Bearish News

Collection

Morgan Stanley Maintains Buy on Aditya Birla Capital; Goldman Sachs Cuts Varun Beverages Target Price

**Global Market Snapshot: Volatility Grips Major Assets** **Wednesday, February 4, 2026** Global markets are navigating a turbulent mid-week session as technology stocks and cryptocurrencies face sharp sell-offs, while geopolitical tensions drive capital into commodities. **Equities: Tech Sell-Off Weighs on Sentiment** US markets closed lower, dragged down by a steep decline in the technology sector. The **Nasdaq Composite** fell **1.43%** to roughly **23,255**, and the **S&P 500** dipped **0.84%** to **6,917**. Investors are reacting to fears that rapid AI advancements are disrupting traditional software models, sparking a rotation out of major tech names. In Asia, the **Nikkei 225** dropped **1.23%**, echoing Wall Street’s weakness. However, Indian markets showed resilience, with the **Nifty 50** trading flat-to-positive near **25,750** and the **Sensex** hovering around **83,755**, supported by optimism surrounding recent India-US trade discussions. **Crypto: Bitcoin Under Heavy Pressure** The cryptocurrency market is witnessing a significant correction. **Bitcoin (BTC)** has slumped to the **$74,500 – $77,000** range, marking its lowest level since early 2025. Sentiment has turned bearish following the nomination of Kevin Warsh as Federal Reserve Chair, raising concerns about tighter monetary policy. Continued outflows from Spot Bitcoin ETFs and fears of a US government shutdown are further dampening appetite for digital assets. **Commodities: Oil & Gold Rally** Geopolitical instability is boosting traditional commodities. **Brent Crude** climbed nearly **1%** to **$68.03** per barrel, and **WTI** rose to **$63.90** after the US military intercepted an Iranian drone, escalating tensions in the Middle East. **Gold** continues to attract safe-haven flows, trading firmly above **$4,700** per ounce globally. In domestic markets, prices remain elevated as investors hedge against the broader equity volatility. **Key Market Drivers** * **AI Disruption:** Fears that AI agents are replacing legacy software services are hurting tech valuations. * **Fed Policy:** Expectations of "higher for longer" interest rates under new leadership. * **Geopolitics:** Renewed US-Iran friction supporting energy prices.

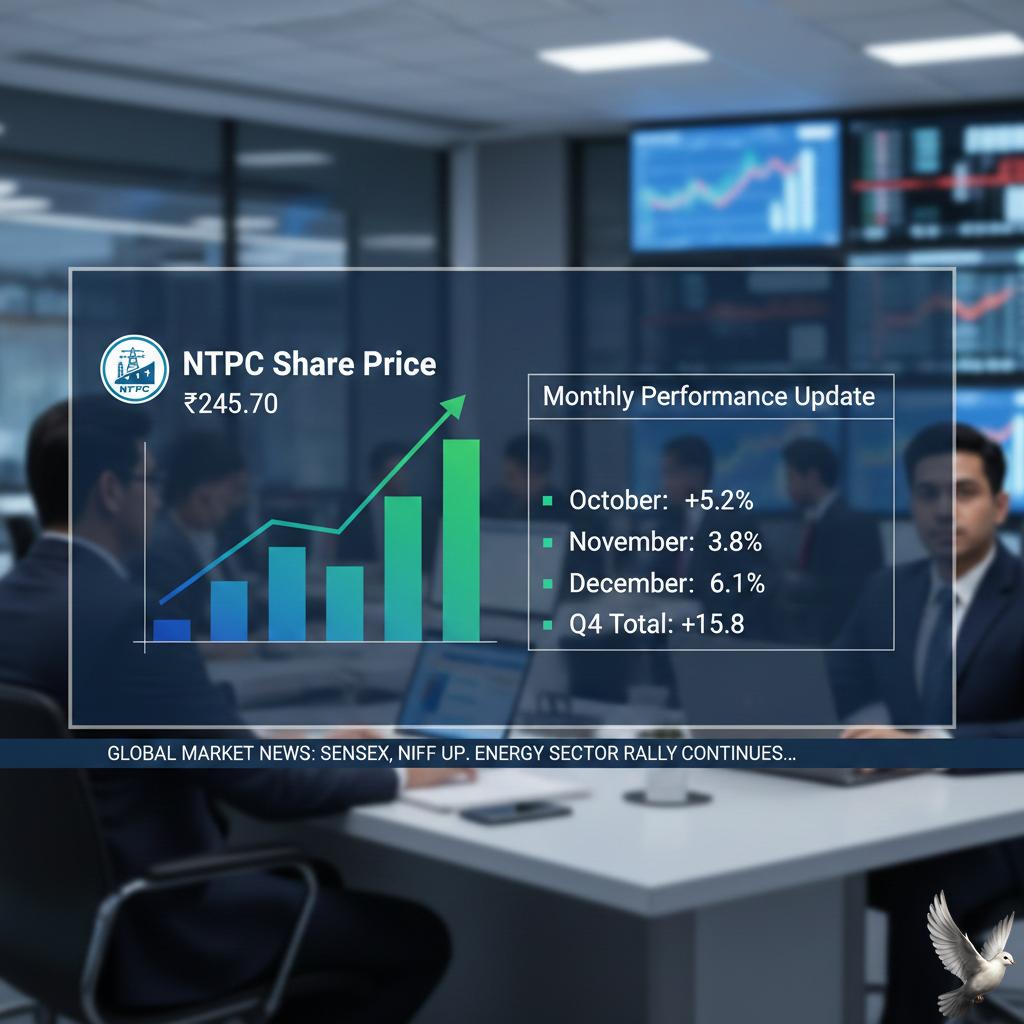

NTPC Share Price and Monthly Performance Update

**Global Market Brief | February 4, 2026** **Executive Summary** Markets are navigating a period of high volatility characterized by a violent rotation out of technology stocks and historic turbulence in precious metals. Geopolitical developments—specifically a new US-India trade pact and rising tensions in the Middle East—are driving sentiment alongside major US policy shifts. **US Equity Markets: Tech Rotation Intensifies** US indices remain divergent as investors flee high-growth tech for value and cyclical sectors. * **Indices:** The **Dow Jones** surged **515 points (+1.1%)** earlier this week, nearly hitting a record close. In contrast, the **Nasdaq 100** slid **1.6%**, and the **S&P 500** dipped **0.8%** amid a tech selloff. * **Tech Under Pressure:** Software stocks faced aggressive selling (down **~4%** broadly). **Nvidia** fell **3%** on news of stalled OpenAI investments. **Oracle** dropped **2.8%** after announcing a massive **$45–$50 billion** capital raise. **Adobe** and **ServiceNow** saw declines of roughly **7–8%**. * **Bright Spots:** **Walmart** defied the trend, surpassing a **$1 trillion** market cap. **Global & Emerging Markets** * **India Rally:** Indian markets (Sensex and Nifty) rallied sharply on Feb 4, fueled by a new trade deal with the US. Key terms include the US lowering tariffs on Indian goods to **18%** (from 25%) in exchange for India halting Russian oil purchases. * **Asia:** Markets were mixed, with South Korea’s Kospi tracking higher while indices in Japan and China faced headwinds from the global tech slump. **Commodities: Historic Volatility** Precious metals are experiencing a "flash crash" scenario following heightened margin requirements and shifting Fed expectations. * **Silver:** Witnessed its worst single-day drop since 1980, crashing nearly **30%** before a slight recovery. Current prices hover around **₹2.6 lakh/kg** in India. * **Gold:** Also faced heavy selling, dropping roughly **9%** in international markets to **~$4,781/oz**. Domestic prices in India corrected to **~₹1.49 lakh** per 10 grams. * **Oil:** Crude prices ticked higher, supported by news of the US Navy intercepting an Iranian drone, reigniting supply disruption fears. **Macroeconomic Drivers** * **Fed Leadership:** Volatility spiked after President Trump nominated **Kevin Warsh** to succeed Jerome Powell as Federal Reserve Chair, signaling a potential hawkish pivot. * **Interest Rates:** The Fed held rates steady at **3.50%–3.75%** in late January. * **Data Delays:** The January US jobs report has been delayed due to a partial government shutdown, leaving investors flying blind on labor market health. * **Crypto:** Bitcoin slumped to **~$78,000**, its lowest level since November 2024, caught in the broader risk-off sentiment.

Bajaj Finserv Share Price Updates: Stock Registers Decline in Returns

**Global Market Brief: India Rallies, Crypto Crumbles & Gold Shines** **Date:** February 4, 2026 **Market Overview** Global markets are witnessing a sharp divergence today. While Indian equities are celebrating a historic trade pact, US markets and digital assets are reeling under the pressure of hawkish Federal Reserve expectations and rising geopolitical tensions. **🇮🇳 India: Historic Surge on Trade Deal** Indian markets have decoupled from global weakness, posting massive gains following the announcement of a landmark **India-US trade deal**. * **Indices Rocket:** The **Nifty 50** surged **2.55%** to close at **25,727**, while the **Sensex** jumped over **2,000 points** (+2.54%) to **83,739**. * **Rupee Strength:** The Indian Rupee logged its best single-day performance in **7 years**, strengthening significantly against the US Dollar as foreign inflows are expected to accelerate. * **Sector Leaders:** Banking and Realty stocks led the charge, with **Bank Nifty** crossing the **60,000** mark (+2.43%). Heavyweights like **Reliance Industries** and **HDFC Bank** were top contributors to the rally. **🇺🇸 US & Global: Fed Fears & Tech Selloff** Wall Street is flashing warning signs as investors digest the nomination of **Kevin Warsh** as the next Federal Reserve Chair. Known for his hawkish stance, Warsh’s nomination has triggered fears of tighter liquidity and a smaller Fed balance sheet. * **Tech Slide:** The **Nasdaq** fell **1.43%** to **23,255**, dragged down by a selloff in AI and semiconductor stocks. **Nvidia** (-2.8%) and **PayPal** (-20%) faced heavy selling pressure. * **Geopolitics:** Tensions in the Middle East escalated after the US shot down an Iranian drone, adding to the risk-off sentiment in western markets. **🪙 Crypto: The "Warsh" Crash** The cryptocurrency market is facing a severe correction, reacting negatively to the potential regime change at the Fed. * **Bitcoin Plunge:** Bitcoin has crashed below the psychological **$80,000** level, trading near **$78,500** (down ~6.5% in 24 hours). This marks its lowest level since November 2025. * **Liquidation Cascade:** Over **$785 million** in positions were liquidated globally as "extreme fear" dominates sentiment. **Ethereum** and altcoins are seeing sharper declines, underperforming Bitcoin. **⚱️ Commodities: Flight to Safety** As equities wobble and war risks rise, capital is fleeing into traditional safe havens. * **Gold at $5,000:** Gold prices have shattered records, soaring above **$5,000 per ounce** globally. In India, prices crossed **₹1.5 Lakh** per 10 grams. * **Silver Surge:** Silver is outperforming gold with a massive **4% jump**, approaching **₹3 Lakh** per kg in domestic futures markets. * **Oil Ticks Up:** Crude oil prices are creeping higher, with **Brent** pushing toward **$68**, supported by supply concerns in the Middle East. **Outlook** Volatility is expected to remain high this week. Traders should watch for the **RBI Policy meeting** (to see if they intervene on the Rupee's rise) and further details on the US-India trade pact. Globally, the focus remains on the bond market's reaction to the new Fed leadership. *** **Next Step:**

RIL Share Price Registers Monthly Decline

Global Market Brief — February 4, 2026 📉 Global Equities: Divergent Trends **India Leads the Charge** Indian markets staged a massive rally today, decoupling from global weakness. The **Nifty 50** surged over **2.5%** to reclaim **25,727**, while the **Sensex** jumped **2,072 points** to close at **83,739**. Adani Group stocks were the primary drivers following strong Q3 results, with **Adani Enterprises** soaring **10.3%** and **Adani Ports** climbing **9.1%**. **US & Tech Under Pressure** In contrast, US markets faced headwinds as investors digested a flood of tech earnings and the recent end to the government shutdown. The **Nasdaq** slid **1.43%** to **23,255**, and the **S&P 500** declined **0.84%** to **6,917**. The **Dow Jones** remained relatively flat, dipping just **0.34%** to **49,240**. 🪙 Commodities & Crypto: Flight to Safety **Gold & Oil Rally** Geopolitical tensions in the Middle East and a weaker dollar have fueled a safe-haven rush. **Gold** prices extended their historic run, breaking past **$4,950 per ounce** after touching an all-time high near **$5,600** last week. **Crude Oil** prices also ticked higher as traders monitored potential supply disruptions. **Crypto "Extreme Fear"** The digital asset market remains in correction territory. **Bitcoin** is struggling to hold the **$76,000** support level after a week-long rout wiped nearly **$500 billion** from the sector. Sentiment has hit "extreme fear," with **Ethereum** trading down around **$2,250**. 🌍 Key Economic Drivers * **US Government Shutdown Ends:** President Trump signed a funding deal with Democrats, alleviating immediate fiscal uncertainty, though market reaction remains tepid. * **Corporate Earnings:** Strong EBITDA beats from Indian infrastructure giants have revitalized domestic sentiment, while US investors rotate out of high-growth tech stocks. * **Geopolitics:** Escalating tensions in the Middle East continue to support energy and precious metal prices, offsetting bearish pressure from equity market volatility.

L&T Shares Post Negative Monthly Returns

**Global Market Brief | February 4, 2026** **📉 Global Sentiment: Tech Stumble & Geopolitics** Global equities face pressure today as a sharp sell-off in US technology stocks dampens sentiment. Investors are reassessing AI valuations, leading to profit-taking in major players like **Nvidia** and **Microsoft** (both down **~3%**). * **Wall Street:** The **Nasdaq** dropped **1.43%** and **S&P 500** fell **0.84%** overnight, driven by fears that new AI tools are disrupting established software pricing power. * **Geopolitics:** Tensions have escalated after US forces downed an Iranian drone, driving capital toward safe-haven assets. **🇮🇳 Indian Markets: Consolidation Ahead** After a massive rally on Tuesday—where the **Sensex** surged over **2,000 points** following the historic **US-India trade deal**—domestic indices are set for a muted or negative start. * **Outlook:** **GIFT Nifty** futures indicate a gap-down opening (approx. **40 points lower**) tracking global weakness. * **Key Levels:** * **Nifty 50:** Closed at **25,728** (+2.55% yesterday). * **Sensex:** Closed at **83,739** (+2.54% yesterday). * **Sector Watch:** * **IT Services:** Likely to face headwinds due to the US tech rout. * **Defense & Aviation:** **Adani Enterprises** is in focus after announcing a helicopter manufacturing partnership with Italy’s **Leonardo**. > **

Kotak Bank Share Price: Monthly Performance Update

Market Brief: February 4, 2026 📉 Global Indices & Equity Performance Global markets face a wave of volatility as investors digest mixed economic signals and rotate out of high-flying tech stocks. * **United States:** Wall Street closed lower Tuesday (Feb 3). The **Nasdaq Composite** led the decline, dropping **1.43%** to **23,255**, pressured by heavy selling in the technology sector. The **S&P 500** fell **0.84%** to **6,917**, while the **Dow Jones Industrial Average** shed **0.34%** to **49,240**. Volatility spiked, with the **VIX** jumping over **10%** to **18.00**. * **Europe:** Indices struggled for direction. The **FTSE 100** (UK) dipped **0.26%** to **10,314**, and the **DAX** (Germany) slipped marginally to **24,780**. * **Asia:** Markets opened mixed on Wednesday. Japan’s **Nikkei 225** opened down **0.86%** at **54,250**, tracking US tech weakness. Australia’s **ASX 200** bucked the trend, rising **0.47%**. 🛠 Sector Spotlight: AI & Semiconductors The "AI trade" is shifting rather than stalling. While major chipmakers like **Nvidia** saw profit-taking (down **~2.8%**), infrastructure and custom-chip players are surging. * **Teradyne** crushed Q4 earnings expectations with a **44%** revenue jump, proving that demand for AI testing equipment is accelerating. * **Broadcom** and **TSMC** continue to outperform, driven by hyperscalers (Amazon, Meta, Google) building custom silicon, diversifying the market beyond standard GPUs. 🛢 Commodities & Currencies * **Oil:** Prices retreated sharply on signs of potential geopolitical de-escalation in the Middle East. **WTI Crude** fell **~2.5%** to **$61.78**, and **Brent** dropped to **$66.50**. * **Metals:** Precious metals experienced wild swings. **Gold** plunged briefly before settling near **$4,650**, down **~2%**. **Copper** was a bright spot, rebounding **4%** on news of China expanding strategic reserves. * **Crypto:** Digital assets remain under pressure. **Bitcoin** tested lows around **$73,100**, correcting significantly from its January levels, as regulatory uncertainty and macro headwinds weigh on sentiment. 🏦 Macroeconomic Backdrop * **Fed Policy:** The Federal Reserve held the benchmark rate steady at **3.50%–3.75%** in its recent meeting. Inflation remains sticky, complicating the path for future cuts despite political pressure. * **Economic Data:** US manufacturing is showing resilience, with the latest PMI inching up to **50.9**, signaling modest expansion. However, rising industrial input prices are a renewed concern for inflation watchers. 📅 What to Watch * **Earnings:** Continued focus on tech supply chain earnings to gauge AI capital expenditure durability. * **Geopolitics:** Ongoing US-Iran talks and their immediate impact on energy markets. * **Data:** Upcoming labor market reports to confirm if the "no-landing" economic scenario holds.

M&M Shares Post Monthly Decline

**GLOBAL MARKET BRIEF: FEB 04, 2026** **Geopolitical Tensions Trigger Risk-Off Wave | India Decouples with Trade Deal Rally** **📉 Global Equities: Tech Under Pressure** US markets closed lower Tuesday as investors rotated out of high-growth tech stocks amidst rising US-Iran tensions. * **S&P 500:** 6,917.81 (-0.84%) * **Nasdaq:** 23,255.19 (-1.43%) * **Dow Jones:** 49,240.99 (-0.34%) Big Tech led the decline, with **Nvidia (-2.84%)** and **Microsoft (-2.88%)** dragging indices. European markets were mixed, while Asian indices are seeing divergence today—Nikkei is down significantly, while Hang Seng remains flat. **🚀 India: Historic Rally on Trade Optimism** Indian markets bucked the global trend, surging on news of a US-India trade deal lowering tariffs to 18%. * **Sensex:** ~83,739 (+2.54%) * **Nifty 50:** ~25,727 (+2.55%) * **INR Strength:** Rupee posted its best single-day gain in years, trading near **90.26 per USD**. **💥 Crypto: Flash Crash** Digital assets suffered a "bloodbath" triggered by geopolitical fears and mass liquidations ($2.5B wiped out). * **Bitcoin (BTC):** Plunged to lows of **$73,000**, now down ~40% from October peaks. * **Ethereum (ETH):** Broke support, trading near **$2,220**. * **Sentiment:** Extreme Fear; investors fleeing to cold storage and traditional safe havens. **🛢 Commodities: Safe Haven Bid** Gold and oil are catching sharp bids as capital flees risk assets. * **Gold:** Reclaimed the **$5,050/oz** level (+2.18%). * **Crude Oil (WTI):** Trading up at **$63.64/bbl** (+0.68%) on supply concerns. **📅 Key Watchlist** * **Geopolitics:** Monitoring US Navy/Iranian drone incidents in the Arabian Sea. * **Central Banks:** Fed rhetoric shifting as inflation concerns resurface alongside growth divergence. * **Earnings:** Tech earnings digestion continues to weigh on US futures.

Cipla Share Price Live Updates: Stock Performance Overview

**Global Market Brief | February 4, 2026** **US Markets Slide as Tech Falters** Wall Street faced significant headwinds on Tuesday, with major indices pulling back as investors rotated out of the technology sector. The **S&P 500** declined by **0.84%** to settle at **6,917.81**, while the tech-heavy **Nasdaq Composite** took a harder hit, dropping **1.43%** to **23,255.19**. The **Dow Jones Industrial Average** also retreated, shedding approximately **166 points** (**-0.34%**) to close at **49,240.99**. Market volatility is visibly rising, with the **VIX** spiking over **10%** to reach **18.00**, signaling growing investor unease amidst a flood of corporate earnings and macroeconomic uncertainty. **Tech Sector Under Pressure** The "Magnificent" tech giants dragged market sentiment lower. **Nvidia** slipped nearly **3%**, and **Microsoft** fell **1.6%**, reflecting broader concerns over valuation and capital expenditure in the AI space. Conversely, **Palantir** surged over **6%**, bucking the trend, while **Disney** faced a sharp selloff of roughly **7.4%**. **ASX 200 Defies Rate Hike** In the Asia-Pacific region, the Australian market showed resilience. The **S&P/ASX 200** gained **0.89%** to close at **8,857.1** (with intraday trading pushing above **8,930** on Wednesday). This positive performance came despite the **Reserve Bank of Australia (RBA)** delivering its first interest rate hike in two years. The central bank raised the cash rate by **25 basis points** to **3.85%**, citing reaccelerating inflation. Investors largely shrugged off the tightening, buoyed by strength in the mining and banking sectors. **Commodities: Precious Metals Rebound** After a period of extreme volatility, precious metals staged a convincing recovery. **Gold** prices climbed back above the **$5,000** mark, trading near **$5,047 per ounce**, a gain of roughly **2%**. **Silver** also saw strong buying interest, rebounding to approximately **$87.46**. Energy markets remain soft but stable. **Brent Crude** hovered around **$67.90** per barrel, while **WTI** traded near **$63.79**. Oil prices have been capped by easing geopolitical fears and demand concerns, though they have stabilized following earlier steep declines. **Key Macro Drivers** **Federal Reserve Leadership:** Markets are digesting President Trump's nomination of **Kevin Warsh** as the next Federal Reserve Chair. Viewed as a "hawk," his nomination has prompted a recalibration of rate cut expectations. **Data Delays:** A partial US government shutdown is complicating the economic picture, causing delays in critical labor data releases, including the highly anticipated non-farm payrolls report. **Geopolitics:** Tensions between the US and Iran remain a focal point, though recent diplomatic talks have slightly eased immediate fears of supply disruptions, keeping a lid on oil price spikes. **Outlook** Investors should brace for continued choppiness as the market processes the dual headwinds of a hawkish Fed pivot and mixed corporate earnings. With volatility indices rising and critical economic data delayed, near-term visibility remains low.

Wipro Share Price and Recent Returns Overview

**GLOBAL MARKET BRIEF: Wednesday, February 4, 2026** **Equities: Volatility Follows Historic Rallies** Global markets are trading with heightened volatility today as investors digest a mix of geopolitical shifts and sector rotations. Following a massive Monday rally where the Dow Jones surged **515 points**, US indices pulled back in the latest session. The tech-heavy Nasdaq dropped **1.43%** and the S&P 500 lost **0.84%** overnight, driven by a sharp rotation out of technology stocks and concerns over stalled AI investments. In Asia, markets are mixed. India’s Sensex and Nifty are pausing for breath after yesterday’s historic **2.5%** surge, triggered by the newly finalized India-US trade deal. This agreement, which slashes US tariffs on Indian goods to **18%**, remains a key sentiment driver, though profit-booking is capping immediate gains. Meanwhile, broader Asian indices are flat to negative, with Japan’s Nikkei losing **0.61%** amid a lack of fresh regional catalysts. **Commodities: Gold Breaks Records** Precious metals are the standout performers. Gold prices have surged past the psychological **$5,000 per ounce** mark, gaining over **1%** intraday and **6%** earlier in the week. Safe-haven demand is spiking due to renewed geopolitical tensions in the Middle East and uncertainty surrounding the partial US government shutdown. Silver is tracking gold’s ascent, trading firmly above **$85 per ounce**, while oil prices remain steady. Brent Crude is hovering near **$67 per barrel**, supported by supply concerns but capped by doubts over global demand growth. **Crypto: Bearish Momentum Persists** The cryptocurrency sector is under significant pressure. Bitcoin has slipped **2.4%** to trade around **$76,600**, struggling to find support as momentum shifts downward. Ethereum has seen steeper declines, dropping **4%** to approximately **$2,258**. Market sentiment is being weighed down by a lack of new liquidity inflows and broader risk-aversion in speculative assets. **Key Economic Drivers** * **US Fed Chair Nomination:** President Trump’s nomination of Kevin Warsh as the next Federal Reserve Chair has introduced uncertainty. Markets view Warsh as potentially more hawkish, tempering expectations for aggressive rate cuts later this year. * **Data Delays:** Investors are flying partially blind as the release of the crucial US January jobs report has been delayed due to the ongoing government shutdown. * **Trade Relations:** The India-US trade pact is providing a structural floor for emerging market sentiment, counteracting some of the gloom from the US tech sell-off. **Market Outlook** Traders should expect choppy conditions to persist throughout the midweek session. The focus remains on whether the "real economy" sectors can sustain the rallies seen earlier this week or if the tech weakness will drag broader indices lower. Watch for support levels in the S&P 500 and continued volatility in gold as geopolitical headlines evolve.

ONGC Stock: Analysis of Monthly Performance and Market Trends

**Global Market Snapshot: February 4, 2026** **US Markets Stumble on Tech Weakness** Wall Street faced a sharp pullback yesterday, driven by a sell-off in major technology stocks and renewed concerns over AI capital expenditures. The **Nasdaq Composite** led the decline, dropping **1.4%** to close at **23,255**, while the **S&P 500** fell **0.8%** to **6,918**. The **Dow Jones Industrial Average** showed more resilience but still slipped **0.3%**, settling at **49,241**. **Sector Watch & Earnings Volatility** investors are rotating out of high-growth tech names amid mixed earnings reports. **Microsoft** shares faced pressure despite beating revenue estimates, as tempered guidance for its Azure cloud unit and massive AI spending spooked traders. Conversely, **Palantir** surged on robust AI-driven revenue growth, highlighting the market's selective appetite for clear AI monetization. Disappointments weighed heavily elsewhere: **PayPal** plummeted nearly **20%** following weak guidance, and **Gartner** slid on earnings misses. **Apple** remains a bright spot, having recently reported record Q1 revenue of **$143.8 billion**, driven by unprecedented iPhone demand. **Geopolitics & Commodities** Oil prices spiked sharply, with **Brent Crude** rising **2.6%** to approximately **$68 per barrel**. Tensions in the Middle East escalated after reports that the US Navy intercepted an Iranian drone, renewing fears of supply disruptions. In bond markets, the **10-year Treasury yield** climbed to **4.28%**, adding further pressure to equity valuations as borrowing costs tick upward. **Global Sentiment: The India Rally** While US markets cooled, Indian equities are digesting a historic surge. The **Sensex** rallied over **2,000 points** yesterday, driven by optimism surrounding a new **India-US trade agreement**. Traders are now bracing for potential volatility and profit-taking in today's session following the massive run-up. **What to Watch Today** * **Alphabet (Google)** is set to report earnings today, a critical test for the digital ad market and AI search competition. * **Amazon** earnings are scheduled for tomorrow, February 5. * **Geopolitical updates** regarding the Middle East and US-Iran relations remain a key risk factor for energy markets.

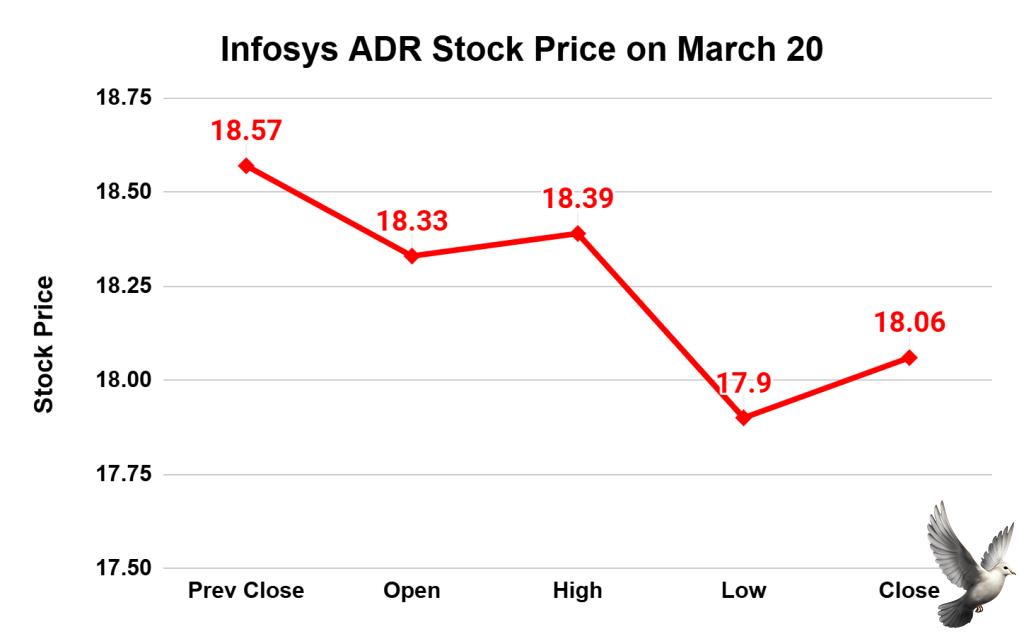

Infosys, Wipro US ADRs Slide up to 6%

**Market Brief: IT Sector Volatility & AI Disruption Fears** **Overnight ADR Sell-Off** Indian IT majors **Wipro** and **Infosys** are facing renewed selling pressure today following a sharp decline in their American Depository Receipts (ADRs) on Wall Street overnight. * **Infosys ADRs** slumped **5.6%** to close at **$17.32**. * **Wipro ADRs** fell **4.8%** to end at **$2.56**. **The AI Trigger** The sudden bearish sentiment stems from **Anthropic’s launch** of a new AI agent designed specifically for legal and compliance workflows. Unlike previous tools that merely assisted humans, this new "agentic" AI automates complex tasks like contract review, due diligence, and regulatory triage. **Sector-Wide Contagion** Investors are reacting to fears that advanced AI is shifting from a productivity enhancer to a direct competitor for core BPO and IT service revenues. The sell-off was not limited to Indian firms; US-listed data and professional service giants also plunged: * **Thomson Reuters** and **Gartner** saw intraday drops of up to **25%**. * The wider **S&P North American Software Index** is facing its worst monthly decline since 2008, with analysts describing the sentiment as a "SaaSpocalypse." **Outlook & Sentiment** While the Nifty IT index showed resilience in the previous session (closing **+1.4%** on Tuesday), the overnight rout in the US signals potential volatility for Indian trading today. The narrative has quickly pivoted from "AI adoption growth" to "AI displacement risk," putting immediate focus on how IT consultancies defend their pricing power and margins in the near term. *** **I can set up a watchlist to track the live spread between these ADR prices and their NSE counterparts for you.**

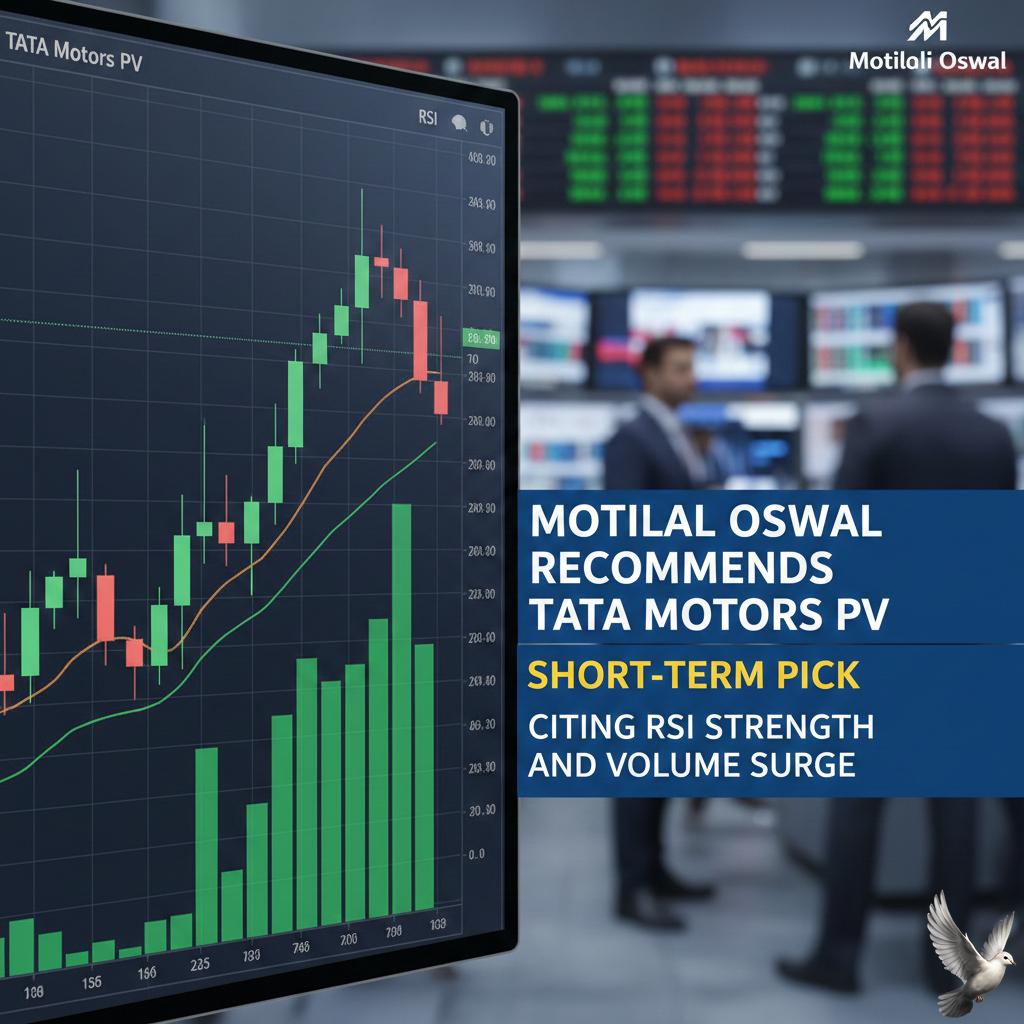

Motilal Oswal Recommends Tata Motors PV as Short-Term Pick Citing RSI Strength and Volume Surge

**Global Market Snapshot: Fed Fears & Tech Rout** **US Markets Under Pressure** US equity indices stumbled today as the Dow Jones Industrial Average slipped to **48,892** (-0.36%) and the tech-heavy Nasdaq retreated nearly **1%** to **23,461**. Market sentiment has turned fragile following the nomination of Kevin Warsh as Federal Reserve Chair, triggering anxiety over potentially tighter monetary policy and "higher for longer" interest rates. **Tech Sector & Crypto Sell-Off** The technology sector led the decline, with heavyweights like Nvidia (**-2.8%**) and Microsoft (**-2.9%**) weighing down the broader market. This "risk-off" tone spilled heavily into digital assets. Bitcoin plunged to **$77,324**, its lowest level since April, driven by over **$1.5 billion** in ETF outflows last week and a wave of leveraged liquidations. **Commodities Face Correction** Safe-haven assets were not spared. Gold prices underwent a sharp correction, dropping **1.5%** to trade around **$4,793** per ounce as the dollar strengthened. Energy markets also softened, with WTI Crude Oil falling to **$63.88** per barrel. The drop in oil follows reports of renewed US-Iran diplomatic talks and a strategic agreement where India committed to reducing Russian oil imports. [Image of WTI crude oil price chart] **Trade & Economic Shifts** Geopolitical plates are shifting with the announcement of a new US-India trade pact, seeing US tariffs on Indian goods cut to **18%**. Despite this positive global development, domestic concerns over a potential partial US government shutdown continue to inject volatility into the trading session. No relevant YouTube video found in the search results.

Data Service Stocks Drop Up to 10% as Anthropic Enters Legal Market

Market volatility surged on Tuesday, February 3, 2026, as the legal tech and data services sectors faced a localized "flash crash." The sharp downturn was triggered by Anthropic’s release of a specialized AI automation tool designed for corporate legal departments. Investors reacted with significant selling pressure, fearing the new tool could disrupt the high-margin business models of established information giants. The sentiment shifted toward "sell first, ask questions later," as traders weighed the threat of AI automation against proprietary legal databases. **Major Stock Movements** The impact on European and North American markets was immediate and severe. RELX Plc, the parent company of LexisNexis, saw its US-listed shares plunge 14.6%. Wolters Kluwer NV experienced a similar decline, with its stock dropping over 11% in European trading and a comparable slide in its ADRs. Thomson Reuters Corp. was among the hardest hit, with its share price tumbling 19% on the Toronto Stock Exchange and over 14.2% on the Nasdaq. The contagion spread to broader data service and software providers. Pearson dropped 6.2%, while Sage Group fell 5.5%. Credit reporting agency Experian and the London Stock Exchange Group both saw declines exceeding 8%, marking the latter's largest single-day drop in nearly five years. **The Disruptive Catalyst** The source of the market anxiety is Anthropic’s new legal plugin for its "Claude Cowork" suite. Unlike general-purpose chatbots, this tool is specifically engineered to automate high-volume legal workflows. Its capabilities include: - Automated contract review and risk flagging - Triage of non-disclosure agreements (NDAs) - Drafting of legal briefs and briefings - Generation of templated responses and compliance workflows While Anthropic clarified that the tool does not provide formal legal advice and requires review by licensed attorneys, the market interpreted the launch as a direct move into the "application layer." This moves AI beyond simple search and into the execution of billable professional tasks. **Sector Outlook and Sentiment** Analysts noted that the sell-off reflects a growing concern over "valuation compression" in the software industry. If general AI models can replicate the workflows of legacy platforms at a fraction of the cost, premium data subscriptions may become harder to justify. Despite the panic, some market observers point to the defensive qualities of the industry leaders. Established firms like RELX and Thomson Reuters hold vast, proprietary datasets and offer legal indemnification—protections that pure-play AI models currently lack. However, for today, the prevailing narrative remains one of intense competition. The iShares Expanded Tech-Software Sector ETF dropped 4.4% in tandem with the news, as the sector enters a period of heightened scrutiny regarding its long-term viability in an AI-first economy.

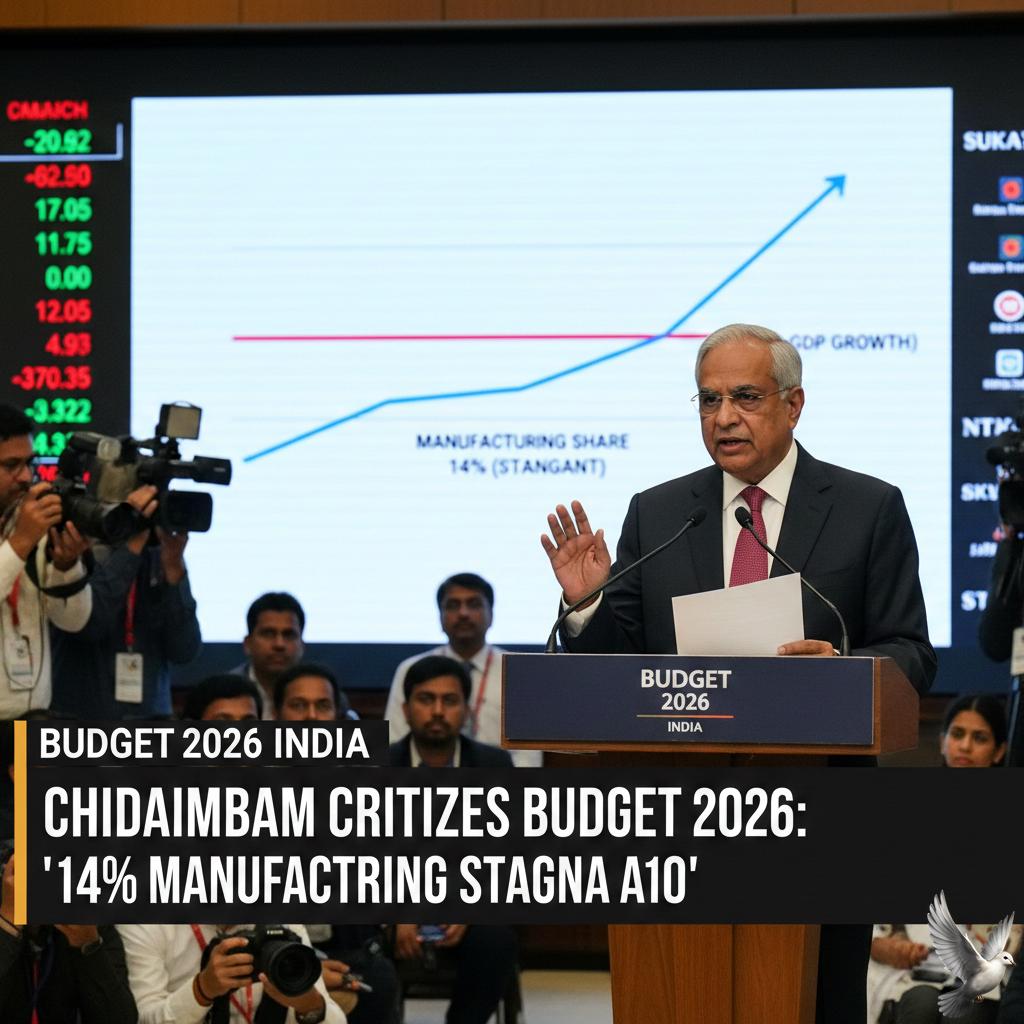

Chidambaram Cites Stagnant 14% Manufacturing Share in Critique of Budget 2026

**Market Brief: Union Budget 2026-27 Analysis & Opposition Critique** **Executive Summary** The Union Budget 2026-27, presented on February 1, 2026, has triggered a sharp divide between government projections and opposition analysis. While Finance Minister Nirmala Sitharaman positioned the budget as a blueprint for sustained growth with a **₹53.5 lakh crore** expenditure plan, former Finance Minister P. Chidambaram has labeled it a "failed test of economic strategy." **Fiscal Consolidation: Ambition vs. Reality** The government has pegged the fiscal deficit target at **4.3%** of GDP for FY27, a marginal improvement from the revised **4.4%** in FY26. However, critics argue this pace violates the Fiscal Responsibility and Budget Management (FRBM) targets. Chidambaram highlighted a discrepancy in the headline numbers, noting that despite the nominal increase in capital expenditure to **₹12.2 lakh crore**, the Centre’s effective capex as a percentage of GDP has actually declined from **3.2%** to **3.1%**. He further pointed out a shortfall of over **₹1 lakh crore** in total expenditure for the outgoing fiscal year (2025-26), questioning the credibility of the new targets. **Manufacturing Sector: Growth Narrative Under Fire** Official data estimates a nominal GDP growth of **10%** for FY27, bolstered by recent Index of Industrial Production (IIP) figures showing manufacturing growth at approximately **5.4%** to **8%** in recent months. Contrasting this, Chidambaram argues the sector remains stagnant structurally, citing the Economic Survey 2025-26. He emphasized that the budget fails to address "stress on manufacturers" caused by penal tariffs from the United States and low Gross Fixed Capital Formation, which hovers around **30%**. The disconnect between official industrial optimism and the reported closure of MSMEs remains a key point of friction. **Trade Deficit & China Exposure** A critical vulnerability highlighted in the post-budget analysis is India's widening trade deficit, particularly with China. Despite "Make in India" initiatives, dependency on Chinese imports for critical components remains high. The opposition flagged this as a strategic failure, noting the budget offered no concrete roadmap to reduce this reliance or address the ballooning deficit. This concern is amplified by global trade conflicts that threaten to weigh heavily on domestic investment and export competitiveness. **The Employment Crisis** While official unemployment rates have reportedly eased to near **5%**, the opposition has termed the job market situation "precarious," particularly for youth. Chidambaram criticized the budget for ignoring the distress in the MSME sector, which is a primary engine for job creation. The cut in allocation for flagship social schemes like the *Jal Jeevan Mission*—reportedly slashed in revised estimates—was cited as evidence of the government disconnecting from ground-level economic realities. **Market Reaction & Investor Sentiment** Market response to the budget has been mixed. Volatility in gold prices and a muted reaction in equity markets suggest investors are cautious. The hike in Securities Transaction Tax (STT) on Futures & Options (F&O) has been introduced to curb speculative trading, but it has also dampened sentiment among retail traders. **Key Takeaways for Investors** * **Fiscal Math:** Watch for slippages; the **4.3%** deficit target relies heavily on optimistic revenue receipts. * **Capex Realities:** The **3.1%** Capex-to-GDP ratio suggests government spending may not be the aggressive growth driver previously anticipated. * **Sector Watch:** Manufacturing incentives are present, but structural headwinds (tariffs, logistics) persist. * **Risk Factors:** The ignored trade imbalance with China and potential global trade wars remain significant external risks.

Zerodha Users Report Technical Issues; Company Issues Response

**Market Brief: Zerodha Outage Mars Historic Rally** **Date:** February 3, 2026 **Executive Summary** Indian equity markets witnessed a historic surge today following the announcement of a landmark India-US trade deal. However, the rally was marred for thousands of retail traders as Zerodha’s Kite platform suffered critical technical disruptions during peak volatility, preventing users from capitalizing on the gains. **Market Context: The Trade Deal Rally** Indices opened with a massive gap-up after the US administration confirmed a reduction in tariffs on Indian goods from **50%** to **18%**. * **Sensex:** Surged over **4,200 points** intraday to hit a high of **85,871**, before settling around **83,739** (+2.5%). * **Nifty 50:** Climbed **1,252 points** to an intraday record of **26,341**, closing near **25,727**. * **Key Sectors:** Textiles, Pharma, and IT stocks led the breakout, driven by the improved export outlook. **Operational Disruption** Coinciding with the market opening, Zerodha’s Kite platform faced widespread outages. Downdetector recorded a spike of over **350** complaints within the first hour of trading. * **Technical Faults:** Users reported "504 Gateway Timeouts," forced logouts, and inability to view funds after selling holdings. * **Data Integrity:** Charts reset automatically, and portfolio values displayed incorrectly or showed zero balance. * **Execution Failure:** Traders were unable to enter or exit positions during the critical opening minutes, leaving them exposed to heightened volatility. **Company Response & Status** Zerodha acknowledged the disruptions on social media, attributing them to intermittent technical issues under high load. While the brokerage stated its teams were investigating and working to stabilize the service, no specific timeline for a full resolution or compensation policy was immediately provided. By late afternoon, reports indicated the platform had begun to stabilize, though user sentiment remained critical regarding the timing of the failure.

Bitcoin Stabilizes Near $78,900 Following Liquidity-Driven Weekend Sell-Off

**Market Brief: Recovery Signals Amidst Extreme Fear** **Overview** The cryptocurrency market is staging a tentative recovery following a sharp weekend sell-off. Global market capitalization has stabilized around **$2.6 trillion**, rebounding slightly as buyers step in to defend lower support levels. Despite the bounce, broader sentiment remains fragile, heavily weighed down by macroeconomic uncertainty and institutional outflows. **Bitcoin (BTC) Performance** Bitcoin has regained footing above **$78,500**, recovering from a dip that saw it briefly test lower liquidity zones. Traders are closely monitoring the **$80,000** resistance level. Current price action suggests a "wait-and-see" approach, with volatility dampening as the market digests recent Federal Reserve signals and continued ETF outflow data. **Ethereum & Altcoins** Ethereum (ETH) is trading near **$2,400**, attempting to consolidate after double-digit percentage losses over the weekend. Select altcoins are outperforming the broader market index: * **Gainers:** Projects like **Zilliqa (ZIL)** and **Stacks (STX)** have posted double-digit recovery gains. * **Trend:** **Hyperliquid (HYPE)** and other decentralized exchange tokens are seeing increased volume, decoupling slightly from the majors. **Market Sentiment & Drivers** * **Fear & Greed Index:** Stalled at **17 (Extreme Fear)**, indicating that despite the price stabilizing, investor confidence is critically low. * **Liquidity:** Trading volumes have thinned following the weekend rout, typical of a consolidation phase. * **Macro Influence:** "Fed worries" regarding interest rate paths continue to suppress risk-on appetite. * **Institutional Flows:** Analysts note that while retail sentiment is bearish, institutional activity remains mixed, effectively masking deeper "crypto winter" conditions. **Key Watchlist** * **$80,000 BTC:** The critical psychological barrier for confirmed bullish reversal. * **ETF Flows:** Net outflows in spot ETFs remain a primary drag on momentum. * **Fed Commentary:** Upcoming statements from US central bank officials are expected to dictate near-term volatility.

Gold and Silver Market Outlook and Strategy Following $7 Trillion Selloff

**Market Brief: Historic Precious Metals Crash & Outlook** **Global Market Rout** Gold and silver markets have suffered a historic collapse, erasing an estimated **$3 trillion to $7 trillion** in value within days. Following a parabolic rally to record highs, aggressive selling pressure has triggered a massive leverage reset, wiping out speculative positions across the board. **Current Price Action (As of Feb 3, 2026)** * **Gold** has retreated significantly from its peak of over **$5,300/oz**. Current spot prices are hovering near **$4,960/oz** (Global) and roughly **₹1.47 Lakh per 10g** (India MCX), marking a sharp correction of nearly **6-10%** in just a few sessions. * **Silver** faced a more brutal sell-off, plunging **25% to 40%** from its recent highs. Prices have slipped to approximately **$88/oz** (Global) and **₹2.67 Lakh per kg** (India MCX), with volatility reaching levels not seen in decades. **Why The Crash Happened** The sudden reversal was triggered by a "perfect storm" of liquidity draining events: 1. **Margin Hikes:** The CME Group raised margin requirements **5 times in 9 days**, forcing highly leveraged traders to liquidate positions immediately. 2. **Fed Policy Shift:** The nomination of Kevin Warsh (a known hawk) as Federal Reserve Chair sparked a dollar rally, dampening demand for non-yielding assets. 3. **Profit Taking:** After months of vertical gains, institutional investors capitalized on record prices, accelerating the downside momentum. **Expert Outlook** Despite the carnage, analysts from **UBS** and **deVere Group** maintain that the structural bull market for gold is intact. They view this as a necessary "leverage flush" rather than a trend change. * **Gold:** Remains a buy-on-dip candidate as central bank demand and fiat currency concerns persist. * **Silver:** Requires extreme caution. With industrial demand cooling and technical damage severe, analysts warn it is **"too early"** to re-enter, suggesting the metal needs a longer consolidation period before becoming attractive again.

Britannia Industries Share Price: Live Market Updates

**GLOBAL MARKET BRIEF: FEBRUARY 03, 2026** **🚨 Macro Sentiment: Fed Shift & Shutdown Jitters** Global markets are navigating a complex landscape dominated by political shifts and monetary policy uncertainty. The nomination of **Kevin Warsh** as the next Federal Reserve Chair has triggered a Dollar rally, as investors price in a potentially more hawkish stance compared to the Powell era. Simultaneously, a partial **US government shutdown** is disrupting the release of key economic indicators, including critical jobs data, leaving the market temporarily flying blind. **📉 Equities: AI Doubts Weigh on Tech** US indices are facing headwinds as scrutiny over Artificial Intelligence capital expenditure intensifies. * **S&P 500 & Nasdaq:** Futures are sliding, driven by renewed skepticism regarding the immediate ROI of massive AI infrastructure spending. * **Global Performance:** European stocks (DAX, FTSE) are attempting to stabilize, while Asian markets show mixed results. Japan's Nikkei remains volatile amid shifting currency dynamics. **₿ Crypto: Bearish Breakout** Digital assets are under significant pressure, erasing recent gains as capital inflows stall. * **Bitcoin (BTC):** Has broken major support, trading below the psychological **$80,000** level (currently ~$78,726). * **Ethereum (ETH):** Struggling near **$2,166**, weighing heavily on the broader altcoin market. * **Solana (SOL):** Dropped below $100 for the first time in nearly 300 days. * **Trend:** Institutional selling and a "risk-off" environment are driving the current correction, with analysts eyeing the $70k–$74k zone for potential support. **🛢 Commodities: Volatility Spikes** The commodities sector is reacting violently to geopolitical updates and the stronger Dollar. * **Gold:** After a steep sell-off, prices have rebounded sharply, climbing **3%** to trade around **$4,921/oz**. Volatility is higher than Bitcoin in recent sessions. * **Silver:** Up over 10% on the day to **$87.54**, recovering from a near-month low. * **Oil:** Crude prices have plunged **5%** (Brent ~$65.62, WTI ~$61.56). The drop follows reports of de-escalating tensions between the US and Iran, alongside a new trade deal announcement between the US and India involving Russian oil restrictions. **📅 Key Watchlist** * **Central Banks:** Reserve Bank of Australia (RBA) interest rate decision is the immediate focus for APAC traders. * **US Fiscal:** Updates on the government funding impasse will drive short-term sentiment. * **Earnings:** Continued focus on Mega-cap Tech earnings to gauge the durability of the AI trade. **Summary:** Investors should brace for elevated volatility across all asset classes as the market digests the "Warsh Fed" regime change and ongoing fiscal dysfunction in Washington. Cash preservation and hedging strategies are currently favored over aggressive risk-taking.

ICICI Bank Share Price: Live Performance Updates

**MARKET BRIEF: 03 FEBRUARY 2026** **Global Equities Surge on Trade Optimism** Global markets are rallying today, driven by a historic trade agreement between the US and India. The deal, announced late Monday, slashes reciprocal tariffs on Indian goods from **25%** to **18%**, triggering a massive risk-on sentiment across Asia. **India** is leading the charge, with the **Sensex** skyrocketing over **4,200 points (+5.14%)** to trade near **85,870**, and the **Nifty 50** surging past **26,300**. **US markets** closed higher yesterday, shaking off government shutdown concerns. The **Dow Jones** climbed **1.05%** to **49,407**, while the **S&P 500** added **0.54%** to reach **6,976**. **Asian indices** followed suit, with South Korea’s **Kospi** rebounding **5%** and gains observed in Japan’s **Nikkei** and Hong Kong’s **Hang Seng**. **Commodities: Precious Metals Crash** Gold and silver prices have collapsed as risk appetite returns and the US dollar firms. * **Gold** plunged significantly, trading globally around **$4,781 per ounce** (down ~1.7%). In domestic Indian markets (MCX), prices crashed by nearly **₹10,000**, hitting lower circuits and trading near **₹1.52 lakh per 10g**. * **Silver** faced a steeper sell-off, plummeting **6–12%** in various markets to trade below **$116 per ounce**. **Oil** remains volatile but relatively stable, with **Brent Crude** hovering between **$66** and **$70 per barrel**, influenced by OPEC+ production decisions and the ongoing US fiscal standoff. **Crypto: Bitcoin Enters Bear Market** The cryptocurrency sector is under heavy pressure. **Bitcoin (BTC)** has dropped approximately **12%** recently, trading around **$71,060**. The asset is struggling to reclaim the **$80,000** level, with analysts citing significant institutional outflows and a "bear market" technical entry after falling **40%** from record highs. **Corporate Highlights** **Disney** reported strong Q1 FY26 results, bolstered by box office blockbusters. *Zootopia 2* and *Avatar: Fire and Ash* both surpassed **$1 billion** globally, driving streaming and park revenue. **Tyson Foods** saw a **5.1%** sales increase but reported a sharp **48%** drop in operating income, highlighting margin pressures despite volume growth. **Super Micro Computer** is set to report earnings today, with markets watching closely for updates on AI infrastructure demand. **Economic & Geopolitical Watch** **US Government Shutdown:** The US federal government has entered a second shutdown period due to budget disagreements. However, markets are largely looking past this, focusing instead on trade diplomacy. **India Union Budget:** The market's euphoric reaction today also factors in the growth-oriented policies from the Union Budget presented on February 1, which, combined with the US trade deal, has ignited "animal spirits" in the economy.

Infosys Share Price and Market Update

**Global Market Brief: February 3, 2026** **Equities: Tech Weighs on Wall Street** US markets opened on a subdued note this Tuesday, with major indices struggling for direction. The **S\&P 500** slipped **0.2%** to approximately **6,939**, while the **Dow Jones Industrial Average** shed **173 points** to trade near **48,892**. The tech-heavy **Nasdaq Composite** also declined **0.2%** to **23,462**, dragged down by large-cap weakness. Investors are digesting mixed corporate earnings and lingering concerns over a potential AI market bubble. While **Meta Platforms** rallied nearly **10%** on strong results, **Microsoft** faced selling pressure. The market is also assessing the nomination of **Kevin Warsh** as the next Federal Reserve Chair, whose perceived hawkish stance has sparked debates about future monetary policy independence. **Commodities: Gold Shines, Oil Tumbles** Safe-haven assets are outperforming riskier trades. **Gold** prices staged a robust recovery, rising over **1.3%** to reclaim the **$4,800 per ounce** level, driven by dollar volatility and geopolitical uncertainty. **Silver** saw even sharper gains, jumping nearly **6%** to **$83.19**. Conversely, energy markets faced a steep sell-off. **WTI Crude** plummeted approximately **5%** to **$62 per barrel**—its lowest level in six months. The drop follows reports of renewed diplomatic talks between the US and Iran, which have significantly reduced the risk premium associated with Middle East supply disruptions. [Image of crude oil price trend chart] **Crypto: Bitcoin Under Pressure** Digital assets remain in a corrective phase amidst the broader risk-off sentiment. **Bitcoin** dipped below **$78,000**, trading down roughly **2–5%** as ETF outflows and leveraged liquidations weigh on prices. The broader crypto market followed suit, with **Ether** and **Solana** posting notable declines as capital rotated back into traditional defensives like precious metals. **Geopolitics & Economy** Geopolitical tensions are easing in key regions, contributing to the slump in oil prices. The Trump administration announced a reduction in tariffs on Indian goods to **18%**, signaling improved trade relations. Meanwhile, the resumption of US-Iran negotiations has calmed immediate fears of a wider regional conflict. Market participants are now awaiting further clarity on the US labor market, although upcoming data releases face potential delays due to the partial government shutdown. [Market Summary: Gold Price Forecast](https://www.google.com/search?q=https://www.youtube.com/watch%3Fv%3DFjIu00uIn8Y) This video provides a technical analysis of the current gold market rally and price targets, relevant to today's sharp recovery in precious metals.