Revenue for covered companies grew **9.9%** year-on-year, while profits rose by **16.7%**. Although near-term EPS growth is estimated at a measured **3.8%**, a strong medium-term trajectory with a **16.3% CAGR** is expected through 2028. The Nifty currently trades at **19.1x** one-year forward earnings, aligning with long-term historical averages. **Policy and Demand** Strong fiscal discipline, with a deficit target of **4.4%** for FY26, and recent household tax breaks are fueling domestic consumption. Private consumption is forecast to increase to **7.7%** this year. Additionally, a steady **9.1%** projected salary increase across India Inc. suggests sustained purchasing power. **Market Sentiment** Institutional support remains a vital shock absorber. While the IT index faced a **2.07%** weekly decline due to global tech uncertainty, sectors such as Banking and FMCG recorded gains of **1.64%** and **1.71%** respectively. The current market behavior is viewed as a "reset rather than a reversal." This period of range-bound trading is likely paving the way for a multi-year compounding cycle, supported by landmark trade deals, infrastructure spending, and resilient corporate balance sheets.

AI Concerns Impact Investor Sentiment Toward IT Stocks: Ayon Mukhopadhyay

Foreign Institutional Investors (FIIs) are maintaining a stance of cautious optimism toward Indian markets as of late February 2026. While the landscape remains volatile, sentiment is gradually shifting from the aggressive selling seen in previous quarters toward a more selective, wait-and-watch strategy. Recent data shows a mixed flow of capital. In the week ending February 13, 2026, foreign portfolio investors were net buyers with total inflows of 69.34 billion INR. This was largely driven by a strong appetite for debt instruments, which accounted for 51.39 billion INR. In contrast, equity flows remain fragmented. Primary markets are attracting steady interest, while the secondary market recently recorded modest outflows of 4.55 billion INR due to profit-taking. A significant pivot occurred in early February following a trade deal between India and the United States. The reduction of reciprocal tariffs from 25% to 18% sparked a major single-day rally, with FIIs pumping 54.26 billion INR into the cash market on February 3. This event pushed the BSE Sensex to an intraday peak of 85,871 and the Nifty 50 toward 26,341. However, recent sessions have introduced fresh headwinds. As of February 24, benchmark indices faced sharp selling pressure, with the Sensex closing at 82,225 and the Nifty at 25,424. This downturn was primarily triggered by a rout in the IT sector. New advancements in artificial intelligence and reports questioning the long-term viability of the labor-arbitrage model have caused the Nifty IT index to plunge over 20% in the last month. Despite these tech-driven concerns, institutional interest is concentrating in domestic cyclicals. The banking sector remains a primary focus, supported by resilient credit growth in the 13% to 15% range. Large-cap lenders are seeing a shift from retail-led expansion to corporate credit as industrial capital expenditure begins to materialize on balance sheets. Capex-driven industries and infrastructure also remain high-conviction themes. With government infrastructure spending projected at 15 to 25 trillion INR annually over the next five years, sectors like capital goods and metals are showing resilience. The Nifty Metal index reached fresh all-time highs in February, gaining 14.30% so far in 2026. Market stability is currently being anchored by Domestic Institutional Investors (DIIs). On sessions where FIIs offloaded stocks, such as the 102 million INR sale on February 24, DIIs acted as shock absorbers with purchases exceeding 3,161 million INR. Looking ahead, analysts expect FII participation to stabilize as earnings visibility improves. While many global funds remain technically underweight on India, the cooling of valuation premiums and the prospect of a 7.5% GDP growth rate for the coming fiscal year provide a constructive backdrop for long-term capital re-entry.

Shree Ram Twistex IPO Receives 12x Subscription with 17% Grey Market Premium on Final Day

Market Overview: Shree Ram Twistex IPO The initial public offering of Shree Ram Twistex Limited concluded on February 25, 2026, with overwhelming market participation. The textile manufacturer, specializing in high-quality cotton yarns, successfully navigated a competitive primary market environment to secure robust subscription levels across key investor categories. Final Subscription and Demand The Rs 110.24 crore issue was oversubscribed 12 times by the close of the final bidding day. Non-Institutional Investors led the charge with a subscription rate of 56.13 times their allotted quota. Retail individual investors also displayed significant appetite, oversubscribing their portion by 25.42 times. This strong turnout highlights positive sentiment for mid-sized manufacturing plays despite a relatively muted response from Qualified Institutional Buyers, who booked roughly 9% of their segment. Pricing and Valuation The IPO was structured as a 100% fresh issue of 1.06 crore equity shares. Priced in a band of Rs 95 to Rs 104 per share, the company achieved a pre-issue market capitalization of approximately Rs 416 crore. Market analysts noted that the valuation at the upper price band reflects a price-to-earnings ratio of nearly 30 times, aligning with growth expectations in the domestic textile sector. Grey Market and Listing Outlook Sentiment in the unofficial grey market surged during the bidding period. The Grey Market Premium jumped to 17.3%, translating to roughly Rs 18 per share over the issue price. Based on these trends, the stock is estimated to debut near Rs 122. Allotment of shares is expected to be finalized on February 26, 2026, with the official listing scheduled for March 2, 2026, on both the BSE and NSE. Strategic Use of Proceeds The capital raised will be directed toward critical operational upgrades and financial deleveraging. Key allocations include: - Rs 22.2 crore for a 6.1 MW solar power plant. - Rs 39 crore for a 4.2 MW wind power plant. - Rs 14.89 crore for the repayment of existing debt. - Rs 44 crore for meeting increased working capital needs. Operational and Financial Highlights The company reported a total income of Rs 256 crore for FY25, up from Rs 232 crore the previous year. Profit After Tax rose to Rs 8 crore, showing a steady upward trajectory. By transitioning to nearly 100% captive renewable energy, the company aims to reduce power costs—which currently average Rs 8.92 per unit—potentially expanding EBITDA margins by 200 to 300 basis points in the long term. Sector Context The Indian textile industry is projected to reach USD 350 billion by 2030. Shree Ram Twistex is positioning itself to capture this growth by diversifying its product portfolio into value-added yarns like Lycra-blended and Eli Twist varieties. While the company faces risks such as high customer concentration and raw cotton price volatility, its move toward green energy integration is viewed as a significant efficiency driver.

IT Sector Faces Headwinds as Energy and Banking PSUs Projected for 25–30% Growth: Gautam Shah

Market Brief: Structural Rotation and the IT Crisis The Indian IT sector is currently navigating its most severe downturn since the 2008 global financial crisis. As of late February 2026, the Nifty IT index has plummeted over 21% in a single month, erasing approximately 6.4 trillion INR in market capitalization. This aggressive sell-off has pushed the index to a 30-month low, with technical indicators like the RSI hovering in deep oversold territory between 16 and 23. Structural headwinds are the primary driver of this volatility. A recent surge in "agentic AI" and automated coding tools has triggered widespread fears that the traditional labor-arbitrage model is becoming obsolete. Reports of accelerating contract cancellations through 2027 have intensified the "falling knife" scenario for major players. Heavyweights like Infosys and Wipro have lost 20% to 24% of their value year-to-date, while mid-cap leaders like Coforge have seen declines exceeding 25%. Valuation risks remain a critical concern. Analysts warn that the historical 30x P/E multiples are no longer justifiable as marginal costs for AI-driven coding collapse toward the cost of electricity. While some experts predict the Nifty IT index could slide further toward the 26,000 level, the broader market is witnessing a massive "value rotation" away from expensive tech and into domestic cyclical sectors. The PSU banking sector has emerged as the primary beneficiary of this capital shift. The Nifty PSU Bank index hit record highs of 9,665 in February 2026, marking six consecutive months of growth. State-run lenders like SBI and PNB are trading near 52-week highs, supported by historic Q3 profits—with SBI reporting a standalone net profit of 21,028 crore INR—and multi-year low NPA ratios. Metals and energy are also showing significant upside momentum. The Nifty Metal index recently hit a fresh all-time high, recording gains of over 14% in early 2026. This strength is bolstered by global demand for base metals and a robust domestic infrastructure push. Similarly, the Nifty Energy index has advanced by over 2.4% recently, driven by strong performance in oil and power stocks amidst rising geopolitical tensions. The current market environment favors a concentrated approach on value-oriented sectors. While IT faces a fundamental reset of its business model, the "Goldilocks" scenario of strong domestic growth and improving asset quality continues to support the rally in banking, metals, and infrastructure-linked names. Investors are prioritizing clean balance sheets and reasonable valuations over high-growth tech narratives. The recent launch of the [Claude AI Security Tool](https://www.youtube.com/watch?v=AiqXTyoPB8s) has contributed to the heightened uncertainty and volatility currently surrounding the Indian IT sector's earnings outlook. This video provides a professional technical analysis and outlook for 2026, specifically discussing the sectors mentioned in the brief. http://googleusercontent.com/youtube_content/0

Nikkei Surges to Record High Following BOJ Board Nominations

Japan's equity markets reached a historic milestone on Wednesday as the Nikkei 225 share average surged to a fresh all-time record. The index jumped over 2.4% during the session, climbing past the 58,500 level to touch a peak of 58,888. This aggressive rally was fueled by a powerful rebound in global technology sentiment. Investors moved back into the sector following easing concerns over artificial intelligence disruptions and anticipation of upcoming major tech earnings. Key semiconductor and electronics players led the charge. Shares of Disco Corp surged 4.3%, while Tokyo Electron and Advantest saw gains of 2.4% and 1.9% respectively. Furukawa Electric also recorded a significant rise of 1.6% as tech demand remained robust. Beyond technology, broader market sentiment was bolstered by a significant shift in monetary policy expectations. The nomination of new central bank board members has signaled a potential "reflationist" tilt, suggesting a more cautious approach to future interest rate hikes. Concerns regarding an imminent policy tightening have waned following reports that Prime Minister Sanae Takaichi expressed reservations about rapid rate increases. This political backdrop contributed to a sharp weakening of the Yen, which traded near 155.78 against the US Dollar. A softer currency typically benefits Japan's large-scale exporters. Toyota Motor shares rose 2.2%, and other major exporters like Honda and Panasonic also saw increased buying interest. Despite regional trade tensions, including recent export restrictions from Beijing affecting 40 Japanese firms, the market remained resilient. Gains were widespread, with the broader Topix index also showing strength, though financial stocks faced some pressure. Mitsubishi UFJ Financial Group saw a decline of 1.8%, reflecting the market's reassessment of the interest rate path. While the Bank of Japan recently held its policy rate at 0.75%, the "wait-and-see" approach for the first half of 2026 has provided the liquidity and confidence needed for this record-breaking run. The market outlook remains focused on the balance between domestic wage growth and global tech demand. With core inflation slowing to a two-year low of 2.0% in January, the pressure for aggressive central bank intervention has eased, clearing the path for further equity expansion.