Bullish News

Collection

Ten Small-Cap Stocks Reporting Highest Year-on-Year Profit Growth for Q3

The Indian small-cap segment is demonstrating notable resilience as of February 2026, navigating a landscape of selective optimism. While the BSE Smallcap index recently experienced a 0.63% dip, the broader market sentiment is buoyed by a robust Q3 earnings season. Recent trade agreements with the US and EU have further stabilized global trade sentiment, turning Foreign Institutional Investors into net buyers in early February. Craftsman Automation has emerged as a standout performer in the automotive components space. For the quarter ended December 2025, the company reported a massive 728% year-on-year surge in consolidated net profit, reaching 107.11 crore. Revenue climbed 30.5% to hit a record 2,057 crore, driven by sustained demand in high-end manufacturing. Operating margins also saw a healthy expansion to 15.18%, signaling improved efficiency despite capital-intensive expansion phases. The logistics sector is witnessing a significant turnaround, led by Delhivery. The company reported a 59% jump in net profit to 40 crore for the December quarter, a sharp recovery from the 50 crore loss recorded in the previous period. Revenue from operations grew 18% to 2,805 crore, fueled by a record 500,000 metric tonne milestone in its Part Truck Load business. Operational leverage from the festive season helped expand operating margins by 481 basis points to 7.44%. In the specialty chemicals arena, Navin Fluorine International continues its aggressive growth trajectory. The company posted a 122% increase in net profit to 185.40 crore for Q3 FY26, significantly beating market estimates. Revenue rose 47% to 892 crore, with its high-performance products and specialty chemicals divisions growing 35% and 60% respectively. The commissioning of new hydrofluorocarbon capacity is expected to drive further volume gains through 2027. Broader economic indicators suggest a strengthening manufacturing core. India's manufacturing GVA growth reached 9.13% in the second quarter, and the Union Budget 2026-27 has introduced a 10,000 crore SME Growth Fund to support high-growth small-cap firms. While market breadth remains sensitive, with 387 stocks advancing against 813 declining in recent sessions, the fundamental strength of these sector leaders points to a decoupling of earnings performance from general market volatility. Investors are increasingly focusing on stock-specific fundamentals as valuation gaps narrow. Nearly a third of the small-cap universe, representing approximately 16 lakh crore in market capitalization, is currently viewed as trading at fair value. This environment favors companies with high capacity utilization and clear order visibility, particularly in the chemicals and auto-component sectors which are benefiting from global supply chain realignments.

LIC Rebalances Portfolio: Increases IT Holdings While Reducing Banking Exposure

Market Brief: LIC Contrarian Shift Life Insurance Corporation of India (LIC) has initiated a significant strategic pivot in its massive **₹17.83 lakh crore** equity portfolio. The state-owned insurer is moving against the prevailing market sentiment by aggressively increasing its stake in the information technology sector while trimming its long-held dominance in the banking space. As of February 2026, LIC has deployed approximately **₹3,136 crore** into Tata Consultancy Services (TCS) and **₹2,293 crore** into HCL Technologies. This move comes at a time when mutual funds and other domestic institutional investors have been net sellers in the IT segment, offloading nearly **₹2,000 crore** in various tech stocks during January alone. IT Sector: The Recovery Bet The insurer’s interest in IT is underpinned by a projected industry recovery. While growth had slowed to **4%–5%** annually in recent years, sector spending in India is now forecasted to hit **$176.3 billion** in 2026—a **10.6%** increase. The focus has shifted from traditional outsourcing to "AI-centric" engagements. Major firms report that nearly **74%** of recent contract wins involve generative or agentic AI. * **TCS:** Currently trading near **₹2,717**, reflecting a significant correction from its 52-week high of **₹3,934**. * **HCL Tech:** Trading around **₹1,461**, as the market prices in a **17.6%** projected rise in software spending for the upcoming year. Banking Sector: Exposure Reduction Simultaneously, LIC is reducing its exposure to banking heavyweights like SBI and HDFC Bank. This reduction coincides with a tightening regulatory environment. Starting April 2026, the Reserve Bank of India (RBI) is set to implement stricter liquidity norms and mandatory two-factor authentication for all digital payments. Banks are also facing a transition toward "agentic banking" and the integration of Central Bank Digital Currencies (CBDCs). While the Nifty Bank index saw a **9.1%** gain in the previous quarter, the sector is entering a high-compliance phase. This transition requires heavy capital investment in backend infrastructure to meet the March 2026 deadline for ring-fencing core operations. Strategic Rationale LIC’s portfolio includes **283** stocks, but the shift highlights a clear preference for "Quality" and "Value" themes. By buying IT leaders during a period of relative underperformance—with TCS and HCL Tech down between **18%** and **30%** from recent peaks—LIC is positioning itself for a long-term earnings revival. The move suggests a conviction that current AI-related market fears are a temporary valuation reset rather than a permanent erosion of the IT service model. Analysts estimate that large-cap IT stocks are now trading at roughly **18 times** estimated fiscal 2027 earnings, which LIC appears to view as a compelling entry point compared to the historically higher multiples in the banking sector.

Netweb Technologies Announces NVIDIA-Powered AI Supercomputing Systems Under ‘Make in India’ Initiative **

Netweb Technologies India Ltd (NETWEB) is under the spotlight following the high-impact launch of its "Make in India" AI supercomputing systems. The company has officially unveiled the Tyrone Camarero GB200 and the ultra-compact Tyrone Camarero Spark, marking a significant leap in domestic high-end computing. These systems are built on the NVIDIA Grace Blackwell platform, specifically the GB200 NVL4 architecture. This technology is engineered to handle massive AI workloads, including real-time inference for large language models with up to 10 trillion parameters. The launch positions Netweb as a primary provider of advanced AI infrastructure in India, bridging the gap between local manufacturing and global performance standards. The market response reflects the company’s strong fundamental growth. As of February 18, 2025, Netweb’s share price is trading around 3,098.80 INR, showing a modest intraday gain of 1.02%. The stock has demonstrated exceptional momentum over the past year, delivering a return of approximately 123.86%. With a market capitalization of roughly 17,647 crore INR, the firm continues to trade at a premium, with a P/E ratio exceeding 98. Netweb’s financial performance supports this valuation. In Q3 FY26, the company reported a record net profit of 73.31 crore INR, more than doubling its previous performance. Revenue growth remains robust, with the company targeting a 30% to 40% CAGR over the next several years. This growth is fueled by a healthy order book and the accelerating demand for data center capacity in India, which is expected to reach 1,800 MW by 2026. The Tyrone Camarero Spark is particularly noteworthy as one of the world’s smallest AI supercomputers. It delivers 1 petaflop of performance in a compact desktop form factor, consuming only 240 watts of power. This "supercomputer on a desk" is designed for the millions of AI developers in India, providing local access to the full NVIDIA AI software stack and 128GB of unified memory. India’s broader IT hardware market is valued at approximately 21.17 billion USD in 2025 and is projected to grow to over 31 billion USD by 2031. Government initiatives like the PLI 2.0 scheme are critical drivers, encouraging domestic players like Netweb to localize high-value assembly and R&D. By integrating the Grace Blackwell architecture, Netweb is not just selling hardware but is providing the "AI Factory" infrastructure required for agentic and physical AI. This strategic alignment with NVIDIA ensures that Indian enterprises have early access to liquid-cooled, energy-efficient systems capable of training the next generation of generative AI models.

**Zomato shares in focus following OpenAI partnership for AI integration across platforms**

Eternal Ltd (ETL) is making a decisive shift toward an AI-first commerce architecture, significantly expanding its strategic partnership with OpenAI. This collaboration aims to embed advanced generative AI at the core of its primary platforms, including food delivery giant Zomato, quick-commerce leader Blinkit, and its newest "Going-out" venture, District. The integration will leverage OpenAI’s Enterprise API to overhaul customer interactions and partner ecosystems. For merchants and delivery partners, Eternal is deploying AI-assisted workflows and contextual assistants to streamline high-volume operations. Internally, the company is testing the latest coding models, such as GPT-5.3-Codex, within its proprietary developer orchestration platform, Stitch, to automate complex software engineering tasks. **Financial Performance and Market Metrics** Eternal’s stock remains in a high-stakes spotlight following robust Q3 FY2026 earnings reported in late January. The company’s financial trajectory continues to show aggressive expansion: * **Consolidated Revenue:** Reported at **₹16,315 crore**, a massive **201.8%** year-on-year increase. * **Net Profit:** Surged by **72.8%** to reach **₹102 crore** for the December quarter. * **Stock Valuation:** Currently trading around **₹281.60**, the company holds a market capitalization of approximately **₹2.7 trillion**. * **Quick Commerce (Blinkit):** Revenue grew nearly **121%** year-on-year, with the segment now representing a significant portion of the group's total revenue mix. * **Food Delivery (Zomato):** Maintained steady growth with a **17%** rise in Net Order Value (NOV), reaching **₹9,846 crore**. **Strategic Impact and Forward Outlook** The partnership with OpenAI is designed to address the "execution gap" in scaling hyper-local delivery. By moving from a standard marketplace model to an AI-driven inventory-led structure, Eternal seeks to optimize its network of over **2,020 dark stores**. The goal is to drive operational efficiency in a market where 75% of urban Indian consumers now use delivery apps weekly. Investors are closely watching the impact of these AI tools on the company's high valuation. While revenue growth has been stellar, Eternal carries a Price-to-Earnings (P/E) ratio exceeding **1,100x**, signaling that the market has priced in near-perfect execution of these technological integrations. Beyond commercial interests, the AI rollout extends to social initiatives like Feeding India and the AI-native venture Nugget. Group CEO Albinder Dhindsa has emphasized that these tools are becoming foundational infrastructure, intended to improve data-driven decision-making across the entire ecosystem of restaurants, delivery partners, and consumers.

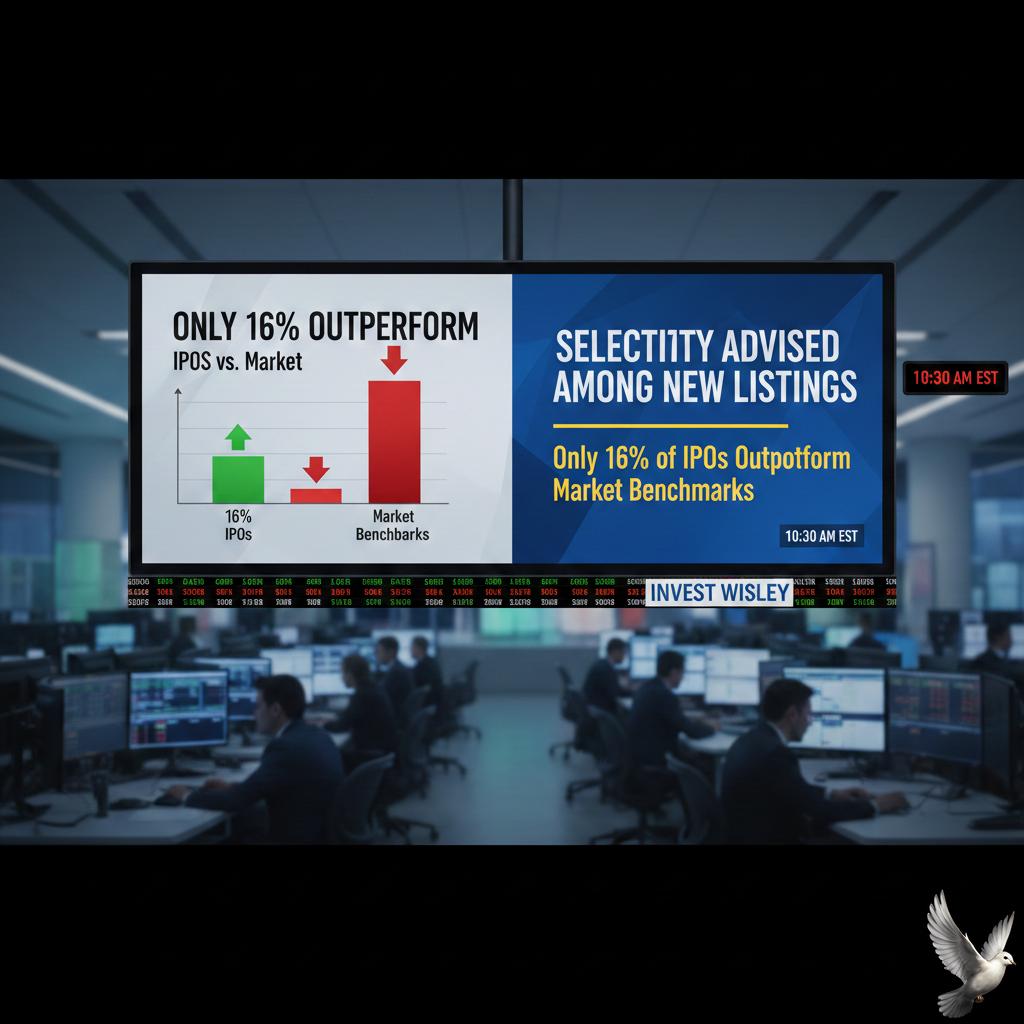

Only 16% of IPOs Outperform Market Benchmarks; Selectivity Advised Among New Listings

The Indian primary market is navigating a pivotal phase in early 2026. After a historic 2025 where 102 companies raised a record **₹1.75 lakh crore**, the momentum has transitioned into a massive but cautious pipeline. Currently, over 190 companies are in the queue, seeking to raise more than **₹2.5 lakh crore**. Despite this volume, the actual launch activity in January and February has been muted as issuers wait for secondary market stability. While the "IPO boom" headline remains attractive, long-term wealth creation data suggests a starkly different reality. Recent analysis reveals that only **16%** of IPOs have managed to outperform the broader market returns over the long term. Furthermore, approximately **50%** of the small-cap universe is currently trading nearly **40%** below their all-time highs. This underscores a significant gap between listing-day euphoria and sustainable shareholder value. Institutional dynamics are providing a unique floor to the current market. Foreign Institutional Investor (FII) ownership has seen periods of selling, with recent net outflows reaching **₹7,395 crore** on specific volatile days in February. However, Domestic Institutional Investors (DIIs) have acted as a consistent shock absorber, frequently recording net buys exceeding **₹5,500 crore** to stabilize the indices. Sectoral performance is diverging based on fundamental recovery rather than speculative heat. The IT sector is positioned for a sharp recovery in 2026, with spending in India projected to reach **$176.3 billion**, a **10.6%** increase from the previous year. This growth is largely driven by AI-centric contracts, which now form nearly **74%** of all new deals for major Indian tech firms. Consumption remains a key theme, though valuations in mid and small-cap segments continue to trigger red flags. The Nifty Smallcap index has faced recent pressure, dropping over **3%** year-to-date, compared to a milder **1.4%** decline in the Nifty 50. This correction is viewed by many as a necessary cooling phase following the multi-year rally that stretched valuation multiples. For the remainder of 2026, the focus is shifting from "liquidity-driven" to "earnings-driven" listings. Marquee names in fintech, consumer tech, and infrastructure are expected to headline the next wave of offerings. Investors are increasingly prioritizing companies with clear profitability pathways and transparent governance over those relying solely on future growth projections. Patience remains the primary tool for navigating this landscape. With the Nifty 50 hovering around the **25,700** level and the India VIX declining to **12.67**, the current environment favors a selective approach. Wealth creation is increasingly concentrated in quality issues that can survive the transition from primary market hype to secondary market reality.

Goldman Sachs Initiates Buy Rating on LG Electronics India with Target Price of ₹1,750

LG Electronics India is maintaining a strong market position despite navigating a complex financial quarter. As of mid-February 2026, the stock is trading near **1,575 INR**, reflecting a robust recovery and an **8.4%** single-day surge. This upward momentum comes as the company settles into its status as a major listed entity following its high-profile **11,607 crore INR** IPO in late 2025. Goldman Sachs has issued a Buy rating for the electronics giant with a target price of **1,750 INR**. This target suggests a potential upside of approximately **11%** from current levels. Analysts point to the company’s "Global South" strategy and its ability to lead in premium categories as primary growth drivers. The brokerage remains bullish on the company’s long-term trajectory, despite recent volatility in the broader consumer durables sector. The financial performance for the third quarter of FY26 revealed significant operational hurdles. Net profit witnessed a sharp **61.6%** year-on-year decline, falling to **89.6 crore INR**. Revenue also saw a contraction of **6.4%**, landing at **4,114 crore INR**. This downturn was largely attributed to a post-festive demand slump and a significant squeeze on margins. Profitability was further pressured by rising operating expenses and commodity costs. The EBITDA margin narrowed to **4.8%**, down from **7.7%** in the previous year. High costs for materials like copper and aluminum, combined with a depreciating rupee, created a challenging environment for maintaining bottom-line growth during the December quarter. Looking ahead, the outlook for the fourth quarter appears more optimistic. Management is pivoting toward a "two-track" strategy to capture upcoming summer demand. This involves expanding the "LG Essential" lineup for aspirational buyers while simultaneously pushing high-end premium offerings. The company is also scaling its high-margin AMC business and exploring B2B infrastructure opportunities to diversify income. The broader Indian consumer electronics market remains a fertile ground for growth, projected to reach **3 lakh crore INR** by FY29. With an expected annual growth rate of **11%**, the sector is benefiting from increased urbanization and government incentives like the PLI scheme for white goods. LG’s focus on domestic manufacturing under the "Make in India" initiative is expected to help the company double its exports to the US and Europe in the coming fiscal year. Market sentiment is currently bolstered by recent GST cuts on large televisions and a general shift toward energy-efficient, smart appliances. While short-term earnings have been hit by seasonal softness and cost inflation, the company’s dominant market share and premiumization strategy keep it positioned as a top pick for institutional investors seeking exposure to India’s consumption story.

Gold Prices Rise While Silver Declines Amid Lunar New Year Trading Conditions

Global Market Brief: February 18, 2026 Global financial markets are navigating a complex landscape defined by shifting technology valuations and heightened geopolitical tension. Following the mid-February U.S. holiday, trading has resumed with a pronounced divergence between traditional industrials and the high-growth technology sector. Equity Indices and Tech Volatility The **S&P 500** recently surpassed the **7,000** level for the first time, though it remains in a volatile consolidation phase near **6,940**. The **Dow Jones Industrial Average** has shown relative strength, reaching record highs above **50,000**, supported by blue-chip resilience in the energy and industrial sectors. In contrast, the **Nasdaq Composite** has faced downward pressure, recently trading around **23,025**. A significant "SaaSpocalypse" sell-off is impacting software firms as investors re-evaluate license demand in the age of autonomous AI agents. While hardware and infrastructure providers continue to see record capital expenditure, software-as-a-service valuations are under scrutiny. Economic Indicators and Monetary Policy U.S. labor data remains surprisingly robust, with **130,000** jobs added in January, far exceeding expectations of **70,000**. The unemployment rate has settled at **4.3%**. Despite this strength, annual inflation has slowed to **2.4%**, the lowest rate since early 2021. Markets are currently pricing in two interest rate cuts for the remainder of 2026. The nomination of Kevin Warsh as the next Federal Reserve Chair has provided some institutional stability, though his future policy leanings remain a central focus for fixed-income traders. Commodities and Energy Energy markets are reacting sharply to tensions in the Middle East and South America. Crude oil prices rose **14.6%** in January to reach **$69.70** per barrel. Tensions in the Strait of Hormuz, through which **21 million** barrels of oil pass daily, continue to inject a risk premium into global energy costs. Precious metals have reached historic levels as a hedge against volatility. Gold, which surged throughout 2025, is currently trading near **$4,300** per ounce. Silver has experienced sharper corrections, recently dipping toward the **$74.85** mark. Global Outlook and Trade International markets are increasingly defined by new trade alliances. India and the European Union have progressed toward a landmark free trade agreement. India’s economy continues to outpace global peers with a real growth rate projected at over **7%** for the year. European benchmarks like the **EURO STOXX 50** are struggling with sluggish luxury demand, while Japan's **Nikkei 225** remains under pressure as the domestic economy maintains a fragile recovery from a near-recession.

One97 Communications and Four Other Stocks Show Bullish Technical Indicators

Market Brief: Nifty 200 Technical Momentum The Indian equity market maintained its upward trajectory through February 17, 2026, with the **Nifty 200 index** closing at **14,367.20**, marking a gain of **0.23%**. This steady climb was supported by a notable intraday recovery, as the index bounced back from a low of **14,281.60** to reach a high of **14,382.90**. Technical scanners highlighted five specific stocks within the Nifty 200 universe that formed the rare and bullish **White Marubozu** candlestick pattern. This formation, characterized by a long body with little to no shadows, indicates that buyers remained in absolute control from the opening bell to the final trade. Key Bullish Movers The surge was led by high-conviction buying across banking and fintech sectors. **One97 Communications (Paytm)** surged **4.11%** to close at **1,169.30**, leading the pack of momentum gainers. The public sector banking space also displayed significant strength. **Bank of Baroda** rose **3.66%** to end the day at **303.25**, while **Punjab National Bank** gained **3.52%**, finishing at **124.82**. These moves suggest a sector-wide accumulation as investors seek value in large-cap financial institutions. Other prominent stocks clearing the bullish threshold included **Coromandel International**, which climbed **3.61%** to **2,369.90**, and **Indian Bank**, which moved up **3.51%** to settle at **920.10**. Broader Market Context The overall market sentiment remained positive, bolstered by steady institutional activity. **Foreign Institutional Investors (FIIs)** were net buyers, injecting **995 crore** into the cash market. **Domestic Institutional Investors (DIIs)** provided further support with net purchases of **187 crore**. The **Nifty 50** ended the session at **25,725.40**, up **0.17%**, while the **BSE Sensex** rose **173.81 points** to reach **83,450.96**. While the metal sector faced headwinds, with **Hindalco** and **Tata Steel** trading lower, the IT and FMCG sectors provided the necessary cushion to keep the benchmark indices in the green. Technical analysts view the appearance of the White Marubozu across multiple liquid stocks as a signal of high demand. These patterns often precede a continuation of the current uptrend, provided the opening levels of the following session hold firm against minor profit-taking.

Adani Power and Four Other Large-Cap Stocks Record Bullish RSI Trends

Market dynamics shifted on February 17 as five large-cap stocks entered a bullish phase, triggered by the Relative Strength Index (RSI) Trending Up scan. This technical movement occurs when the RSI crosses above the 50-level threshold, signaling a transition from neutral or bearish territory to strengthening price momentum. The stocks identified in this momentum shift include Bank of Baroda, Punjab National Bank, Solar Industries India, Canara Bank, and Adani Power. These equities recorded gains between 2% and 5% during the session, drawing significant interest from institutional and retail traders looking for trend continuation. Bank of Baroda led the technical surge with its RSI jumping to 58.89 from a previous reading of 49.34. The stock’s current market price settled at 303.25. Close behind was Punjab National Bank, which saw its RSI climb to 54.32 from 43.88, with shares trading at 124.82. Both public sector banks benefited from a broader sector-wide rally that provided a tailwind for the Nifty Bank index. In the industrial and energy sectors, Solar Industries India moved into a bullish zone with an RSI of 51.85, up from 49.38, closing at a price of 13,266. Canara Bank also crossed the midline with an RSI of 51.33, ending the day at 149.11. Adani Power rounded out the list, narrowly crossing the threshold with an RSI of 50.30 and a closing price of 144.35. These technical breakouts coincided with a resilient day for the broader Indian indices. The BSE Sensex rose by 174 points to end at 83,450.96, while the NSE Nifty 50 gained 43 points to close at 25,725.40. Despite a global backdrop of muted cues and ongoing concerns regarding AI-driven disruptions in the IT sector, domestic liquidity remained high. Institutional activity showed a diverging trend on February 17. Foreign Portfolio Investors (FPIs) were net buyers to the tune of 995.21 crore, while Domestic Institutional Investors (DIIs) also supported the market with net purchases of 187.04 crore. This combined buying pressure helped stabilize the market after recent volatility. Traders often view an RSI crossing above 50 as a "buy on dips" signal, suggesting that the path of least resistance has shifted to the upside. While some heavyweights like Larsen & Toubro moved closer to overbought territory with an RSI above 70, these five stocks are considered to be in the early stages of a momentum buildup. Market focus now turns to whether these levels can be sustained. With the Nifty 50 maintaining support near the 25,500 zone, technical analysts suggest that these RSI breakouts could lead to further gains if the benchmark indices continue their recovery towards the 25,900 resistance level. [Adani Power RSI Bullish Upswing](https://www.youtube.com/watch?v=zXrSfaoKyTw) This video provides a detailed breakdown of the technical momentum and RSI trends for large-cap stocks like Adani Power, offering insight into the current market sentiment. http://googleusercontent.com/youtube_content/0

13 Stocks Surpass 200-Day Moving Average

Market Outlook: The 200-Day SMA Pivot The **200-day Simple Moving Average (SMA)** remains the definitive line in the sand for global equity markets this February 2026. As a primary indicator of long-term health, the ability of major indices to hold above this level is currently dictating investor appetite. In the U.S., the **S&P 500** is navigating a complex technical landscape, trading near **6,836**. While the index has faced resistance near the psychological **7,000** mark, it maintains a structural uptrend by staying comfortably above its 200-day SMA, which currently aligns with the **6,500 to 6,532** support zone. The **Nasdaq 100** shows a more polarized picture. Although it continues its multi-year climb, trading around **24,878**, internal breadth has thinned. Data shows only **51.48%** of stocks within the Nasdaq 100 are currently trading above their individual 200-day averages, suggesting a market led by a narrowing group of performers. Global Resilience and Breakouts Emerging markets are seeing a surge in technical momentum. In India, the **Nifty 50** recently bounced off a critical confluence of its 20-day and 200-day moving averages near **25,500**. This "golden" support zone has re-energized the bullish case for domestic equities. Recent scans identified **13 major stocks** in the Nifty 500—including names like **Adani Green Energy** and **One97 Communications**—that have successfully crossed back above their 200-day SMAs. This crossover is widely viewed as a transition from a corrective phase to a fresh uptrend. * **Adani Green Energy**: Crossed 200-day SMA of **996.05**; current price **1,016.80**. * **One97 Communications**: Reclaimed 200-day SMA of **1,142.42**; current price **1,169.30**. * **Delhivery**: Surpassed 200-day SMA of **418.76**; current price **434.85**. Economic Catalysts and Volatility The market’s technical floor is being tested by shifting macro data. U.S. consumer inflation has moderated to **2.4%**, while the unemployment rate sits at **4.3%**. These figures keep the Federal Reserve on a path of "modest easing," which typically supports valuations for stocks trending above their long-term averages. However, short-term volatility is rising. The **VIX** remains elevated at **20.60**, and the **VIX1D** (one-day volatility) is even higher at **22.43**. This suggests that while the long-term trend is up, investors are paying a high premium for protection against immediate catalysts like the upcoming FOMC minutes. In commodities, **Silver** and **Gold** continue to trade well above their respective 200-day SMAs, confirming that the secular bull market in precious metals remains intact despite recent profit-taking. Summary of Key Support Levels The following levels represent the final line of defense for the current uptrend. A daily close below these figures would signal a shift from a "buy the dip" environment to a potential trend reversal. * **S&P 500**: Critical support at **6,500** (200-day SMA). * **Nasdaq 100**: Monitoring the **24,000** floor to maintain the 2023–2026 rally. * **Nifty 50**: Strong technical base established at **25,500**. As long as prices sustain these levels, the market remains in a confirmed uptrend, favoring long-term positioning over aggressive short-selling.

Five long-term stock picks for 2026, including Titagarh Rail and Ipca Lab, with projected returns of 10-40%.

Market Overview Indian equity benchmarks maintained a positive trajectory on February 18, 2026, with the Nifty 50 trading above the **25,750** mark and the S&P BSE Sensex advancing to **83,584.87**. This resilience comes despite mixed global cues and ongoing geopolitical tensions in the Middle East. Market breadth remains strong, with **2,417** shares rising against **1,505** declines on the BSE. Volatility, as measured by the India VIX, has cooled by **4.29%** to a stable level of **12.76**. Sector Performance and Economic Triggers The IT and Defence sectors are leading the current charge. Defence stocks are gaining momentum following Cochin Shipyard's status as the lowest bidder for a **₹5,000 crore** Ministry of Defence project. The manufacturing sector is showing structural recovery with Q2 FY26 growth hitting **9.13%**. Government-led PLI schemes have now attracted over **₹2.0 lakh crore** in actual investment. India's external buffers remain robust with foreign exchange reserves at **$701.4 billion**, providing approximately **11 months** of import cover. Top Brokerage Recommendations **Energy and Infrastructure** Motilal Oswal has reiterated a Buy on **IGL** with a target of **₹235**, representing a potential upside of **41%** from the current market price of **₹166**. **Siemens Energy** has seen its target price raised to **₹3,600** from **₹3,400** by Motilal Oswal, citing a **31%** upside potential from the current level of **₹2,738**. Elara Capital remains bullish on **ONGC**, increasing its target to **₹320** (up from **₹304**), suggesting a **19%** gain from the current price of **₹267**. **Pharmaceuticals and Consumer Goods** Citi has upgraded the target for **Lupin** to **₹2,540**, up from **₹2,260**, following its specialty pharma expansion in Canada. This offers a **15%** upside from the current **₹2,199**. **Britannia Industries** is favored by multiple firms. Motilal Oswal maintains a target of **₹7,150**, while technical analysts eye a shorter-term target of **₹6,570** as long as it stays above **₹5,930**. **Banking and Telecom** Anand Rathi suggests a Buy for **Bharti Airtel** with a target of **₹2,100**, noting strong momentum as the stock holds its support near **₹2,020**. **Canara Bank** is showing a "double-bottom" reversal pattern. Analysts set a target of **₹160** with a stop-loss at **₹144**. **RBL Bank** is also gaining interest with a target range of **₹350–₹355** following a surge in trading volumes. Emerging Opportunities **Coal India** is positioned as a technical buy in the **₹415–₹425** range, with analysts targeting **₹470** as it recovers from a corrective phase. In the mid-cap space, **Delhivery** is highlighted with a target of **₹570** (**36% upside**), driven by its acquisition of Ecom Express and expanding EBITDA margins of **7.4%**. **Amber Enterprises** is recommended by Yes Securities with a high conviction target of **₹8,962**, fueled by the doubling of revenue expectations in its railway business.

Gold Prices Stabilize Following Recent Sell-off

Market Brief: Gold Performance and Outlook Gold prices are demonstrating a cautious recovery this Wednesday, February 18, 2026, following a period of intense volatility. After a significant retreat earlier in the week, bullion is stabilizing as traders reassess the geopolitical landscape and domestic economic indicators. Spot gold is currently trading around **$4,880 per ounce**, attempting to find a firm floor after dropping more than **2%** in the previous session. In domestic markets, 24K gold is hovering near **₹15,435 per gram**, reflecting a correction of approximately **1.4%** from yesterday’s levels. Geopolitical De-escalation The primary driver behind the recent price dip has been a perceived cooling of tensions in the Middle East. Progress in second-round negotiations between the U.S. and Iran in Geneva has significantly eroded the safe-haven premium that supported gold’s record-breaking rally earlier this year. Reports of potential document exchanges between the two nations have led investors to scale back risk hedges. Interest Rate Trajectory Market participants are closely monitoring the Federal Reserve's next moves. While January inflation data slowed to **2.4%**, coming in below the forecast of **2.5%**, Fed officials have signaled a cautious approach. Current sentiment suggests the central bank may hold rates steady for some time to ensure inflation remains on a path toward the **2%** target. Higher-for-longer interest rates typically pressure non-yielding assets like gold. However, many analysts still anticipate at least two rate cuts of **25 basis points** later in 2026, which provides a long-term support pillar for the metal. Holiday Liquidity and Demand Trading volumes remain subdued as major Asian markets, particularly China, are closed for the Lunar New Year. This seasonal absence of the world's largest gold consumers has led to thinner liquidity, which can often exaggerate price swings. Despite the lull in active trading, physical demand in the lead-up to the holiday was exceptionally high. In China, gold jewelry prices surged over **70%** year-over-year to approximately **¥1,529 per gram**, highlighting the deep cultural value and inelastic demand for the metal even at elevated price points. Technical Support and Currency Impact The U.S. Dollar Index has shown resilience, exerting downward pressure on dollar-denominated bullion. Technically, gold is testing key support levels. If it fails to hold the **$4,850** mark, further profit-taking could be triggered. Conversely, maintaining stability near the psychological **$5,000** level remains the goal for bullish investors looking toward the second half of the year.

USD Steady Amid Geopolitical Negotiations and Upcoming Fed Minutes

Global markets remained cautious on Wednesday, February 18, 2026, as investors navigated a complex landscape of cooling inflation and persistent geopolitical friction. Major U.S. indices showed marginal movement, with the S&P 500 edging up 0.1% to 6,843.22, while the Dow Jones rose 0.07% to 49,533.19. The tech-heavy Nasdaq Composite saw a modest gain of 0.14%, ending the session at 22,578.38. Market participants are focused on the Federal Reserve's current pause in rate adjustments. The federal funds rate remains held in the 3.5% to 3.75% range. Investors are scrutinizing recent Fed communications for clarity on the path forward, especially following the nomination of Kevin Warsh to succeed Jerome Powell. While the economy remains solid, a recent uptick in the VIX to 20.29 reflects a slight increase in underlying market anxiety. In Asia, the Japanese yen showed stability against the dollar, trading near the 156.50 level. This follows reports of a manufacturing sector recovery, with the Japan Manufacturing PMI hitting 51.5 in early 2026—the strongest expansion in factory activity since mid-2022. Domestic sentiment is bolstered by rising machine tool orders, which surged 25.3% in January, signaling robust capital investment. Geopolitical developments have provided a mix of optimism and caution. In Geneva, U.S. and Iranian negotiators reported progress on "general guiding principles" for a potential nuclear agreement. While significant gaps remain regarding uranium enrichment and verification, both sides characterized the latest round as constructive, reducing immediate fears of military escalation in the region. Simultaneously, trilateral peace negotiations between Ukraine, Russia, and the U.S. continued in Switzerland. Despite ongoing airstrikes targeting Ukrainian energy infrastructure, delegations have moved into discussions on the "mechanics of possible decisions." Ukraine maintains its stance against territorial concessions in the Donetsk region, keeping expectations for a total breakthrough measured as the conflict nears its four-year mark. European equity markets reflected this wait-and-see approach. The DAX in Germany gained 0.8% to reach 24,998.40, while the FTSE 100 in London rose 0.79% to 10,556.17. Global growth for 2026 is currently projected at 3.3%, a slight upward revision that suggests resilience despite the shifting trade policies and high-stakes diplomacy currently dominating the headlines.

US Stock Market: Equities Close Slightly Higher Amid Tech Recovery

Indian Markets Extend Recovery The Indian equity market maintained its upward momentum for a second consecutive session. The **Nifty 50** rose **42.65 points** to close at **25,725.40**, while the **Sensex** settled **173 points** higher at **83,450.96**. Public sector banks spearheaded the rally, with the **Nifty PSU Bank** index jumping **2.1%** on robust credit growth expectations. Technology shares also staged a notable recovery, gaining **1.0%** following a major collaboration between **Infosys** and an AI firm. Market volatility, measured by the **India VIX**, dropped significantly by **4.93%**, suggesting a shift toward stability. However, gold and silver futures saw a sharp decline of up to **3%** as investors reacted to a firmer dollar and higher bond yields. Strategic Shift for Norwegian Cruise Line Shares of **Norwegian Cruise Line** surged over **12%** following revelations that **Elliott Investment Management** has built a stake exceeding **10%**. The activist firm is now one of the company's largest shareholders and is pushing for a comprehensive board overhaul. The cruise operator has faced criticism for underperforming its peers, with its stock remaining near pandemic-era levels. Elliott’s intervention, which includes plans to nominate new directors, has fueled investor optimism for a strategic turnaround. The company recently appointed a new CEO and announced orders for three high-tech ships scheduled for delivery in **2036**. Despite record revenues of **$2.94 billion** in late **2025**, the firm continues to battle inconsistent cost discipline. Danaher to Acquire Masimo for $10 Billion Medical technology firm **Masimo Corporation** saw its stock skyrocket **34.3%** to **$174.78** after a definitive agreement for its acquisition by **Danaher Corporation**. The all-cash deal is valued at **$180 per share**, totaling approximately **$9.9 billion**. The transaction will integrate Masimo into Danaher’s diagnostics segment as a standalone unit. Masimo is a global leader in pulse oximetry, with its technology used on more than **200 million** patients annually. Danaher expects the acquisition to be accretive to earnings, projecting **$125 million** in annual cost synergies within five years. The deal is slated to close in the second half of **2026**, pending regulatory and shareholder approval. General Mills Revises Outlook Downward **General Mills** faced a sharp decline after cutting its fiscal **2026** financial outlook during the Consumer Analyst Group of New York conference. The company now expects organic net sales to drop between **1.5%** and **2.0%**. Adjusted operating profit and diluted earnings per share are projected to fall by **16%** to **20%** in constant currency. This revision is more severe than the previous forecast of a **10%** to **15%** decline. Management cited a "volatile operating environment" and weak consumer sentiment as the primary drivers of the slower-than-expected volume recovery. Despite the downturn, the firm maintains a healthy dividend yield of **5.05%** and aims for a **95%** free cash flow conversion.

Portland General Electric to Acquire PacifiCorp’s Washington Assets for $1.9 Billion

PacifiCorp has reached a definitive agreement to sell its Washington state energy assets and infrastructure to Portland General Electric (PGE) for **$1.9 billion**. This major divestiture by the Berkshire Hathaway-owned utility comes as it faces significant financial pressure from ongoing wildfire litigation in Oregon. The deal includes a comprehensive portfolio of generation and distribution assets. PGE will acquire the **477-MW** Chehalis natural gas plant alongside the Goodnoe Hills and Marengo wind facilities. The transaction also encompasses **4,500 miles** of transmission and distribution lines, serving approximately **140,000 customers** across **2,700 square miles** in central and southern Washington. PacifiCorp is taking this step to bolster liquidity as it manages potential liabilities from the 2020 Labor Day wildfires. While the utility has recently settled smoke-related claims with Oregon wineries for **$125 million**, it still faces broader class-action litigation where damage claims have been estimated as high as **$52 billion**. The company cited "extraordinary pressure" from diverging state policies and regulatory challenges across its six-state service area as a primary driver for the sale. This move is intended to simplify operations and stabilize credit ratings that have been impacted by the legal landscape in the Pacific Northwest. For Portland General Electric, the acquisition represents a transformational expansion. To fund the **$1.9 billion** purchase, PGE has secured bridge and term loans from major financial institutions and partnered with Manulife Investment Management, which will take a **49%** stake in the newly acquired Washington business. The transaction is expected to be accretive to PGE’s earnings within the first full year of ownership. The deal now enters a regulatory review phase involving federal and state commissions, with a final closing expected to take at least **12 months**. During this period, existing electricity rates and local operations in areas like Yakima and Walla Walla are expected to remain stable.

Berkshire Hathaway Adds New York Times Stake, Reduces Apple Holding

Berkshire Hathaway Market Brief: Q4 2025 – Feb 2026 Berkshire Hathaway has marked a strategic return to the media sector by acquiring **5.07 million shares** in **The New York Times (NYT)**. This investment, valued at approximately **$352 million** as of the latest regulatory filings, represents a significant reversal from Warren Buffett’s 2020 exit from the newspaper industry. The disclosure on **February 17, 2026**, sent NYT shares climbing more than **3%** in after-hours trading. The publisher recently reported strong momentum, hitting an all-time high of **$74.23** and boasting over **12 million** digital subscribers, fueled by its diversified digital strategy including games and sports. Leadership Transition This quarterly update arrives at a historic pivot point for the conglomerate. **Greg Abel** officially succeeded Warren Buffett as Chief Executive Officer on **January 1, 2026**. While Buffett remains Chairman of the Board, Abel now holds day-to-day leadership of the **$1.1 trillion** enterprise. The transition has been accompanied by a broader leadership overhaul, including the departure of portfolio manager Todd Combs to JPMorgan Chase and the appointment of new lieutenants to oversee Berkshire’s **32** core operating businesses. Portfolio Rebalancing and Tech Adjustments In the final months of 2025, Berkshire continued to aggressively rebalance its massive equity portfolio. The conglomerate trimmed its stake in **Apple** for the third consecutive quarter, selling roughly **10.3 million** shares. Despite a **4.3%** reduction in position size, Apple remains Berkshire’s largest holding, valued at approximately **$62 billion**. The firm also executed a substantial exit from **Amazon**, slashing its position by **77%**. The holding was reduced from roughly **$2.2 billion** to **$525 million**. This move follows a year where Amazon underperformed the broader market, dropping **11%** while the S&P 500 rose. Banking and Energy Shifts The financial sector saw a notable reduction as well, with Berkshire selling **50.8 million** shares of **Bank of America**. This **8.9%** cut reflects a long-term trend, as the firm has halved its stake in the bank over the past **18 months**, reducing it from over **1 billion** shares to approximately **517 million**. Conversely, Berkshire increased its exposure to the energy sector. The firm added **8 million** shares of **Chevron**, bringing its total to more than **130 million** shares. Chevron’s stock has surged nearly **19%** since the start of **2026**, driven by geopolitical shifts and its unique operational position in South American oil markets. Future Outlook Investors are now looking toward **February 28, 2026**, when Berkshire will release its full-year financial results. This will feature Greg Abel’s first annual letter to shareholders, a document expected to clarify the firm’s strategy for its **$300 billion** cash reserve and the future of its decentralized operating model.

Indian Indices Set for Positive Start Amid Strong Global Cues

Market Dynamics and Economic Shift The global economy enters mid-February 2026 at a critical juncture, characterized by a sharp divergence between traditional sectors and the rapid expansion of technology infrastructure. While the probability of a global recession remains pegged at **35%**, the first half of the year is buoyed by front-loaded fiscal stimulus and a notable rebound in investor sentiment. Inflation continues to be "sticky," hovering around the **3%** mark, as trade-related pressures on goods prices persist. Emerging markets are emerging as the primary engine for growth. India is currently leading major economies with a real growth rate of **7%**, supported by recent credit rating upgrades. Conversely, developed markets are navigating a more complex path of uneven monetary policy and stalling job gains in non-tech sectors. Equities and the AI Paradox Wall Street is currently navigating a period of "directionless" volatility. The S&P 500 stands near **6,820**, while the Dow Jones Industrial Average maintains a narrow lead at approximately **49,525**. The Nasdaq Composite, currently around **22,395**, has faced significant pressure as the initial "AI euphoria" transitions into a demanding "AI disruption" phase. Investors are now scrutinizing the actual return on investment for artificial intelligence. Software leaders have seen dramatic shifts, with some enterprise giants recording year-to-date declines of **30%** to **31%**. Despite these fluctuations, the semiconductor industry remains a powerhouse, with global sales projected to hit a historic peak of **$975 billion** in 2026. This growth is increasingly concentrated in high-performance logic and memory chips, which are expected to see annual growth exceeding **30%**. Energy and Commodities Outlook The energy landscape is defined by a looming supply glut. Brent crude oil is forecasted to average **$58** per barrel in 2026, a result of production levels outpacing global demand. In contrast, U.S. natural gas prices at the Henry Hub have seen a sharp **40%** increase in early 2026 due to inventory withdrawals, with an annual average forecast of **$4.31** per MMBtu. The transition to renewables is accelerating, particularly in the Asia-Pacific region, which is currently in the midst of a **$4 trillion** power market investment boom. Solar generation is expected to surge by **17%** this year alone. However, this shift is creating an acute deficit in industrial metals; copper is projected to swing into a **1 million metric ton** deficit as data centers and electric vehicle infrastructure demand more of the material. Precious Metals and Safe Havens Gold has solidified its position as the premier hedge against geopolitical and financial risk. Prices have experienced extreme volatility, recently reaching record levels near **$4,700** per ounce. While gold maintains strong structural support from emerging market central banks, silver has proven more volatile, experiencing record intraday drops of up to **26%** during recent corrections. The current "gold-to-crude" ratio of **74.87** reflects a market that favors defensive assets over industrial energy. Investors are increasingly adopting "barbell" strategies—pairing the protection of gold with industrial metals like copper and nickel to capture the upside of the ongoing electrification and AI infrastructure buildout.

Paul Samuelson on the Passive Nature of Successful Investing

Market Dynamics and Strategic Patience Successful wealth creation remains a disciplined process, often compared to watching paint dry. In the current 2026 landscape, the **S&P 500** continues to test this patience. As of February 18, 2026, the index is trading near **6,843**, reflecting a period of consolidation after reaching historical highs earlier in the quarter. The market has entered a phase of heightened selectivity. While the broad index is forecast to deliver a **12% total return** for the year, investors are facing increased dispersion. The "Magnificent 7" leaders, which drove much of the **17.9% gain** in 2025, are seeing a divergence in performance. Currently, six of these top tech leaders are trading roughly **15% below** their all-time peaks, shifting the focus toward broader market participation. Economic Indicators and Rate Cycles Inflationary pressures are showing signs of stabilization. The latest retail inflation data shows a rate of **2.75%**, a significant shift from the volatile peaks of previous years. This cooling trend has allowed major central banks to pause their aggressive tightening. The **Federal Reserve** currently maintains interest rates in the **3.50% to 3.75%** range, providing a more stable backdrop for corporate earnings. Global growth is projected to hold steady at **3.3%** for 2026. This resilience is supported by a rebound in manufacturing and the continued integration of efficiency-driving technologies. However, the 35% probability of a localized recession keeps defensive positioning relevant for disciplined portfolios. Rationality Over Stimulation Modern markets provide constant stimulation, yet the most effective strategies remain rooted in quiet compounding. Retail investor behavior in 2026 shows a maturing trend, with a notable increase in "dip-buying" through diversified ETFs. This reflects a shift away from chasing momentum and toward capturing value during technical pullbacks. Total household wealth has reached record levels, yet cash balances remain in the **98th percentile** historically. This "dry powder" suggests that while investors are cautious, the capacity for long-term reinvestment is substantial. Rationality and diversification continue to serve as the primary defenses against the emotional volatility of daily price swings. Strategic Outlook Market leadership is broadening beyond mega-cap technology into cyclical sectors. Financials, industrials, and materials are gaining momentum as investors rotate toward value. Analysts suggest the S&P 500 could reach **8,500** by the end of the year if earnings growth, currently projected at **12% to 14%**, meets expectations. True wealth is being built by those who ignore the noise of short-term swings—such as the recent **2% fluctuations** in early February—and remain committed to the long-term compounding cycle. The reward for this discipline is a share in the historical **9.8% annual growth** that has characterized the market since its inception.

Global Markets: Asian Equities Rise as Gold Prices Decline

Asia Market Brief: February 18, 2026 Asian equity markets demonstrated a measured upward trend during Wednesday's session. Trading volumes remained notably thin as several regional hubs continued to observe Lunar New Year festivities. Investors are navigating a complex landscape defined by high-stakes central bank decisions and a reassessment of the technology sector’s growth trajectory. Regional Performance and Trends Regional performance was varied, with major indices showing slight gains despite a lack of strong direction from overnight global cues. * **Japan:** The Nikkei 225 hovered around **56,467**, reflecting a slight pullback of **0.60%** as investors weighed currency pressures and upcoming inflation data. * **Hong Kong:** The Hang Seng Index edged up by **0.52%** to approximately **26,706**. Technical indicators suggest the index is finding immediate resistance near the **27,300** level. * **India:** The BSE Sensex rose **0.21%** to **83,451**, while the Gift Nifty showed a modest gain of **0.18%**, reaching **25,710**. Central Bank Policy Focus The Reserve Bank of New Zealand (RBNZ) released its February Monetary Policy Statement today, maintaining the Official Cash Rate (OCR) at **2.25%**. Policymakers indicated that while annual inflation sits slightly above the **1% to 3%** target band, they expect it to return to the **2%** midpoint within the next **12 months**. The RBNZ signaled that policy will remain "accommodative for some time" as the economic recovery remains in its early stages. Meanwhile, the U.S. Federal Reserve remains a focal point. Recent signals from Fed officials suggest a "meeting-by-meeting" approach. While the benchmark rate currently sits in the **3.50% to 3.75%** range, market participants are pricing in approximately **two rate reductions** by the end of **2026**, contingent on inflation moderating toward the **2%** target. Technology and AI Outlook Volatility in the technology sector persists as investors recalibrate expectations for artificial intelligence. Concerns regarding the "AI divide" and the high capital expenditure required for AI infrastructure have led to a more cautious valuation of the "Magnificent Seven" and their Asian counterparts. Market data shows significant year-to-date pressure on major tech entities, with some large-cap names seeing double-digit corrections. However, enterprise software demand remains a pillar of support, with projections suggesting **40%** of applications will integrate task-specific AI agents by the end of the year. Economic Indicators In China, the Renminbi reached a **33-month high** against the dollar, trading near **6.90**. This strength comes despite mixed domestic data, including a Producer Price Index (PPI) decline of **1.4%** and a Consumer Price Index (CPI) growth of only **0.2%**, highlighting persistent deflationary risks that may require further government stimulus. Gold and silver markets also showed activity, with silver inventories at the Shanghai Futures Exchange approaching a **10-year low** of **342.1 tonnes**, indicating robust industrial demand.

Supreme Court permits Aakash Educational Services rights issue

The Supreme Court of India has finalized a critical ruling on Tuesday, February 17, 2026, allowing Aakash Educational Services (AESL) to proceed with its second tranche of a 240 crore INR rights issue. The court has granted Byju’s parent company, Think & Learn (TLPL), exactly one week to subscribe to the shares, setting a final deadline for next Monday, February 24, 2026. This move follows a protracted legal battle where TLPL challenged the fundraising, alleging that it would lead to a significant dilution of its holding. Currently, Aakash is raising 140 crore INR in this second phase to meet operational expenses for its 350,000 students and 10,000 employees. To balance the interests of the bankrupt parent company, the court recorded an assurance from Aakash that 25.75% of Byju's stake will remain secured until the National Company Law Appellate Tribunal (NCLAT) makes a final decision. This legal protection is vital as TLPL’s shareholding in Aakash had already been reflected as dropping to 10.99% in earlier notices, down from its original 25.75%. The dispute intensified after Aakash previously withheld share allotments to Byju's, citing concerns over the foreign source of funds and potential violations of exchange laws. The broader Indian edtech market continues to show resilience despite these corporate disputes. The sector is projected to reach a valuation of 10.4 billion USD by the end of 2025 and 33.3 billion USD by 2034. Aakash remains a top performer in the test preparation segment, which is growing at a compound annual rate of nearly 28%. The Manipal Group, led by Ranjan Pai, now holds a dominant position in Aakash with an estimated 58% stake. This shift in power occurs as Think & Learn remains under insolvency proceedings, triggered by unpaid dues of 158 crore INR originally owed to the BCCI. Investors are closely monitoring whether Byju’s can arrange the necessary capital from overseas before the Monday deadline to prevent further dilution. The court's ruling ensures that while Aakash gains the liquidity it needs to operate, the underlying asset value for Byju’s creditors remains protected during the insolvency process. [Aakash Rights Issue Dispute](https://www.youtube.com/watch?v=nX_ey6eADEk) This video provides an in-depth analysis of the high-stakes insolvency battle involving Byju's and Aakash, explaining the roles of key players like the Manipal Group and the impact of the rights issue on the company's valuation. http://googleusercontent.com/youtube_content/0