Bullish News

Collection

Global Fund Inflows to Indian Equities Reach $2.1 Billion Amid Improved Earnings Outlook

Foreign capital is flooding back into Indian equities at the highest velocity seen in nearly a year. After a volatile start to 2026, foreign portfolio investors (FPIs) have turned into aggressive net buyers, injecting over **₹33,487 crore** (approximately **$4 billion**) into the capital markets during the first half of February alone. This surge marks the strongest fortnightly buying since April 2025. It effectively reverses the heavy selling pressure seen in late 2025 and January 2026, when global funds pulled out more than **₹35,000 crore** due to valuation concerns and shifting US bond yields. The primary catalyst for this shift is a landmark **India-US trade deal** finalized in early February. Under this agreement, reciprocal tariffs on Indian goods have been slashed from **25% to 18%**, significantly boosting the competitive edge for Indian exporters. Goldman Sachs analysts suggest this deal could provide an incremental growth boost of **0.2 percentage points** to India's GDP. The market has reacted with optimism, viewing the deal as a "generational reset" that reduces supply chain uncertainty and strengthens the "China plus one" manufacturing narrative. Corporate health is providing a solid floor for this rally. Third-quarter earnings have stabilized, with banks and financial institutions reporting robust balance sheets. Financial services and capital goods have emerged as the top sectors for foreign inflows, attracting **₹6,175 crore** and **₹8,032 crore** respectively this month. Broader economic indicators remain resilient despite global headwinds. India's real GDP is projected to grow by **7.4%** for the 2025-26 fiscal year. While the Nifty 50 and Sensex have faced tactical corrections—closing at **25,178** and **81,287** respectively in the final session of February—the long-term outlook is supported by a "Strong Recovery" phase. Inflation is trending toward the RBI’s **4%** target, currently hovering near **3.9%**. Additionally, India’s foreign exchange reserves remain a formidable buffer at approximately **$701 billion**, providing enough cover for 11 months of imports. Investors are now rotating capital away from services-heavy segments into capital-intensive sectors. While IT has faced temporary headwinds due to AI disruption fears, the overall momentum is being sustained by strong domestic consumption, which is estimated to rise to **7.7%** year-on-year. [FPI Inflow Trends](https://www.youtube.com/watch?v=gBWVd4ALqIg) This video provides a breakdown of the 18% tariff reduction and identifies the specific sectors poised to benefit most from the new trade landscape. http://googleusercontent.com/youtube_content/0

Britannia Share Price and Trading Volume Updates

Global Market Brief: February 27, 2026 Equity markets are navigating a period of intense consolidation as the final trading days of February reveal a sharp divide between sectors. While the **Dow Jones Industrial Average** managed a fractional gain of **17.05 points** to settle at **49,499.20**, the tech-heavy **Nasdaq Composite** faced significant pressure, sliding **1.2%** to finish at **22,878.38**. This divergence highlights a shift in investor sentiment away from high-growth technology names toward more cyclical areas of the economy. The **S&P 500** also retreated, falling **0.5%** to **6,908.86**. Much of the downward momentum was driven by a sharp sell-off in the semiconductor space. **Nvidia** shares tumbled more than **5%**, marking its worst single-day performance since last spring. Despite reporting a fourth-quarter revenue beat, the market's reaction suggests that investors are increasingly wary of valuation extremes and the sustainability of the artificial intelligence trade. Commodities and Energy Energy markets are currently defined by geopolitical jitters. **Brent crude** is trading near **$71.27** per barrel, while **WTI crude** holds at **$66.69**. Prices experienced a mid-week dip following a substantial jump in U.S. crude inventories, yet they recovered slightly as traders monitor high-stakes nuclear negotiations in Geneva. Analysts note a "weekend risk" premium, with potential outcomes ranging from a diplomatic breakthrough to renewed supply constraints. Precious metals continue to act as a primary hedge against uncertainty. **Spot gold** remains resilient above the **$5,000** threshold, currently positioned near **$5,168** per ounce. The rise of tokenized assets has added a new layer of liquidity to the market, with digital gold products now seeing trading volumes that rival traditional ETFs. Monetary Policy and Digital Assets The **Federal Reserve** has maintained the benchmark interest rate in the **3.5% to 3.75%** range. Under the leadership of the new chair, the central bank appears to be transitioning from an active easing cycle to a "higher-for-longer" hold. Economic data shows a cooling but resilient labor market and inflation hovering near **2.7%**, which has led markets to price in a lower probability of a rate cut in the immediate future. In the digital asset space, **Bitcoin** is exhibiting sideways movement, trading at approximately **$67,452**. While institutional forecasts for the year remain bullish—with some targets reaching **$150,000**—the short-term outlook is cautious. The market is currently seeking a clean break above the **$72,000** resistance level to confirm a new uptrend. Emerging Markets and Outlook International sentiment remains mixed. India's **Nifty 50** closed flat near **25,500** as the country prepares to release its **Q3 GDP** data. Despite global volatility, domestic institutional buying has provided a floor for emerging market equities. The broader global economic forecast for 2026 remains steady at **2.9%** growth, supported by a recovery in manufacturing and easing trade headwinds in the Eurozone and Asia.

Titan Company Closes at Rs 4325.0

Market Overview: February 27, 2026 Global financial markets are closing the week under significant pressure as geopolitical tensions and cooling sentiment in the technology sector drive a shift toward defensive assets. The **S&P 500** fell **0.54%** to **6,908.86** points, marking a volatile end to February. The **Nasdaq Composite** saw a steeper decline of **1.18%**, finishing at **22,878.38**. In contrast, the **Dow Jones Industrial Average** managed a marginal gain of **17.05** points to settle at **49,499.20**. Sector Performance and Technology The "AI trade" that fueled record highs throughout late 2025 is showing signs of exhaustion. **Nvidia** shares dropped more than **5.5%** today; despite beating earnings expectations, the results failed to satisfy high investor demands for sustained growth. The **Philadelphia Semiconductor Index** retreated **3.2%**, reflecting a broader rotation into cyclical sectors as investors reassess the immediate return on investment for large-scale AI infrastructure. Commodities and Safe Havens Gold continues to serve as a primary hedge against rising global uncertainty. Prices firmed around **$5,180** per ounce, tracking toward a seventh consecutive monthly gain. The **US 10-year Treasury real yield** has declined to **1.72%**, further supporting non-yielding bullion. In energy markets, **Brent crude** is trading near **$70.58** a barrel, while **WTI crude** sits at **$65.03**. Prices remain sensitive to the stalled nuclear negotiations in Geneva and escalating border tensions in South Asia. Monetary Policy and Interest Rates Central banks are adopting a "wait and watch" stance. The **Reserve Bank of India** maintained its repo rate at **5.25%** this month, signaling a shift to a neutral policy. In the United States, the probability of a Federal Reserve rate cut before June has fallen to **50%**. Sticky inflation, currently hovering around **3%**, has tempered expectations for aggressive monetary easing in the first half of 2026. Emerging Markets Asian markets experienced heavy selling today. India’s **Nifty 50** dropped **1.25%** to close at **25,178.65**, while the **Sensex** tanked **961.42** points. Foreign institutional investor (FII) outflows remain a primary drag, driven by a strengthening dollar and regional security concerns. The **Indian Rupee** is currently under pressure at **91** against the US Dollar, though domestic fundamentals remain resilient with a projected GDP growth of **6.9%** for the upcoming fiscal year.

Brokerages Initiate Coverage on LG Electronics, Fractal Analytics, Hitachi, and Five Other Stocks with Up to 55% Upside

Market Overview The global financial landscape enters the final days of February 2026 defined by a sharp divergence between resilient economic growth and localized sector volatility. While global GDP is projected to expand by **2.7% to 3.3%** this year, market participants are navigating a transition from active monetary easing to a high-level hold. In the United States, economic performance remains steady with growth forecasts revised upward to **2.6%**. However, major indices show a significant rotation. Small-cap stocks in the Russell 2000 surged **5.39%** recently, outperforming the S&P 500's **1.45%** and the NASDAQ's **1.23%**. This shift reflects a move away from the heavy tech concentration that dominated previous cycles. The Tech and AI Landscape A "SaaS-pocalypse" sentiment has rattled the software sector this month. Rapid advances in autonomous AI tools have sparked fears that traditional software-as-a-service products may become obsolete. The iShares Expanded Tech-Software Sector ETF plunged nearly **30%** in February. Specific session losses were even more dramatic, with some major software firms dropping over **34%** in a single day following the release of new agentic AI solutions. Despite this turmoil, the broader "AI supercycle" is still expected to drive earnings growth of **13% to 15%** for leading hardware and infrastructure providers. Inflation and Interest Rates Global disinflation continues, with headline inflation projected to slow to **3.1%** in 2026. In the US, the Federal Reserve is expected to maintain a cautious stance, with potential rate cuts totaling **50 basis points** later this year to reach a terminal rate of **3.0% to 3.25%**. Emerging markets show varying trends. India’s headline CPI fell to **2.1%** annually, prompting the Reserve Bank of India to maintain a prolonged pause on rates. Domestic growth remains a bright spot there, with a revised FY26 GDP forecast of **7.3%**. Energy and Commodities Commodity markets are experiencing a clear split. Energy prices are under pressure due to a global supply glut. Brent crude is forecasted to average **$58** per barrel in 2026, down from previous highs. Conversely, metals are outperforming. Copper has entered a deficit of **1 million metric tons** as demand from data centers and electric vehicles accelerates. Precious metals remain highly active, with silver reaching its most overbought phase in decades and gold prices supported by central bank hedging. Key Risks and Outlook Institutional activity shows a disconnect between global and domestic flows. In several emerging markets, significant foreign selling—totaling over **₹3,400 crore** in recent sessions—is being absorbed by record-level domestic institutional buying. The primary risks for the remainder of the quarter include the refinancing of nearly **25%** of US national debt and the potential for trade policy shifts. However, the overall outlook remains cautiously bullish for global equities as corporate earnings remain robust and fiscal stimulus in the Eurozone and Japan begins to take hold.

SBI Share Price: Market Performance and Trading Volume

Market Overview: February 27, 2026 The U.S. equity markets are closing out a volatile February with the S&P 500 positioned for a monthly loss. This downward pressure follows a significant selloff in the technology sector, where even record-breaking corporate results failed to soothe investor anxiety. The S&P 500 index recently dipped to the **6,909** level, while the Nasdaq Composite fell to **22,878**. This retreat is being characterized as an "AI scare trade," with market participants rotating away from high-valued tech giants toward international markets and cyclical sectors tied to broader economic growth. Treasury Yields and Federal Reserve A sharp rally in the bond market has pushed the **10-year Treasury yield** down to **3.99%**. This move represents the best monthly performance for Treasuries in over a year, with yields tumbling roughly **25 basis points** throughout February. The Federal Reserve maintained interest rates at a target range of **3.50% to 3.75%** during its last assessment. Market expectations for a rate cut have shifted further into the future, with the probability of a reduction by June falling to **50%**. Most analysts now anticipate only one or two quarter-point cuts for the remainder of 2026. Tech Sector and Corporate Earnings Nvidia reported monumental results for its fiscal fourth quarter, with revenue hitting **$68.1 billion**, a **73%** increase year-over-year. Despite record Data Center revenue of **$62.3 billion**, shares fell over **5%** in recent trading to approximately **$184.72** as bubble concerns outweighed the growth narrative. Other notable movers include Dell Technologies, which surged **12%** on strong AI server forecasts, and Netflix, which jumped **7%** after withdrawing from a major acquisition bid. Conversely, the semiconductor industry faced broad pressure, with peers like AMD seeing shares decline. Commodities and Economic Data Gold has reached a significant milestone, trading near **$5,180 per ounce**. The precious metal is on track for its seventh consecutive monthly advance, supported by geopolitical tensions in the Middle East and Central Asia. In domestic markets, 24K gold is hovering around **₹16,157 per gram**. Crude oil remains stable near **$70.78**, despite volatility in Brent futures. On the economic front, January inflation data showed a cooling trend with the Consumer Price Index (CPI) at **2.4%** year-over-year. Retail sales have also shown resilience, marking a fourth consecutive monthly rise of **0.2%**. Global Market Sentiment While U.S. benchmarks struggle, international markets are seeing a divergence. Europe’s Stoxx 600 is tracking its eighth straight monthly advance, and Asia-Pacific indices have recorded their best February performance on record. Investors are currently balancing a resilient U.S. economy against new trade policies, including a **10%** global tariff that took effect this week. This policy shift has reignited some inflation fears, contributing to the cautious stance observed across major asset classes.

L&T Finance and Other MFI Stocks Decline Following Passage of Bihar Microfinance Bill 2026

Market Brief: Bihar MFI Regulatory Shift Shares of India’s leading microfinance-linked lenders experienced a sharp sell-off on February 27, 2026, following the passage of the Bihar Micro Finance Institutions Bill, 2026. The legislation introduced stringent oversight for a region that represents the largest microfinance market in India, holding roughly 15% of the national industry portfolio. Market Reaction and Stock Performance Major lenders with significant exposure to the state saw immediate double-digit corrections. Fusion Finance plummeted 11% to 181 INR, while Utkarsh Small Finance Bank—which holds a 46% exposure to Bihar—fell 5% to 14.10 INR. L&T Finance also shed 5% to settle at 286 INR. Other key players like Satin Creditcare and Spandana Sphoorty, which maintain exposures of 13% each, remained under intense selling pressure. Key Provisions of the 2026 Bill The new law mandates that all micro-lenders, including those already licensed by the Reserve Bank of India, must obtain separate state-level registration. Crucially, institutions are now required to seek prior approval from the state Finance Department before any loan disbursement. The bill also caps lending to a maximum of two MFIs per borrower and prohibits total interest from exceeding 100% of the principal amount. To curb aggressive collection, special courts will be established at the district level to hear borrower grievances. Sector Trends and Asset Quality The regulatory tightening comes at a time of existing stress for the microfinance sector. Data for the 2024-25 fiscal year revealed a surge in delinquencies, with loans overdue by more than 30 days jumping to 6.2% nationally. Bihar recorded the highest rate of default in the country, with 7.2% of its 57,712 crore INR outstanding loan book categorized as overdue. Analysts estimate that between 5% and 45% of MFI exposure in the state could face further delinquency as these new rules disrupt debt-cycling practices. Outlook and Regional Risk While the immediate financial impact on balance sheets may be manageable for larger entities, the "precedent risk" is the primary concern for investors. If other high-exposure states adopt similar restrictive measures, it could trigger a fundamental reassessment of growth and valuation multiples across the Small Finance Bank and NBFC-MFI space. For the 2026 fiscal year, credit growth is expected to remain moderate at approximately 4% as institutions prioritize asset-quality repair over aggressive expansion. The shift marks a transition toward a more regulated, welfare-oriented lending model. However, the requirement for state-level registration and disbursement approvals is expected to slow operational speed and increase compliance costs across the industry in the near term.

Block Shares Rise 25% Following Workforce Reductions and AI Integration Strategy

Block Inc. is executing a radical transformation to become an "intelligence-native" company, marked by a decisive reduction of its workforce by approximately 4,000 employees. This move slashes the total headcount from over 10,000 to just under 6,000, representing nearly 40% of its global staff. CEO Jack Dorsey has framed this restructuring as a proactive bet on artificial intelligence rather than a reaction to financial distress. The strategy aims to replace traditional labor with smaller, high-performance teams empowered by AI-driven automation tools, such as the company’s internal "Goose" system. The market has reacted with overwhelming optimism to this efficiency-first pivot. Block's stock surged more than 24% in recent trading sessions, reflecting investor confidence in the company’s ability to scale margins. This enthusiasm is supported by strong financial fundamentals, including a 24% year-over-year jump in gross profit to $2.87 billion in the final quarter of 2025. Total gross profit for the full year reached $10.36 billion, a 17% increase. Performance was particularly robust within the Cash App ecosystem, which saw gross profit climb 33% to $1.83 billion. The platform now serves 59 million monthly active users, while primary banking actives grew by 22% to 9.3 million customers. Management has set ambitious targets for 2026, projecting $3.20 billion in adjusted operating income and an 18% growth in gross profit. The company is also doubling down on shareholder returns, having executed $2.3 billion in share repurchases throughout 2025. This transition reflects a broader structural shift in the fintech sector. Industry data suggests the AI in fintech market will reach $17.79 billion in 2025, with organizations increasingly using intelligence tools to automate risk management, customer service, and software development. By taking a single, hard action now, Dorsey intends to avoid the morale-eroding effects of repeated "slow-drip" layoffs. The objective is to emerge as a leaner, faster organization that dictates its own growth terms rather than reacting to external market pressures. [Block's Strategic Shift](https://www.youtube.com/watch?v=eml2imnhwZg) This video provides a deep dive into Jack Dorsey's decision to cut nearly half of Block's workforce as a strategic bet on AI-driven productivity. http://googleusercontent.com/youtube_content/0

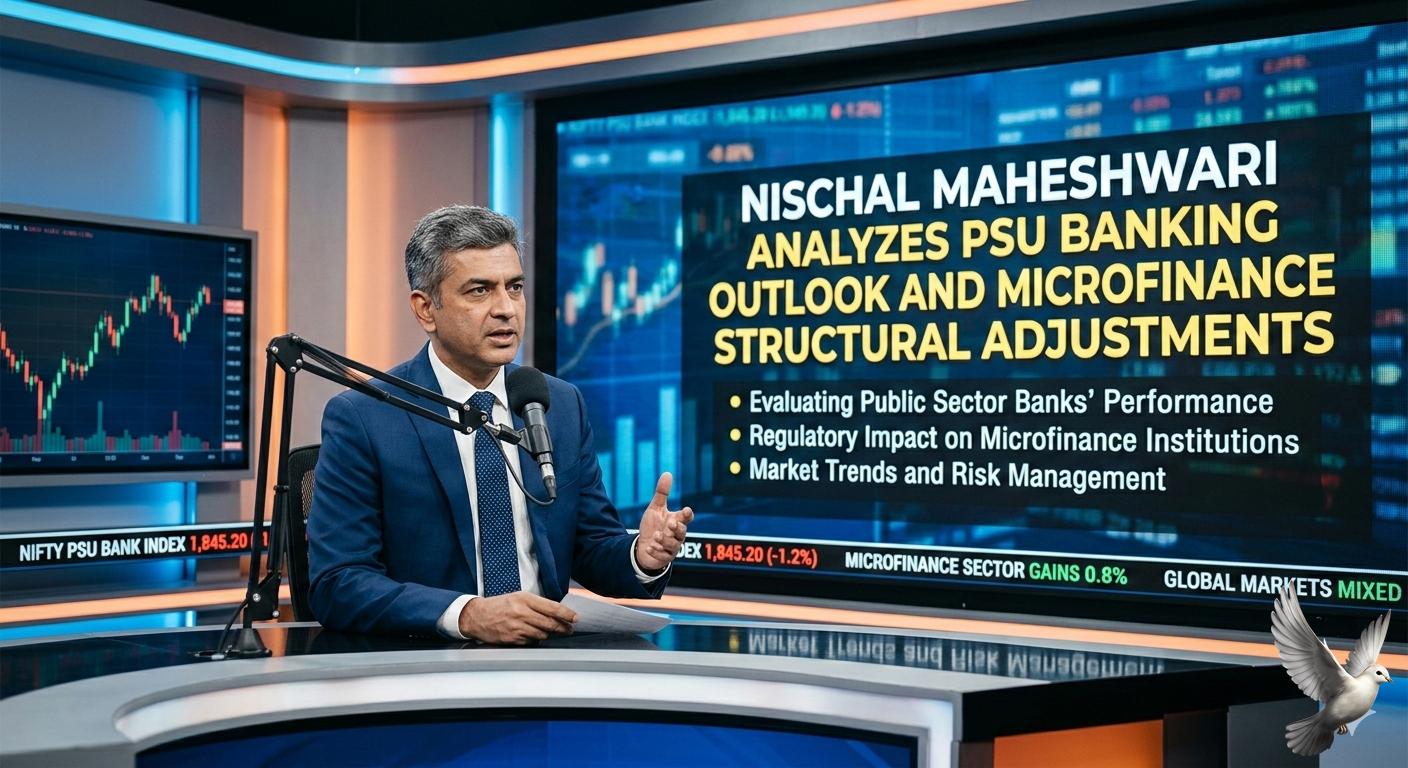

Nischal Maheshwari Analyzes PSU Banking Outlook and Microfinance Structural Adjustments

Market Outlook: High-Conviction Sector Rotation Market strategy is currently defined by a "valuation-first" approach. Investors are rotating away from overheated segments toward areas with structural tailwinds and reasonable pricing. Banking: The PSU Advantage Public Sector Undertakings (PSU) banks are currently outperforming private peers. This is driven by a significant divergence in **Credit-to-Deposit (CD) ratios**. While many large private banks are operating at tight **CD ratios of 90–92%**, PSU lenders maintain levels near **74–75%**. This provides PSU banks with substantial headroom to grow lending without the immediate pressure to raise high-cost deposits. Microfinance: Regulatory Reset The microfinance (MFI) sector is navigating a major structural shift following the **Bihar MFI Bill 2026**. This legislation mandates state registration and limits borrowers to a maximum of **two lenders**. While these rules caused immediate share price drops of **9% to 11%** for lenders with high exposure to the region, the long-term outlook is viewed as a "healthy reset." Restricting multiple loans is expected to stabilize the system and improve long-term asset quality by curbing over-leverage. Auto and Commercial Vehicles: The Renewal Cycle The automotive sector remains a primary bright spot. The **Nifty Auto index** recently reached record highs near **29,179 points**. Growth is being fueled by "replacement demand" as a major **five-year fleet renewal cycle** begins. Analysts project robust double-digit growth for February 2026, with commercial vehicle (CV) wholesales for major players expected to rise between **26% and 33%**. Energy and Power: Tactical Shifts In the power sector, product-based companies are currently considered expensive, with many stocks discounting **two to three years** of future growth. Investors are shifting focus toward Transmission and Distribution (T&D) players, which remain more reasonably priced. Additionally, upstream energy companies like **ONGC and Oil India** are emerging as tactical plays due to ongoing geopolitical risks. Defence: Priced to Perfection The defence sector, while fundamentally strong, faces a valuation challenge. Following the **Union Budget 2026**, which set capital expenditure at **₹2.19 lakh crore**, the Nifty Defence index saw a sharp correction. The market had already priced in aggressive growth, and the **21–22% year-on-year** spending increase was not enough to sustain record-high multiples. For many, the sector is now a "hold" rather than a "fresh buy." Data Centers: Structural Growth Data centers represent a high-visibility theme for the next **3 to 5 years**. India’s data center market is valued at approximately **$10.48 billion in 2025** and is projected to grow at a **CAGR of 14.6%** through 2032. Capacity is expected to surge from **1,150 MW** to over **2,000 MW by March 2027**, driven by AI integration and local data localization laws. Metals: Quarter-by-Quarter Play The metals sector requires extreme agility due to global volatility. While long-term conviction is low, the ferrous segment (steel) currently looks more attractive than non-ferrous. Copper remains a critical bottleneck for the energy transition. Projections suggest a global refined copper shortfall of **150,000 tonnes in 2026**, which could push prices toward **$13,000 per ton** by year-end.

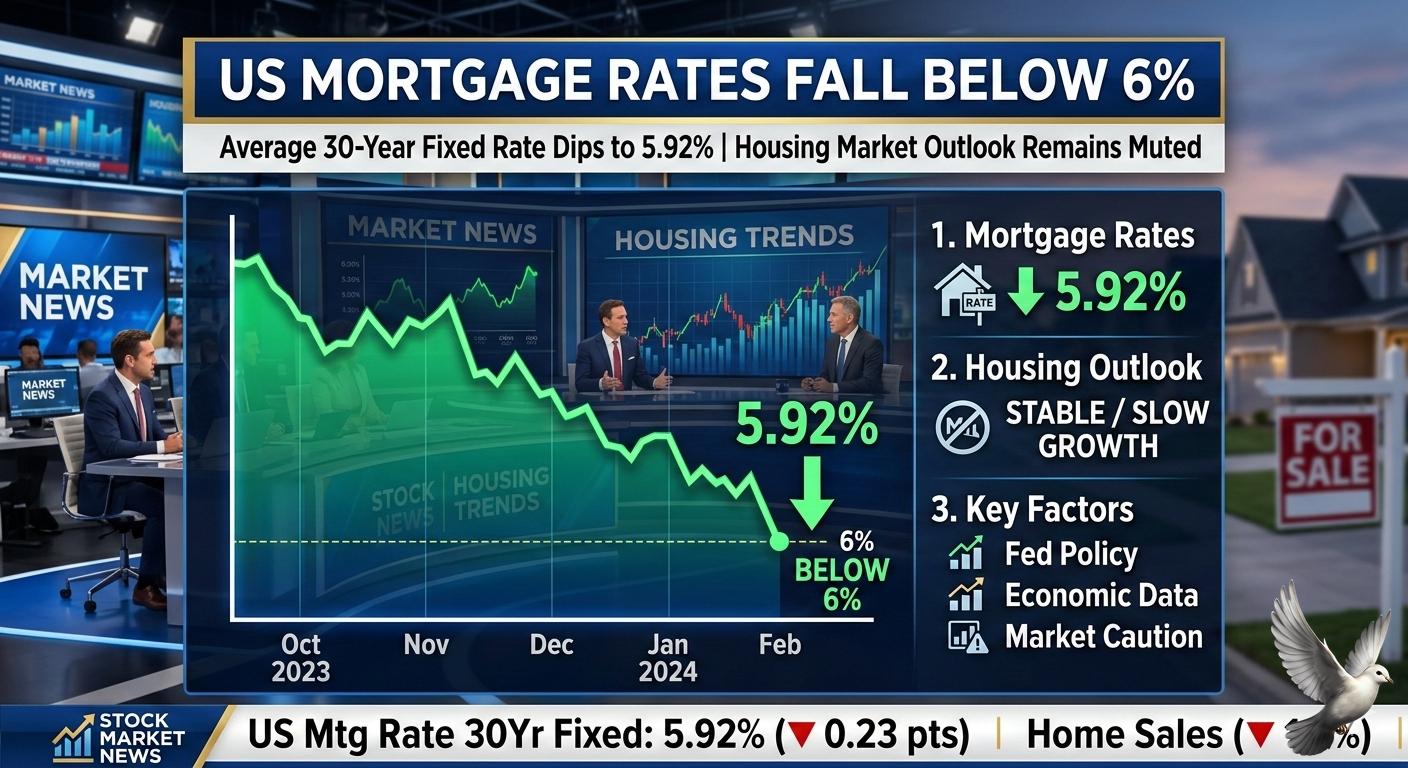

US Mortgage Rates Fall Below 6% Amid Muted Housing Market Outlook

US 30-year fixed mortgage rates have officially dropped below the 6% threshold for the first time in three and a half years. As of February 26, 2026, the benchmark rate averaged 5.98%, a notable decline from 6.01% the previous week and significantly lower than the 6.76% recorded a year ago. This shift marks the lowest borrowing cost for American homebuyers since September 2022. The 15-year fixed mortgage rate followed a different path, rising slightly to 5.44% this week. These movements are closely tracking the 10-year Treasury yield, which currently sits near 4.00% as investors move toward safer bond assets amid broader market volatility. Market analysts view the sub-6% rate as a critical psychological milestone. While the dip provides a boost to purchasing power, the housing market remains in a state of transition. Recent data shows existing home sales dropped 8.4% in January, reaching an annualized pace of under 4 million units—the slowest in over two years. Supply constraints continue to dominate the narrative. Total housing inventory sits at approximately 1.22 million units, and while this is an improvement over 2025, it remains below pre-pandemic norms. The median sales price for existing homes is currently $396,800, reflecting a 1.1% year-over-year increase despite the high-rate environment of the past year. Affordability remains a challenge for many, as nearly 69% of existing homeowners hold mortgages with rates at or below 5%. This "lock-in effect" disincentivizes selling, keeping supply tight. However, experts anticipate that if rates remain under 6%, the upcoming spring season could see a significant increase in both listings and buyer activity. Refinancing activity is already responding to the rate drop. Mortgage applications for refinancing have surged, with some indices showing a 130% increase compared to the same period last year. For a standard $400,000 home with a 20% down payment, the current rate environment translates to roughly $2,268 in annual savings compared to 2025 figures. The Federal Reserve is scheduled to meet in mid-March to discuss further interest rate policy. Current market sentiment suggests that while volatility persists, the combination of cooling inflation and government initiatives, such as the recent $200 billion mortgage-backed securities purchase order, may help sustain these lower rate levels through the first half of the year.

JGB Yields Decline Amid Portfolio Adjustment Demand

Japan's sovereign debt market saw a notable shift on Friday as 10-year government bond yields retreated to approximately 2.12%. This movement ended a three-day climbing streak and was fueled by a combination of technical portfolio adjustments and fresh economic data that cooled expectations for immediate monetary tightening. Investors moved aggressively to purchase bonds to rebalance their portfolios against market indices. This demand was intensified by a large volume of Japanese government bonds reaching maturity, prompting large-scale reinvestment into the market. Inflationary pressures in the capital showed signs of stabilization. Tokyo’s core consumer price index, which excludes fresh food, rose 1.8% in February. While this slightly exceeded economist forecasts of 1.7%, it represented the slowest pace of growth in over a year. The headline figure was significantly influenced by government utility subsidies that curbed household energy costs. The Bank of Japan remains in a complex position. While the core-core inflation metric—which strips out both fresh food and energy—remains higher at 2.5%, the headline drop below the 2% target complicates the central bank’s communication regarding future interest rate hikes. Political developments are also weighing on the market outlook. Prime Minister Sanae Takaichi recently appointed two reflationist academics to the central bank’s policy board, signaling a potential preference for maintaining supportive monetary conditions. Recent reports also suggest the Prime Minister has expressed reservations about aggressive rate increases during private meetings with Governor Kazuo Ueda. Current market pricing reflects a cautious path forward. The 2-year yield softened to 1.23%, while the 30-year yield dipped to 3.33%. Despite the current cooling, some hawkish members of the board continue to advocate for a gradual transition toward higher rates, arguing that price stability is nearing a sustainable achievement. The yen showed resilience following the data release, trading near 155.76 against the U.S. dollar. Analysts suggest the central bank will likely wait for broader national data and results from the March and April policy meetings before committing to the next phase of its normalization cycle.

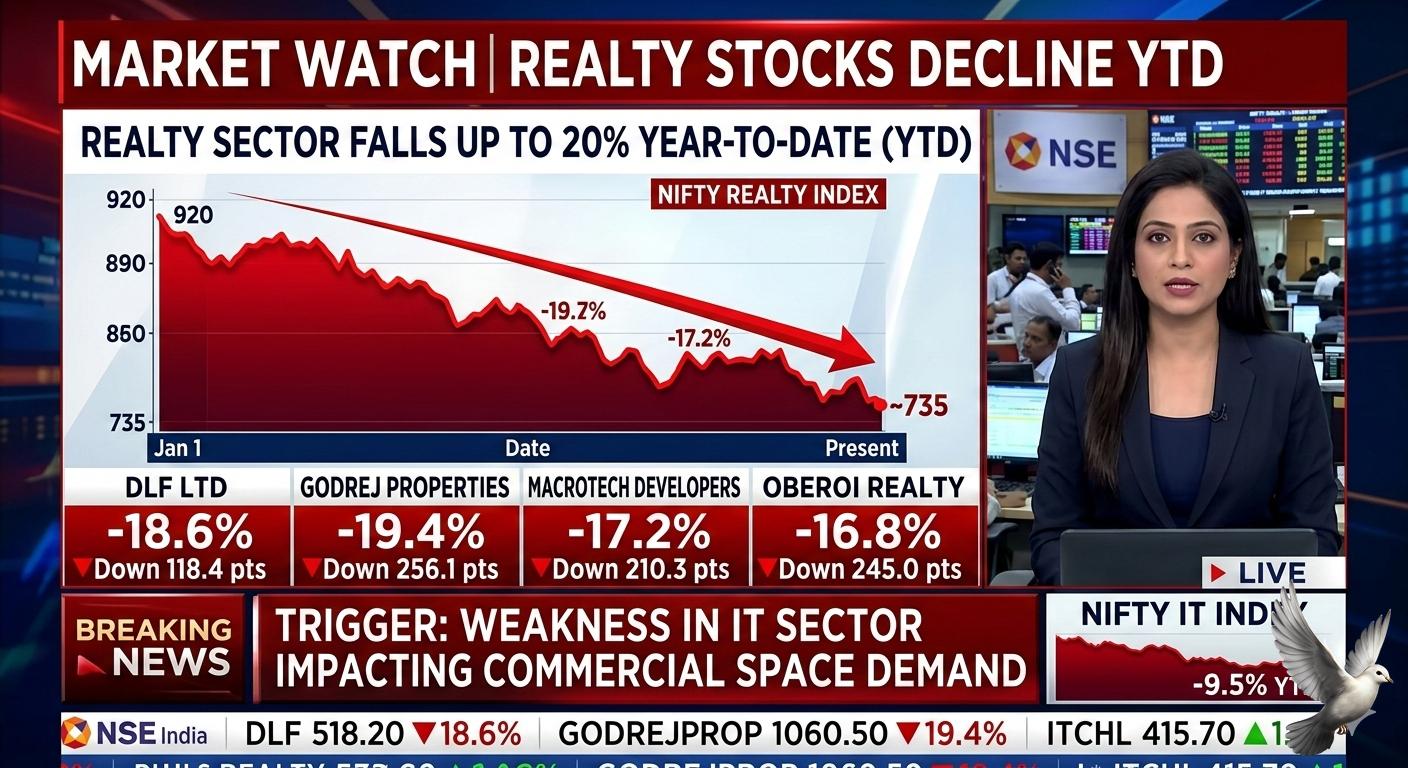

Realty Stocks Decline up to 20% Year-to-Date Amid IT Sector Weakness

Indian real estate stocks have faced a significant correction in early 2026, with the Nifty Realty index dropping nearly 12% year-to-date and falling over 26% from its previous all-time highs. This downturn has pushed the sector into official bear market territory, driven primarily by a "rub-off effect" from global technology volatility and local concerns over artificial intelligence. Investors are increasingly wary that AI-led disruption could fundamentally alter the employment landscape in India’s software industry. Because residential absorption and Grade A office leasing in hubs like Bengaluru are tied to IT services and Global Capability Centers, the prospect of slower hiring has dampened market sentiment. Sector experts note that if AI-driven efficiency gains translate into workforce reduction, the spillover into housing upgrades and commercial expansion could be substantial. The impact is most visible among developers with heavy exposure to South Indian tech corridors. Brigade Enterprises has seen the steepest decline, with shares falling more than 20% this year. Other major players including Prestige Estates and Sobha Limited have recorded losses ranging from 1% to 11%. Even national heavyweights like DLF and Godrej Properties have retreated by as much as 12% as the narrative of an IT slowdown gains momentum. Beyond the tech narrative, the sector is grappling with valuation and operational hurdles. Many real estate stocks saw their prices double over the last 18 months, leading to a phase of profit-booking as valuations outpaced fundamentals. Recent operational data has also added pressure; Oberoi Realty reported a 56% year-on-year decline in pre-sales, while other developers faced inventory shortages and administrative bottlenecks that delayed new project launches. Despite these headwinds, the broader real estate market shows signs of a K-shaped recovery. While the mid-segment faces caution due to shifting job security, the luxury segment remains resilient. Sales for homes priced above 4 crore rose nearly 28% last year, and institutional investment reached a historic high of 25,375 crore in the third quarter of 2025. This suggests that while stock prices are correcting, physical demand for premium assets and data centers continues to attract significant capital. Policy shifts are providing a localized floor for the industry. The Reserve Bank of India recently cut the repo rate by 25 basis points to 6.25%, the first reduction since 2020. This move, combined with the Union Budget’s focus on increasing middle-class spending power through tax cuts, is expected to support demand in the affordable and mid-tier housing segments in the long term. The current market environment is characterized by a transition from a broad-based rally to a period of selective consolidation. Analysts view the AI threat as a near-term overhang that may delay purchase decisions and increase financial caution among buyers. However, the structural drivers of Indian real estate—including rapid urbanization and the consolidation of the market toward organized, large-scale developers—remain intact as the industry adapts to a new technological and economic reality.

JM Financial Initiates ‘Buy’ on Urban Company and Physicswallah; Sets Upside Targets Up to 23% **

JM Financial has officially initiated coverage on newly listed internet giants Urban Company and PhysicsWallah, issuing Buy ratings for both. The brokerage highlights these companies as high-growth, scalable leaders within India’s digital economy, projecting significant upside from current levels. **Urban Company: Dominating the Gig Economy** Urban Company currently holds a commanding **60% market share** in the home services sector. The stock is trading near **₹108**, with JM Financial assigning a target price of **₹125**, implying a **16% upside**. The company recently reported a **33% revenue surge** to **₹383 crore** for the quarter ending December 2025. While it posted a net loss of **₹21 crore** for the period due to high investment costs, its core operations remain robust. A key driver for future growth is "InstaHelp," which has already crossed **50,000 daily bookings**. Analysts view this as a potential "Blinkit-like" opportunity that could revolutionize high-frequency domestic services. **PhysicsWallah: Digital Efficiency vs. Offline Scaling** PhysicsWallah has faced recent market pressure, with shares touching a low of **₹87.60**, well below its **₹109** issue price. However, JM Financial sees this as a recovery play, setting a target of **₹110** which suggests a **23.5% upside**. The edtech firm’s financial strength lies in its digital-first model. In the first nine months of FY26, revenue reached **₹2,980 crore**, already surpassing its entire FY25 performance. For the December 2025 quarter alone, the company reported a net profit of **₹102 crore** on revenue of **₹1,082 crore**. Its marketing spend remains remarkably lean at roughly **10% of revenue**, compared to the **20–30%** industry average. **Market Outlook and Risks** The broader Indian edtech sector is shifting toward "phygital" models. PhysicsWallah is aggressively expanding into K-12 schooling with a **₹400 crore** strategic pivot and the launch of its AI mentor, "Aryabhata." For Urban Company, the primary moat is its network effect across **12,000+ service micro-markets**. The company maintains a zero-debt balance sheet and a strong cash position, allowing it to absorb the current EBITDA losses associated with new category launches. Investors should note that while the digital segments of both companies show high-margin stability, scaling physical infrastructure—such as offline tuition centers for PhysicsWallah and regional service hubs for Urban Company—remains the primary execution risk. At current valuations, the brokerage views the risk-reward profile as favorable for long-term growth.

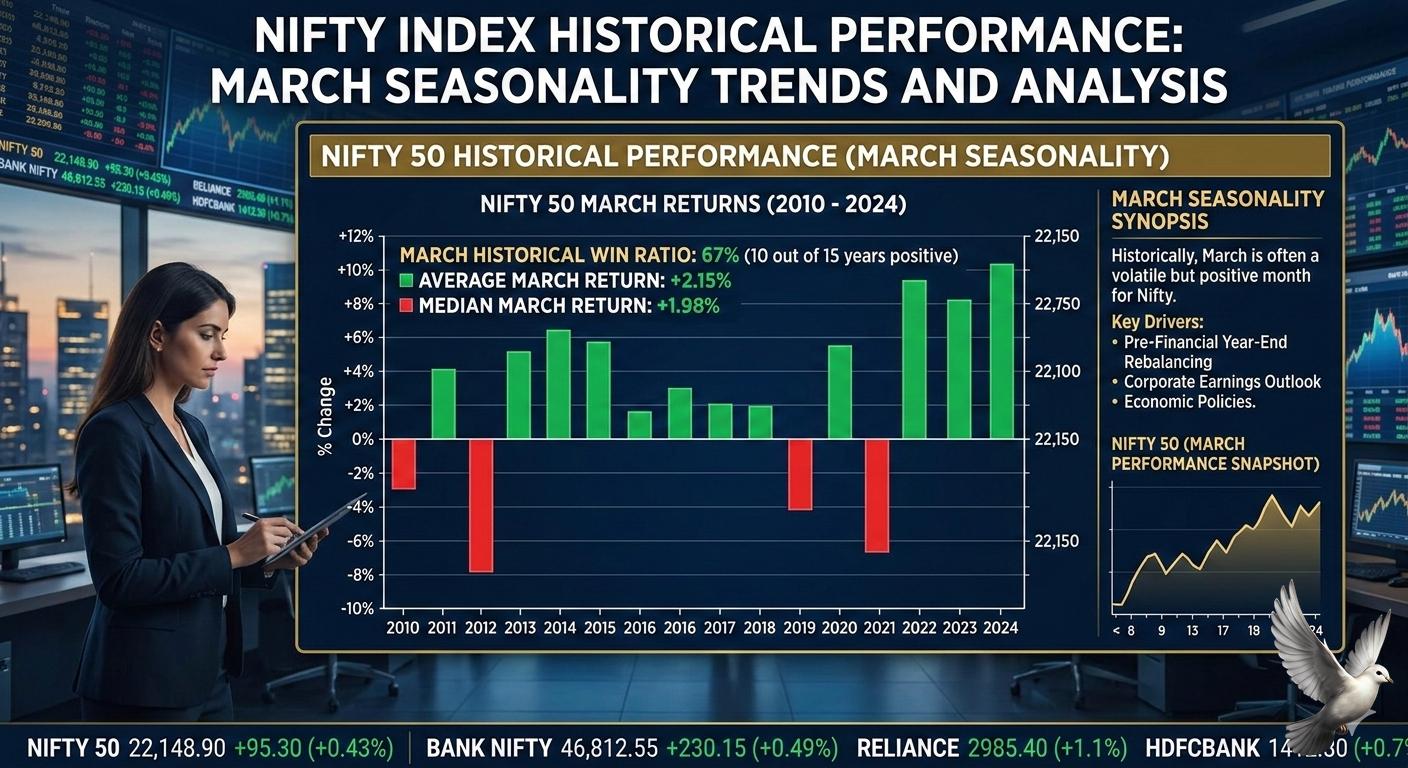

Nifty Index Historical Performance: March Seasonality Trends and Analysis

The Indian equity market enters **March 2026** backed by a decade-long seasonal strength. Historically, the Nifty 50 has closed higher in **80%** of the instances over the last **10 years** during this month. As of **February 27, 2026**, the Nifty 50 closed the final session of the month at **25,178.65**, reflecting a day-on-day decline of **1.22%**. Despite this immediate volatility, long-term trends remain supported by institutional behavior and robust economic fundamentals. Institutional Flow Dynamics Foreign Institutional Investors (FIIs) have historically been net buyers in March **70%** of the time. While global factors like US interest rates and geopolitical shifts caused intermittent selling in early 2026, FIIs have shown a recent trend of selective buying in the financial and capital goods sectors. Domestic Institutional Investors (DIIs) have been a stabilizing force, acting as net buyers in **seven out of the last 10 years**. In a historic shift recorded in **2025**, DII holdings in NSE-listed companies reached **17.62%**, officially overtaking FII holdings at **17.22%**. Macroeconomic Performance India remains the world's fastest-growing major economy. Real GDP growth for **FY26** is estimated at **7.4%**, with the third-quarter (Q3) growth projected to reach as high as **8.3%**. Inflation has cooled significantly, with the Consumer Price Index (CPI) averaging **1.7%** in late 2025. This low-inflation environment has boosted private consumption, which now accounts for **61.5%** of the GDP. Key Indicators to Watch * **Manufacturing GVA:** Grew by **9.1%** in the most recent quarter. * **Foreign Exchange Reserves:** Stand at **$701.4 billion**, providing an **11-month** import cover. * **Auto Sales:** Anticipated to show strong growth in early March, with passenger vehicle wholesales expected to rise by **12%**. The market is currently navigating a technical phase where the **25,000** mark serves as a critical psychological support for the Nifty 50. Analysts have set a base-case target for the index at **29,150** by the end of **2026**, suggesting an annual upside of approximately **12%**.

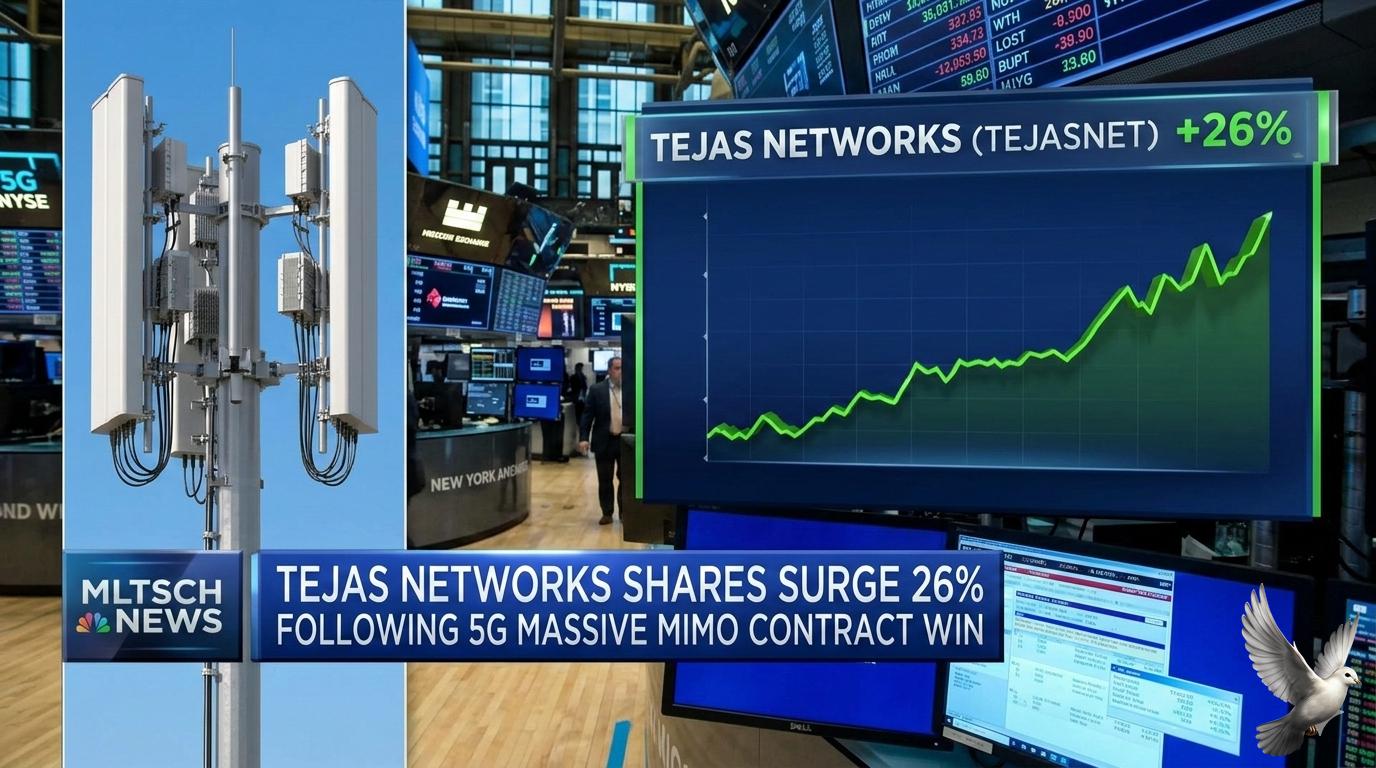

Tejas Networks Shares Surge 26% Following 5G Massive MIMO Contract Win

Tejas Networks has witnessed a massive surge in market activity, with shares jumping as much as 14.3% in a single session on February 27, 2026. This rally extends a multi-day winning streak that has seen the stock gain approximately 26% in just 48 hours. The primary catalyst for this vertical move is a landmark agreement with Japan’s NEC Corporation. Under this partnership, Tejas will manufacture and supply advanced 5G Massive MIMO radios for global markets. These radios, including high-capacity 32TR and 64TR models, are designed to enhance network capacity and spectral efficiency using targeted beamforming technology. Market data as of today shows the stock hitting an intraday high of ₹429.45, significantly outperforming the broader Nifty and Sensex indices, which faced volatility. Trading volumes have reached a staggering 2.24 crore shares, nearly 13 times the 30-day average. This surge indicates strong institutional interest following a period of long-term pressure where the stock had declined nearly 43% over the past year. Financially, the company is at a critical pivot point. While it reported a consolidated loss of ₹196.55 crore for the most recent quarter ending December 2025, the order book remains resilient. Tejas recently received ₹69.97 crore from the Indian government under the Production Linked Incentive (PLI) scheme, providing a strategic capital injection to support its manufacturing scale-up. This deal with NEC Corporation is a major milestone for the Tata Group-backed company as it transitions from a domestic supplier to a global contender in the 5G ecosystem. By aligning with Japanese technology standards, Tejas is positioning itself as a key alternative in the global telecom supply chain, which is currently seeking greater diversification. Looking ahead, market participants are focused on the company’s ability to convert its high inventory levels, valued at over ₹2,300 crore, into finished 5G products. Analysts have noted that while fundamental challenges remain, the technical momentum and the new international pipeline have shifted the short-term outlook to a bullish trajectory. The broader Indian telecom sector is also entering a value-creation phase in 2026, moving away from rapid rollouts toward monetization. With nationwide 5G coverage largely established, the demand for indigenous hardware and 5G-Advanced solutions is expected to drive steady order inflows for domestic manufacturers like Tejas Networks.

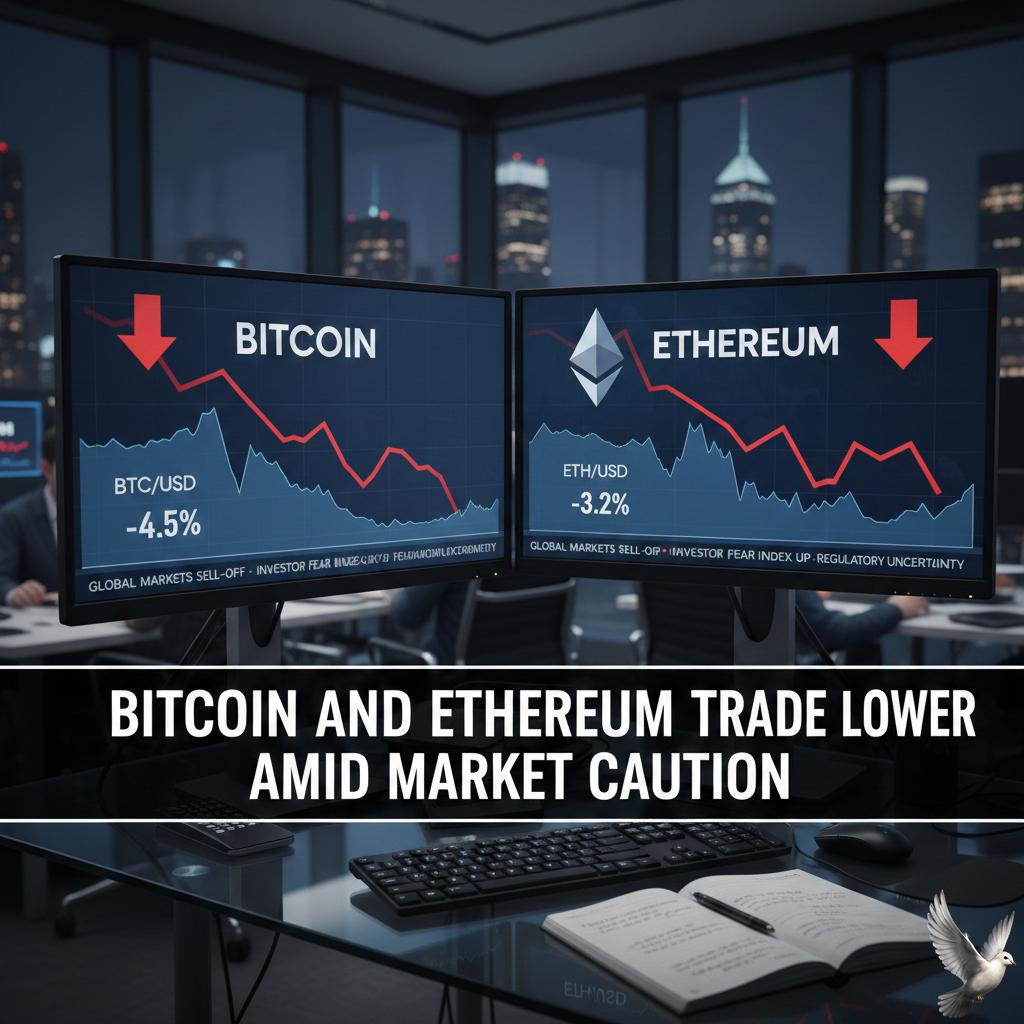

Bitcoin and Ethereum Trade Lower Amid Market Caution

Crypto Market Brief: February 27, 2026 The digital asset market is entering a high-velocity phase as of today, February 27, 2026. Bitcoin and Ethereum are navigating a complex landscape of massive derivatives settlement and shifting institutional flows. While underlying fundamentals remain active, a cautious atmosphere prevails across global trading desks. Derivatives Settlement and Price Action A massive **$9 billion** in cryptocurrency options is set to expire today. This event includes **116,000 BTC** contracts and **206,000 ETH** contracts. Historically, such large-scale expirations trigger heightened volatility as traders rebalance their delta-hedged positions. Bitcoin has staged a recovery toward the **$68,000** to **$69,000** range, regaining footing after dipping near the **$60,000** support level earlier this month. Ethereum has similarly reclaimed the **$2,000** psychological barrier, currently trading around **$2,026** after a period of intense selling pressure. ETF Inflows and Institutional Sentiment The institutional landscape shows a distinct "V-shaped" recovery in demand. US spot Bitcoin ETFs recorded significant momentum this week, highlighted by a single-day net inflow of **$507 million**. Over a recent 48-hour window, total inflows reached **$765 million**, suggesting that professional allocators are buying the dip. However, the broader 2026 trend remains mixed. Year-to-date, Bitcoin ETFs have seen a net reduction of over **$4 billion** in assets. This suggests that while recent daily data is bullish, long-term holders are still engaged in strategic profit-taking following the record highs seen in late 2025. Macro Risks and Global Market Cap The global crypto market capitalization has stabilized near **$2.2 trillion**, a significant retreat from previous peaks. Macroeconomic headwinds are currently the primary cap on gains. Investors are closely monitoring the impact of a new **10% to 15%** global trade surcharge implemented under Section 122 of the Trade Act. This policy uncertainty, combined with a "Fear & Greed Index" currently sitting at a low of **16**, indicates a state of extreme caution. High-beta assets like cryptocurrencies are being re-rated as liquidity conditions tighten globally. Network Developments and Support Zones Despite the price stagnation, network activity remains robust. Ethereum developers are preparing for the "Glamsterdam" upgrade in the first half of 2026. This technical milestone aims to introduce parallel execution to boost throughput. Currently, roughly **37 million ETH**—one-third of the total supply—is locked in staking, providing a floor for network security. Technical analysts identify **$68,000** as the critical "pivot" for Bitcoin. If this level holds, the next liquidity magnet is projected at **$75,000**. Conversely, a failure to maintain this support could reopen a path toward the **$60,000** zone. For Ethereum, staying above **$1,800** is considered essential to avoid a fresh slide toward 2024 lows. Staggered accumulation near these established support zones remains a prevalent strategy for participants looking to mitigate the immediate impact of the options-driven volatility.

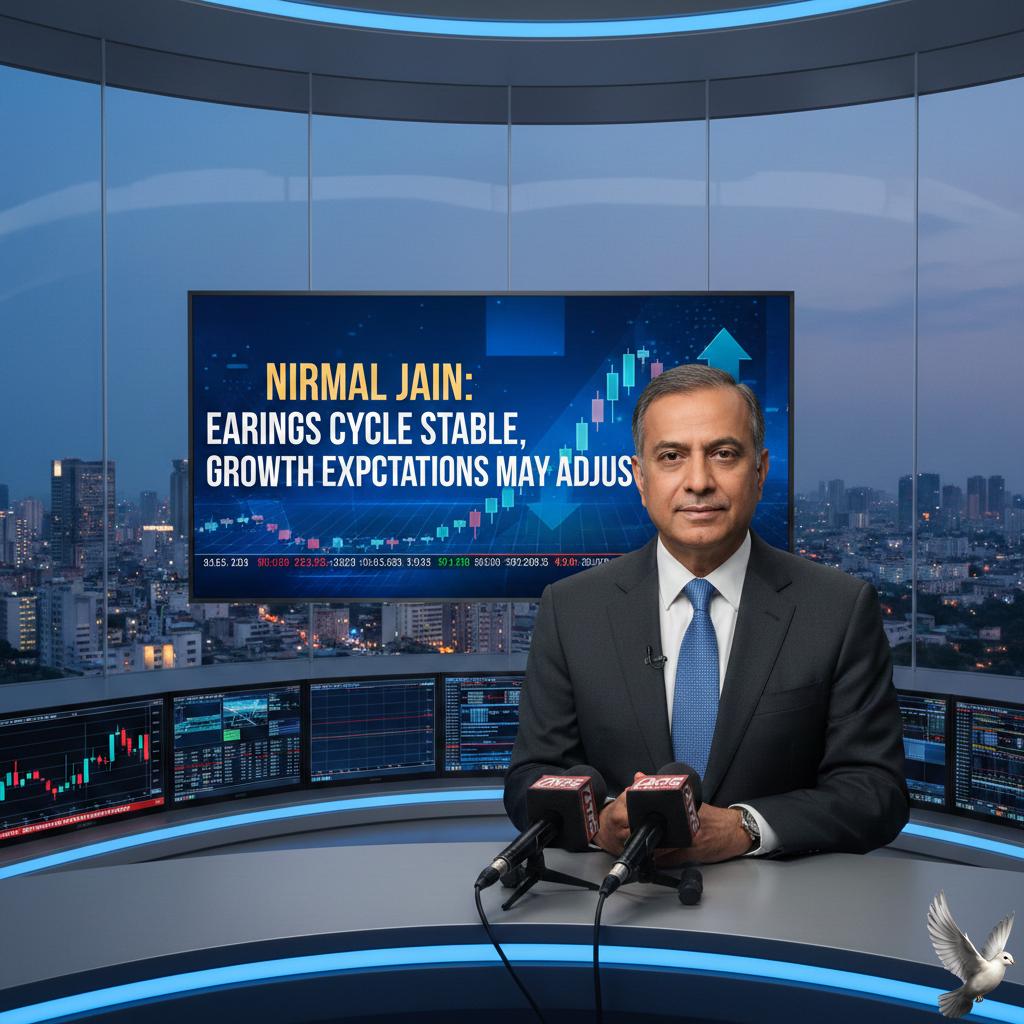

Nirmal Jain: Earnings Cycle Stable but Growth Expectations May Adjust

Market Brief: India Financial & Tech Outlook 2026 India's financial sector continues to exhibit resilience, supported by a significant shift in foreign institutional positioning. As of late February 2026, Foreign Portfolio Investors (FPIs) have funneled **₹19,675 crore** into the market, with a decisive rotation toward domestic growth themes. The Financial Services sector remains a primary beneficiary, attracting **₹6,175 crore** in recent weeks. The Nifty Financial Services index has maintained a steady trajectory, recently trading near **27,971**, while the Nifty Bank index has moved toward the **61,193** mark. This momentum is bolstered by a "domestic cushion," where local institutional buying of over **₹5,031 crore** in a single session has effectively offset global volatility and selective foreign selling. Artificial Intelligence has transitioned from an experimental phase to a core operating model for the tech industry. The Indian tech sector is projected to reach **$315 billion** in revenue for FY26, a **6.1%** increase. AI-specific services are now estimated to contribute between **$10 billion and $12 billion** as enterprises move toward scaled deployments and measurable ROI. Workforce dynamics are evolving rapidly within the IT space. While revenue growth is beginning to decouple from traditional headcount expansion, the industry remains a net hirer with a **2.3%** increase in staff. Over **2 million** professionals have been upskilled in AI, reflecting a strategic shift toward "Human + AI" delivery models. Corporate earnings are entering a double-digit recovery phase following a period of single-digit growth. However, macroeconomic indicators suggest a "reset" in expectations. Real GDP growth for FY26 is pegged at **7.4%**, but nominal growth has moderated to **8.0%**, down from nearly **10%** in the previous cycle. Investors are currently prioritizing quality large-caps in banking and capital goods. While the broader indices remain near record levels, market participants are focused on sectors benefiting from the ongoing capex cycle and stabilized domestic consumption, which is expected to contribute **4.4%** to GDP growth by the end of the year.

India Sovereign Bond Yields Rise Amid Scheduled $8 billion Debt Auction

The Indian sovereign bond market is currently navigating a period of heightened volatility as a massive supply of fresh debt meets cautious investor sentiment. Benchmark bond yields have trended upward, recently touching the 6.71% mark as traders adjust to the heavy issuance calendar and shifting liquidity conditions. Supply dynamics remain the primary driver of market movement. The central government and state authorities are set to raise significant capital, including an immediate 320 billion rupee auction of the benchmark 2035 bond. Total state government issuances for the week are projected at approximately 445 billion rupees. This influx of paper has tested the market's absorption capacity, leading to a slight dip in bond prices. Economic growth data provides a supportive but complex backdrop. Market participants are closely watching for the latest growth figures, with projections indicating a resilient 7.4% expansion for the fiscal year 2025-26. High-frequency indicators suggest even stronger quarterly momentum, with some estimates pointing toward 8.1% growth for the October-December period. This robust performance complicates the outlook for interest rate cuts, even as retail inflation has softened significantly to approximately 2.75%. The Reserve Bank of India has actively managed the debt profile through strategic switch auctions. A recent 25,000 crore rupee switch operation was conducted to replace short-term bonds maturing in 2027 with longer-dated securities. This move aims to reduce the massive 5.47 trillion rupee redemption pressure looming in the next fiscal year and maintain overall financial system stability. Despite the supply pressure, specific segments of the curve show strength. Ultra-long securities, specifically 30-year and 40-year bonds, have attracted sustained interest from institutional investors like insurance companies. While 10-year yields have seen a modest 10-basis-point increase over the financial year, longer-dated paper has experienced a steeper rise of roughly 45 basis points. Global factors continue to exert influence, with the rupee trading near 90.95 against the dollar and international oil prices hovering around $71 per barrel. Analysts expect the 10-year benchmark yield to remain within a range of 6.65% to 6.78% in the near term as the market balances strong domestic fundamentals against the persistent issuance overhang. [Indian Debt Market Outlook](https://www.youtube.com/watch?v=z01RGOV-ZNw) This video provides an expert analysis of the February 2026 debt market, covering the specific impact of government borrowing and yield spikes on fixed-income strategies. http://googleusercontent.com/youtube_content/0

US Market: Bond Volatility Impacts Mortgage Rates and Equities

The average rate on a 30-year fixed mortgage in the US has officially breached a major psychological barrier, falling to 5.98% this week. This marks the first time since September 2022 that long-term borrowing costs have dipped below the 6% threshold. According to the latest data from Freddie Mac, this new figure represents a steady decline from 6.01% just one week ago. More significantly, it shows a substantial drop from the 6.76% average recorded during the same period last year. The recent downward movement is largely tied to a dip in the 10-year Treasury yield, which currently hovers around 4.02%. This shift followed recent market volatility and cooling inflation data, which saw the annual rate drop to 2.4% in early 2026. Despite the relief in rates, the housing market remains in a state of transition. Existing home sales fell by 8.4% in January to an annualized rate of 3.91 million, the sharpest one-month decline in nearly four years. This indicates that while financing is becoming cheaper, buyers remain cautious. Inventory levels are beginning to show signs of life, rising approximately 10% year-over-year. This increase in supply is helping to stabilize prices, with the national median home price currently holding near $405,000. Some regions, particularly in the West Coast and Sun Belt, are seeing more pronounced price corrections. Affordability is gradually improving as wage growth begins to outpace home price appreciation for the first time in several years. The income required to purchase a median-priced home has decreased to roughly $94,000, down from $103,000 a year ago. The Federal Reserve currently maintains its benchmark interest rate in the 3.5% to 3.75% range. While the Fed has remained on hold recently, the mortgage market has preemptively adjusted to the lower inflation outlook and shifts in secondary market demand. Refinancing activity is the primary driver of current mortgage application growth, which rose 2.8% recently. Homeowners who locked in higher rates during the 2023 peak of 7.8% are now moving to capitalize on the sub-6% environment to lower their monthly payments. Looking ahead to the spring buying season, economists suggest that if rates remain below 6%, it could finally break the "lock-in effect" that has kept many homeowners from listing their properties. Increased listings would provide the necessary supply to meet the pent-up demand of shoppers who have been sidelined for over three years.

Jitendra Gohil on PSU Banks Outlook and Consumption Stock Risks

Indian markets are currently navigating a phase of intense sector rotation as investors balance high valuations with emerging growth drivers. While the broader Nifty 50 recently hovered around the 25,560 level, market participants are being advised to remain highly selective. The era of easy gains across the board is shifting toward a period where company fundamentals and specific policy beneficiaries will dictate performance. Foreign Institutional Investors (FIIs) have shown a significant change in behavior. After a prolonged period of selling, February 2026 saw the strongest monthly net inflows in 17 months, totaling approximately $2.44 billion. Globally, these investors remain heavily focused on the Artificial Intelligence (AI) boom, which is beginning to reshape the domestic landscape through massive infrastructure requirements. Public Sector Undertaking (PSU) stocks, particularly state-owned banks, continue to be a primary area of attraction. The Nifty PSU Bank Index recently hit record levels near 9,665, supported by historic Q3 earnings. Major lenders like SBI have reported record quarterly profits exceeding ₹21,000 crore, while aggregate net profits for the sector are projected to cross ₹2 lakh crore by the end of the 2026 fiscal year. Improving asset quality, with Gross NPA ratios falling toward 2.30%, remains a key structural tailwind. The digital infrastructure and power sectors are emerging as critical growth pillars. India’s data center capacity is on a trajectory to reach 1.8 GW by 2027, fueled by a 22% compound annual growth rate. This expansion is tightly linked to the AI super-cycle, creating a massive demand for power. Investors are increasingly focusing on companies that benefit from the 2026-27 Union Budget's emphasis on infrastructure and the new 20-year tax holiday for global cloud operators. Conversely, caution is advised in segments where valuations have become disconnected from earnings potential. Analysts suggest avoiding lower-end consumption stocks and overvalued companies in the paint and cement sectors. While some cement players are undertaking cost-reduction initiatives, the broader trend favors investment-led sectors over mass consumption. Corporate earnings growth is expected to stabilize at around 10% for the current fiscal year, with a potential recovery to mid-teen levels in 2027. With a targeted fiscal deficit of 4.3% and nominal GDP growth estimated at 10%, the focus remains on reform beneficiaries and high-quality large caps that can withstand global volatility and shifting interest rate cycles.

Rupee declines 0.04 to 90.95 against US dollar

MARKET BRIEF: RUPEE AND EQUITIES The Indian rupee faced mild pressure in early Friday trade, depreciating by **4 paise** to hit **90.95** against the US dollar. This movement follows a period of volatile institutional flows and cautious sentiment in domestic equity markets. Despite the slight dip, the local currency found a floor near the **91.00** mark. This stability was primarily supported by a softer US Dollar Index (DXY), which slipped to **97.67**, and a cooling trend in global energy markets. EQUITY MARKET PERFORMANCE Domestic benchmarks opened in the red as investors reacted to global trade uncertainties. The **BSE Sensex** dropped over **250 points** in early deals, testing levels around **81,992**. Simultaneously, the **Nifty 50** hovered near **25,413**, marking a decline of approximately **0.33%**. Selling pressure was most visible in the automotive and telecommunications sectors. Heavyweights such as **Maruti Suzuki** fell **1.5%**, while **Bharti Airtel** and **Mahindra & Mahindra** also featured among the top laggards. In contrast, the IT sector emerged as a defensive stronghold. The **Nifty IT index** climbed over **1%**, led by a **2%** gain in **Infosys**. Other tech giants, including **TCS** and **HCLTech**, traded in green territory, helping to offset broader index losses. INSTITUTIONAL FLOWS AND CRUDE IMPACT Foreign Institutional Investors (FIIs) remained net sellers, with an outflow of **₹3,465.99 crore** recorded in the latest session. This persistent exit by foreign funds has been a primary driver of recent rupee depreciation. However, Domestic Institutional Investors (DIIs) acted as a significant cushion, recording a net purchase of **₹5,031.57 crore**. This strong domestic support has prevented a more aggressive sell-off in Indian equities. On the commodities front, **Brent crude** prices remained relatively stable, trading near **$70.84** per barrel. Markets are currently weighing the impact of extended US-Iran nuclear negotiations and an upcoming OPEC+ meeting scheduled for Sunday. A steady or falling oil price typically eases the import bill for India, providing fundamental support to the rupee. KEY INDICATORS AT A GLANCE * **USD/INR:** 90.95 (-0.04 paise) * **Dollar Index (DXY):** 97.67 (-0.12%) * **Brent Crude:** $70.84 (+0.21%) * **FII Net Flow:** -₹3,465.99 Cr * **DII Net Flow:** +₹5,031.57 Cr The near-term outlook for the currency remains tied to the **21-day Exponential Moving Average** on equity charts and the outcome of international geopolitical discussions. While FII caution persists, the robust participation of domestic funds continues to stabilize the broader financial landscape.