Bullish News

Collection

Waaree Energies Aims to Mitigate 126% Solar Import Duties via US Manufacturing Expansion

The United States has moved to impose aggressive preliminary countervailing duties on solar imports from India, Indonesia, and Laos. Announced by the Department of Commerce on February 24, 2026, the decision targets manufacturers accused of receiving unfair government subsidies that allow them to undercut American-made products. India faces a staggering general subsidy rate of 125.87%. Specific companies have been hit even harder; individual rates for Indonesian exporters range from 86% up to 143.3%, while products from Laos carry a duty of 80.67%. These levies are separate from the 10% baseline global tariffs recently introduced by the administration. The trade implications are massive. In 2024, solar imports from India alone reached 792.6 million USD, a nine-fold increase from 2022. Together, India, Indonesia, and Laos accounted for approximately 4.5 billion USD in solar shipments last year, representing nearly two-thirds of all U.S. solar imports in 2025. Industry giant Waaree Energies has seen immediate market volatility following the news, with shares dropping as much as 14.6%. The company is now pivoting toward local production to bypass these trade barriers. Waaree currently operates 2.6 GW of manufacturing capacity in the U.S. and is exploring further expansion to leverage incentives from the Inflation Reduction Act. Market analysts suggest these duties could make the U.S. market virtually inaccessible for many Asian exporters in the short term. While the move aims to protect domestic giants like First Solar and Qcells, it risks driving up installation costs for U.S. developers who rely on high-volume, low-cost imported panels. A final determination on these subsidy rates is expected by July 6, 2026. Simultaneously, the Department of Commerce is conducting an anti-dumping investigation into whether these same nations are selling solar cells below their cost of production. This dual-track legal pressure signals a permanent shift toward "America First" energy manufacturing.

ASX Hits Record High Amid Strong Earnings and Elevated Inflation Data

Australian shares have reached a historic milestone, with the S&P/ASX 200 index surging to a record high of 9,130.30 points. The market closed 1.2% higher at 9,128.30 points, marking its strongest single-session performance in two weeks. This rally was powered by a wave of exceptional corporate earnings that overshadowed mounting concerns regarding persistent inflation and higher interest rates. Woolworths emerged as a primary catalyst for the market's ascent. The retail giant’s shares jumped 13% to reach a 17-month high after reporting a first-half profit that exceeded market expectations. The company also upgraded its full-year guidance, driving the broader consumer staples sector to its best day in six years with a 5.7% gain. Technology and mining stocks provided additional momentum. WiseTech Global shares surged more than 10% following a robust revenue report and news of an efficiency-driven restructuring. In the resources sector, Fortescue led the charge with a 4.7% gain after announcing a 23% jump in half-year profits and record iron ore shipments. This performance pushed the materials index to its own record high, with BHP and Rio Tinto also recording gains of 2.8% and 2.4%, respectively. Economic data released simultaneously revealed that the Australian economy remains hotter than anticipated. The annual inflation rate rose to 3.8% in January, slightly above the forecast of 3.7%. Core inflation, as measured by the RBA’s trimmed mean, also edged up to 3.4%. This inflationary pressure has intensified expectations for further monetary tightening. Investors have increased the probability of a quarter-point rate hike in May to 80%. The Reserve Bank of Australia previously raised the cash rate to 3.85% earlier this month, and current projections suggest it could reach 4.10% by mid-year. Despite the prospect of higher borrowing costs, the equity market remains anchored by resilient corporate fundamentals and a tight labor market, where unemployment holds steady at 4.1%. Analysts have recently upgraded aggregate earnings-per-share forecasts for 2026 by roughly 2.2%, suggesting a constructive outlook for the medium term.

Angel One Scheduled to Implement 1:10 Stock Split on February 26

Angel One is moving forward with its first-ever 1:10 stock split, marking a significant milestone in its corporate history. The brokerage has officially designated February 26, 2026, as the record date. This move will transform each existing equity share with a face value of ₹10 into 10 new shares with a face value of ₹1 each. The primary objective is to boost market liquidity and make the stock more accessible to a broader retail investor base by lowering the entry price. The stock has recently experienced volatility, trading near ₹2,452.80 as of today. Intraday activity saw the share price fluctuate between a high of ₹2,504.50 and a low of ₹2,437.75. Currently, the company holds a market capitalization of approximately ₹22,299 crore with a price-to-earnings ratio of 29.06. Financial performance for the quarter ended December 31, 2025, showed a consolidated profit after tax of ₹269 crore. While this represents a 4.5% year-on-year decline, total income grew to ₹1,338 crore. Operating expenses for the period rose to ₹964.2 crore, largely driven by higher employee benefit costs and operational spends. Operational metrics remain robust as the firm continues to lead the listed retail brokerage space. The client base has expanded significantly, reaching 34.1 million by late 2025, a growth of 24% year-on-year. Furthermore, the company’s share in India’s total demat accounts now stands at roughly 16.5%. Despite a general trend of retail exits in the broader brokerage sector during early 2025, Angel One has maintained a steady market share in retail equity turnover at 20.5%. The average daily turnover for the F&O segment remains a core driver, recently reported at ₹34.98 trillion. Investors holding the stock on or before the February 26 record date will be eligible for the split. The additional shares are expected to be credited to demat accounts within two working days following the record date, at which point the stock will begin trading at its new adjusted price. [Angel One 1:10 Stock Split News](https://www.youtube.com/watch?v=5nu5v2vxQMI) This video provides further context on the recent trends affecting major Indian brokerages and the competitive landscape Angel One operates in ahead of its stock split. http://googleusercontent.com/youtube_content/0

Analysis of the Viral AI Industry Memo and its Impact on Financial Markets

Market sentiment has shifted dramatically following a viral 7,000-word analysis by Citrini Research founder James van Geelen. The report, titled The 2028 Global Intelligence Crisis, outlines a hypothetical scenario where artificial intelligence disrupts the global economy to an unprecedented degree. The immediate reaction on Wall Street was a sharp selloff. The S&P 500 fell more than 1% in a single session, while the Nasdaq Composite dropped 1.1%. Software stocks bore the brunt of the volatility, with a major sector ETF tumbling over 4%. This "scare trade" suggests that investors are increasingly sensitive to the long-term structural risks posed by rapid AI adoption. The essay describes an "intelligence displacement spiral." It suggests that as AI becomes capable of executing complex business tasks, it could hollow out the white-collar workforce. The report projects a potential unemployment rate exceeding 10% by 2028. This loss of human income leads to what Van Geelen calls "Ghost GDP"—a situation where corporate productivity rises due to automation, but consumer demand collapses because machines do not buy goods or services. Market data reflects these growing anxieties. While big tech firms reported high revenue growth of 9% for the previous quarter, analysts are now forecasting a slowdown. Estimated revenue growth for 2026 has been adjusted downward to 8.7% for the first quarter and as low as 7.3% by the third quarter. The tech sector, which led the market for years, saw a 5% decline in early February 2026 as skepticism over return on investment intensified. The fallout is spreading beyond software into credit and housing markets. Private credit lenders, who financed many tech firms based on steady revenue projections, now face higher default risks if AI undercuts those business models. Additionally, if mass white-collar layoffs occur, the strain on mortgage payments could trigger a broader housing crisis. The Citrini report even speculates on a 57% crash in the S&P 500 by late 2027 if these trends accelerate. Current economic indicators provide a mixed picture. While national weekly wages grew by 7.5%, employment in AI-exposed sectors like computer systems design has already declined by 5%. This suggests that while top-tier talent is seeing higher pay, entry-level and mid-tier roles are being phased out. Investors are now rotating toward "safe-haven" assets. Gold and Treasuries have seen increased interest as the VIX volatility index rose 10.1% to reach 21.01. The market is no longer pricing in just the potential of AI, but the potential for a deflationary economic cascade that could redefine the global financial landscape.

Anthropic Valuation Surpasses Total Market Capitalization of Indian IT Sector

The global technology landscape has reached a historic pivot point as of February 2025. Anthropic, the San Francisco-based AI firm, has achieved a staggering post-money valuation of $380 billion following a massive $30 billion Series G funding round. This single private entity is now significantly more valuable than the combined market capitalization of India’s five largest IT services giants. The collective value of Tata Consultancy Services (TCS), Infosys, HCL Technologies, Wipro, and Tech Mahindra currently hovers around $240 billion to $250 billion. The valuation gap reflects a brutal structural shift. In February 2026 alone, the Nifty IT index in India plummeted by over 20%, marking its sharpest decline since the 2008 global financial crisis. This sell-off was triggered by the release of Anthropic’s "Claude Code" and "Claude Cowork" tools, which investors fear will dismantle the traditional labor-arbitrage model. Anthropic’s growth is explosive. The company’s annualized revenue run rate has surged to $14 billion, growing tenfold annually for three consecutive years. Its latest AI agents can now automate complex enterprise workflows, software modernization, and high-level coding—tasks that previously required thousands of human engineers at Indian IT firms. The market impact has been immediate and severe for legacy players. Stocks like TCS and Infosys have faced intense pressure as Anthropic demonstrated that AI can modernize COBOL-based systems—the backbone of global banking—faster and cheaper than manual teams. While the "Big 5" of Indian IT are witnessing billions in market value evaporate, Anthropic is preparing for a potential initial public offering in the second half of 2026. The company recently initiated a secondary share sale for employees at a $350 billion valuation to provide liquidity ahead of its listing. Despite the volatility, the Indian sector is attempting a pivot. Domestic IT spending is projected to reach $176 billion by 2026, with a heavy focus on AI-enabled software and data centers. However, the current "SaaSpocalypse" suggests that the premium once held by service providers is rapidly migrating toward frontier AI research labs. For the first time, a five-year-old AI startup has dwarfed an entire national industry that took four decades to build. The market has sent a clear message: innovation and agentic AI are now the primary drivers of technology valuations, overshadowing traditional scale and headcount.

Bitcoin and Ethereum Rise 3% Following Presidential State of the Union Address

Crypto Market Brief: February 25, 2026 Digital assets recorded a decisive recovery on Wednesday as market sentiment pivoted following high-profile political and economic updates. Bitcoin and Ethereum both surged by over **3%**, effectively reversing the downward pressure seen earlier in the week. This rebound was largely catalyzed by President Trump’s State of the Union address. Investors reacted positively to the administration's defense of its economic record and the signaling of policy continuity. The broader market viewed the remarks as a stabilizing force after a period of high volatility. Key Price Action and Valuation The global cryptocurrency market capitalization climbed to **$2.25 trillion**, a **3%** increase within a 24-hour window. This shift reflects a renewed appetite for risk assets as technical selling pressure began to ease. **Bitcoin (BTC)** climbed as high as **$66,300** during intraday trading, marking its most significant single-day gain since mid-February. The asset found strong support near the **$63,000** level before the leg up, though it continues to face technical resistance around the **$66,500** mark. **Ethereum (ETH)** followed a similar trajectory, rising nearly **4.8%** to reach approximately **$1,944**. The second-largest cryptocurrency found solid footing at the **$1,800** support zone, buoyed by the general recovery in the technology sector. Altcoin Performance and Sector Trends The rally extended beyond the two leaders, with major altcoins participating in the relief move. * **Solana (SOL)** outpaced many peers with a **6.7%** surge, climbing back above **$81**. * **XRP** and **Binance Coin (BNB)** saw gains ranging from **2%** to **3%**. * **XMR** and **LEO** also posted notable jumps, with some assets seeing double-digit percentage increases in volatile trading conditions. The market recovery coincided with a positive session on Wall Street. Cooling concerns regarding immediate trade tariff impacts—following recent Supreme Court rulings—helped steady the correlation between crypto assets and U.S. technology shares. Investor Sentiment and Outlook The "Fear & Greed Index" showed signs of moving out of extreme fear territory as bargain buying emerged. While long-term holders have been seen trimming positions at higher levels, smaller retail investors added approximately **31,000 BTC** during the recent dip. Current market dynamics suggest a shift from pure speculation toward utility-driven value. The integration of autonomous agents and on-chain government bonds remains a primary focus for institutional participants heading into the second quarter of the year. The immediate outlook remains tied to macro strength and institutional flows. Traders are currently monitoring for a potential short squeeze that could provide the momentum needed to test higher resistance levels.

Piyush Pandey Views IT Stocks as Buying Opportunity Amid AI Concerns

The Indian Information Technology sector has entered a definitive recovery phase in February 2026. While early 2025 was marked by geopolitical concerns and trade policy shifts, the current landscape reflects a transition from cautious experimentation to high-impact execution. Market analysts now view fears regarding AI-driven disruption as significantly overstated. Instead of replacing the traditional workforce, generative AI is serving as a catalyst for productivity. Industry leaders highlight that the fear of job losses is being replaced by the reality of "Human + AI" delivery teams. Over 2 million Indian IT professionals have already been upskilled in advanced AI domains. Valuations for major players have stabilized at attractive levels. Tata Consultancy Services (TCS) maintains a dominant market capitalization of approximately 11.64 trillion, while Infosys stands at 6.61 trillion. These figures are increasingly supported by fundamental earnings rather than speculative growth, with the Nifty 50 trading near its 5-year average price-to-earnings ratio of 20.5x. Sector performance in FY26 remains resilient, with total industry revenue projected to hit 315 billion, representing a 6.1% increase. While FY26 is characterized by cost discipline and a single-digit earnings growth environment, the outlook for FY27 is considerably more aggressive. Analysts predict double-digit earnings expansion as the industry fully adopts outcome-based project models. The structural shift toward outcome-led transformation is a key theme for 2026. Global clients are moving away from traditional time-and-material contracts in favor of strategic partnerships. These new agreements prioritize measurable ROI and specific business results, allowing Indian firms to capture higher margins through proprietary AI platforms. Investment in the sector remains robust, supported by a normalization of attrition rates to 16.4%. Domestic institutional flows continue to provide a floor for stock prices, with monthly SIP inflows reaching record highs of nearly 30,000 crore in late 2025. This domestic liquidity has helped the IT sector withstand the volatility of foreign institutional outflows. Global Capability Centers (GCCs) are emerging as a powerful growth engine within the ecosystem. These centers are projected to see salary increments of 10.4% in 2026, outperforming the broader tech industry’s 9.1% average. This trend underscores the growing sophistication of work being offshored to India, extending beyond maintenance into core R&D and semiconductor design. Looking toward FY27, the convergence of "Agentic AI" and intelligent operations is expected to drive a new cycle of growth. With corporate tax realizations rising and a disciplined fiscal deficit, the macroeconomic environment remains conducive for long-term equity accumulation in the technology space.

Indian Rupee Stabilizes Amid Weaker Dollar and Moderate Capital Inflows

Market Intelligence Brief: Rupee Resilience and IT Volatility The Indian rupee remains in a narrow trading band, holding near **90.96** against the U.S. dollar. Stability in the currency is currently being maintained by aggressive dollar sales from foreign banks and a slight softening of the greenback on the global stage. Despite persistent external pressures, the local unit has managed to avoid a deeper slip toward the **91.00** psychological floor. Tech Sector Correction and AI Disruption The domestic equity market is navigating a significant correction, particularly within the technology sector. The **Nifty IT index** has plunged approximately **21%** in February 2026, marking its most severe monthly decline since the **2008** financial crisis. This sell-off was accelerated by global concerns over artificial intelligence tools that automate legacy system updates. Major Indian players like **TCS** and **Infosys** recently touched **52-week lows**, with intraday drops exceeding **5%** in recent sessions. Investors are pivoting away from traditional software models as AI-driven automation raises questions about long-term profitability and service commoditization. Trade Policy and Global Uncertainty International markets are grappling with renewed trade friction following a **U.S. Supreme Court** ruling that struck down previous emergency tariffs. In a rapid response, the **Trump administration** announced a new **15%** temporary tariff on imports under Section 122 of the Trade Act of 1974. This move covers an estimated **$1.2 trillion** in annual imports. While the measure is slated for a **150-day** duration, it has triggered widespread unease among major trading partners, including India, South Korea, and the EU. The unpredictability of these unilateral measures continues to weigh on global supply chains and investor sentiment. Economic Indicators and Growth Outlook Despite the turbulence in tech stocks and trade policy, India's broader economic fundamentals show resilience. Real **GDP growth** for the third quarter is projected at **8.1%**, supported by robust domestic consumption and private investment. Inflation remains a bright spot, with recent figures showing a decade-low average of **1.7%** to **1.8%**. This cooling of prices has bolstered rural demand and allowed the **Reserve Bank of India** more flexibility, although the central bank remains cautious regarding the narrowing interest rate differential with the U.S. Federal Reserve. Key Market Levels to Watch * **USD/INR:** Immediate support is holding at **90.92**, with resistance near **91.10**. * **Nifty IT:** Technical analysts identify the next major support zone near **29,600**. * **Oil Prices:** Brent Crude is hovering around **$72 per barrel** as geopolitical tensions influence energy markets. The combination of strong domestic growth and significant disruption in the export-heavy IT sector is creating a divergent market landscape as the month concludes.

Indian Bond Prices Increase Amid Speculation of RBI Market Intervention

Indian government bonds are experiencing a notable upward trend, underpinned by a surge in demand and strategic liquidity management. The benchmark 10-year G-Sec yield recently eased to **6.68%**, a significant move from levels above **6.73%** seen earlier in February. This price appreciation reflects a shift in market sentiment as yields and bond prices move in opposite directions. A primary driver for this rally is the aggressive participation of the "others" investor category. This segment, which includes insurance companies, pension funds, and provident funds, has been actively absorbing supply. Their long-term investment horizon provides a stable floor for prices, especially as they look to lock in yields before potential future rate cuts. Liquidity conditions in the banking system have turned favorable, currently maintaining a surplus of nearly **3 trillion INR**. The Reserve Bank of India has been instrumental in this shift, adopting a "proactive and pre-emptive" approach to liquidity management. By conducting bond buybacks and debt-switch operations—such as the recent buyback of **755 billion INR** in bonds maturing in 2027—the central bank is effectively reducing near-term redemption pressures. Monetary policy remains a key anchor for the debt market. In its February 2026 meeting, the RBI maintained the repo rate at **5.25%** with a neutral stance. While the rate was held steady, the decision followed a **25-basis point** cut in December 2025, signaling that the tightening cycle has peaked. Inflation remains well-contained at **2.75%**, comfortably within the target range, which further supports the bullish outlook for fixed-income assets. Global factors are also playing a decisive role. Indian sovereign bonds continue to benefit from their inclusion in major global indices, attracting steady passive inflows estimated at **2 billion to 3 billion USD** per month. Although Bloomberg recently deferred the inclusion of Indian bonds into its Global Aggregate Index, the market remains resilient, focusing on the strong domestic fundamentals and the anticipated inclusion in other diversified indices later this year. Looking ahead, the market anticipates the 10-year benchmark yield to trade within a range of **6.65% to 6.78%**. While heavy supply from state government auctions—totaling approximately **445 billion INR** this week—may cap sharp gains, the combination of healthy forex reserves at **723.8 billion USD** and consistent domestic institutional buying suggests a sustained positive trajectory for the bond market.

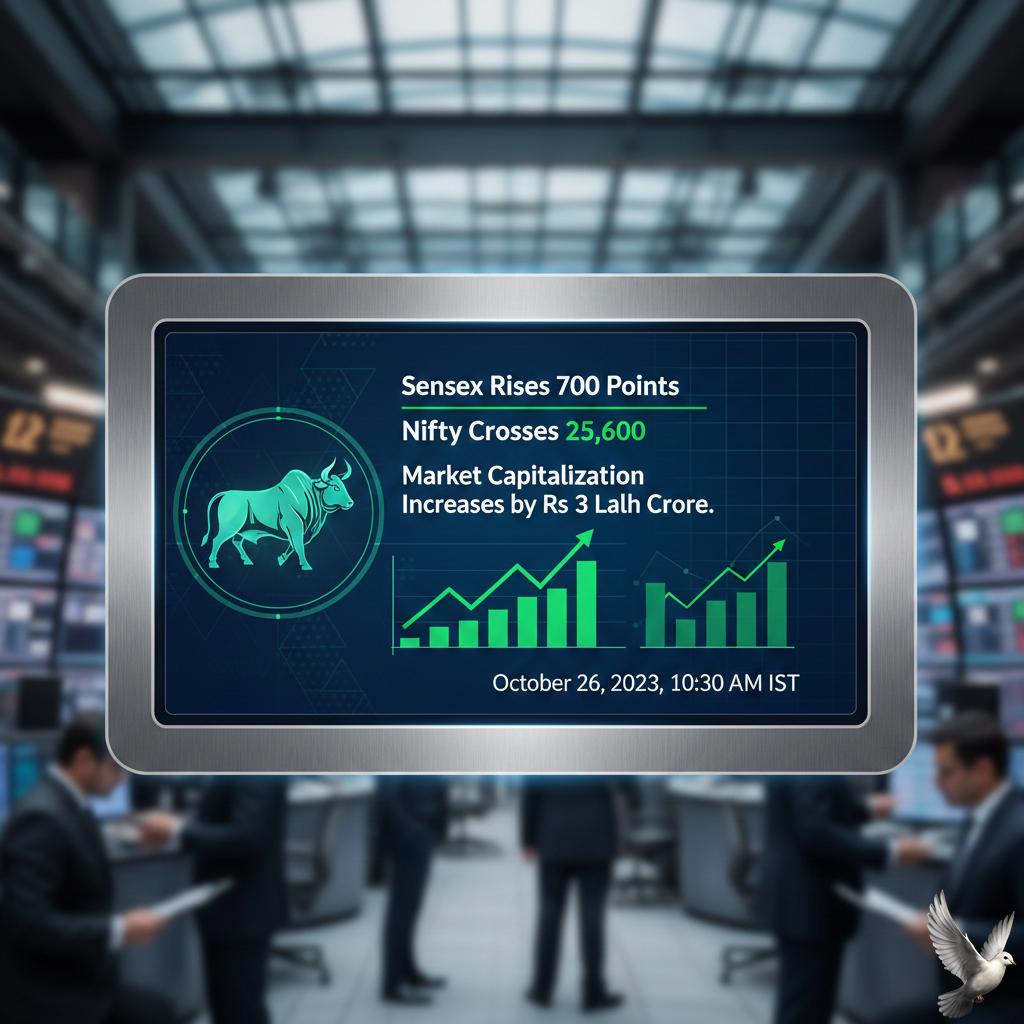

Sensex Rises 700 Points and Nifty Crosses 25,600 as Market Capitalization Increases by Rs 3 Lakh Crore

Market Pulse: Indian Equities Rebound Indian benchmark indices staged a robust recovery on Wednesday, February 25, 2026, effectively erasing a significant portion of the previous session's losses. The **BSE Sensex** surged by **587.33 points** or **0.71%** to reach **82,813.25**, while the **NSE Nifty 50** climbed **195.70 points** or **0.77%** to settle at **25,620.35**. This bounce-back followed a sharp decline on Tuesday where the Sensex had plummeted over **1,000 points**. The recovery added approximately **₹3 lakh crore** to the total market capitalization of BSE-listed firms, reflecting a swift return of investor confidence. Sectoral Performance and Drivers The rally was primarily driven by a resurgence in the **IT sector**, which snapped a five-day losing streak. The **Nifty IT index** jumped more than **2%**, tracking a tech-led recovery on Wall Street. * **Tech Mahindra** and **HCL Tech** led the gains, rising between **2.9%** and **3.5%**. * **TCS** and **Infosys** both advanced by approximately **2.5%** to **3.0%**. The **Metal sector** also showed significant strength, gaining over **2%**. **Tata Steel** was a standout performer, rising more than **3%**, while **Vedanta** saw a sharp increase of **5%**. Institutional Activity and Global Cues Market sentiment was bolstered by strong global cues as US and Asian markets traded higher. Concerns regarding AI-led disruptions in the software sector appeared to ease following new collaboration announcements between global AI firms and service providers. Domestic institutional dynamics played a crucial role. On the previous trading day, **Domestic Institutional Investors (DIIs)** were massive net buyers, injecting **₹3,161.22 crore** into the market. This helped offset the marginal selling by **Foreign Portfolio Investors (FPIs)**, who offloaded shares worth **₹102.53 crore**. Key Stock Movements While the broader market was painted green, some stock-specific volatility remained. * **Gainer Highlights:** **L&T Technology Services** surged over **5%**, and **Schaeffler India** jumped **6%** following positive corporate updates. * **Laggards:** **Indian Railway Finance Corporation (IRFC)** fell nearly **4%** after the government announced a stake sale via an Offer for Sale (OFS) with a floor price of **₹104**. * **Solar Sector:** Stocks like **Waaree Energies** and **Premier Energies** faced pressure, declining up to **10%** due to new US import duty developments. The Indian Rupee remained relatively stable, trading near the **90.87** mark against the US Dollar. In commodities, **Gold** was priced at approximately **₹1,61,790** per 10 grams as volatility in the dollar index influenced bullion prices.

Chakri Lokapriya Identifies Value in Cyclical and PSU Stocks Amid Market Volatility

**Market Brief: Selective Growth in Cyclical & State-Run Sectors** The Indian equity market continues to show a sharp divergence, with structural growth themes outperforming broader indices. While global uncertainty and tariff concerns remain, selective opportunities in **Railways, Defence, and PSU Banks** are attracting significant long-term capital due to record order books and improving return ratios. **PSU Banks: The ₹2 Lakh Crore Milestone** State-owned lenders are witnessing a historic rally fueled by a fundamental shift in asset quality and record earnings. * The **Nifty PSU Bank Index** hit a record high of **9,796.90** this week, gaining nearly **12%** in the last month alone. * Combined profits for PSU banks are projected to cross the **₹2,00,000 crore** mark for **FY26**. * **State Bank of India (SBI)** briefly crossed a **₹12 lakh crore** market cap, posting a record quarterly net profit of **₹21,028 crore**, a **24%** year-on-year increase. * Average Net NPAs across the sector have reached multi-year lows, supported by a healthy credit growth rate of **12%**. **Railways: A Multi-Year Capex Pipeline** The railway sector is transitioning from a "recovery" phase to a "structural growth" cycle, backed by massive government allocations. * The **Union Budget 2026** has allocated an estimated **₹2.75 to ₹2.8 trillion** for railway capital expenditure. * **Rail Vikas Nigam Limited (RVNL)** holds a staggering order book of **₹87,000 crore**, ensuring revenue visibility for the next three years. * The focus has shifted toward high-speed rolling stock and the **Kavach 4.0** safety mandate, benefiting manufacturers and infrastructure developers alike. * **Indian Railway Finance Corporation (IRFC)** is diversifying its portfolio, recently signing a major lease agreement with **NTPC** to fund power sector projects. **Defence: Indigenisation Driving Returns** Defence stocks have emerged as the top performers of early **2026**, with several names delivering returns between **30% and 68%** over the past year. * The **Ministry of Defence** is seeking a **20%** increase in the capital acquisition budget for **FY27**, the steepest single-year jump. * **Bharat Electronics Ltd (BEL)** and **Hindustan Aeronautics Ltd (HAL)** are primary beneficiaries of a **₹1.85 to ₹2.1 lakh crore** estimated capital pool for military modernization. * The domestic procurement threshold has crossed **65%**, reducing reliance on imports and creating a captive market for local firms. * Export targets remain ambitious, aiming for **₹50,000 crore** by **2028-29**, which is already reflected in the growing international orders for private players like **Solar Industries**. **Strategic Outlook** Market sentiment remains cautious toward the IT sector due to global shifts, leading to a rotation into domestic cyclical plays. Investors are prioritizing "execution over narrative," favoring companies with low debt and high dividend potential. Although short-term volatility persists, the visibility of government-backed contracts provides a strong cushion for those focused on the medium-to-long term.

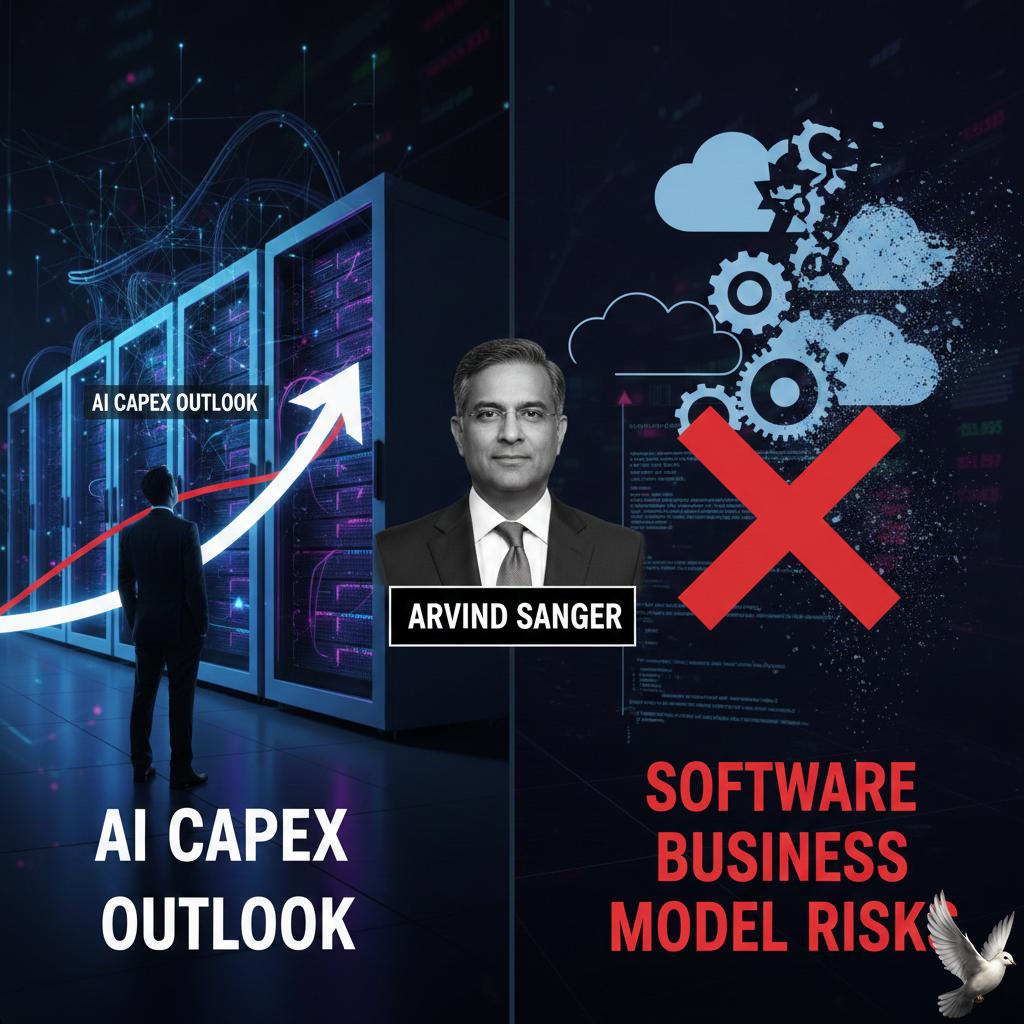

AI Capex Outlook and Software Business Model Risks: Arvind Sanger

The global technology landscape is undergoing a massive structural shift as artificial intelligence moves from the experimental phase to core industrialization. Spending on AI-related infrastructure and services is projected to reach **$1.5 trillion** in 2025, with major US hyperscalers—Alphabet, Amazon, Meta, and Microsoft—accounting for over **$320 billion** in capital expenditures this year alone. Estimates for 2026 suggest this combined investment could soar to **$650 billion**, reflecting a firm belief that AI represents a long-term value creation wave rather than a speculative bubble. This aggressive capital allocation is driving a divergence in the IT market. While overall global IT spending is expected to grow by nearly **8%** in 2025, the data center and AI-optimized server segments are expanding at double-digit rates, often tripling the growth of traditional hardware. However, this surge in infrastructure is creating immediate pressure on traditional software and IT services firms. For the Indian IT sector, the risk is centered on business model disruption rather than a lack of demand. High-manpower services, particularly application managed services which account for **22% to 45%** of revenue for major firms, are facing potential revenue deflation. Analysts warn that as AI coding agents and automation tools become more sophisticated, the traditional "per-hour" billing model is under threat. In worst-case scenarios, this could lead to a **14% to 16%** deflation in managed services revenue over the next few years. Market sentiment reflects these structural concerns. The Nifty IT index has seen sharp declines in early 2025, underperforming broader indices as foreign institutional investors reduced their exposure to legacy outsourcing models. Major players like TCS, Infosys, and HCLTech have seen valuation de-ratings, even as they pivot toward "AI-first" delivery models and outcome-based pricing. Despite the turbulence, there is a clear path toward renewal. India currently holds roughly **16%** of the global AI talent pool with over **600,000** professionals. Enterprises are shifting their focus to advisory and implementation engagements, where the demand for AI agents and agentic workflows is creating new high-value opportunities. By fiscal 2026, the Indian tech industry is still projected to cross the **$315 billion** revenue mark, driven by a rebound in discretionary spending and the industrial-scale integration of generative AI. The transition requires a complete overhaul of talent strategies. Firms are moving away from scale-led growth to value-led innovation, upskilling thousands of engineers in large language model deployment and prompt engineering. While the "managed services" segment may shrink, the rise of "consulting and AI-led transformation" is expected to define the next era of profitability, provided firms can successfully navigate the shift from labor-intensive work to intelligent, automated execution.

Mobilise App SME IPO: Subscription Status and GMP Trends

Mobilise App Lab Limited has successfully concluded its three-day bidding window for its 20.10 crore SME IPO, witnessing significant momentum on the final day of subscription. The issue, which was open from February 23 to February 25, 2026, closed with a total subscription of approximately 13 times. Demand was led by Non-Institutional Investors (NII) at 20 times and Retail Investors at 17 times, signaling strong confidence in the company’s SaaS-based business model. Shares were offered in a price band of 75 to 80 per share. With the upper price band fixed at 80, the Grey Market Premium (GMP) has been fluctuating between 8 and 16 per share. This suggests a potential listing price in the range of 88 to 96, representing a possible gain of up to 20% for successful allottees. The company operates a B2B Software-as-a-Service model, specializing in ERP platforms for education, healthcare, and supply chain management. Financial performance highlights a robust trajectory, with revenue growing from 12.06 crore in FY24 to 16.14 crore in FY25. Profitability remains a key highlight for investors. The firm reported a Profit After Tax (PAT) of 4.71 crore in FY25, maintaining a healthy net margin of 29%. For the nine months ending December 2025, the company has already clocked 4.01 crore in profit with an improved EBITDA margin of 48.34%. Proceeds from the 100% fresh issue will be strategically deployed to fuel future growth. Approximately 5.54 crore is earmarked for product development and talent acquisition, while 5.47 crore will fund infrastructure upgrades. Another 3.03 crore is set aside for business development and marketing. While the company shows strong growth, investors are tracking high revenue concentration, as the top 10 clients currently account for over 94% of total income. Additionally, a significant portion of business is currently localized within Maharashtra. The allotment of shares is expected to be finalized on February 26, 2026. Following the credit of shares to demat accounts, the company is scheduled to make its debut on the NSE Emerge platform on March 2, 2026. This listing comes at a time of high activity in the SME segment, with several other issues like Kiaasa Retail and Accord Transformer also competing for liquidity. Mobilise App Lab’s lean, debt-free balance sheet and scalable digital architecture position it as a notable player in the expanding Indian enterprise tech space.

South Korea’s Kospi Index Reaches Historic Highs Amid Market Outlook Uncertainty

South Korea's benchmark KOSPI index has entered a historic era, shattering the symbolic 6,000-point barrier for the first time on February 25, 2026. This milestone represents a staggering 40% gain since the beginning of the year, cementing Seoul’s position as one of the world's best-performing equity markets. The surge has pushed South Korea’s total market capitalization to approximately 3.76 trillion USD, allowing it to overtake France as the ninth-largest stock market globally. The rally is primarily fueled by the explosive growth in the semiconductor and artificial intelligence sectors. Market leaders Samsung Electronics and SK Hynix have both reached unprecedented price levels, with Samsung recently touching 200,000 KRW and SK Hynix vaulting over 1,000,000 KRW. Analysts have raised price targets further, with some projecting 300,000 KRW for Samsung as the memory boom coincides with massive AI-driven capital expenditures from global big tech firms. Beyond technology, the government's Corporate Value-up Program is fundamentally altering market dynamics. By incentivizing companies to address the "Korea Discount" through improved governance and higher shareholder returns, the initiative has led to a sharp rebound in dividend payout ratios, which recently climbed to 21.3%. Investors are increasingly rewarding firms that commit to share cancellations and capital efficiency, with high-yield indices and dedicated ETFs gaining significant traction. Economic indicators provide a stable backdrop for this momentum. The South Korean economy is projected to grow by 1.9% to 2.0% in 2026, supported by robust exports. Inflation has cooled to a five-month low of 2.0%, aligning with the central bank’s target and allowing the Bank of Korea to maintain a steady policy rate of 2.5%. While manufacturing growth has seen some deceleration, the service sector and consumption are showing gradual signs of improvement. Despite the optimism, the rapid ascent has triggered a parallel rise in cautious sentiment. The KOSPI 200 Volatility Index, often called the "fear index," has climbed for six consecutive sessions, reflecting unease over the pace of the rally. Short-selling reserve funds have hit a record 150 trillion KRW, signaling that a segment of the market is bracing for a potential correction. Institutional investors currently serve as the primary engine for the index's upward trajectory, often offsetting significant profit-taking by individual and foreign investors. While some analysts maintain a bullish outlook with targets as high as 8,000 points, others warn that the market is entering an overheated phase. This clash of perspectives has introduced heightened daily volatility, with the index frequently experiencing intraday swings exceeding 100 points.

Vedanta Shares Gain 5% Following BofA Upgrade to Buy and Increased Price Target

Vedanta Ltd shares traded with a bullish tone on Wednesday, February 25, 2026, gaining approximately 1.98% to reach levels around 709.20. The metal and mining giant continues to ride a wave of positive sentiment following a significant rating upgrade from BofA Securities. The brokerage shifted its stance from Neutral to Buy, nearly doubling its target price to 840 from a previous 480. This aggressive 75% increase in target value is anchored by a surging global outlook for aluminum and silver, which are central to the company’s revenue streams. Market dynamics currently favor the conglomerate as aluminum prices are forecasted to hit 3,000 USD per tonne by late 2026. This trend is driven by supply constraints and increasing production curbs. Similarly, silver is projected to maintain its strength, with price estimates hovering around 81 USD per ounce for the coming year. A standout feature for investors remains the company’s dividend profile. Analysts estimate a dividend yield exceeding 6% for FY27, positioning it as a top pick for yield-focused portfolios. This attractiveness is further bolstered by a massive 91% recovery in the stock price from its 52-week low of 362.20 recorded in April 2025. Operationally, the company is in the midst of a transformative phase. A strategic demerger is underway to split the business into five sector-specific listed entities, including dedicated units for Aluminum, Power, and Oil & Gas. This restructuring is aimed at unlocking shareholder value and providing direct exposure to specific commodity cycles. In the most recent financial results, the company reported a record-high consolidated profit of 7,807 crore, marking a 60% year-on-year increase. Quarterly revenue also hit an all-time high of 45,899 crore, supported by record production levels in the aluminum and zinc segments. Debt management remains a priority for the group. Recent fundraising plans through the issuance of non-convertible debentures are part of a routine refinancing strategy to lower borrowing costs. The current net debt to EBITDA ratio stands at a healthy 1.3x, reflecting improved financial stability. Promoter holding remains stable at approximately 56.4%, while foreign institutional investors have slightly increased their stake to over 12%. With technical momentum appearing moderately bullish, the stock is testing resistance levels near 713 and 727 as it approaches its recent all-time high of 770.

Strategies for Navigating Global Market Volatility: An Investor Perspective

The global financial landscape in February 2026 is defined by a "Great Rotation." Capital is aggressively migrating from mega-cap technology into the real economy. Investors are increasingly demanding immediate profitability over long-term AI speculation. The tech-heavy Nasdaq 100 has struggled as companies face an "AI ROI Reckoning." Massive capital expenditures, projected to reach a collective **$440 billion** for giants like Microsoft and Meta this year, are weighing heavily on margins. Consequently, the Dow Jones Industrial Average and the S&P 500 Equal Weight Index have recently touched new all-time highs. India: IT Correction and Banking Strength The Indian market reflects this global divergence. The Nifty IT index has experienced a sharp correction of nearly **30%** from its peak. This sell-off is driven by medium-term structural fears rather than immediate earnings misses. Estimates suggest Generative AI could disrupt **25% to 30%** of traditional software maintenance and testing work. In stark contrast, the banking sector remains a primary pillar of strength. The Bank Nifty recently surged to levels near **60,800**, outperforming broader benchmarks. Private and PSU lenders like SBI have seen double-digit weekly gains, supported by steady credit growth and healthy asset quality. Pharma: The GLP-1 Generics Wave A massive opportunity is emerging in the pharmaceutical sector. The patent for Semaglutide, the active ingredient in blockbuster weight-loss drugs, expires on **March 20, 2026**. This event is expected to trigger an aggressive price war in India. At least six major domestic players, including Sun Pharma and Dr. Reddy's, are preparing day-one launches. Market experts anticipate price cuts of up to **75%**, which could double the current **₹1,400 crore** market valuation within a year. Generic GLP-1 analogues are positioned to become a high-volume, global growth driver for Indian manufacturers. Real Assets and Cyclical Gains Industrials and metals are benefiting from a "return to reality" in valuations. Global copper prices have seen significant volatility, recently fluctuating around **$13,000 per ton** on the LME. In India, the Nifty Energy and Nifty Metal indices are providing a cushion against tech weakness. Defensive sectors like FMCG have also gained traction, with companies like Hindustan Unilever seeing steady inflows. * **Nifty IT:** Corrected approximately **15%** in the last month alone. * **Bank Nifty:** Gained over **1%** in recent sessions, leading the market recovery. * **Pharma:** Anticipated **60-70%** price drop in weight-loss generics post-March. The current regime change favors sectors with tangible assets and realized earnings. While IT valuations are becoming historically attractive, the immediate momentum rests with cyclicals, financials, and specialized healthcare players.

IIFL Capital: Airtel’s ₹14,000 Crore NBFC Investment Managed by ₹60,000 Crore FCF with Potential Dividend Upside

Bharti Airtel has officially launched a major expansion into India’s financial services sector, marking a strategic pivot toward high-margin digital lending. On February 13, 2026, the Reserve Bank of India granted an NBFC license to the company’s subsidiary, Airtel Money. This clears the path for a massive ₹20,000 crore capital infusion over the next few years. Airtel will hold a 70% stake in the new venture, with the promoter group, Bharti Enterprises, providing the remaining 30%. The company is not starting from scratch; it has already disbursed over ₹9,000 crore through its existing digital lending platform. By leveraging a team of 500 data scientists and a massive telecom subscriber base, the NBFC aims to bridge India's credit gap, where the formal credit-to-GDP ratio remains at just 53%. The core telecom business continues to show resilience. In the quarter ended December 2025, consolidated revenue reached ₹53,982 crore, a 19.6% increase year-on-year. While net profit moderated to ₹8,503 crore due to exceptional items and rising costs, the Average Revenue Per User (ARPU) climbed to ₹245. This financial strength is fueling a heavy capital expenditure cycle focused on two main pillars beyond mobile services. The first pillar is the "Nxtra" data center business. Airtel is targeting a massive 1 GW capacity within the next 3 to 4 years. This expansion is timed to benefit from a newly announced 20-year tax holiday for data centers in India. The second pillar is home broadband, which witnessed its highest-ever quarterly net additions of 2 million subscribers recently. The company now services over 13 million homes through its fiber and 5G Fixed Wireless Access (FWA) networks. Investors are rewarding this diversification. The stock has outperformed its peers with a 29% growth rate over the past four years, recently trading near the ₹1,940–₹2,000 range. With a market capitalization exceeding ₹11 trillion, the company maintains a healthy dividend payout ratio of approximately 38%. The strategy reflects a shift from a "minute factory" to a "money factory." By integrating credit products directly into the daily digital habits of its 577 million global customers, Airtel is building a defense against traditional lenders and new competitors like Jio Financial Services. While execution risks exist in the lending space, the company’s robust free cash flows and strengthened balance sheet provide a significant cushion for this ambitious growth phase.

IBM Stock Performance and Market Volatility Analysis

IBM shares experienced a historic 13.2% collapse on February 23, 2026, marking the steepest single-day decline for the technology giant since the year 2000. The sell-off erased approximately $31 billion in market capitalization in a single session, triggered by fears that rapid advancements in artificial intelligence are poised to dismantle the company’s high-margin legacy business. The primary catalyst for the crash was an announcement from AI startup Anthropic regarding its "Claude Code" tool. This platform claims the ability to automate the modernization of COBOL, the 60-year-old programming language that powers 95% of U.S. ATM transactions and 80% of in-person credit card swipes. Historically, updating these systems required massive teams of IBM consultants and years of manual labor. Anthropic suggests AI can now compress these multi-year projects into mere quarters. Market sentiment shifted instantly from viewing AI as a growth catalyst to recognizing it as a structural threat to traditional service models. Investors are concerned that if AI automates code analysis and migration, IBM’s lucrative consulting and mainframe maintenance revenue will face significant margin compression. The ripple effect was felt globally, dragging down major Indian IT firms by as much as 8% as the industry reassesses the value of labor-heavy outsourcing. Despite the volatility, IBM’s underlying fundamentals remain resilient. The company recently reported Q4 2025 revenue of $19.7 billion, a 12% year-over-year increase that exceeded analyst expectations. Its generative AI book of business has surged to over $12.5 billion, and infrastructure revenue grew by 21%, driven by strong adoption of the z17 mainframe cycle. CEO Arvind Krishna has labeled the stock’s plunge an "overreaction," citing $4.5 billion in internal productivity gains already achieved through AI. Analysts remain divided on the long-term impact. While some see a tactical entry point with a consensus price target of $314, others warn that the "moat" around legacy systems is thinning. IBM expects to generate more than 5% revenue growth and an additional $1 billion in free cash flow throughout 2026, relying on its watsonx platform to transition from a defender of legacy code to a leader in enterprise AI governance. The current market environment reflects a "tug-of-war" between structural bears and value-oriented bulls. With the stock down nearly 22% year-to-date, the focus has shifted to how quickly highly regulated sectors like banking and government will actually adopt unproven AI tools for mission-critical infrastructure. For now, the narrative of "efficiency gains" equaling "profit compression" dominates the ticker.

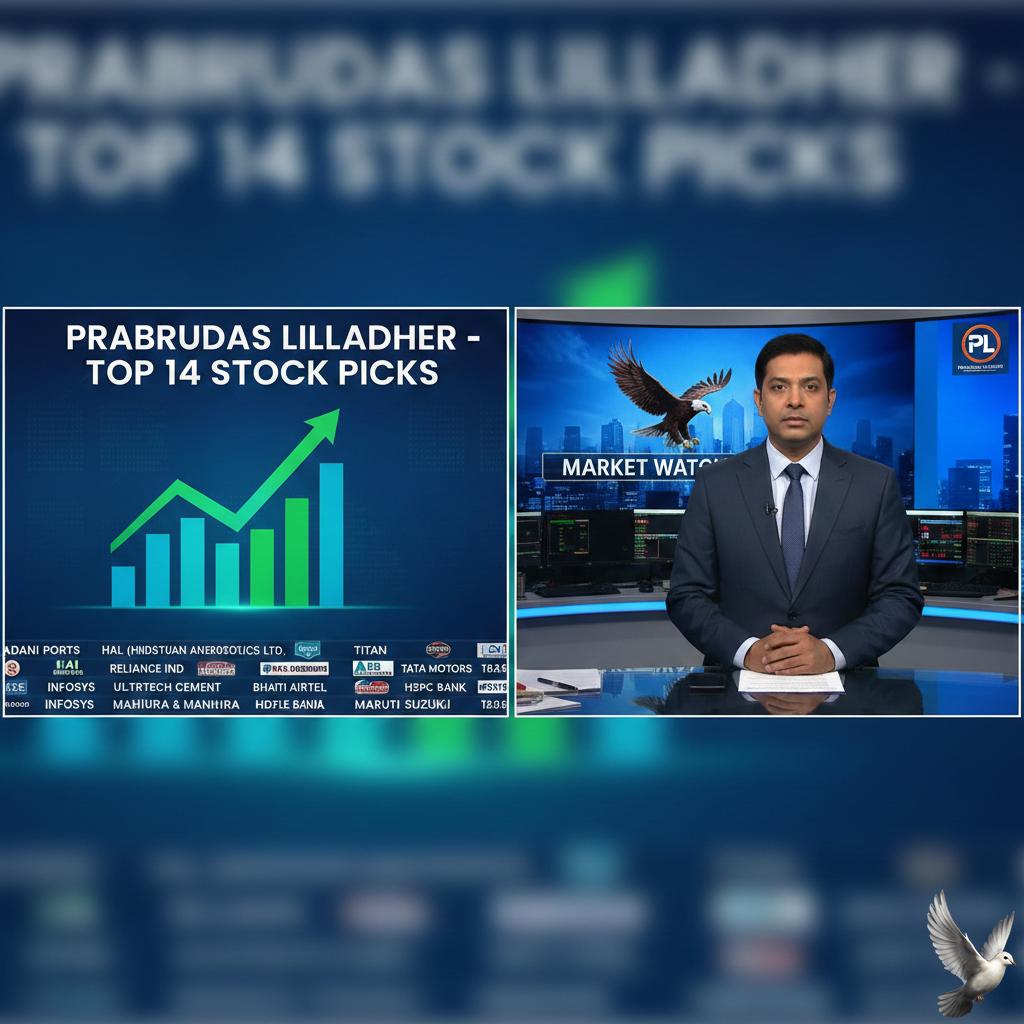

Prabhudas Lilladher Lists 14 Top Stock Picks Including Adani Ports, HAL, and Titan

Indian equity markets are showing resilience as of February 25, 2026, with the Nifty 50 rebounding above the 25,550 mark. This recovery follows a sharp 1% drop in the previous session driven by volatility in the technology sector. Prabhudas Lilladher (PL Capital) maintains a positive long-term outlook, identifying 14 top stock picks across large-cap and mid-cap segments. The brokerage has set a 12-month target for the Nifty 50 at 27,958, suggesting a potential upside of approximately 10% despite global geopolitical uncertainties. Adani Ports remains a structural favorite in the PL Capital model portfolio. Analysts have set a target price of 1,900 INR per share, representing a projected upside of over 22%. The firm views the company as a primary play on India’s rising global trade and infrastructure expansion. Hindustan Aeronautics (HAL) is highlighted as a top pick within the capital goods and defense sector. The brokerage remains overweight on this segment, citing strong domestic order pipelines. Similarly, Titan Company is backed with a "Buy" rating and an updated target price of 4,917 INR, driven by its strategic entry into the lab-grown diamond market and robust jewelry demand. The banking sector continues to be a core pillar of the recommended strategy. PL Capital remains bullish on State Bank of India (SBI), raising its target price to 1,200 INR following strong credit growth of 15.6%. Federal Bank also received a target upgrade to 275 INR, supported by improving asset quality and a healthy 3.18% net interest margin. In the industrial space, ABB India is positioned as a key beneficiary of the private capital expenditure revival. The firm has assigned an "Accumulate" rating to the stock with a revised price target of 6,319 INR. This outlook is supported by a significant 52% year-on-year growth in order inflows. Consumer-focused stocks like Britannia Industries are also seeing increased allocation. Analysts have maintained a "Buy" rating on the stock with a target of 6,972 INR, expecting a 14% upside. Current market sentiment is balanced by strong domestic institutional buying, which totaled over 3,161 crore INR in recent sessions. While technology stocks face pressure from shifting global service models, sectors like metals, financials, and capital goods are leading the current market recovery. Investors are keeping a close watch on the upcoming GDP data scheduled for release on February 27. The broader economy is expected to expand between 6.5% and 7.0% for the current financial year, providing a stable foundation for corporate earnings growth.

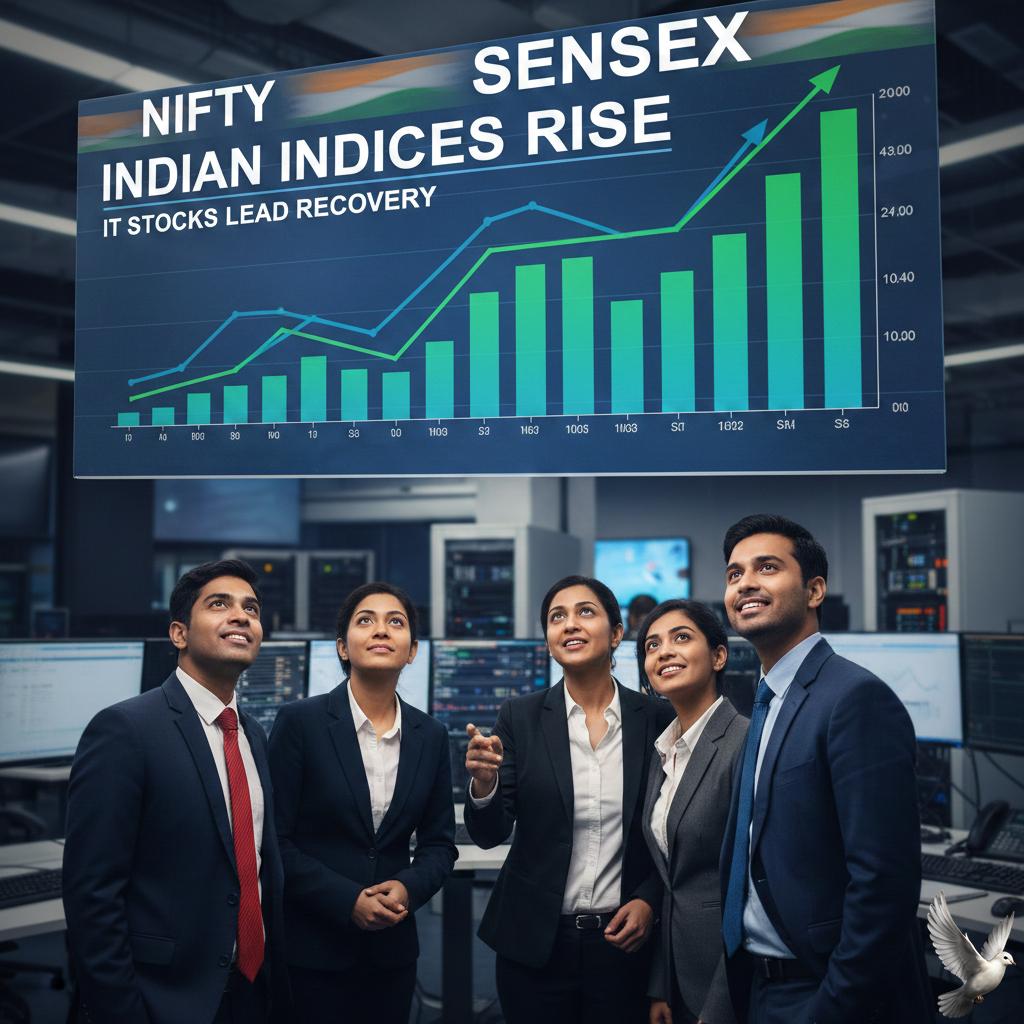

Indian Indices Rise Led by Recovery in IT Stocks

Indian Market Brief: February 25, 2026 Indian equity benchmarks staged a significant recovery on Wednesday, rebounding from a sharp selloff in the previous session. The recovery was driven by a strong bounce-back in technology shares and positive cues from global markets. **Market Performance Indices** The **BSE Sensex** surged by **515.93 points**, or **0.62%**, to reach **82,741.85** in early trade. Simultaneously, the **NSE Nifty 50** reclaimed the **25,550** level, advancing **146.40 points** (**0.58%**) to trade at **25,571.05**. This upward movement comes after a volatile Tuesday where the Sensex had plummeted over **1,000 points**. **Sectoral Leaders and Laggards** The **Nifty IT index** led the charge with a **2.5%** gain, as major players like **Tech Mahindra**, **HCL Technologies**, and **TCS** saw jumps of up to **3%**. This rally follows a period of intense pressure where some IT stocks corrected by **18% to 26%** over the past month. Metal and banking sectors also supported the rally. **Tata Steel** hit a new all-time high of **₹211.45**, outperforming its peers. However, the solar energy segment faced heavy headwinds, with companies like **Waaree Energies** and **Premier Energies** plunging up to **14%** following reports of high initial import duties from the US. **Institutional Activity** Market dynamics continue to be shaped by a "tug of war" between institutional players. On the previous trading day, **Foreign Institutional Investors (FIIs)** were net sellers, offloading shares worth **₹102.53 crore**. **Domestic Institutional Investors (DIIs)** provided a substantial cushion, acting as net buyers to the tune of **₹3,161.22 crore**. This domestic support remains a critical stabilizing factor for the Indian indices amidst global uncertainty. **Global Context and Commodities** US markets provided a supportive backdrop, with the **Dow Jones** rising **0.76%** and the **Nasdaq** climbing **1.04%** overnight. In Asia, Japan’s **Nikkei** and South Korea’s **KOSPI** both hit record highs, fueled by a rally in semiconductor stocks. Crude oil prices showed a slight upward trend as investors weighed supply risks against geopolitical developments. **WTI Crude** rose to approximately **$66.20 per barrel**, while **Brent Crude** traded near **$71.44**. Concerns remain focused on the **Strait of Hormuz**, a vital transit point for **20%** of global oil supply. **Currency and Outlook** The **Indian Rupee** remained nearly unchanged, opening at **90.93** per US dollar. While the immediate market sentiment has turned positive, analysts remain watchful of US trade policies and their impact on Indian exports, particularly in the renewable energy and technology sectors.