Bullish News

Collection

Cochin Shipyard, Bharat Forge, HUL, Dr Reddy's, and L&T in focus today

Indian equity markets maintained positive momentum for the third consecutive session as key benchmarks climbed higher. The Nifty 50 finished at **25,819.35**, gaining **0.37%**, while the BSE Sensex rose by **283.29 points** to settle at **83,734.25**. Financial and metal sectors spearheaded the rally, with state-owned banks adding approximately **1.3%**. Metal stocks also surged by **1.3%** following reports of potential easing in international steel tariffs. In the currency market, the Indian rupee appreciated by **6 paise** to close at **90.66** against the US dollar. Cochin Shipyard emerged as a major focal point after being declared the lowest bidder for a Ministry of Defence project. The contract, valued at approximately **5,000 crore**, involves the construction of five Next Generation Survey Vessels for the Indian Navy. The stock responded with a rally of over **5.5%**, reaching an intraday high of **1,574.50**. Bharat Forge demonstrated robust technical momentum, recently hitting a 52-week high of **1,592**. The company reported a significant **111.98%** increase in operating profit, driven by healthy long-term sales growth of over **20%**. Institutional investors remain confident, maintaining a substantial **46.63%** stake in the firm. Hindustan Unilever (HUL) announced a major manufacturing expansion plan involving an investment of **2,000 crore** over the next two years. The capital expenditure will target premium categories in beauty, wellbeing, and home care liquids. This strategic move aims to build a technology-enabled supply chain operating on **100%** renewable energy. Dr. Reddy’s Laboratories strengthened its gynaecology portfolio by acquiring trademarks for specialty brands Progynova and Cyclo-Progynova in India. The deal, valued at **$32.15 million**, integrates brands that recorded sales of **100 crore** in 2025. The company’s latest quarterly revenue stood at **87,268 crore**, reflecting steady growth despite pricing pressures in global markets. Larsen & Toubro (L&T) unveiled a high-tech venture to establish India’s largest gigawatt-scale AI factory. The project will scale GPU cluster deployments at data centers in Chennai and Mumbai, reaching capacities of **30 MW** and **40 MW** respectively. Shares of L&T traded higher following the announcement, as the company’s total data center capital expenditure is estimated near **1,000 crore**.

Asian Equities Gain Following Wall Street Technology Sector Rally

Global Market Update February 19, 2026 Asian equity markets extended their recovery for a second consecutive session today, bolstered by a strong rebound in **U.S. technology shares**. Regional sentiment was further supported by robust economic data, despite light trading volumes as markets in China and Hong Kong remain closed for the Lunar New Year. The **MSCI Asia Pacific Index** climbed **0.6%**, reversing a three-day slide. In Japan, the **Nikkei 225** showed resilience as investors shifted back into hardware and chip-making stocks, which are central to the global electronics supply chain. Tech Sector and AI Sentiment Investor confidence is stabilizing as markets reassess the long-term impact of artificial intelligence. While early February saw the **Nasdaq 100** dip due to concerns over high valuations, recent earnings reports have provided a necessary cushion. The **S&P 500** remains supported by an earnings cycle in expansion mode, with **Q4 2025** blended earnings growth reaching **13.2%**. Information technology revenues specifically surged **20.6%**, led by massive prints from **Apple ($143.76B)** and **Microsoft ($81.27B)**. Investors now view the recent tech sell-off as a temporary overreaction. However, the forward **P/E ratio** for the **S&P 500** stands at **21.5**, suggesting the margin for error remains slim as growth rates are expected to normalize throughout **2026**. Energy and Commodities Oil prices maintained their recent upward trajectory, marking the most significant gains since last October. **WTI Crude** is trading near **$63.66** per barrel, up **1.22%**, while **Brent Crude** sits at approximately **$68.47**. Supply risks are currently the primary driver of price action. Market participants are monitoring naval drills near the **Strait of Hormuz**, a critical transit point for global crude. This geopolitical tension has added a risk premium to prices, even as the **IEA** forecasts a potential supply surplus later this year. Global oil demand is projected to rise by **850,000 barrels per day** in **2026**, with growth concentrated almost entirely in non-OECD economies, particularly in Asia. Economic Outlook The **IMF** has revised its global growth projection for **2026** slightly upward to **3.3%**. This resilience is attributed to steady technology investment and private sector adaptability. In the United States, consumer liquidity is expected to receive a boost from tax refunds. Early **2026** data indicates average refunds are up **10.9%** to **$2,290**, which may serve as a catalyst for a consumer-led revival in the coming months. This [Global Market Update](https://www.youtube.com/watch?v=u6KQYIW5XKo) provides deeper context on how enterprise technology and AI spending are shaping the current economic landscape. http://googleusercontent.com/youtube_content/0

LGT Prince: India Growth Hindered by Regulatory Complexity

LGT Group has identified India as a central pillar of its global international strategy, targeting a wealth management market currently valued at 154.25 billion USD. With projections suggesting this market will climb to 286.91 billion USD by 2030, the firm is intensifying its local operations to capture a larger share of the country's rapidly expanding affluent class. The group reported a strong financial performance for the first half of 2025, with total operating income rising 10% to 1.42 billion CHF. Group profits saw a significant 38% surge to 240.6 million CHF during this period. These gains come despite negative currency effects that slightly adjusted total assets under management to 359.6 billion CHF as of mid-2025. Prince Max von und zu Liechtenstein, Chairman of LGT, continues to emphasize that India is a key growth market capable of becoming a highly meaningful contributor to the group’s global footprint. To support this, LGT Wealth India recently expanded its leadership by onboarding a seven-member senior team from Barclays Private Bank. This move reinforces the firm’s commitment to providing high-touch advisory services to Ultra-High-Net-Worth families. Market dynamics in India are shifting toward more sophisticated financial instruments. Local Chief Investment Officers at the firm anticipate a return to double-digit corporate earnings growth by 2026. Key growth sectors include Information Technology, driven by 100 billion USD in quarterly global AI infrastructure spending, and the financial services sector, which is expected to account for nearly 50% of the index’s incremental earnings through 2028. Investor behavior in the region is maturing, with a marked shift from physical assets like gold and real estate toward financial savings. High-Net-Worth individuals are increasingly diversifying into alternative investments, including private credit and ESG-focused funds. The number of millionaires in India grew by 5.6% last year, and the total population of High-Net-Worth individuals is expected to reach 611,000 by the end of 2025. LGT is addressing these opportunities through a multi-year 200 million CHF investment in digitalization and artificial intelligence. These tools are designed to enhance internal efficiency and provide hyper-personalized portfolio recommendations, catering to a younger demographic of investors who prioritize transparency and sustainability alongside long-term capital appreciation. While navigating complex regulatory landscapes remains a priority, the firm maintains a disciplined outlook. By blending global investment expertise with deep local market knowledge, LGT aims to solidify its position as a preferred platform for India's evolving wealth ecosystem.

Metal Stocks Rise on Expectations of Strong Q4 Results

Indian Metal Sector: Market Brief February 2026 The Indian metal sector is maintaining a robust growth trajectory as of mid-February 2026. The Nifty Metal Index reached **11,985.75** on February 18, reflecting a steady **3.06%** gain over the last month and a remarkable **46%** surge over the past year. This performance significantly outpaces the broader benchmark indices, driven by a combination of domestic policy support and a stabilizing global demand outlook. Steel Sector Dynamics Steel stocks are leading the rally, with major players like Tata Steel and JSW Steel gaining between **1% and 2%** in recent intraday sessions. Domestic Hot-Rolled Coil (HRC) prices are currently averaging approximately **₹50,500** per ton. Market sentiment is bolstered by a **12% safeguard duty** implemented in late 2025, which has successfully shielded domestic producers from cheap imports and allowed for a price realization increase of roughly **₹3,500** per ton quarter-on-quarter. Demand is projected to grow by **9%** through 2026, fueled by aggressive infrastructure spending and a resurgent automotive sector. Non-Ferrous and Strategic Metals Non-ferrous producers are benefiting from a recovery in global commodity prices. Aluminum rose to **$3,084.50** per ton this week, marking a **14.93%** increase compared to last year. In the domestic scrap market, copper is trading at approximately **₹1,250** per kg for high-grade variants, while Zinc-Hindustan rates are holding firm at **₹347** per kg. A weaker rupee continues to provide a competitive edge for exporters, while limited global supply caused by energy-related smelter disruptions in other regions is keeping local inventories tight and prices elevated. Policy and Long-term Outlook The Ministry of Steel has recently reaffirmed its goal to reach a crude steel capacity of **300 million tonnes** by 2030. Current efforts are focused on a "Green Steel" transition, with the government introducing incentives for scrap recycling and low-carbon production technologies. Operating margins for the sector are stabilizing around **12.5%**. While raw material costs—specifically coking coal—showed some volatility early in the year, the current quarter remains seasonally strong for volume growth. Investors are closely watching the upcoming 2026 industrial roadmaps which emphasize digital integration and domestic value addition to reduce reliance on high-grade alloy imports.

**Indian Banks Eye \$15 Billion Opportunity as M&A Funding Norms Ease**

The Indian banking sector is on the verge of a structural transformation following the finalization of the Reserve Bank of India (RBI) guidelines for acquisition financing. These norms, set to take effect for the next financial year (FY27), dismantle long-standing barriers that prevented domestic banks from funding the purchase of corporate shares. This shift is expected to unlock a massive domestic credit market, previously the exclusive domain of offshore lenders, private credit funds, and Non-Banking Financial Companies (NBFCs). The revised framework allows commercial banks to finance up to 75% of an acquisition’s total value. To ensure "skin in the game," the acquiring entity must contribute the remaining 25% through equity or internal accruals. This is a significant expansion from previous drafts and signals the central bank’s growing confidence in the risk management capabilities of Indian lenders. Prudential safeguards remain central to the rollout. The post-acquisition consolidated debt-to-equity ratio is capped at 3:1 to prevent excessive leverage. Furthermore, the RBI has established a tiered eligibility system: listed acquirers must have a minimum net worth of 500 crore INR and a three-year track record of profitability. Unlisted companies can also participate but must hold an investment-grade credit rating of at least BBB-minus. The timing aligns with a significant surge in deal-making activity. Domestic consolidation in India reached a robust 104 billion USD in 2025, a two-year high driven by sectors like financial services, automotive, and technology. Total M&A value across the country climbed 37% year-on-year by the end of Q3 2025, reaching 26 billion USD in that quarter alone. Automotive led the charge in value, notably through Tata Motors' 4.45 billion USD acquisition of Iveco. For the banking system, this represents a major new asset class. Total bank credit in India crossed a historic milestone of 200 lakh crore INR in early 2026, with public sector banks currently outpacing private rivals in credit growth for the first time in over a decade. By allowing these banks to fund strategic, synergy-driven acquisitions, the RBI is positioning domestic capital to anchor India’s corporate expansion. The new rules also include sub-limits within the Capital Market Exposure (CME) framework. While a bank’s aggregate CME is capped at 40% of its Tier 1 capital, direct exposure and specific acquisition finance are each capped at 20%. These calibrated limits ensure that while the 10-15 billion USD annual financing opportunity is realized, the banking system remains insulated from volatile market swings. As 2026 progresses, the combination of healthy corporate balance sheets and this liberalized funding environment is expected to maintain momentum in mid-market deals and large-scale consolidations alike. The transition from offshore-dominated financing to a domestic bank-led model is likely to reduce the cost of capital for Indian corporates and foster a more self-reliant financial ecosystem. The comprehensive guidelines for acquisition financing can be explored in the [RBI Draft Rules](https://law.asia/rbi-acquisition-finance-draft-directions/), which details the eligibility and risk management requirements for banks entering this new asset class. This video provides an expert analysis of how the recent RBI reforms and the surge in M&A financing are evolving the Indian financial services landscape in 2026.

RBI Mandates Unique Transaction Identifiers for OTC Derivative Trades

The Reserve Bank of India has introduced a major regulatory overhaul for the over-the-counter (OTC) derivative markets, mandating the use of Unique Transaction Identifiers (UTIs) for all trades starting January 1, 2027. This directive, finalized in February 2026, applies to all direct private trades in rupee interest rate derivatives and foreign currency instruments. The move is designed to bring India’s reporting standards in line with global financial practices. By assigning a 52-character code to every contract, the RBI aims to create a permanent audit trail that remains constant throughout the lifecycle of a trade. This will allow regulators to aggregate data effectively and monitor systemic risks in a market that has seen significant scale. Recent data highlights the importance of this oversight. India’s foreign exchange market reached a valuation of approximately 33.40 billion USD in 2025 and is projected to grow at a compound annual rate of 8.4% through 2034. Within this space, currency swaps currently lead with a 40.28% market share, while reporting dealers facilitate 42.1% of all transactions. In the interest rate segment, the RBI’s recent policy shift provides a backdrop of stability for these derivatives. Following a cycle of 125 basis points in rate cuts during the 2024-2025 period, the central bank held the repo rate steady at 5.25% in February 2026. This "neutral" stance is intended to support a projected GDP growth of 7.4% for the 2025-2026 fiscal year while keeping inflation near the 4% target. The UTI mandate specifically targets OTC instruments such as forward contracts in government securities, credit derivatives, and overnight index swaps. Previously, market participants relied on internal deal numbers, which often led to inconsistencies between counterparties. Under the new framework, if a transaction is reported without a UTI, the Clearing Corporation of India Limited (CCIL) will generate one automatically to ensure no trade remains untracked. Financial institutions, including large private banks and corporate treasuries, are now required to upgrade their internal systems to handle these identifiers. While this transition may involve initial compliance costs, the structural shift is expected to reduce counterparty credit risk. To further deepen the market, the government also recently announced the introduction of total return swaps on corporate bonds and new derivatives on corporate bond indices. The timeline through 2027 provides a clear window for the industry to adapt. Operational guidelines from the CCIL are expected shortly to assist with the technical transition, ensuring that India’s derivatives ecosystem—which recently saw cumulative FDI inflows hit the 1 trillion USD milestone—remains transparent and resilient against global volatility.

**Indian Steel Sector Anticipates Multiple IPOs Over the Next Eight to Ten Months**

India’s steel sector is entering a high-velocity phase of primary market activity. Over the next eight to ten months, at least 10 steel producers and related entities are set to launch IPOs. These companies aim to raise between **₹5,000 crore** and **₹7,000 crore**. The momentum is supported by a robust domestic demand outlook. For the 2025-26 period, steel consumption in India is projected to grow by **9%** to **10%**. This outpaces the global demand forecast, which remains muted at roughly **1.2%**. Market activity is picking up as of February 2026. Domestic steel indices show a steady uptrend, with the BigMint India Steel Composite Index recently rising **1.7%**. This reflects higher mill prices and improving sentiment as the fourth quarter of the fiscal year begins. Key prices have seen upward revisions to counter rising input costs. Primary mills have hiked rebar prices by up to **₹3,000** per tonne. Hot-rolled coil (HRC) trade prices currently hover around **₹53,800** per tonne, while cold-rolled coil (CRC) is priced near **₹59,400** per tonne. The industry is undergoing a massive capacity expansion. India’s crude steel production capacity has already hit **205 million tonnes (MT)**. Major players are driving this further, with the national goal set at **300 MT** by 2030. Government intervention is a critical driver for this growth. A **12% safeguard duty** introduced in December 2025 has helped protect domestic manufacturers from cheap imports. Additionally, the Production Linked Incentive (PLI) scheme has attracted committed investments of over **₹27,100 crore** for specialty steel. Infrastructure and defense remain the primary consumers. However, newer segments like electric vehicles and renewable energy are emerging as major demand drivers for high-grade steel. Listed steel stocks are reflecting this positive environment. In mid-February 2026, shares of leaders like Tata Steel and JSW Steel gained up to **2%** in a single session. Many top-tier steel stocks have outperformed the broader benchmark indices by **7%** to **16%** over the last month. Expansion remains the priority for capital use. Tata Steel alone has committed **₹15,000 crore** in capital expenditure for the 2025-26 fiscal year. These funds are being directed toward scaling production and modernizing plants to meet stricter environmental standards. While global conditions remain volatile, the Indian steel market is decoupling from international slowdowns. Tighter inventory levels at primary mills—down nearly **40%** month-on-month in early February—suggest a supply-side crunch that could sustain price levels in the near term.

AI to Drive Modernization Rather Than Disruption, Says Barclays CEO C.S. Venkatakrishnan

India is solidifying its status as a premier global growth engine, with recent forecasts projecting real GDP to expand by 8.2% in the current fiscal cycle. This momentum is expected to remain robust, with estimates for 2026-27 hovering between 6.8% and 7.2%. The nation’s digital economy is scaling rapidly, currently accounting for 10% of GDP and on track to reach 20% by 2026. This shift is headlined by the Unified Payments Interface (UPI), which now processes approximately 49% of all global real-time transactions. In November 2025 alone, UPI recorded over 19 billion transactions valued at 24.58 trillion rupees. Barclays CEO C. S. Venkatakrishnan emphasizes that India’s digital transformation is moving beyond basic access into a phase of "Intelligent India." AI is viewed as a critical modernizing force rather than a threat to employment. Current data shows AI adoption among Indian firms has surged from 8% in 2023 to 25% by 2024, with generative AI projected to add up to 438 billion dollars to the economy by 2030. The global credit environment is entering a sensitive phase as the era of cheap borrowing concludes. Market analysts highlight a tightening credit cycle, with global sovereign outlooks shifting toward more cautious territories. Rising debt and funding costs are pressuring developed markets, while emerging economies face increased volatility. Geopolitical dynamics are increasingly mirroring the structural shifts of the 1970s and 80s. The decline of hyper-globalization has forced nations to prioritize supply chain security and bilateral trade agreements. India’s strategic focus on securing critical minerals and its new trade deals with the U.S. and EU are central to this realignment. Despite global trade uncertainties and tariff risks, India’s external buffers remain formidable. Foreign exchange reserves stand at approximately 701.4 billion dollars, providing nearly 11 months of import cover. Inflation has also softened significantly, with core figures hitting historic lows near 2% in late 2025. The infrastructure landscape is also pivoting toward sustainability. India recently achieved 50% of its electricity capacity from non-fossil sources, reaching 262.74 GW. This convergence of green energy and digital infrastructure is creating a resilient foundation for long-term industrial expansion. Capital markets reflect this optimism, with FDI in computer software and hardware making up over 15% of cumulative inflows. The startup ecosystem has also rebounded, securing 10 billion dollars in funding during recent cycles, signaling a transition from capital preservation to profitable growth.

Pernod Ricard Explores Stock Market Listing for India Unit

Pernod Ricard is reportedly exploring a separate stock market listing for its Indian subsidiary. Preliminary talks with financial advisors are currently underway as the French drinks giant seeks to unlock value in its second-largest global market. The move comes at a critical time for the brand in India. Recent financial filings for the 2024-25 fiscal year show Pernod Ricard India maintaining its position as the country's leading alcoholic beverage firm by value. The company reported consolidated sales of 27,445.80 crore rupees, narrowly edging out its primary competitor, Diageo India. Profitability remains strong despite complex local regulations. The Indian unit recorded a net profit of 1,734.59 crore rupees in the latest fiscal cycle, marking an 8% increase from the previous year. This growth is largely driven by a aggressive "premiumization" strategy, as consumers shift toward high-end spirits like Chivas Regal, Glenlivet, and Jameson. The potential IPO follows a year of significant portfolio shifts. Pernod Ricard recently hived off its popular Imperial Blue brand to Tilaknagar Industries for approximately 3,442 crore rupees. This divestment allows the firm to focus on higher-margin, super-premium categories where demand is surging. However, the path to a public listing faces notable regulatory hurdles. The company is currently navigating an investigation by the Competition Commission of India into alleged collusion with retailers in southern states. Simultaneously, it is contesting a federal tax demand of roughly $250 million related to liquor import valuations. Market dynamics in India remain highly attractive for investors. The domestic alcohol sector is projected to reach a valuation of over $208 billion by late 2026. Experts anticipate a steady growth rate of 7.2% through the next decade, fueled by a young demographic and rising disposable incomes in urban centers. A local listing would offer Pernod Ricard a dedicated capital structure to navigate India's state-specific tax laws and licensing frameworks. With the Indian spirits market outperforming global averages, a successful IPO could set a new benchmark for multinational beverage players in the region.

Starbucks Investor Group Seeks Board Changes Amid Labor Dispute

Starbucks is currently navigating a pivotal transformation period as shareholders prepare for the 2026 Annual Meeting on March 25. A coalition of institutional investors, including the New York City Comptroller, is formally urging a vote against the re-election of directors Jørgen Vig Knudstorp and Beth Ford. The pressure stems from what investors describe as sustained oversight failures regarding labor relations. Despite a public commitment to reach a first contract with the Starbucks Workers United union by the end of 2024, negotiations have reportedly stalled. To date, no collective bargaining agreement has been ratified for the more than 11,000 unionized baristas across 490 stores. Financial and operational risks are mounting alongside these disputes. In December 2025, Starbucks reached a record 38.9 million dollar settlement with New York City over Fair Workweek Law violations. Furthermore, the "Red Cup Rebellion" strikes have expanded to over 670 locations, impacting brand reputation and consistent store performance. On the market front, the "Back to Starbucks" strategy led by CEO Brian Niccol is showing early signs of financial recovery. For the first quarter of fiscal 2026, the company reported total revenue of 9.9 billion dollars, a 6% increase year-over-year. Global comparable store sales grew by 4%, marking the first U.S. transaction growth in eight quarters. Stock performance remains steady but cautious. As of mid-February 2026, Starbucks shares are trading around 95.39 dollars, with a market capitalization of approximately 107 billion dollars. While revenue is rising, operating margins have contracted to 10.1% due to heavy investments in labor and technology. Management continues to emphasize a "partners-first" approach, highlighting significant investments in worker benefits and store-level technology. However, the investor group argues that the recent elimination of the Board’s dedicated labor oversight committee signals a retreat from these promises. The outcome of the March director vote will likely serve as a referendum on whether the current leadership can balance aggressive financial growth with the resolution of long-standing labor conflicts. For now, the company maintains its fiscal 2026 guidance, targeting earnings per share between 2.15 and 2.40 dollars while continuing its global expansion.

Market Outlook: 10 Key Factors Influencing Thursday's Trading Action

Indian equity markets demonstrated resilience as the Nifty 50 and BSE Sensex extended their winning streak for a third consecutive session. Gains were primarily fueled by a strong showing in the metal and PSU banking sectors, which managed to offset continued weakness in the IT space. **Benchmark Performance** The **BSE Sensex** rose by **283.29 points** or **0.34%** to settle at **83,734.25**. The **Nifty 50** climbed **93.95 points** or **0.37%** to finish at **25,819.35**. **Market Breadth and Institutional Activity** The overall market sentiment remained positive, with the **Nifty Midcap 100** adding **0.50%** to reach **60,183.20**. Institutional data revealed a supportive environment as **Foreign Institutional Investors (FIIs)** turned net buyers, purchasing shares worth **₹995.21 crore**. **Domestic Institutional Investors (DIIs)** also remained on the buy side with a net inflow of **₹187.04 crore**. **Sectoral Highlights** **Top Gainers**: Metal stocks and state-owned lenders led the rally. Individual standouts included **Kwality Wall’s** (up **4.97%**), **HDFC Life** (up **3.39%**), and **Tata Steel** (up **2.84%**). **Top Losers**: The IT sector faced renewed pressure. **Wipro** declined **1.64%**, while **Tech Mahindra** and **Infosys** fell by **1.56%** and **1.38%** respectively. **Macroeconomic Landscape** The market is reacting to a backdrop of cooling inflation. India's retail inflation (CPI) eased significantly to a seven-month low of **3.61%**, down from **4.26%** in the previous month. This cooling was largely driven by a sharp drop in food inflation, which fell by **222 basis points** to **3.75%**. Industrial activity remains robust, with the **Index of Industrial Production (IIP)** expanding by **5.0%**, surpassing market expectations. Growth was particularly strong in manufacturing (**5.5%**) and electrical equipment (**21.7%**). **Technical Outlook** Analysts anticipate a period of consolidation following this three-day rally. **Nifty 50 Support/Resistance**: Immediate support is identified at **25,600**, with a deeper demand zone at **25,300**. Resistance is capped at **26,000**, which serves as a significant psychological barrier. **Sensex Support/Resistance**: The index finds key support near **83,000**, while resistance is expected between **83,850 and 83,950**. The short-term bias remains sideways-to-bullish, though investors are advised to track global cues and continued FII flows as the indices approach these overhead hurdles. [Indian Stock Market Today: Latest on Nifty and Sensex](https://www.youtube.com/watch?v=qCwV0unkLWg) This video provides a deep dive into the latest retail inflation and industrial production data, which are key drivers for current market movements. http://googleusercontent.com/youtube_content/0

**Pinterest Stock Climbs as Revenue Outlook Increases Following tvScientific Partnership**

Pinterest has finalized its acquisition of tvScientific, marking the platform’s most significant move in the ad-tech space since 2022. This deal, valued by industry analysts in the range of **$300 million** to **$350 million**, directly integrates performance-driven Connected TV (CTV) capabilities into Pinterest’s existing advertising ecosystem. The transaction has immediate financial implications, as Pinterest recently raised its first-quarter 2026 revenue guidance to a range of **$958 million** to **$978 million**. This update, which incorporates partial-quarter contributions from tvScientific, reflects a year-over-year growth target of **11%** to **14%**. The company also projected Adjusted EBITDA between **$163 million** and **$183 million** for the same period. Strategically, the acquisition addresses the rising demand for accountability in television advertising. By merging its high-intent shopper data with tvScientific’s outcome-based engine, Pinterest enables brands to track whether a TV ad leads to a specific purchase. This "closed-loop" measurement is critical as the U.S. CTV ad market is projected to reach **$37.95 billion** by the end of 2026. The integration focuses on Pinterest’s "Performance+" suite, an AI-powered tool designed to automate media buying and optimize campaigns across multiple screens. With over **600 million** monthly active users and a **14%** increase in 2025 annual revenue, Pinterest is positioning itself to capture a larger share of performance budgets. This shift is particularly relevant as **69%** of viewers now use a second screen, such as a mobile phone, while watching TV. While the deal strengthens Pinterest’s competitive stance against larger players, the company faces a complex macroeconomic environment. Executives have noted potential headwinds from new tariffs and intense competition from Meta and Google, which may impact ad spending volatility. Despite these challenges, the platform maintains a strong liquidity position with a cash and equivalents balance of approximately **$2.7 billion**. This acquisition signals a broader industry trend where the lines between social media performance and traditional brand awareness are disappearing. By owning the underlying technology for CTV attribution, Pinterest aims to offer advertisers a unified system that connects mobile intent with large-screen impact, moving beyond "views and vibes" toward measurable return on ad spend.

**Hassett Critiques New York Fed Tariff Research Amid Policy Debate**

Market Brief: US Import Tariffs and Domestic Cost Dynamics The domestic economic landscape is shifting as recent data confirms that the burden of massive import tax increases is falling almost entirely on American shoulders. While the administration has historically argued that foreign exporters would absorb these costs, a landmark report from the New York Fed released in February 2026 reveals a different reality. Key data points show that U.S. firms and consumers bore 94% of the tariff burden during the first eight months of 2025. By November, this figure adjusted slightly to 86%, yet the overarching trend remains clear: the domestic economy is footing the bill for trade policy shifts. The average effective tariff rate on U.S. imports surged from a mere 2.6% at the start of 2025 to 13.5% by early 2026. This is the highest level of import taxation recorded since 1946. The Treasury Department reported collecting $287 billion in customs duties and fees in 2025 alone, a staggering 192% increase compared to the previous year. At the household level, the impact is becoming tangible. Analysts estimate that the current tariff structure resulted in a $1,000 cost increase per U.S. household in 2025, with that figure projected to rise to $1,300 in 2026. These costs are primarily driven by "pass-through" pricing, where importers raise retail prices to maintain margins. Sector performance shows significant price divergence. Personal Consumption Expenditure (PCE) for core goods rose 1.5% through late 2025, while durable goods—those most exposed to international supply chains—saw even sharper climbs. Imported durable goods prices are currently 3.1% above their pre-2025 trends. Global trade flows are also reconfiguring. China’s share of U.S. imports dropped below 10% for the first time in decades as businesses moved sourcing to Mexico and Vietnam to mitigate tax exposure. However, even with these shifts, the cost of domestic-affected goods has risen, as local producers often raise prices in tandem with their newly expensive foreign competitors. While the administration points to robust GDP growth of 4.3% in late 2025 as evidence of a successful "Buy American" strategy, the New York Fed research suggests these gains may be tempered by long-term productivity losses. The central bank's findings have been echoed by other international bodies, including the Kiel Institute, which found that foreign exporters absorbed only 4% of the total tax burden. Looking ahead, market volatility remains tied to the legal and political status of these measures. With roughly $168 billion in potential refunds pending a Supreme Court decision on emergency tariff powers, businesses are navigating a high-stakes environment where the cost of entry for foreign goods has become a permanent fixture of the domestic price index.

Bank of India and Select PSU Bank Stocks Project Up to 8% Upside Potential

The Nifty 50 extended its winning streak to a third consecutive session on February 18, 2026, closing at **25,819.35**. This represents a gain of **93.95 points** or **0.37%**. The index successfully reclaimed key support levels, demonstrating resilience despite early-session volatility. Broad-based buying across the Metal, FMCG, and PSU Bank sectors fueled the rally. Market participants witnessed a significant wealth addition of nearly **₹2 lakh crore** as the total market capitalization of BSE-listed firms rose to approximately **₹472 lakh crore**. Nifty 50 Technical Outlook The index is currently testing immediate resistance in the **25,900 – 25,950** zone. Technical analysts suggest that a sustained move above this range could pave the way for a psychological target of **26,000**, with further upside potential reaching toward **26,300** in the short term. On the downside, the **25,700 – 25,650** zone is acting as immediate support. The broader structure remains constructive as long as the index holds above the **25,500** demand base. Banking Sector Breakouts Public Sector Banks (PSBs) emerged as top performers, with the Nifty PSU Bank index rising **1.31%**. Key breakouts in mid-tier state-run lenders have signaled fresh bullish momentum. **Bank of Maharashtra (MAHABANK)** The stock hit a new **52-week high** of **₹69.21** during intraday trade, eventually settling at **₹69.00**. This reflects a daily gain of **2.52%**. The bank has seen a cumulative appreciation of **4.28%** over the last three days, supported by high trading volumes of over **31 million shares**. **Bank of India (BANKINDIA)** Shares surged to a **52-week high** of **₹173.29** before closing at **₹172.40**, up **1.29%**. The stock has maintained strong upward momentum, gaining over **6%** within the last week. Momentum indicators like the RSI and MACD remain in bullish territory, suggesting continued strength. Market Drivers and Sentiment Sectoral performance was led by **Nifty Metal (up 1.33%)** and **Nifty FMCG (up 1.21%)**. Top individual gainers included Kwality Walls, which jumped **4.94%**, and HDFC Life, which rose **3.37%**. In contrast, the **Nifty IT index (down 1.23%)** was the sole laggard among major sectors. Selling pressure in heavyweights like Wipro and Tech Mahindra capped the overall gains of the benchmark index. Foreign Institutional Investors (FIIs) turned net buyers in the previous session with an inflow of **₹995.21 crore**, while Domestic Institutional Investors (DIIs) also remained positive, contributing **₹187.04 crore** to the market liquidity. Global cues remained largely supportive. While major Chinese and Hong Kong markets were closed for the Lunar New Year, the Japanese Nikkei gained over **700 points**, providing a positive backdrop for the late-session surge in Indian equities.

US Stocks Edge Up Amid Tech Rebound and Anticipation of Fed Minutes

Market Brief: February 18, 2026 Indian equity benchmarks extended their winning streak to a third consecutive session as domestic markets staged a late-hour recovery. Despite a cautious opening and persistent global uncertainties, a surge in buying during the final hour pushed the indices higher. The **BSE Sensex** climbed **283.29 points**, or **0.34%**, to settle at **83,734.25**. The **NSE Nifty 50** gained **93.95 points**, or **0.37%**, closing at **25,819.35**. Investor wealth saw a significant boost, with the total market capitalization of BSE-listed firms rising by approximately **₹2 lakh crore** to reach nearly **₹472 lakh crore**. Sector Performance and Key Drivers While the broader market momentum turned positive, sectoral performance remained polarized. The **Nifty IT** index faced headwinds, sliding **1.23%** as major players like **Infosys** and **Tech Mahindra** underperformed due to concerns over margin pressures. In contrast, the **Metal** and **PSU Bank** sectors led the gains, rising **1.33%** and **1.31%** respectively. Consumer-facing stocks also saw traction, with **ITC** jumping over **2.1%** following prospects of price hikes in the cigarette segment. * **Top Gainers:** Tata Steel (**+2.93%**), HDFC Life (**+3.37%**), and ITC (**+2.15%**). * **Top Laggards:** Wipro (**-1.73%**), Infosys (**-1.26%**), and Tech Mahindra (**-1.25%**). Global Technology and AI Influence Sentiment in the tech space was heavily influenced by **Nvidia’s** multi-year partnership expansion with **Meta**. Nvidia shares rose over **2%** after confirming a deal to supply millions of AI chips for Meta’s infrastructure buildout, which includes the deployment of Blackwell and Rubin GPUs. While this boosted megacap sentiment in the US, it put pressure on rival chipmakers. Meta's capital expenditure forecast for 2026 remains aggressive, projected between **$115 billion and $135 billion**. Macroeconomic Outlook and Interest Rates Investors remain laser-focused on the **US Federal Reserve**, which recently held interest rates steady in the **3.50% to 3.75%** range. Market participants are analyzing minutes and economic data for signs of a potential **25 basis point cut** later this year. On the domestic front, India's retail inflation for January 2026 was reported at **2.75%** under a newly revised series with a **2024 base year**. While food inflation stood at **2.13%**, the overall cooling trend has reinforced expectations that the **Reserve Bank of India** may maintain a stable policy environment in the medium term. Foreign and Domestic Flows Institutional activity provided a supportive floor for the indices. Foreign Institutional Investors (**FIIs**) were net buyers, purchasing equities worth **₹995.21 crore**, while Domestic Institutional Investors (**DIIs**) added **₹187.04 crore** to their holdings. Crude oil remains a factor for the trade balance, with **Brent crude** trading at approximately **$67.64 per barrel**, reflecting a slight daily increase of **0.33%**.

RBI Mandates Unique Transaction Identifiers for All OTC Derivative Trades Effective January 1, 2027

The Reserve Bank of India (RBI) has introduced a significant shift in the oversight of over-the-counter (OTC) markets. Effective January 1, 2027, the Unique Transaction Identifier (UTI) will be mandatory for all direct private trades involving rupee interest rate and foreign currency derivatives. The UTI is a global 52-character code designed to identify specific transactions, complementing the existing Legal Entity Identifier (LEI) which identifies the parties involved. This move aligns India with global standards set by the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO). **Regulatory Timeline and Context** The implementation date of January 1, 2027, represents an extension from an earlier proposed timeline of April 2026. This adjustment provides market participants additional time to upgrade technical systems and reporting frameworks. The mandate covers a broad spectrum of instruments, including: - Rupee interest rate swaps (IRS) - Forward contracts in government securities - Foreign currency derivatives - Credit derivatives **Current Market Landscape** As of early 2026, the Indian rupee has faced persistent volatility, recently trading near 90.56 against the US dollar. This depreciation, up from 83 levels in 2024, has driven record demand for hedging instruments among exporters and corporates. Interest rate dynamics also remain a core focus. The RBI maintained the repo rate at 5.25% in its February 2026 meeting, following a 25-basis-point cut in December 2025. With inflation projected at 2.1% for the 2025-26 fiscal year and GDP growth forecasted at 7.4%, the demand for sophisticated risk management tools is at an all-time high. **Market Growth and Data Trends** The OTC interest rate derivative market has seen a massive surge in activity. Global data indicates that daily average turnover for these instruments reached 7.9 trillion dollars in 2025, a 59% increase from 2022. In India, the Clearing Corporation of India Limited (CCIL) continues to serve as the primary trade repository. The new UTI mandate will require all trades entered into after the 2027 start date to be reported with the unique identifier, allowing regulators to aggregate global exposures and identify systemic risks more effectively. **Strategic Implications** For market participants, the transition requires a "waterfall mechanism" to determine which entity generates the UTI for a specific trade. Banks and financial institutions must now focus on: - Integrating UTI generation into automated trade feeds. - Ensuring data integrity across the 52-character alphanumeric strings. - Harmonizing reporting with international counterparts to avoid duplicate or inconsistent data. While the administrative burden on sales desks and compliance teams will increase, the long-term benefit is a more transparent and stable derivatives ecosystem. This transparency is critical as India's outward foreign direct investment nearly doubled to 6.8 billion dollars in late 2025, reflecting deeper integration with global financial markets.

Liberty Global Acquires Vodafone’s 50% Stake in VodafoneZiggo for $1.18 Billion

Vodafone has officially confirmed the sale of its 50% stake in the Dutch joint venture VodafoneZiggo to its partner Liberty Global. The transaction is valued at 1 billion euros ($1.08 billion) in cash, alongside a 10% equity interest in a newly formed entity named Ziggo Group. This strategic move marks the end of a decade-long partnership and the creation of a regional powerhouse. Ziggo Group will consolidate Liberty Global’s major Benelux assets, including the 100% interest in VodafoneZiggo and the Belgian telecom operator Telenet. The deal highlights significant financial shifts for both companies. Vodafone shares climbed 4.3% following the announcement, as investors welcomed the cash influx. Liberty Global’s stock also saw a sharp 8.6% rise in New York, reflecting market confidence in the consolidation strategy. The transaction is valued at approximately 7.1 times the estimated 2025 adjusted EBITDA. Liberty Global plans to list Ziggo Group on Euronext Amsterdam in 2027, with intentions to spin off 90% of the shares to its current shareholders. Operationally, Vodafone will continue to support the Dutch business. The two firms have established a long-term service agreement where Vodafone will provide brand licensing and technical services for a total consideration of 625 million euros over the next 10 years. The Dutch telecom market remains highly competitive, valued at approximately 9.1 billion euros in 2025. VodafoneZiggo currently maintains a strong footprint, reporting quarterly revenue of 1.02 billion euros and adjusted EBITDA of 425 million euros. The new Ziggo Group aims to generate approximately 500 million euros in adjusted free cash flow by 2028. The company is also targeting a combined net present value of 1 billion euros in synergies through this regional integration. Regulatory approvals are required before the deal can finalize. Completion is expected in the second half of 2026. Until then, both VodafoneZiggo and Telenet will continue to operate under their existing brands and management teams. This divestment allows Vodafone to streamline its European portfolio while maintaining a 10% upside in the enlarged Benelux entity. For Liberty Global, the move simplifies its corporate structure and prepares its regional assets for a major public listing.

SEBI Establishes Working Group to Review Regulatory Framework for ESG Rating Providers

SEBI Market Update: ESG Rating Framework Review The Securities and Exchange Board of India (SEBI) has officially constituted a dedicated working group to conduct a comprehensive review of the regulatory framework for **ESG Rating Providers (ERPs)**. This move, announced on **February 18, 2026**, follows extensive feedback from market participants and aims to align India’s sustainability standards with evolving global practices. The sustainable finance market in India has seen exponential growth, reaching a valuation of approximately **$653.76 billion** in 2025. Projections indicate this sector could expand to **$2.42 trillion** by 2034, maintaining a compound annual growth rate (CAGR) of **14.44%**. This rapid scaling necessitates a more robust oversight mechanism for the agencies responsible for scoring corporate environmental, social, and governance performance. Structural Composition and Mandate The newly formed working group includes a diverse range of stakeholders: * Domestic and global ESG Rating Providers * Institutional investors and ESG analysts * Legal experts, academics, and corporate issuers The group’s primary mandate is to enhance transparency and reliability in ratings. It will examine current methodologies to mitigate "greenwashing" and address significant discrepancies in scores. Recent market data shows instances where a single company received a local ESG rating of **65** while maintaining global scores as high as **78**, highlighting the urgent need for standardized benchmarks. Strategic Alignment with Global Trends SEBI’s initiative coincides with major international shifts. In the European Union, new ESG Rating Regulations are set for application by **July 2026**, pushing for tighter supervision of providers. SEBI intends to evaluate these international developments to ensure the Indian framework remains competitive for foreign capital while respecting the unique context of the domestic market. Current mandates in India already require the top **1,000** listed entities to undertake reasonable assurance of their Business Responsibility and Sustainability Reporting (BRSR) Core. The working group will explore how ERPs can better utilize this assured data to provide more "Core ESG Ratings," which are seen as more reliable by the investor community. Market Impact and Outlook The global ESG investing market is projected to reach **$45.61 trillion** in 2026. As institutional investors now account for nearly **47.28%** of this segment, the demand for precise data is at an all-time high. In India, ESG integration remains the largest revenue-generating segment within sustainable finance, while Green Bonds are emerging as the fastest-growing instrument. The working group is expected to submit a report detailing recommended policy changes and regulatory tweaks. These recommendations will likely focus on internal governance at rating agencies, disclosure of scoring methodologies, and the management of potential conflicts of interest. This regulatory evolution is viewed as a critical step in maintaining investor confidence as India’s ESG-linked assets continue their double-digit growth trajectory through 2030.

Large-Cap Stocks With Decreased Domestic Institutional Investor Ownership in Q3

Market Brief: Institutional Shifts in NSE Large-Caps Domestic Institutional Investors (DIIs) significantly adjusted their positions in December 2025, reducing stakes in nine high-profile NSE large-cap stocks. This move, characterized by profit-booking and tactical rebalancing, affected key industry leaders including Bharat Petroleum (BPCL), Tata Motors, and the State Bank of India (SBI). Energy and Automotive Adjustments Bharat Petroleum (BPCL) witnessed a notable reduction in DII holdings, which dropped to **19.56%** by the end of December 2025 from **21.30%** in the previous quarter. Despite this institutional trimming, BPCL remains a favored value pick, trading near **₹380.60** as of February 18, 2026. The stock has maintained a strong one-year return of approximately **48%**, supported by a robust net profit of **₹7,188 crore** reported in the latest quarter. Tata Motors also saw a shift in its investor base. DII exposure in the automotive giant softened as the market navigated a transition in its passenger vehicle segment. By mid-February 2026, Tata Motors' share price consolidated around the **₹493** mark. While institutional activity showed signs of cooling, the stock remains a central focus for analysts, holding a **52-week high of ₹500**. Banking Sector Sentiment The State Bank of India (SBI) was another major target for institutional trimming during the December 2025 period. Domestic funds appeared to lock in gains following a period of sustained outperformance in the public sector banking space. Currently, SBI is trading at approximately **₹1,220**, reflecting a stable recovery trend despite the earlier reduction in domestic stakes. Broader Market Context The overall market sentiment in early 2026 has been defined by a "tug of war" between institutional players. While DIIs lightened their large-cap loads in late 2025, they have returned as net buyers in February 2026, injecting **₹1,667 crore** in single sessions to absorb Foreign Institutional Investor (FII) selling. This tactical rebalancing suggests that while DIIs reduced exposure to specific large-cap names in December, their broader commitment to Indian equities remains intact, supported by consistent SIP inflows. The Nifty 50 has recently tested the **25,600** level, with volatility remaining moderate as investors eye sector rotation into mid-caps and specialty chemicals.

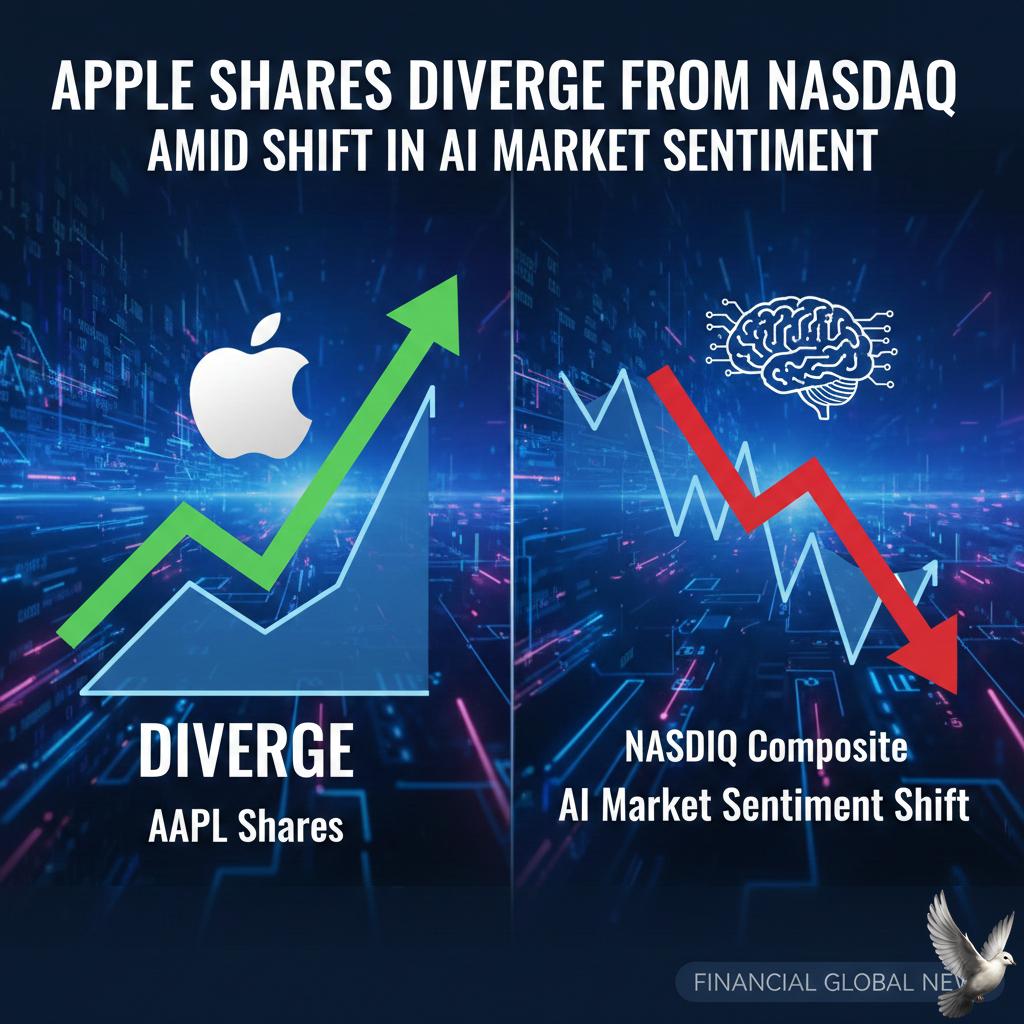

Apple Shares Diverge From Nasdaq Amid Shift in AI Market Sentiment

Apple Inc. is currently demonstrating a significant departure from broader technology sector movements, as the stock’s correlation with the Nasdaq 100 Index has plunged to a 20-year low. This decoupling highlights Apple’s unique position as a defensive play within a market increasingly defined by volatile artificial intelligence spending. As of February 18, 2026, Apple shares are trading near $265.21, reflecting a market capitalization of approximately $3.9 trillion. While the stock has faced recent pressure, dropping nearly 6% year-to-date and 8% in the past week due to regulatory scrutiny and rumors of AI feature delays, it remains a pillar of relative stability compared to peers heavily exposed to the AI "arms race." Recent fiscal Q1 2026 earnings results underscore this resilience. The company reported record-breaking quarterly revenue of $143.8 billion, a 16% increase year-over-year. This growth was fueled primarily by robust iPhone sales, which generated $85.3 billion in revenue—a 23% jump from the previous year. Services also reached new heights, contributing $30.01 billion to the top line. Apple’s primary advantage lies in its restrained capital expenditure. Unlike competitors spending tens of billions on data centers and specialized chips, Apple is leveraging partnerships, such as a collaboration with Alphabet to power its upcoming Siri 2.0 with Gemini models. This strategy preserves a massive cash pile of over $130 billion, offering a safety net during market uncertainty. Growth in emerging markets continues to provide a strong offset to maturity in Western regions. India has emerged as a critical driver, setting all-time revenue records for iPhones and Macs. Analysts estimate that 15.1 million iPhones were shipped to India in 2025 alone, a trend expected to accelerate as Apple expands its retail presence in the country. The outlook for the remainder of 2026 remains focused on a hardware supercycle. Investors are anticipating the fall launch of the iPhone 18 and a refreshed lineup of M5-powered MacBooks. Revenue for the current quarter is projected to rise between 13% and 16%, well above previous consensus estimates. Despite a valuation of roughly 30 times forward earnings—higher than many tech peers—Apple’s 40-day correlation to the Nasdaq 100 has dropped to 0.21. This confirms its status as an "AI-insulated" asset, attracting investors who seek shelter from the high-stakes spending cycles of the software and semiconductor industries.