Bullish News

Collection

Block Shares Rise 20% Following Workforce Reduction of 4,000 Employees

Shares of Block, Inc. surged nearly 20% in late February 2026 trading following a transformative fourth-quarter earnings report. CEO Jack Dorsey announced a massive structural reset, reducing the company's workforce by 40%. The headcount will drop from over 10,000 to approximately 6,000 employees as the firm pivots toward an AI-native operational model. Markets responded with high conviction to this efficiency-driven strategy. Block reported a Q4 gross profit of $2.87 billion, marking a 24% year-over-year increase. Monthly active users on Cash App reached 59 million, while primary banking actives grew 22% to 9.3 million. This performance pushed the company's 2025 annual gross profit to $10.36 billion, with December alone crossing the $1 billion milestone for the first time. The pivot to artificial intelligence is central to Block's new growth thesis. Management cited that intelligence tools are now advanced enough to allow significantly smaller teams to outpace larger, traditional workforces. Internal productivity gains from AI integration are expected to accelerate product development cycles and expand operating margins, which reached 20% in the final quarter of 2025. For the 2026 fiscal year, Block has issued aggressive guidance. The company expects gross profit to reach approximately $12.2 billion, representing 18% growth. Adjusted operating income is projected at $3.2 billion, which would signify a 54% increase over the previous year. This outlook underscores a shift in investor sentiment, where lean, AI-driven profitability is now prioritized over total workforce scale. Despite the positive market reaction, the broader fintech sector remains in a state of flux. While Block's shares rallied on the news, the stock had faced a 22% decline earlier in the year due to persistent economic headwinds. The current rally reflects a "Rule of 40" reckoning, as the company balances growth with disciplined cost management. The structural changes at Block serve as a bellwether for the industry. Other major fintech players are increasingly adopting "agentic AI" and automated compliance systems to reduce overhead. As the sector moves through 2026, the focus has shifted entirely to high-margin lending, primary banking engagement, and AI-powered operational leverage. [Block Q4 2025 earnings review](https://www.youtube.com/watch?v=eml2imnhwZg) This video provides a professional breakdown of Jack Dorsey's decision to cut half of Block's staff to focus on AI productivity. http://googleusercontent.com/youtube_content/0

Brigade Group and Primus Senior Living Partner for Three Senior Housing Projects

**Senior Living Market Brief: Brigade Group Expansion** **Strategic Partnership and Financial Impact** Brigade Group has entered into a strategic alliance with Primus Senior Living to develop three specialized housing projects in South India. This collaboration is set to unlock a combined Gross Development Value of 750 crore. The projects will deliver over 600 residential units specifically designed for the elderly, marking a significant move by the developer to diversify its residential portfolio beyond conventional formats. **Project Integration and Infrastructure** Two of the three upcoming communities will be integrated within larger existing township developments. This "senior-first" design approach allows residents to access shared social infrastructure while maintaining age-specific amenities. Key features include wellness centers, medical bays, hobby lounges, and fully accessible pathways. The model emphasizes inter-generational connectivity, bridging the gap between independent living and professional care. **Regional Market Dominance** South India currently accounts for nearly 60% of the organized senior living market in the country. This dominance is driven by advanced medical infrastructure, higher social acceptance of retirement communities, and a significant NRI base with aging parents in the region. Bengaluru and Chennai remain the primary hubs for these developments, with Chennai recently recording a 55% year-on-year surge in housing sales during the 2025-2026 period. **Sector Growth and Investment Trends** The Indian senior living market, valued at approximately 11.16 billion dollars in 2025, is projected to grow at a compound annual rate of 10% to 25% through 2031. This expansion is fueled by a doubling of the elderly population, which is expected to reach 347 million by 2050. Changing family structures and rising disposable incomes have shifted the segment from a niche "need-based" category to an aspirational lifestyle choice. **Pricing and Portfolio Outlook** Current market data indicates that senior living units in major South Indian metros typically range from 45 lakh to 75 lakh for standard configurations, with premium luxury projects exceeding 2 crore. For Brigade Group, this partnership builds on the success of their Parkside at Brigade Orchards project, which has been operational since 2017. As of early 2026, the developer continues to maintain a strong presence in the broader residential market, recently launching separate landmarks in Chennai with an estimated value of 1,700 crore.

Stock Market Top Gainers and Losers: Redington, Tejas Networks, and Others in Focus on Friday

Market Brief: Late February Volatility Indian equity markets witnessed a sharp downturn as of **February 27, 2026**, with benchmark indices erasing recent gains in a broad-based sell-off. The **BSE Sensex** plunged **961.42 points**, or **1.17%**, to settle at **81,287.19**. Similarly, the **NSE Nifty 50** tumbled **317.90 points**, or **1.25%**, closing at **25,178.65**. The crash wiped out approximately **₹5 lakh crore** in investor wealth in a single session. Total market capitalization of BSE-listed firms slipped to nearly **₹463 lakh crore** as risk aversion gripped the floor. Sectoral Pressure Points The decline was led by heavyweights in the **Auto**, **Financial Services**, and **FMCG** sectors. Foreign Institutional Investors (FIIs) intensified the pressure by offloading equities worth **₹3,465.99 crore** in the preceding session. Banking and financial counters were particularly hit. Private lenders faced persistent selling amid concerns over valuation comfort and margin stability. Furthermore, sentiment in the microfinance space soured following the passage of the **Bihar MFI Bill 2026**, causing stocks like **Utkarsh Small Finance Bank** and **Fusion Finance** to tank between **6%** and **11%**. Global and Macro Triggers Geopolitical uncertainty acted as a primary catalyst. Inconclusive **U.S.–Iran nuclear talks** raised fears of escalation in the Middle East. Simultaneously, **Wall Street** faced its own pressures, with the **Nasdaq** bracing for its steepest monthly drop since early 2025 due to cooling sentiment around high-growth technology and AI sectors. Domestically, while **GDP data** remained a point of underlying strength, the immediate focus shifted toward a "risk-off" tone as the earnings season concluded. Rising **U.S. bond yields** and a stronger dollar further incentivized FII outflows from emerging markets. Resilient Counters and Deal Drivers Despite the general gloom, specific stocks rallied on significant corporate developments. **Tejas Networks** emerged as a top gainer, surging **17.50%** to close at **₹436.00**. This rally followed a strategic agreement with **NEC Corporation** to manufacture and supply **5G Massive MIMO radios** for global telecom operators. **XTGlobal Infotech** also defied the market trend, hitting its upper circuit with a **19.98%** gain. The stock reached an intraday high of **₹39.99** on the back of strong buying momentum and an unfilled demand for small-cap IT services. Other notable performers included **Sanofi Consumer**, which advanced **14%** following a robust quarterly report showing a **50%** rise in net profit, and **KSB**, which gained **9%** post-earnings. Market Outlook The session left the **Nifty 50** testing immediate support levels near **25,100–25,150**. While the broad market remains volatile, selective buying persists in counters with clear regulatory or deal-driven triggers. Investors are maintaining a cautious stance, monitoring global macro factors and FII activity as the new trading month approaches.

Redington Shares Surge 17% Following Apple Product Launch Teaser

Redington shares experienced a significant surge, gaining as much as 17% in a single session to reach an intraday high of ₹286.00 on the BSE. This rally followed a strategic teaser from Apple CEO Tim Cook, who hinted at a "big week" of product announcements starting Monday, March 2, 2026. The stock closed approximately 13% higher at ₹276.00, pushing Redington’s market capitalization above ₹22,000 crore. Trading activity was notably aggressive, with volume reaching 8.5 million shares, significantly outpacing the two-week average. Investor sentiment is centered on Redington’s role as a primary distributor for Apple in India and international markets. Apple products now account for roughly 33% of the company's total revenue, up from 30% in previous quarters. The anticipated "big week" is expected to feature a refresh across multiple Apple categories. Markets are specifically watching for the debut of the iPhone 17e, positioned as a high-volume, affordable entry-level smartphone. Other rumored launches include new MacBook Pro models powered by M5 Pro and M5 Max chips, a refreshed MacBook Air, and updated iPad models. Reports also suggest the introduction of a low-cost MacBook, which could broaden the brand’s reach in the education and value sectors. Financially, Redington reported a strong Q3 FY26, with global revenue reaching ₹30,959 crore, a 16% year-on-year increase. Its core SISA (Singapore, India, and South Asia) region saw a 24% revenue jump to ₹16,600 crore. Despite robust top-line growth, profit margins in the region grew more modestly at 3%, signaling some cost pressures even as demand for premium electronics remains high. The company is actively diversifying through its "Unlock Next" strategy, focusing on cloud and enterprise solutions to balance its hardware distribution. Market analysts note that Redington's 1-year performance has now moved to approximately 11.5%, largely aligning with broader benchmark indices like the Nifty 50. However, today's breakout highlights the stock's high sensitivity to Apple’s product cycles and launch momentum. Industry trends for 2026 suggest a deepening of the premium smartphone and AI-ready PC segments in India. As Apple continues to expand its local manufacturing footprint and retail presence, distributors like Redington remain positioned to capture increased volume from upcoming hardware refreshes.

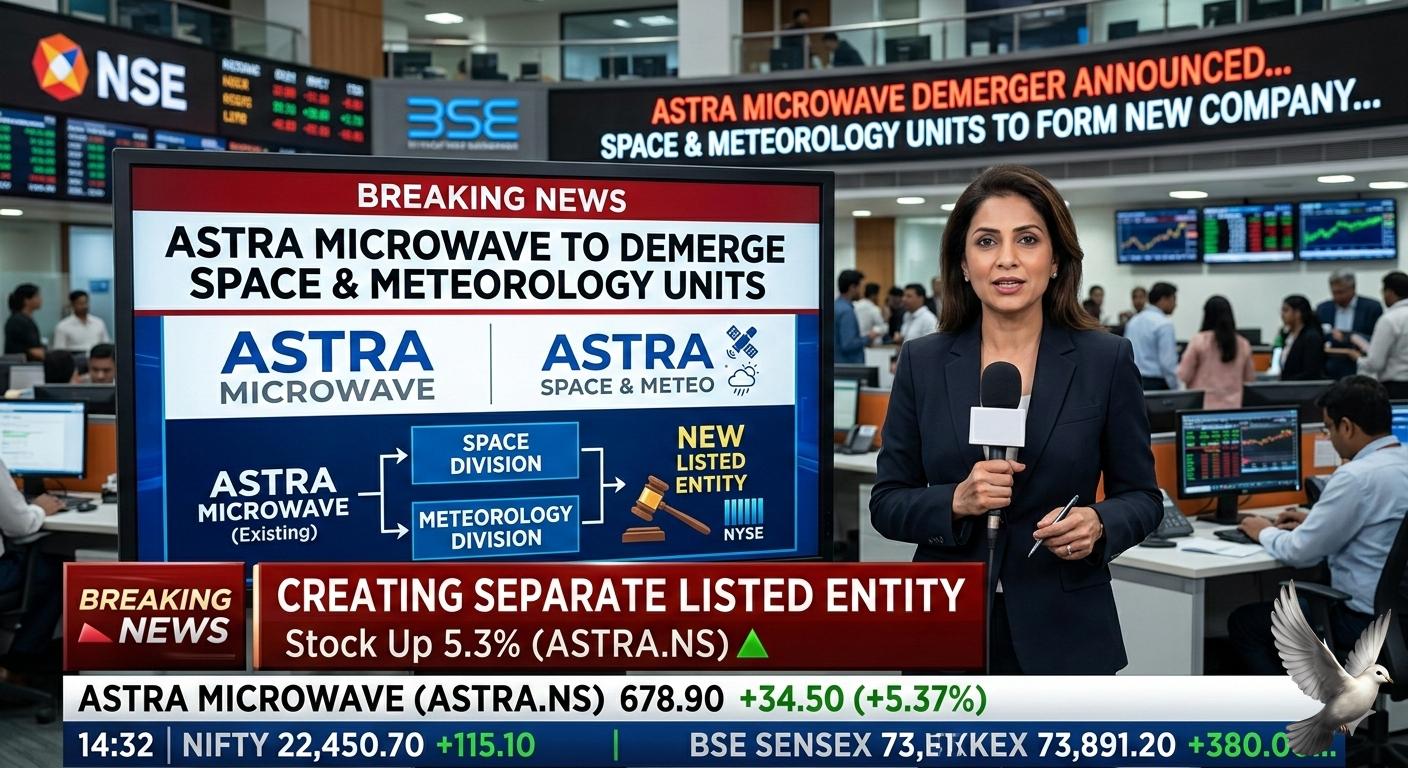

Astra Microwave to Demerge Space and Meteorology Units into Separate Listed Entity

Astra Microwave Products has reached a major corporate milestone with its Board granting in-principle approval for the demerger of its space, meteorology, and hydrology business. This strategic pivot will result in the creation of a new, independently listed entity named **Astra Space Technologies Private Limited (ASTPL)**. The restructuring is designed to separate the company’s core Defence and Aerospace operations from its rapidly scaling Space and Meteorology segments. Management expects the transition to be completed by **Q1 FY28**. **Financial Snapshot and Market Context** Astra Microwave’s market capitalization currently stands at approximately **₹9,419 crore**. As of February 27, 2026, the stock closed near **₹968.60**, maintaining a strong year-on-year growth of over **62%**. The company recently reported its best-ever quarterly performance for Q3 FY26, with revenue reaching **₹258 crore** and a significant EBITDA margin of **30.9%**. This profitability surge is attributed to a favorable product mix and disciplined execution of its expanding order book. **The Space and Meteorology Business (ASTPL)** The new entity, ASTPL, will inherit a legacy of high-performance engineering. Over the past two decades, the space division has executed orders exceeding **₹750 crore** for ISRO, with an additional **₹250 crore** in contracts scheduled for completion by **FY28**. The Meteorology and Hydrology segment adds further stability, having delivered over **₹330 crore** in contracts to date. This division currently holds an order book of **₹285 crore**. By spinning off these assets, the company aims to provide more granular management focus on capital-intensive satellite and weather radar technologies. **Strategic Rationale** The demerger follows a "mirror shareholding" model, ensuring that existing investors receive shares in the new company proportionate to their current holdings. This move is expected to unlock significant shareholder value by: - Enabling specialized capital allocation for distinct business needs. - Improving operational efficiency and governance oversight. - Allowing each entity to pursue sector-specific growth strategies in India’s expanding defense and space ecosystems. **Looking Ahead** Astra Microwave continues to hold a robust standalone order book of **₹2,226 crore**. The defense segment remains the primary driver, accounting for roughly **89%** of the total backlog. With revenue targets set between **₹1,400–₹1,500 crore** for FY27, the company is positioning itself to capitalize on the Indian government’s self-reliance initiatives and the increasing commercialization of the global space sector.

Indian Rupee Records First Monthly Advance Since April as Traders Evaluate Seasonal Trends

The Indian rupee recorded its first monthly appreciation in nearly a year this February, breaking a downward trend that had persisted since April 2025. The currency strengthened by approximately 1% during the month, climbing from historic lows to trade near the 90.40 level against the U.S. dollar in mid-February. The primary catalyst for this recovery was the breakthrough announcement of a landmark trade deal between India and the United States. Under the agreement, U.S. tariffs on Indian goods were reduced from 25% to 18%, a move that significantly brightened the outlook for Indian exports. This policy shift effectively removed a major layer of uncertainty that had previously triggered heavy speculative selling of the local unit. Capital flows also provided a vital cushion. Foreign Portfolio Investors (FPIs) turned into net buyers during the first half of the month, with total net inflows reaching 19,675 crore. A significant portion of this interest was concentrated in debt markets and domestic growth sectors such as capital goods and financials. In a single week ending February 13, net inflows reached 69.34 billion, highlighting a pivot in global investor sentiment toward Indian assets. Macroeconomic data released in late February added further support to the currency's narrative. India’s GDP growth for the third quarter of fiscal year 2026 reached 7.8% under a newly introduced 2022-23 base year series. While this represented a slight sequential moderation from the previous quarter's 8.4%, it surpassed many market estimates. Additionally, January inflation was contained at 2.75%, remaining well within the central bank's comfort zone. However, the final days of the month saw some of these gains pared back. On February 27, 2026, the rupee settled at 90.99 against the dollar as profit-taking in the equity markets and renewed geopolitical tensions in the Middle East pressured emerging market currencies. Brent crude oil prices rose to 71.91 per barrel, increasing the dollar demand from importers. Despite the month-end volatility, the Reserve Bank of India’s strategic interventions near the 91.00 level helped prevent a deeper slide. The month concluded with the rupee positioned significantly higher than its January close, supported by a much-improved trade landscape and a robust domestic growth trajectory.

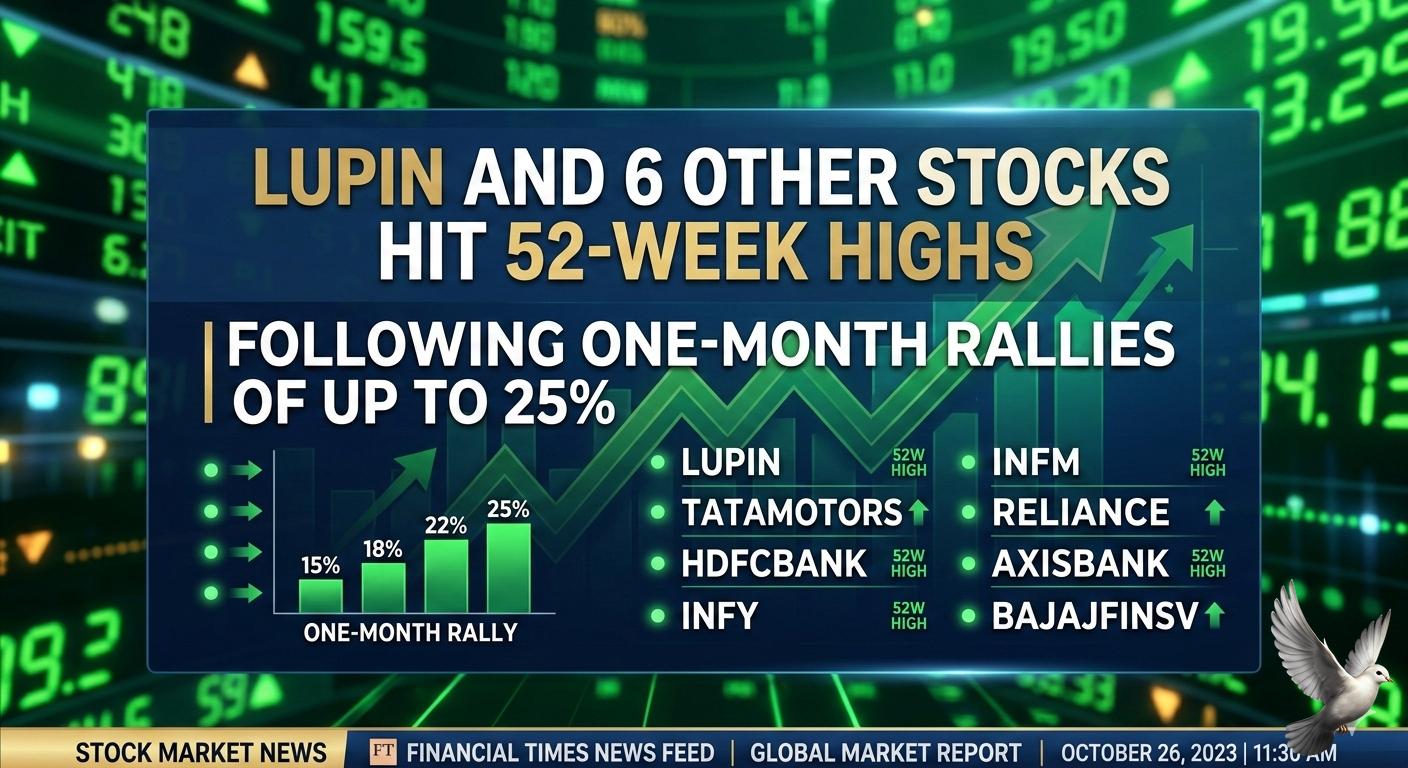

Lupin and 6 Other Stocks Reach 52-Week Highs Following One-Month Rallies of Up to 25%

Global Market Brief: February 27, 2026 Global financial markets are navigating a complex landscape of geopolitical negotiations and shifting economic data. Recent sessions show a distinct divergence between blue-chip stability and high-growth volatility, as investors recalibrate expectations for the remainder of the first quarter. Equity Market Performance Wall Street ended its latest session with a mixed profile. The **Dow Jones Industrial Average** managed a slim gain of **0.03%** to close at **49,499.20**. In contrast, the tech-heavy **Nasdaq Composite** saw a sharper decline of **1.2%**, falling to **22,878.38**, while the **S&P 500** retreated **0.5%** to settle at **6,908.86**. In Asian markets, performance remained fragmented. Tokyo’s **Nikkei 225** rose **0.29%** to **58,753.39**, while South Korea’s **Kospi** tumbled **1.72%**. Indian benchmarks showed resilience but faced pressure, with the **Sensex** holding near **82,248** and the **Nifty 50** hovering around the **25,500** mark. Commodity Trends and Energy Energy markets have seen a slight cooling as diplomatic channels remain active. **WTI Crude** eased to **$65.03** per barrel, while **Brent Crude** stayed above the **$70.50** threshold. Despite the immediate dip, analysts maintain a cautious outlook for 2026, with some forecasting an average of **$60.00** per barrel due to a projected supply surplus. Precious metals are currently in a consolidation phase following a historic rally. Gold futures in New York are trading near **$5,199** per ounce. In domestic markets, **24K Gold** is priced at approximately **₹16,183** per gram, reflecting a minor pullback. Silver has shown significant intraday strength, surging over **3%** to reach **₹2.67 lakh** per kilogram on the back of safe-haven demand. Inflation and Central Bank Policy The **European Central Bank** has maintained its deposit facility at **2.00%**, signaling confidence that inflation is converging toward target levels. In India, the **Reserve Bank of India** kept the repo rate unchanged at **5.25%** with a neutral stance. Economic indicators suggest that global inflation is stabilizing, though base effects from the previous year may cause temporary upticks. The **U.S. Producer Price Index (PPI)** forecast stands at **0.3%**, a figure closely watched as a precursor to consumer pricing trends. Sector Analysis The technology sector continues to experience headwinds, with the **Information Technology** sector falling **1.8%** in recent U.S. trading. However, specific pockets of the market, such as **Financials**, gained **1.3%**. In emerging markets, electronics and appliances have seen a reversal in trends, with high-volume trading in local mid-cap leaders indicating a potential floor for recent corrections. Market volatility, as measured by the **VIX**, increased by **3.9%** to reach **18.63**, suggesting that while panic is absent, caution remains the prevailing sentiment among institutional participants.

Bharat Biotech Weighs $500 Million Initial Public Offering

Market Brief: Bharat Biotech IPO Outlook Bharat Biotech International Ltd, the Hyderabad-based pioneer behind India’s indigenous Covid-19 vaccine, is actively exploring an initial public offering (IPO) targeted to raise upwards of **$500 million**. The move comes as the company seeks to capitalize on its global prominence, having delivered more than **9 billion** vaccine doses worldwide since its inception in **1996**. While the promoter family currently holds **100%** equity, this potential listing would mark a significant transition toward public transparency and market-driven valuation. Financial Performance & Growth Recent financial data indicates a strengthening bottom line. The company's revenue rose to **₹1,462.9 crore** in **FY25**, up from **₹1,323.2 crore** the previous year. More impressively, operating profit margins saw a sharp ascent to **28.2%** in **FY25**, compared to just **8.8%** in **FY24**. This growth is supported by a diversified portfolio. While the oral polio vaccine was historically the primary revenue driver, the company has successfully shifted focus toward higher-volume products like its Typhoid Conjugate (TCV), Rotavirus (RV), and Japanese Encephalitis (JE) vaccines. Strategic Infrastructure To bolster future capacity, Bharat Biotech is investing heavily in its Sapigen Biologix facility in Bhubaneswar. The project involves a capital expenditure of **₹200–250 crore** for **FY26**, aimed at creating a large-scale manufacturing hub. The start of production at this plant is expected to optimize the company's working capital, which saw inventory days spike to **340** in **FY25** due to supply chain build-outs. Sector Dynamics The Indian pharmaceutical market is entering **2026** with strong fundamentals, projecting a growth rate between **7.8% and 8.1%**. This momentum is supported by the federal "Biopharma Shakti" initiative, which has earmarked **₹10,000 crore** over the next five years to boost domestic production of biologics and biosimilars. As a key supplier to the Government of India and UNICEF, Bharat Biotech remains central to institutional procurement, though it continues to navigate the volatility of tender-based pricing and increasing competition in export markets. IPO Market Context The primary market for new share sales in India has seen a selective start in **2026**. Investors are currently prioritizing volume-driven growth and sustainable earnings over pandemic-era peaks. If it proceeds, Bharat Biotech’s **$500 million** offering would serve as a major bellwether for the biotechnology sector, joining a high-profile pipeline that includes major players like Jio Platforms and the National Stock Exchange. Proceeds from the sale are expected to fund further R&D and next-generation vaccine platforms.

Howard Marks on Investment Strategies Amidst AI Market Growth

Market Brief: AI Investment Landscape The artificial intelligence sector has reached a critical inflection point where technical capability is no longer in doubt, but market profitability remains a central debate. Billionaire investor **Howard Marks** recently reinforced this sentiment, characterizing AI as a "real" and revolutionary technology capable of reshaping global labor. However, he remains cautious on the investment outlook, noting that current valuations for some startups resemble "lottery tickets" rather than guaranteed returns. Market Performance and Volatility February 2026 has been defined by a sharp divergence between record-breaking financial results and cooling investor enthusiasm. **Nvidia**, the industry bellwether, reported a staggering **$68.1 billion** in quarterly revenue—a **73%** year-over-year increase. Despite these historic figures, its stock price fell by over **5.5%** following the announcement, wiping out roughly **$260 billion** in market capitalization as investors questioned the sustainability of massive infrastructure spending. Broader indices have felt the pressure of this "AI paradox." In early February, the **Nasdaq Composite** saw a pull-back of over **1%** in a single day, while the **S&P 500** continues to hover near the **7,000** mark. This volatility highlights a growing market rotation away from "builders"—the companies providing chips and data centers—toward "users" who can demonstrate clear AI-driven revenue growth. Infrastructure vs. Monetization Global spending on AI is projected to exceed **$2.02 trillion** in 2026, a **36%** annual increase. A significant shift is occurring in how this capital is deployed. Expenditure is moving from speculative model training toward **inference**, which focuses on meeting the actual demand for active AI applications. * **Hyperscaler Capex:** Major tech firms are on track to spend **$527 billion** on capital expenditures this year. * **Infrastructure Growth:** Software frameworks required to scale autonomous agents are seeing an **83%** growth rate. * **Economic Impact:** Analysts estimate that AI-related investments contributed roughly **1%** to U.S. GDP growth over the past year. Strategic Transition to Agentic AI The market is transitioning from simple generative tools to **Agentic AI**—systems capable of independently executing complex workflows in finance, HR, and legal sectors. While efficiency gains are widespread, the "hard truth" of 2026 is the difficulty of monetization. Companies are moving away from "AI moonshots" to focus on cost minimization and error elimination. The Investor Dilemma Howard Marks suggests a balanced approach is mandatory in this environment. While the potential of AI is likely underestimated in the long term, current market prices do not necessarily reflect "bargains." The focus has shifted from whether a company uses AI to how it translates that usage into the bottom line. Success is now measured by **outcome-aligned services** rather than the mere adoption of new tools.

Twelve Large-Cap Stocks Record 50-80% Gains Within One Year

Global Large-Cap Performance Brief: February 2026 The large-cap landscape has shifted into a high-conviction phase as we move through the first quarter of **2026**. While broad market indices show modest gains, a select group of industry leaders is quietly delivering powerful returns between **50% and 80%** over the trailing twelve months. Market leadership is currently undergoing a structural rotation. The heavy concentration in "Magnificent Seven" stocks that defined recent years is broadening. Investors are now favoring "steady compounders" with resilient cash flows over pure momentum plays. US Market Momentum The S&P 500 maintains a bullish trajectory, closing recently near **6,928** points. This represents a year-to-date gain of approximately **8.2%** for the Dow and **12.5%** for the Nasdaq. However, the "easy money" phase has matured, and the market is now rewarding specific execution over general sector exposure. * **Technology & Infrastructure:** Oracle and Netflix have surged, with gains of **5%** in single sessions, as AI monetization moves from hardware to the application layer. * **Industrial Strength:** Companies like Caterpillar and Progressive are outperforming without the typical tech-heavy volatility, supported by infrastructure spending and pricing power. * **Valuation Gap:** The forward P/E ratio for the top mega-caps stands at **28.3x**, while the broader market remains more attractive at **21.8x**. Emerging Market Resilience Indian large-caps are showing significant stability despite global volatility. The Nifty 500 delivered a **7%** gain recently, but specific blue-chip leaders are anchored by domestic institutional support and a recovery in rural consumption. * **Reliance Industries:** Holds a dominant market cap exceeding **₹19,00,000 crore**, acting as a primary stabilizer for regional indices. * **Banking Sector:** HDFC Bank and ICICI Bank continue to command massive liquidity, with market caps of **₹14,00,000 crore** and **₹10,00,000 crore** respectively. * **Growth Projections:** India’s GDP is projected at **6.7%** for **2026**, providing a fertile backdrop for large-cap earnings to stabilize even as global rate-cut cycles slow. Sector Rotation and Risks A "vicious rotation" is underway as capital exits overcrowded AI trades. Investors are increasing allocations to financials and industrials, which have seen single-day advances of up to **1.4%** even when tech indices retreat. * **Energy Outperformance:** The energy sector has emerged as a surprise leader in early **2026**, with some constituents up over **55%** on average. * **Inflation Watch:** Real-time inflation estimates have dipped to **1.55%**, suggesting that while large-caps are sensitive to rates, the downward trend in pricing pressure supports sustained margin expansion. The current environment defines **2026** not as a crisis year, but as a transition year. Success is no longer guaranteed by buying the "whole shelf" of big tech; it now requires selecting individual "bottles" where earnings growth is backed by actual revenue receipts.

IndiGo and Adani Power Added to Chris Wood’s India Portfolio Following Reshuffle

India Market Brief: Portfolio Shifts & Economic Anchors The Indian equity landscape is witnessing a strategic realignment as institutional leaders adjust to evolving sector dynamics. Jefferies' Christopher Wood has executed a significant reshuffle in his India long-only portfolio, signaling a pivot toward power infrastructure and large-cap aviation. Strategic Rebalancing In a notable move, Wood has added **Adani Power** and **InterGlobe Aviation (IndiGo)** to the flagship GREED & fear India basket. Both stocks have been assigned a **4% allocation** each. To fund these entries, the portfolio has exited positions in Home First Finance and the travel platform Le Travenues Technology (Ixigo). This shift highlights a preference for industrial scale and dominant market players over niche finance and small-cap travel tech. The inclusion of Adani Power follows the group's massive **$100 billion** investment plan for AI-ready data centers and renewable energy infrastructure, while the move to IndiGo reflects its commanding **62% market share** in a recovering aviation sector. Market Context & Performance The reshuffle comes at a time when Indian equities are navigating a period of sideways movement. As of late February 2026, the **Nifty 50** is trading near the **25,178** mark, reflecting a broader market consolidation. Despite recent volatility, Wood remains **overweight** on India. He notes that while the MSCI India index has underperformed emerging market peers by **41%** on a total-return basis since late 2024, the structural story remains intact. Key performance metrics for the new portfolio additions include: * **Adani Power:** Current market cap stands at approximately **₹2.73 trillion**, with a 1-year return of over **41%**. * **IndiGo:** Shares are trading near **₹4,933**, with institutional block trades recently exceeding **₹100 crore**, signaling strong liquidity and professional interest. Macroeconomic Foundations India’s economic fundamentals continue to provide a robust "double engine" of growth. The GDP growth for **FY26** is estimated at **7.4%**, maintaining India's status as the fastest-growing major economy. Real GDP growth for **Q3 FY26** surprised on the upside at **7.8%**, driven by a **7.6%** expansion in gross fixed capital formation. Domestic liquidity remains the primary shock absorber for the market. While Foreign Institutional Investors (FIIs) have shown intermittent selling pressure—with recent daily outflows of roughly **₹3,465 crore**—Domestic Institutional Investors (DIIs) have countered with net purchases exceeding **₹5,031 crore**. Structural Resilience The market is increasingly "locally anchored" due to consistent retail participation. Monthly SIP inflows have stabilized between **₹25,000 crore and ₹30,000 crore**, providing a steady stream of domestic capital that mitigates the impact of global volatility and US interest rate shifts. Industry-wide manufacturing growth at **8.4%** and a resilient construction sector further support the overweight stance on industrials. These factors, combined with ongoing policy reforms, underpin the long-term structural opportunity Wood continues to champion in the Indian market.

Australian Stock Market Records Highest February Gains Since 2019 Amid Corporate Earnings Growth

Australian shares concluded February 2026 on a record-breaking note, with the S&P/ASX 200 index rising 0.3% on the final Friday to close at an all-time high of 9,198.60 points. This performance capped the market's strongest February since 2019, delivering a 3.5% monthly gain and pushing year-to-date returns to 5.39%. The benchmark hit three distinct record peaks throughout the month, defying a more aggressive stance from the Reserve Bank of Australia. The Materials sector emerged as the month's primary driver, advancing 1% on the final day of trade. Mining giants reported exceptional results, with BHP reaching six consecutive all-time highs and a valuation of 271 billion dollars. Fortescue also impressed investors, reporting a 23% jump in half-year net profit to 1.9 billion dollars and lifting its interim dividend by 24%. Energy stocks followed suit with a 0.94% gain, supported by geopolitical premiums in oil prices. Heavyweights like Woodside and Santos are entering a transition phase, with major projects like Scarborough and Barossa on track to deliver first production later this year. In the technology space, Block Inc provided a massive boost with a 27.83% single-day surge to 94.15 dollars. The jump followed a 24% increase in gross profit to 2.87 billion dollars and a strategic workforce reduction of 6,000 positions. The Financials sector remained a point of friction, slipping 0.24% as investors rotated out of major banks. Commonwealth Bank, the nation's largest lender, saw its shares fall 1.5% as high valuations and the shift toward resources dampened sentiment. Economic headwinds persist as the Reserve Bank raised the cash rate by 25 basis points to 3.85% this month. Inflation remains a concern, with the CPI hitting 3.8% in December—well above the 2-3% target band. Analysts now project the cash rate could reach 4.10% by May to combat "sticky" service inflation. Retail and consumer staples also struggled. Supermarket giant Coles reported a 16.5% jump in underlying profit to 699 million dollars, yet broader household consumption remains weak as higher interest rates weigh on discretionary spending. The Australian dollar responded to the rate hike by climbing toward 70 US cents. While this has strengthened local purchasing power, it has created a 2% headwind for global equity returns in unhedged terms, further focusing investor attention on domestic resource and energy leaders.

Nikkei 225 Reaches Record High Following Largest Monthly Gain in Four Months

Japan's equity markets have entered a historic "Golden Age" as the benchmark Nikkei 225 surged to a new record close of 58,850.27 points on Friday, February 27, 2026. This milestone capped an explosive month of growth, with the index posting a 10.37% gain for February alone. This represents the largest one-month percentage increase since late 2025 and marks the third consecutive month of gains. Year-to-date, the index has already soared by 16.91%, adding over 8,510 points since the start of January. The rally is largely fueled by the "Takaichi Trade," a wave of investor optimism following Prime Minister Sanae Takaichi’s landslide election victory. Her administration’s commitment to a 17.1 trillion yen economic stimulus package—roughly 10% of Japan’s GDP—has signaled a clear path toward aggressive fiscal expansion and tax relief. Market sentiment was further bolstered this week by the government’s nomination of two "reflationist" academics to the Bank of Japan’s policy board. These appointments suggest that the central bank will maintain a highly accommodative, low-interest-rate environment to support domestic growth, even as global markets face volatility. Corporate Japan is playing a central role in this ascent. Investors are aggressively betting on the structural transformation of domestic firms, which are now prioritizing shareholder returns and return-on-equity (ROE) improvements. Sony Group, for example, saw its shares jump 7.2% after expanding its share buyback program to 250 billion yen. SoftBank Group also trended upward, rising over 4% during the week. While global semiconductor stocks faced some profit-taking pressure—with firms like Advantest and Tokyo Electron seeing slight Friday pullbacks—the broader market momentum remained resilient. Economic data released today supports a cooling inflation narrative. Tokyo’s core consumer price index (CPI) slowed to 1.8% in February, falling below the central bank's 2% target for the first time in over a year. This cooling phase, aided by government energy subsidies, provides the Bank of Japan with additional flexibility regarding the timing of future rate hikes. Despite the rapid ascent, technical analysts note that the index is operating in "overbought" territory. While the 58,586 level has transitioned from resistance to a key support floor, the accumulation of 12-month gains exceeding 53% suggests that short-term volatility and profit-taking remain possible in the coming weeks.

Compass and Redfin Partner to Share Off-Market Real Estate Listings

In a significant shift for the U.S. residential real estate market, Compass and Redfin have entered a three-year strategic alliance that immediately integrates their digital ecosystems. This partnership allows Compass to display its exclusive "Coming Soon" and "Private Exclusive" listings directly on Redfin’s high-traffic consumer portal. The agreement could potentially inject more than 500,000 additional listings into the Redfin platform. This move is designed to provide sellers with greater flexibility, allowing them to test market demand without publicly tracking "days on market" or price reduction histories. It effectively bypasses traditional listing constraints during a period of evolving industry standards. The broader housing market is currently showing signs of a "slow thaw" as it enters the 2026 spring season. National mortgage rates have recently reached multi-year lows, with the 30-year fixed-rate mortgage averaging 5.98% as of February 26, 2026. This dip below the 6% threshold is expected to stimulate buyer activity after a prolonged period of stagnation. While mortgage rates are cooling, home prices remain resilient. Recent data from the Federal Housing Finance Agency shows a surprising 0.6% month-over-month increase in home prices. However, the national annual appreciation has slowed to a modest 1.4%, the lowest rate since 2011, indicating a move toward a more balanced market. Financial incentives are a core component of this new industry alliance. Through Rocket Mortgage, the parent company of Redfin, Compass clients are eligible for preferred pricing. This includes a 1 percentage point interest rate reduction for the first year of their loan or a lender credit of up to $6,000. Market reaction to the announcement was immediate. Following the news on February 26, 2026, shares of Compass (COMP) closed the regular session up 5.2% before experiencing a slight 1.6% correction in after-hours trading. Rocket Companies saw an even stronger response, closing 2.5% higher and surging an additional 8% in late-market activity. Inventory levels remain a critical factor for the 2026 outlook. While new listings rose 3.2% year-over-year in early February, total supply is still roughly 1.2 million homes short of demand. Compass and Redfin are positioning this partnership as a solution to increase transparency and inventory access for the 60 million monthly visitors on Redfin’s site. This collaboration marks a notable departure from previous industry tensions. By merging the largest U.S. brokerage by sales volume with one of the nation’s most visited search portals, the companies aim to streamline the homebuying process as the market navigates persistent affordability challenges and shifting regulatory environments.

A Balasubramanian Forecasts Market Rally Led by IT, Auto, and Banking Sectors

Indian equity markets are navigating a complex phase marked by recent volatility and a sharp late-session sell-off. As of February 27, 2026, the benchmark Sensex plunged approximately 961 points to close at 81,287, while the Nifty 50 dropped 318 points to finish at 25,179. This downturn has wiped out over 5 lakh crore in investor wealth, reflecting a cautious atmosphere despite solid underlying macro data. A. Balasubramanian, CEO of Aditya Birla Sun Life AMC, maintains a constructive outlook, describing the current environment as the "calm before a big move." He suggests that the market is in a pre-rally consolidation phase. While AI-related disruption fears and geopolitical noise have dampened sentiment, he believes these factors are overshadowing positive domestic drivers that have yet to be fully priced in. The IT sector has faced a significant de-rating due to "AI doomsday" fears. However, current data shows a marginal turnaround, with large-cap IT revenue growth exceeding expectations in recent quarters. Companies like TCS and HCL Tech are reporting AI-related revenues growing at nearly 20% quarter-on-quarter, albeit from a small base. Selective positions in large-cap IT remain a strategic play as these firms reinvent their service models. Auto and consumption sectors are also at a turning point. Monthly auto sales in two-wheelers and passenger vehicles show resilience, while the commercial vehicle segment is beginning to recover. A major catalyst on the horizon is the 8th Pay Commission, expected to take effect in 2026. Projections suggest a salary hike of 30% to 34% for over 1 crore central government employees and pensioners. This could inject massive discretionary income into the economy, serving as a structural demand catalyst. Investment flows have seen a notable shift. While Foreign Institutional Investors (FIIs) have been volatile, Domestic Institutional Investors (DIIs) and retail SIPs provided a cushion throughout 2025. However, February 2026 saw DII equity inflows hit a 10-month low of approximately 26,130 crore as investors shifted focus toward outperforming precious metals like gold and silver. For those navigating this volatility, the recommendation is to avoid narrow sectoral bets. Flexicap and multicap funds are favored for their ability to diversify across market caps. This approach allows investors to capture growth in midcaps while maintaining the stability offered by large caps, which currently trade at more reasonable valuations of around 18.5 times future earnings. The long-term trajectory remains supported by India’s GDP resilience and the potential for a recovery in corporate earnings. By ignoring short-term noise and focusing on sectors with structural tailwinds like IT, auto, and domestic consumption, investors can position themselves for the next leg of the market cycle. [A. Balasubramanian on the upcoming market rally](https://www.youtube.com/watch?v=yzQ_5pcVxsw) This video provides direct insights from the CEO of Aditya Birla Sun Life AMC regarding the sectors poised for growth and his perspective on the current market consolidation. http://googleusercontent.com/youtube_content/0

India's Economic Position Supported by Growth and Subdued Inflation: Aurodeep Nandi

India is currently maintaining a "goldilocks" economic environment, characterized by high growth and low inflation. Fresh data released in late February 2026 confirms that the economy is outperforming earlier expectations, supported by a significant revision in national accounting series. GDP Growth Performance The Ministry of Statistics has projected a real GDP growth of **7.6%** for the 2025–26 financial year. This is an upward revision from previous estimates, driven by a robust **7.8%** expansion in the October–December quarter. Nominal GDP, which includes the impact of inflation, is expected to grow by **8.6%** during the same period. The manufacturing sector remains a primary engine of this momentum, recording double-digit growth. Additionally, both the secondary and tertiary sectors have expanded by more than **9%**, reflecting broad-based resilience across the industrial and services landscape. Inflation and Price Trends Retail inflation continues to remain well within the official tolerance band. In January 2026, headline CPI stood at **2.75%**, marking the 12th consecutive month where inflation stayed below the medium-term target of **4%**. Core inflation, which excludes volatile items like food and energy, remains stable at approximately **2.6%**. While food inflation showed a slight uptick to **2.13%** in January, it remains historically low. Projections for the full 2025–26 fiscal year place average inflation at roughly **2.1%**, though a low base effect is expected to push this figure toward **4.3%** in the following year. Monetary Policy and Interest Rates The Reserve Bank of India (RBI) maintained the repo rate at **5.25%** during its February 2026 meeting. This decision follows a cumulative reduction of **125 basis points** over the past year. The central bank has signaled a "prolonged pause," shifting its focus to a neutral stance to ensure price stability while supporting growth. Liquidity in the banking system remains in surplus, averaging **₹3.5 lakh crore**. To manage this, the RBI has employed open market operations and forex swaps. The current policy environment suggests that lending rates will remain steady for the foreseeable future. Manufacturing and Services Momentum High-frequency indicators show accelerated private sector activity. The Composite PMI Output Index rose to **59.3** in February 2026, the strongest expansion in three months. Manufacturing PMI reached a four-month high of **57.5**, supported by domestic orders and increased production capacity. While services growth cooled slightly to **58.4**, the sector saw the fastest rise in new export orders since August 2025, indicating strong international demand for Indian services. Currency and External Factors The Indian Rupee has shown notable resilience, trading in a steady range of **90.2 to 90.5** against the US Dollar. This stability is bolstered by a recent trade agreement with the United States, which reduced tariffs on Indian imports from nearly **50%** down to **18%**. Robust foreign exchange reserves and steady foreign portfolio inflows continue to act as a shield against global volatility, maintaining the currency's strength despite geopolitical uncertainties.

NTPC Share Price: Closing Performance and Market Updates

Market performance as of late February 2026 reflects a landscape of cautious optimism mixed with significant sector rotation. While major indices remain near record territories, the breakneck momentum of previous cycles is being replaced by a broader, more balanced foundation of growth. The S&P 500 has maintained a steady footing, posting a one-month return of **1.54%** and a year-to-date gain of **0.82%**. Investors are increasingly moving capital away from hyper-concentrated technology names and into "real economy" sectors. Energy has emerged as a powerhouse leader, surging **14.32%** over the last month and **21.87%** year-to-date, fueled by geopolitical shifts and resilient global demand. Sector Performance and Economic Shifts The rotation toward value and defensive plays is evident in the Industrials and Materials sectors, which have recorded year-to-date gains of **14.09%** and **16.27%** respectively. In contrast, the Information Technology sector has faced a cooling period, down **3.63%** for the year as markets digest the high valuations of the "Magnificent Seven." Central bank policies remain a primary focus. The U.S. Federal Reserve has held the benchmark interest rate steady between **3.5% and 3.75%**. While inflation remains slightly "sticky" around the **3%** mark, the stabilizing unemployment rate has allowed the Fed to pause its easing cycle for the first half of the year. Commodities and Forex Dynamics Commodity markets are witnessing intense volatility. Gold has reclaimed its status as a premier hedge, rising **17.71%** since the start of the year to trade near **$2,800** per ounce. Silver has seen even more aggressive action, jumping **23%** in the same period. Energy prices are reacting to ongoing diplomatic exchanges in Geneva. Brent crude is currently trading near **$70.47** per barrel, while WTI futures sit at approximately **$64.92**. Prices recently eased from higher peaks as progress in U.S.-Iran negotiations reduced the immediate risk of supply disruptions. In the currency space, the U.S. Dollar Index (DXY) has shown resilience despite an early-year downward trend. The Japanese Yen remains under pressure following comments from leadership opposing further rate hikes beyond the current **0.75%** level. Emerging Markets and Technology India continues to be a global standout, with Q3 GDP growth reported at **7.8%**. The Indian manufacturing sector is seeing double-digit expansion, and domestic institutional investors are providing a strong cushion against foreign capital outflows, which reached approximately **₹3,466 crore** in recent sessions. The semiconductor industry is shifting its focus toward "Edge AI"—embedding intelligence directly into devices rather than relying solely on data centers. While AI-driven demand remains high, the industry is navigating a transition from training models to inference-based applications. Memory revenues for 2026 are projected to reach **$200 billion**, accounting for a quarter of total global chip sales. Overall, the global expansion is at a critical juncture. Analysts estimate a **35%** probability of a mild recession later in the year, but the front-loaded fiscal stimulus and robust corporate earnings growth are expected to support a rebound in sentiment through the coming months.

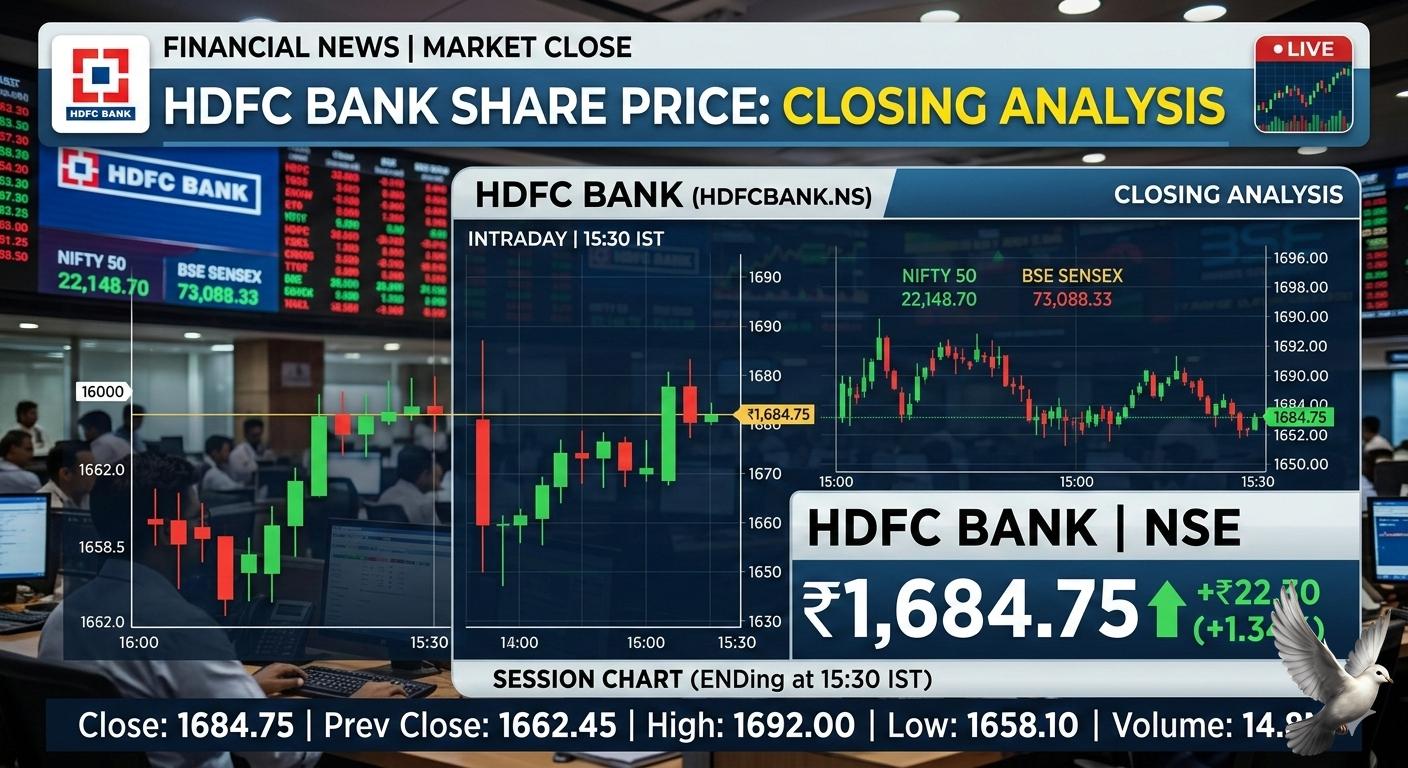

HDFC Bank Share Price: Closing Analysis

Market Brief: Global Financial Landscape **Friday, February 27, 2026** Global equity markets are navigating a period of heightened volatility as the final trading session of February closes. Investor sentiment is currently caught between resilient corporate earnings and significant geopolitical uncertainty. High-growth sectors, particularly those tied to emerging technologies, have faced sharp corrections, while traditional defensive sectors show relative stability. North American Indices Wall Street experienced a split performance in its most recent sessions. The **S&P 500** declined **0.54%** to settle at **6,908.86**, while the tech-heavy **Nasdaq Composite** saw a more pronounced drop of **1.18%**, closing at **22,878.38**. This downward pressure was largely driven by a major sell-off in the semiconductor space; despite beating revenue estimates, industry leader Nvidia fell over **5%**, marking its worst day since early 2025. In contrast, the **Dow Jones Industrial Average** managed a marginal gain of **0.03%**, closing at **49,499.20**. Investors are increasingly rotating capital toward cyclical industries, with financials and industrials outperforming as the broader tech rally cools. The yield on the **10-year Treasury** note eased slightly to **4.03%**, reflecting a cautious move toward safer assets. Asia-Pacific and Emerging Markets Indian markets witnessed a sharp downturn today. The **BSE Sensex** plummeted **961 points** (down **1.17%**), while the **NSE Nifty 50** dropped **311 points** to close below the **25,200** mark. This correction comes despite the government revising its **GDP growth forecast** for the current fiscal year to **7.6%**, following a rebasing of the economic framework to better capture digital economy gains. Across the region, the **Nikkei 225** slid **0.6%**, and South Korea’s **Kospi** declined **1.1%**. Market participants are closely monitoring U.S.-Iran nuclear negotiations in Geneva, as any diplomatic breakthrough or breakdown directly impacts regional risk appetite and energy costs. Commodities and Energy Crude oil prices remain sensitive to the stalling of diplomatic talks in the Middle East. **Brent crude** is trading near **$71.19 per barrel**, while U.S. **West Texas Intermediate (WTI)** rose to **$65.62**. While geopolitical tensions provide a floor for prices, gains are capped by expectations that **OPEC+** may resume production increases in April, potentially adding **137,000 barrels per day** to global supply. Gold continues to serve as a primary hedge against uncertainty. Spot gold prices remained steady near **$5,168 per ounce**, holding significant gains after recently breaching the psychological **$5,000** threshold. Monetary Policy Outlook Central banks are largely adopting a "wait and watch" stance. The **Reserve Bank of India** recently maintained its repo rate at **5.25%**, signaling a neutral stance as it monitors the impact of previous cuts. Globally, the focus remains on the **U.S. Federal Reserve**, with upcoming Producer Price Index (**PPI**) data expected to influence the trajectory of interest rate decisions for the second quarter of 2026.

Tata Steel Share Price: Daily Closing Performance

Market Brief: Late February 2026 Global markets are navigating a complex intersection of geopolitical risk and shifting monetary expectations as February draws to a close. Technical breakouts in commodities are clashing with cautious sentiment in equity and debt markets. Precious Metals Surge Gold prices have demonstrated significant bullish momentum, consistently trading above the **$5,200** per ounce threshold. In domestic markets, 24K gold reached a notable high of **₹160,210** per 10 grams on February 27, marking a **0.54%** daily gain. Silver has mirrored this strength with a dramatic **9%** bounce recently, driven by short-covering in futures markets. Analysts suggest the current bull cycle remains mid-stage, with potential historical targets as high as **$6,750** per ounce by late 2026. Energy Market Breakout Brent crude oil decisively cleared the psychological **$70** per barrel resistance level this week, trading near **$71.35**. This technical shift represents a **10%** increase from end-2025 levels. A "war premium" of **$4** to **$10** per barrel is currently embedded in prices due to stalled nuclear talks and military posturing in the Middle East. WTI crude is following closely, stabilizing around **$66.55** per barrel. Central Bank Watch The US Federal Reserve maintained interest rates at the **3.50% to 3.75%** range following its January pause. Market pricing suggests only one or two additional **25 basis point** cuts for the remainder of 2026. US inflation has shown stickiness, with the Consumer Price Index (CPI) recently recorded at **2.4%**, still above the **2%** target. In India, the RBI held the repo rate steady at **5.25%**, supported by a benign domestic inflation rate of **2.1%** for the current fiscal year. Equity and Economic Trends U.S. equities showed resilience with the S&P 500 up **0.95%** for the week ending February 20. However, the Nasdaq remains down **1.61%** year-to-date as investors reassess spending in the technology sector. Global growth projections for 2026 remain subdued at **2.6%**. Major shifts in trade are emerging, characterized by a **15%** reciprocal tariff environment and the conclusion of several major Free Trade Agreements, including the India-EU pact. The interplay between elevated energy costs and persistent interest rates continues to be the primary driver of market volatility heading into March.

Sensex Drops 961 Points as Market Cap Declines by Rs 5 Lakh Crore Amid Four Key Factors

Market Brief: India Equity Selloff The Indian stock market witnessed a significant downturn on **February 27, 2026**, marking a sharp conclusion to the month as the benchmark indices plunged over **1%**. The **BSE Sensex** crashed by **961.42 points** to settle at **81,287.19**, while the **NSE Nifty 50** dropped **317.90 points**, closing at **25,178.65**. This slide effectively pushed the Nifty below its critical **200-day Exponential Moving Average (EMA)**, signaling a shift in technical sentiment. The session’s volatility resulted in a loss of over **Rs 5 lakh crore** in investor wealth. Market capitalization for BSE-listed firms fell to approximately **Rs 463 lakh crore**, down from **Rs 468.5 lakh crore** in the prior session. Heavyweight financial stocks like **HDFC Bank** and **ICICI Bank** were the primary drags, alongside a late-session selloff that erased midday stabilization efforts. Sectoral Impact and Performance The decline was broad-based, with the **Nifty Realty** index leading the losses, tumbling **2.26%**. Other major sectors under pressure included **Auto**, **Financial Services**, and **FMCG**, all of which saw declines exceeding **1%**. Despite the general gloom, the **Nifty IT** index managed a marginal gain of **0.16%** on the day, though it remains on track for its worst monthly performance since 2008 due to ongoing disruption concerns. The broader market reflected similar stress. The **Nifty Midcap 100** and **Smallcap 100** indices closed down **1.10%** and **1.14%** respectively. Defensive buying was scarce, though the **Nifty Media** index emerged as a rare gainer, ending the day up **0.6%**. Primary Market Drivers Institutional activity remains a key pressure point. Foreign Institutional Investors (FIIs) offloaded equities worth **Rs 3,465.99 crore** in a single session. While Domestic Institutional Investors (DIIs) attempted to cushion the fall by injecting roughly **Rs 5,032 crore**, the scale of global risk-off sentiment outweighed domestic support. Geopolitical tensions between the **US and Iran** have intensified, following statements from Washington hinting at potential military action. This uncertainty has driven **Brent Crude** prices above the **$71 per barrel** mark. For India, elevated oil prices pose a dual threat to the fiscal deficit and the domestic currency. The **Indian Rupee** consequently weakened to **90.95** against the US dollar. Global and Macro Context The domestic selloff mirrors cautious sentiment on Wall Street and mixed performance across Asian markets. Investors are also closely monitoring India's **Q3 GDP data**, with growth estimates hovering between **7.4% and 8.1%**. However, concerns over weak nominal GDP growth and elevated valuation multiples—with the Nifty 50 trading at a P/E ratio of approximately **25x**—continue to make the market sensitive to further corrections.