Bullish News

Collection

Top-Performing Indian Small-Cap Fund Increases Allocation to Internet Value Stocks

Market Brief: Bandhan Small Cap Fund Strategy The **Bandhan Small Cap Fund** continues to pursue a contrarian investment path, focusing on "beaten-down" sectors despite a cooling phase in the broader small-cap universe. As of **February 18, 2026**, the fund’s Net Asset Value (NAV) stands at **46.12**, managing a significant asset base of **19,267 Crores**. While the Nifty Smallcap index has faced a **3%** decline year-to-date in **2026**, the fund remains a category leader with a **3-year CAGR of 30.18%** and a **5-year CAGR of 23.2%**. High-Conviction Tech Recovery The fund has aggressively increased its exposure to the Indian internet space, specifically targeting firms that faced heavy regulatory and valuation corrections in previous cycles. **Paytm (One 97 Communications)** and **Info Edge** are core components of this "value-hunting" strategy. Analysts note that approximately **61%** of market experts currently maintain a **Buy** rating on Paytm as it stabilizes. Info Edge, a leader in digital classifieds, remains a top holding as the fund manager bets on a long-term turnaround in recruitment and real estate tech. Sectoral Shifts: Real Estate & Textiles Portfolio allocation has shifted toward labor-intensive and infrastructure-linked sectors. The fund is currently **overweight on Financial Services (21.05%)** and **Real Estate (9.06%)**. * **Real Estate:** The **2026-27 Union Budget** increased infrastructure outlay to **12.2 lakh crore**, directly benefiting holdings like **Sobha Ltd** (3.64% of the portfolio) and **Prestige Estates**. * **Textiles:** The fund has been building positions in **Arvind Ltd** and **Nitin Spinners**. This sector is supported by a new **10,000 crore SME Growth Fund** aimed at scaling manufacturing exports. Resilience Amid Volatility The small-cap segment is currently in a "reset phase," with nearly **50% of stocks** in this category trading roughly **40% below** their all-time highs. This widespread correction has created an entry point for the fund’s "Growth at Reasonable Price" (GARP) framework. Despite a short-term dip of **1.89%** over the last year, the fund has maintained a **Sharpe ratio greater than 1**, indicating superior risk-adjusted returns compared to its peers. The current strategy prioritizes businesses with healthy cash flows and high scalability, avoiding overleveraged firms. Key Indicators * **Latest NAV (Regular):** 46.12 * **Fund AUM:** 19,267 Crores * **Expense Ratio:** 1.62% * **Top Sector:** Financial Services (21.05%) * **3-Year Annualized Return:** 30.18% The manager remains benchmark-agnostic, trimming holdings in metals and commodities while shifting capital into renewables and consumer discretionary themes to capture the next growth cycle.

Indian Benchmarks Trade Higher Led by Gains in IT Stocks

Market Brief: Indian Equities Indian equity benchmarks, Nifty and Sensex, opened higher on **Thursday, February 19, 2026**, marking their fourth consecutive session of gains. This winning streak follows a period of consolidation, with the indices now testing critical psychological resistance levels. Index Performance The **BSE Sensex** rose over **146 points** at the opening bell, trading near the **83,880** level. Simultaneously, the **NSE Nifty 50** gained momentum to trade above **25,839**, sustaining its position above key moving averages. Sectoral Movers Information Technology (IT) and Metals emerged as the primary engines of growth. The **Nifty IT index** rallied **1.5%**, led by gains in heavyweights like **HCLTech**, **Infosys**, and **Tech Mahindra**. The **Metal sector** followed with a **0.5%** rise, supported by **Tata Steel** and **Hindustan Copper**. Conversely, the **Private Bank index** saw a marginal dip of **0.2%**, acting as a slight drag on the broader market surge. Key Market Data Institutional activity remains a pivotal driver for the current rally. **Foreign Portfolio Investors (FPIs)** were net buyers on the previous session, purchasing shares worth **₹1,154 crore**, while **Domestic Institutional Investors (DIIs)** added **₹440 crore** to the tally. The volatility gauge, **India VIX**, has cooled to approximately **12.22**, reflecting a reduction in market nervousness and a shift toward a "buy-on-dip" sentiment among traders. Technical Outlook Market analysts identify **25,700** as a robust support zone for the Nifty. On the upside, **26,000** remains the immediate hurdle. A decisive breach above this resistance could potentially trigger a fresh acceleration toward the **26,300** mark. Global cues provided a supportive backdrop, with **GIFT Nifty** indicating a positive start and major Asian indices, including Japan's **Nikkei**, trading significantly higher. Investors are also monitoring domestic inflation forecasts, with current estimates placing fiscal **2026 CPI at 2.5%**.

Aurobindo Pharma Leads Top 4 F&O Stocks in Open Interest Growth

Energy Market Brief | February 19, 2026 The global energy landscape is currently defined by a tug-of-war between heightened geopolitical risk and a persistent underlying supply surplus. While immediate supply shocks have provided technical support for prices, long-term indicators suggest a cooling trend as production capacity remains robust across both OPEC+ and non-OPEC+ nations. Crude Oil Performance Benchmark prices have experienced significant volatility throughout early **2026**. Brent crude is currently trading around **$70** per barrel, while West Texas Intermediate (WTI) is positioned near **$63**. Recent price action was driven by a **$10** per barrel surge in January, sparked by escalating tensions in the Persian Gulf and severe winter weather that disrupted North American operations. However, prices have retreated from those highs as markets digest a projected global surplus of approximately **3.2 million** barrels per day for the remainder of the year. Supply and Production Dynamics World oil supply is forecast to rise by **2.4 million** barrels per day in **2026**, reaching a total of **108.6 million** barrels per day. This growth is roughly split between OPEC+ and non-OPEC+ producers. * **OPEC+ Strategy:** Member nations recently reaffirmed a pause in production increments through March **2026** to manage seasonal demand shifts. The group maintains a significant effective spare capacity of over **4 million** barrels per day. * **Non-OPEC Growth:** Increased output from the "Americas quintet"—the United States, Canada, Brazil, Guyana, and Argentina—continues to provide a buffer against potential disruptions. * **Inventory Builds:** Global inventories rose by **37 million** barrels in December, with Chinese crude stocks and "oil on water" accounting for a substantial portion of the increase. Natural Gas and LNG Expansion Natural gas is emerging as a central pillar of energy infrastructure growth this year. The industry is witnessing the most active period for gas-fired generation development in over a decade. North American LNG export capacity is entering a major growth phase, on track to climb toward **30 billion** cubic feet per day by **2027**. This expansion is solidifying the U.S. Gulf Coast as the global anchor of gas supply, reshuffling global trade flows as European and Asian demand remains sustained. Key Risks and Indicators Geopolitical uncertainty remains the primary "war premium" driver. Analysts estimate that a total removal of Iranian crude from the market—roughly **3.3 million** barrels per day—could push Brent toward **$91** by late **2026**. Economic indicators in the U.S. show unexpected resilience, with capital goods orders rising **0.6%** in December and housing starts hitting a five-month high. This domestic strength is supporting energy demand even as central banks shift toward more accommodative monetary policies. Outlook for 2026 The consensus forecast points to a gradual decline in oil prices as production continues to outpace demand. The EIA projects Brent crude will average **$58** per barrel across **2026**. Investment is increasingly focused on operational efficiency and "behind-the-meter" projects. Energy companies are prioritizing capital discipline and shareholder returns, with large-cap firms expected to return up to **78%** of free cash flow to investors this year.

USD/JPY Volatility and Fed Rate Outlook Drive Currency Intervention Speculation

**MARKET BRIEF: DOLLAR-YEN VOLATILITY AND INTERVENTION SPECULATION** The US Federal Reserve recently confirmed it conducted rare market inquiries into the dollar-yen exchange rate. This move, known as a "rate check," was executed at the direct request of the US Treasury Department. Such actions are highly uncommon and typically interpreted by market participants as a precursor to physical currency intervention. The New York Fed’s trading desk sought these quotes from dealers in late January 2026, sparking immediate speculation of coordinated action between Washington and Tokyo to stabilize the yen. **Current Exchange Rate Dynamics** As of February 19, 2026, the USD/JPY pair is trading near **155.18**. This follows a period of intense volatility where the pair swung between **153.00** and **159.00** over the last thirty days. The yen recorded a massive surge last week, gaining nearly **3%** against the dollar. This was the currency’s strongest weekly performance in approximately **15** months. The appreciation was fueled by the "rate check" news and a decisive election victory for the current Japanese administration, which investors believe provides the political mandate for further monetary tightening. **Policy Divergence and Economic Data** Despite the brief yen rally, the currency remains under pressure due to the widening interest rate gap between the US and Japan. The Federal Reserve's January meeting minutes revealed a hawkish stance, with policymakers emphasizing that interest rate cuts are not imminent while inflation remains above target. In Japan, the economic backdrop is mixed. Recent data showed a massive **16.8%** year-on-year surge in Japanese exports for January 2026. However, preliminary GDP figures indicated the economy grew at a meager **0.1%** in the final quarter of last year, missing the **0.4%** market consensus. **Intervention Outlook** US Treasury Secretary Scott Bessent has publicly pushed back against claims of active market intervention. However, the Federal Reserve’s confirmation that it acted as a fiscal agent for the Treasury has kept traders on high alert. Market analysts note that coordinated intervention between the US and Japan has not occurred in roughly **15** years. While no large-scale dollar sales have been confirmed, the constructive ambiguity of the "rate check" has effectively placed a psychological floor under the yen near the **159.00** level. Investors are now focused on upcoming US PCE inflation figures and the Bank of Japan’s March meeting. Markets currently assign a **20%** probability to a Japanese rate hike in March, though many economists expect the central bank to wait until mid-year. The yen's path forward remains tethered to US Treasury yields. The US 10-year yield is hovering near **4.08%**, while the Japanese 10-year yield remains stable above **2.21%**. This yield differential continues to be the primary driver for USD/JPY price action in the near term.

Dr. Reddy’s Acquires HRT Drug Trademarks in India for $32 Million

Dr. Reddy’s Laboratories (DRREDDY) has moved into the spotlight following its strategic entry into the Indian Hormone Replacement Therapy (HRT) market. On February 18, 2026, the pharmaceutical major finalized a definitive agreement to acquire the India trademarks for specialty brands Progynova and Cyclo-Progynova from the UK-based Mercury Pharma Group for USD 32.15 million. The deal highlights Dr. Reddy's aggressive expansion within the gynecology segment. Progynova, an estradiol valerate therapy, is currently ranked as the number one brand in the Indian estradiol market, recording annual sales of approximately INR 100 crore as of December 2025. Cyclo-Progynova complements this by offering a combined therapy for estrogen deficiency symptoms. This acquisition arrives as the Indian pharmaceutical market (IPM) shows resilient growth. The sector kicked off 2026 with a 10.2% value increase in January, driven largely by chronic and specialty therapies. While the broader market is projected to grow between 7.8% and 8.1% throughout 2026, lifestyle-driven segments such as hormonal treatments and oncology are expected to outpace general growth. Dr. Reddy's recent financial performance underscores this growth potential despite global headwinds. For the quarter ending December 2025, the company reported consolidated revenue of INR 8,727 crore, a 4.4% year-on-year increase. While higher R&D investments and operating costs led to a 15.3% dip in net profit to INR 1,190 crore, the India business remained a standout performer, growing by 19% to reach INR 1,603 crore. Market reaction to the stock has been mixed but generally positive regarding long-term domestic strategy. As of February 19, 2026, Dr. Reddy's shares are trading near INR 1,276.60, with various brokerages maintaining "Buy" ratings and price targets ranging up to INR 1,737. The stock has delivered a return of over 10% in the past month alone. Investors are closely monitoring the company's shift toward high-value specialty products. With the HRT market in India gaining momentum due to increased awareness and an aging population, the integration of these newly acquired brands is expected to provide a steady revenue stream and solidify the firm's position as a leader in women's healthcare.

Cochin Shipyard Secures $360 Million LNG Vessel Contract from CMA CGM Group

Cochin Shipyard has reached a major milestone in the global maritime market, securing a landmark contract worth approximately $360 million (₹3,267 crore) with France-based logistics giant CMA CGM Group. This agreement covers the construction of six 1,700 TEU container vessels powered by Liquefied Natural Gas (LNG), signaling a strategic shift for the French firm, which has historically relied on Chinese and South Korean yards. The deal effectively pushes Cochin Shipyard’s unexecuted order book to a record ₹23,000 crore, providing immense revenue visibility for the next several years. Engineering and design will be handled in collaboration with Korea Maritime Consultants (KOMAC). The first vessel is scheduled for delivery by February 2029, with a steady rollout of two vessels per year thereafter. Market sentiment remains highly reactive to these developments. On February 17, 2026, the company’s stock surged over 7% to an intraday high of ₹1,575 following news of this contract and the company being declared the lowest bidder (L1) for a separate ₹5,000 crore Indian Navy project. As of mid-February 2026, the stock is trading near the ₹1,470–₹1,500 range, supported by a market capitalization of over ₹40,000 crore. Financial performance for the quarter ending December 2025 showed a mix of scale and pressure. Revenue from operations grew by 17.7% year-on-year to reach ₹1,350 crore. However, consolidated net profit for the quarter dipped by 18.3% to ₹144.67 crore, primarily due to higher input costs and operational expenses. Despite this margin compression, the board declared a second interim dividend of ₹3.50 per share, demonstrating confidence in its cash flow. Beyond traditional shipbuilding, the company is aggressively pivoting toward green technology and global expansion. It recently approved a 23% stake acquisition in the Netherlands-based ship design firm Conoship International to penetrate the European market. Additionally, a new joint venture with HBL Engineering has been established to develop indigenous electric mobility and energy storage solutions for the marine sector. This expansion into sustainable, LNG-powered vessels aligns with India’s Maritime Vision 2047. By successfully competing for high-value international commercial orders alongside its massive defense backlog, Cochin Shipyard is positioning itself as a central player in the global transition toward cleaner maritime energy and self-reliant manufacturing.

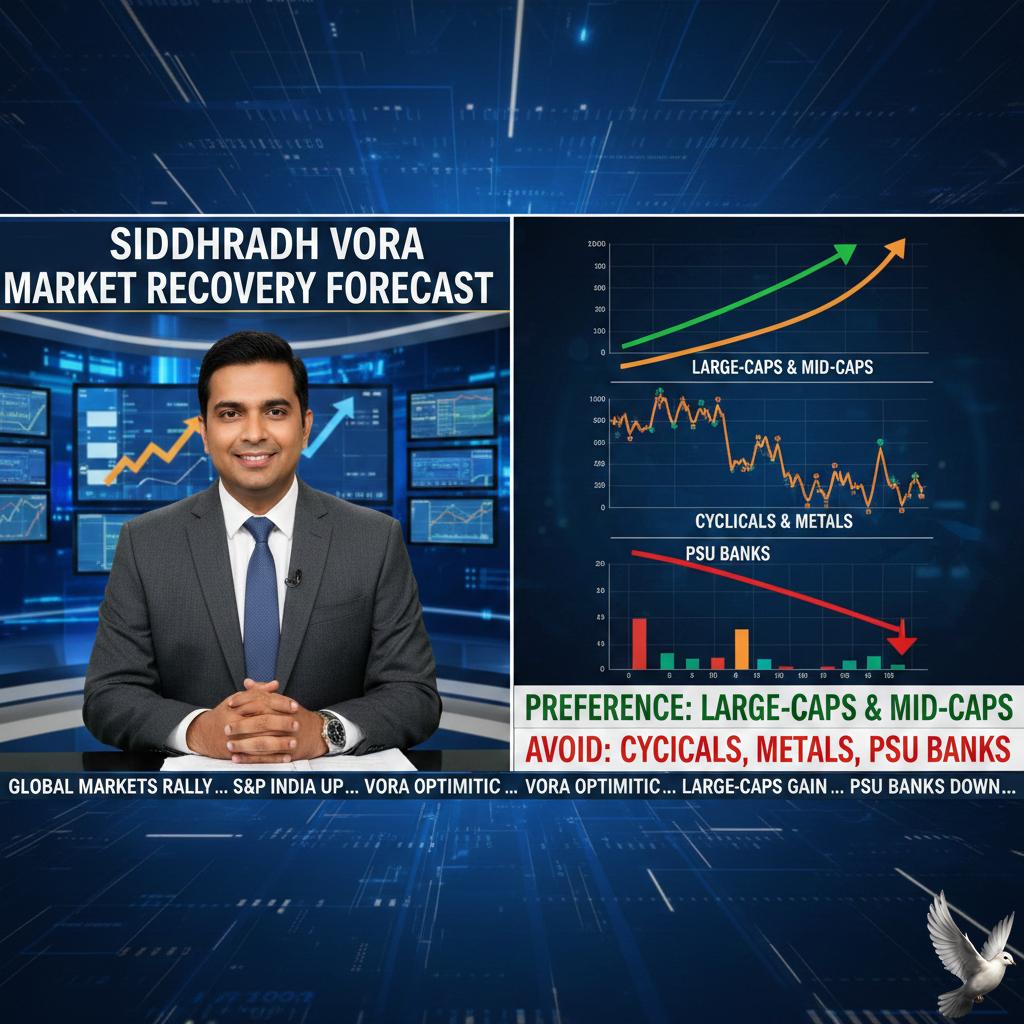

Siddharth Vora Forecasts Market Recovery with Preference for Large-caps and Mid-caps Over Cyclicals, Metals, and PSU Banks

Indian equity markets are entering a constructive phase in February 2026, characterized by a transition from global underperformance to a potential period of mean reversion. Benchmark indices have shown resilience, with the Nifty 50 sustaining levels around **25,819** and the Sensex trading near **83,734**. Macroeconomic stability serves as a foundational pillar for this outlook. India’s retail inflation for January 2026 moderated to **2.75%** under the newly implemented CPI series. This cooling of price pressures, coupled with a Real GDP growth estimate of **8.2%**, reinforces India’s position as a leading growth economy. The current market environment is increasingly viewed as a contrarian opportunity. Analysts note that India’s relative underperformance against global peers and precious metals has reached a multi-decadal low, hitting the bottom **10th percentile**. Historically, such extremes often precede a cycle of outperformance. Sectoral leadership is shifting toward cyclicals and value-oriented themes. PSU banks have emerged as significant performers, with the State Bank of India recording a YTD return of **16.5%** as of mid-February. Improved asset quality and a **26%** increase in net profits across the public banking sector have bolstered investor confidence. Metals and energy remain key overweight areas. The Nifty Metal index continues to benefit from supply tightness and rising global commodity prices, with Hindustan Copper delivering a YTD return of **15.8%**. Upstream energy companies like Oil India have gained **15.3%** in the first two months of 2026, supported by geopolitical factors and firm crude prices. Institutional activity shows a notable shift in dynamics. While foreign institutional investors (FIIs) have been net sellers in early 2026, domestic institutional investors (DIIs) have acted as a critical cushion, infusing over **₹9,775 crore** in February alone. This domestic liquidity has prevented deep corrections despite global volatility. Largecaps and midcaps are currently preferred over speculative segments. Earnings revisions are reportedly bottoming out after several weak quarters, signaling a potential recovery in corporate profitability for the fiscal year ahead. Technical indicators support this bullish bias, with the Nifty 50 maintaining its position above major moving averages. Market participants are watching the **26,000** level as a psychological hurdle that could trigger the next leg of the rally. Recent trade agreements, including the India-US trade pact and the EU Free Trade Agreement, are viewed as long-term structural wins. These developments, alongside a stabilizing rupee trading near **90.68** against the dollar, provide a favorable backdrop for Indian cyclicals to lead the market recovery.

Bharat Forge Signs MoU for Automotive, Defence, and Data Centre Collaboration

Bharat Forge has entered into a strategic Memorandum of Understanding with VVDN Technologies to pioneer next-generation solutions across the automotive, defense, and data center sectors. This partnership combines Bharat Forge’s global leadership in precision manufacturing with VVDN’s expertise in electronics design and AI-driven system integration. The collaboration comes as Bharat Forge reports a strong financial trajectory. In the quarter ended December 31, 2025, the company saw its consolidated revenue jump 25% year-on-year to 4,342.93 crore. Net profit for the same period climbed 28.2% to reach 272.80 crore, demonstrating robust operational resilience despite global supply chain fluctuations. The defense segment remains a critical growth engine. Bharat Forge’s defense order book has expanded to a record 11,130 crore, bolstered by a significant recent contract with the Ministry of Defence for the supply of 250,000 carbines. The new alliance with VVDN is expected to further enhance these capabilities by integrating advanced AI and autonomous systems into military platforms. In the automotive space, the partners are targeting the rise of software-defined vehicles. Recent market data indicates that nearly 95% of Indian consumers are now willing to pay for advanced digital vehicle features. The collaboration focuses on developing AI server platforms and high-compute electronics to meet this surging demand for intelligent mobility. The market has reacted positively to these developments. As of February 19, 2026, Bharat Forge’s stock is trading near its 52-week high of 1,784.20, with a current price of approximately 1,771.85. The company’s market capitalization has surged to approximately 84,712 crore, reflecting investor confidence in its diversification strategy. To reward shareholders, the board has declared an interim dividend of 2 per equity share. The partnership with VVDN is strategically timed to capitalize on the government's push for domestic electronics manufacturing and the rapid adoption of generative AI in industrial applications. By merging heavy engineering with high-tech electronics, the two entities aim to create a scalable ecosystem for sustainable compute infrastructure. This synergy is designed to shorten development cycles and deliver future-ready products to a global client base increasingly focused on autonomous and digital-first technologies.

L&T Partners with Nvidia to Build India’s Largest Gigawatt-Scale AI Factory

Larsen & Toubro has officially entered a strategic venture with Nvidia to develop India’s first sovereign, gigawatt-scale AI factory. Announced during the India AI Impact Summit in February 2026, this collaboration integrates L&T’s heavy engineering and data center expertise with Nvidia’s full-stack AI computing platform. The project is a cornerstone of the national IndiaAI Mission, which recently secured over 10,300 crore INR in government backing to democratize high-end compute access. The infrastructure footprint is massive. L&T is scaling its Chennai campus to a 30 MW GPU cluster within a 300-acre site, while simultaneously executing a new 40 MW data center in Mumbai. These facilities are designed to be "sovereign by design," ensuring that critical data and AI workloads for Indian enterprises remain within national borders while maintaining global interoperability. Market sentiment reflects the scale of this ambition. As of February 19, 2026, L&T’s stock is trading near record highs at 4,326 INR, reflecting a 34% gain over the past year. The company’s market capitalization has crossed 5.95 lakh crore INR, buoyed by a consolidated order book that has reached an unprecedented 7.33 lakh crore INR. The partnership is timed to meet a surge in domestic demand. India’s total AI investment is projected to scale significantly from its current 1.2 billion USD base, with the government aiming to deploy over 38,000 GPUs to support startups and researchers. By providing "production-grade" AI capacity, L&T and Nvidia are shifting the market focus from experimental AI pilots to large-scale industrial deployment. Beyond infrastructure, the venture enables L&T group companies—including L&T Technology Services and LTIMindtree—to deploy live AI agents on a sovereign cloud. These agents will power "Lights-Out" factories and autonomous industrial operations, leveraging Nvidia’s Omniverse libraries to create digital twins for manufacturing, energy, and healthcare sectors. This move positions India as a global hub for digital infrastructure. With the Indian IT sector projected to reach 350 billion USD this year, the L&T-Nvidia factory provides the foundational compute needed to transform India from a consumer of AI into a global producer of intelligence-led services.

MCX and NSE End Additional Margins on Gold and Silver Futures

The Multi Commodity Exchange (MCX) and National Stock Exchange (NSE) have officially withdrawn additional margins on gold and silver futures, effective today, February 19, 2026. This tactical reversal marks the end of heightened risk controls introduced earlier this month to combat extreme price swings. The clearing corporations have scrapped the 3% additional margin on all gold futures variants and the 7% extra levy on silver contracts. This rollback significantly lowers capital requirements for traders, with the primary goal of boosting market liquidity and improving capital efficiency for leveraged participants. This policy shift follows a substantial correction in bullion prices from their historic peaks. Gold has retreated nearly 20% from its record high of 1.93 lakh per 10 grams, currently trading near 1.56 lakh in domestic markets. International spot gold is hovering around $4,961 an ounce, down from levels exceeding $5,100 seen earlier this year. Silver has experienced a much sharper downturn. After a historic single-day crash of 27% on January 31, the metal has fallen approximately 42% from its peak of 4.20 lakh per kilogram. Domestic silver futures are now positioned around 2.43 lakh per kg, while international prices have stabilized near $76 per ounce, down from a high of $120. The removal of these curbs is expected to encourage fresh positions and higher intraday activity. While volatility remains present due to geopolitical tensions and U.S. economic indicators, the decline in daily price ranges suggests a relative stabilization compared to the chaotic trading environment of late January. Market participants are currently monitoring the U.S. Dollar Index and Treasury yields, which continue to influence precious metals. Despite the recent price cooling, global demand remains supported by central bank purchases and persistent safe-haven interest amid ongoing trade and tariff uncertainties.

5 Nifty500 Stocks, Including Godfrey Phillips and Netweb Tech, Exhibit Bullish RSI Upswing

Market Brief: Global Equity and Commodity Update Global markets are showing resilience as of **February 19, 2026**, supported by strong technology investments and a stabilization in global growth projections. The International Monetary Fund recently adjusted its **2026 global growth forecast to 3.3%**, citing private sector adaptability and fiscal support as primary drivers against ongoing trade policy shifts. U.S. Equity Performance U.S. indices reached fresh milestones in mid-February. The **S&P 500** is currently trading near **6,881**, reflecting a daily gain of **0.56%**. The **Nasdaq 100** has reclaimed the **25,000** level, up **0.78%** as large-cap technology stocks continue to lead the market rebound. The **Dow Jones Industrial Average** stands at **49,662**, a gain of **0.26%**. While the "Magnificent Seven" stocks have provided a significant bounce, analysts are closely monitoring potential resistance at the **50,272** mark. Market volatility remains present, with the **VIX** cooling by **3.3%** to settle at **19.62**. Commodities and Energy Precious metals are experiencing significant price swings. **Gold** prices have faced recent pressure, falling below the **$4,900** per ounce mark to trade near **$4,861**. Despite this short-term volatility, some long-term forecasts remain bullish, with projections suggesting a potential rise toward **$5,600** by year-end due to sustained macroeconomic demand. **Silver** experienced a sharper correction, with prices dropping roughly **5.6%** to settle near **$73.45** per ounce. In the energy sector, **Brent crude** remains range-bound, currently trading near **$62** per barrel. Geopolitical tensions in the Middle East provide a floor for prices, while rising supply from North America prevents a significant breakout. **Natural gas** remains under bearish pressure, with futures hovering around the **$2.75** mark. Central Bank Policy The **Federal Reserve** and other major central banks are maintaining a "wait and watch" approach. Recent FOMC minutes suggest a hawkish tilt as officials look for more definitive signs that inflation is returning to the **2%** target. In India, the **Reserve Bank of India** kept the repo rate unchanged at **5.25%** during its February meeting. The bank maintains a neutral stance, noting that while inflation is currently benign, global uncertainties warrant a cautious approach to further rate cuts. Regional Highlights Asian markets show a divergent trend. **South Korea** reported a surge in semiconductor exports, while **China’s** growth outlook remains at approximately **4.6%** for 2026. Trade patterns are shifting, with U.S. imports from Southeast Asia—particularly Thailand and Vietnam—increasing as companies diversify supply chains away from traditional hubs.

Five stocks including Infosys and Maruti for potential long-term returns in 2026.

Market benchmarks **Nifty 50** and **BSE Sensex** extended their recovery into a third consecutive session on **February 18, 2026**, as positive sentiment returned to the banking and metal sectors. The **Nifty 50** closed up **0.37%** at **25,819.35**, while the **Sensex** rose **283.29 points** to settle at **83,734.25**. Investor confidence was bolstered by state-owned lenders, with the **PSU Bank index** surging **1.3%**. Metal stocks followed suit, gaining **1.33%** amid reports of potential global tariff easing. In contrast, the **IT sector** faced selling pressure, with the **Nifty IT index** declining **1.2%**. Top Brokerage Recommendations **Motilal Oswal** has highlighted **Delhivery** as a high-conviction pick with a target of **420** to **570**, representing a **36% upside**. The firm also maintains a positive outlook on **Britannia Industries**, targeting **7,150** (a **20% upside**) following strong margin expansion in the third quarter. **Anand Rathi** technical research suggests immediate buys on **Bharti Airtel** at a target of **2,100** and **Coal India** with a target of **470**. Analysts note that **Bharti Airtel** is finding strong support at its short-term mean, while **Coal India** is entering a reversal phase after a healthy correction. **Nuvama** and **Citi** remain constructive on large-cap leaders. **Citi** has raised its target price on **R R Kabel** and maintained a buy on **Hyundai Motor**, while **Nuvama** recently upgraded **Prestige Estates** and **Brigade Enterprises** to capture gains in the real estate cycle. Key Market Data Points * **Rupee Status**: The Indian rupee appreciated by **6 paise** to close at **90.66** against the US dollar. * **Breadth**: Market breadth favored gainers, with **2,224 stocks advancing** against **1,903 declines** on the BSE. * **Foreign Inflow**: Renewed confidence in India's **7.4% GDP growth projection** for **FY26** has seen a revival in FII net buying. * **Corporate Moves**: **SBI Funds Management** has announced a landmark **$1.5 billion IPO** slated for March. Sector and Economic Outlook Industrial activity is gaining momentum with a projected growth of **6.2%** for **FY26**. The services sector continues to lead the economy, now contributing **60%** of Gross Value Added. Recent budget provisions for **2026** have introduced a **Rs 40,000 crore** outlay for electronics manufacturing, benefiting semiconductor and tech hardware players. However, volatility remains elevated as investors track the **U.S. Federal Reserve** minutes for interest rate guidance. Financial experts suggest a **buy-on-dips** strategy, focusing on blue-chip names like **ICICI Bank**, **Reliance**, and **Hindustan Aeronautics**, which have shown resilient **5-year CAGR** performance. Analysts expect **Nifty** to face resistance at **26,000**, with strong support established in the **25,400–25,500** range.

7 Stocks Cross Above 200-Day Moving Average

Equity markets are currently navigating a critical technical junction as of February 19, 2026. The 200-day Simple Moving Average (SMA) remains the primary barometer for long-term sentiment. In the U.S., the S&P 500 continues to trade above this vital level, currently hovering near **6,843**, maintaining its broad uptrend despite a recent cooling of momentum. The market breadth reveals a growing divergence. While the headline index remains bullish, only **66%** of S&P 500 constituents are currently trading above their 200-day SMA. The technology sector is under notable pressure, with **57%** of its stocks now languishing below their long-term averages due to concerns over high valuations and shifting demand. Indian benchmarks show similar resilience. The Nifty 50 settled at **25,819**, holding firm above its 200-day support near **25,500**. Technical scans identified seven major stocks, including Yes Bank and PVR Inox, making fresh breakouts above their 200-day DMAs this week, signaling a potential shift from sideways consolidation to active uptrends. Economic indicators are providing a mixed backdrop for these technical levels. U.S. Consumer Price Index (CPI) data shows headline inflation at **2.4%**, while core inflation remains stickier at **3.6%**. Investors are closely monitoring the Federal Reserve's stance, as interest rate expectations directly impact the ability of growth stocks to stay above their moving averages. Commodities are undergoing their own technical tests. Gold has corrected to approximately **$5,047** per ounce, yet it remains structurally sound within a long-term bull market as long as it holds above its 200-day floor. Silver has faced steeper volatility, retreating toward **$77.01** but staying within its medium-term upward channel. Corporate earnings are the current catalyst for price action. As heavyweights report fourth-quarter results, the ability of individual stocks to reclaim or defend the 200-day SMA will determine whether the current market phase is a healthy consolidation or the start of a deeper trend reversal. Volatility, measured by the VIX at **13.33**, suggests that while fear is not at extreme levels, the market is sensitive to technical breaches. Analysts emphasize that the 200-day SMA is a lagging indicator; therefore, price action near these levels often attracts significant institutional liquidity and serves as a "line in the sand" for trend followers.

Marushika Technology IPO: Shares to List Today Following NSE SME Debut

Marushika Technology marks its entry onto the NSE SME platform this February 19, 2026. The company’s debut comes after a successful public offer that raised 26.97 crore. Investor demand was notably robust, with the issue being oversubscribed 17.94 times. The retail portion saw significant interest at 16.51 times, while non-institutional investors led the charge with 41 times subscription. The shares were issued at a price of 117 per share, the upper end of the established price band. Early grey market activity indicates a steady sentiment, with premiums hovering around 2%. This suggests a potential listing price near 119 to 120 per share. The company’s financial health supports this entry, reporting a total income of 85.63 crore and a profit after tax of 6.29 crore for the 2025 fiscal year. Operating in the high-growth IT and telecom infrastructure sector, Marushika manages complex projects across data centers, cybersecurity, and surveillance. A key differentiator is its involvement in the defense segment, where it provides specialized repair, refurbishment, and reverse engineering solutions. The firm serves a high-profile client base including Bharat Electronics Limited and the National Security Guard. The capital raised from the 23.05 lakh fresh shares will be strategically deployed to strengthen the balance sheet. Approximately 5 crore is earmarked for the repayment of existing borrowings, while 14.68 crore will fund essential working capital. This move is designed to support an order book that stood at 28.35 crore as of late 2025. The listing coincides with a broader push in India’s digital infrastructure. National trends for 2026 highlight a shift toward capital efficiency and enterprise monetization in telecom. With the domestic telecom sector transitioning toward 5G value-added services and satellite connectivity, infrastructure providers are positioned at the center of this transformation. Market conditions remain supportive as the Nifty maintains levels above 25,800. The SME sector continues to attract liquidity, reflected by the broad-based buying seen in recent sessions. Marushika enters the secondary market with a post-issue promoter holding of 58.19%, aiming to leverage its track record of over 150 completed projects to capture emerging opportunities in sovereign digital networks and defense technology.

Gold Prices Decline Amid Strengthening Dollar and Upcoming Inflation Data

Market Brief: Gold Price Action and Outlook **February 19, 2026** Gold prices are experiencing a marginal retreat this Thursday, with spot prices hovering near the **$4,980** level. This follows a volatile Wednesday session where the metal briefly breached the psychological **$5,000** resistance mark, reaching a peak of **$5,003.85** before easing. The current dip is primarily driven by a strengthening U.S. Dollar and a cautious stance from investors ahead of critical economic triggers. Markets are closely analyzing the recently released Federal Reserve meeting minutes, which suggested a more patient approach to interest rate cuts than some had anticipated. Key Price Levels and Data In the global spot market, gold remains consolidated just below the **$5,000** per ounce threshold. Silver has shown relative strength, rebounding to approximately **$76** per ounce during Asian trading hours. Domestic markets in India reflect this global cooling. 24K gold is currently trading near **₹15,419** per gram, while 22K gold stands at **₹14,134**. These rates represent a slight correction from earlier February highs, which saw prices peak near **₹16,058** at the start of the month. Factors Influencing the Market Several macroeconomic and geopolitical variables are currently dictating price direction: * **Inflation Metrics:** Market participants are focusing on the upcoming Personal Consumption Expenditures (PCE) report. Current data shows annual inflation at **2.4%**, with core inflation holding at **2.5%**. * **Monetary Policy:** The Federal Reserve maintained rates at **3.75%** in January. Current market pricing suggests a potential for two to three rate cuts later this year, with the first likely in June. * **Geopolitics:** Ongoing tensions in the Middle East and Eastern Europe continue to provide a floor for prices, though recent "guiding principles" for nuclear talks between the U.S. and Iran have temporarily dampened safe-haven urgency. * **Central Bank Demand:** Structural support remains robust as central banks are projected to purchase approximately **755 tonnes** of gold in 2026, continuing a trend of reserve diversification. Sector Performance and Supply Mining sector performance remains a highlight for the year. Major producers are reporting expanded margins due to the elevated price environment. Production guidance for 2026 remains steady, though supply is projected to remain tight due to regulatory constraints and limited new mining permits. Despite the immediate pullback, the broader technical trend for 2026 remains bullish. Analysts point to a long-term trajectory that could see gold challenge the **$5,100** resistance level in the coming weeks, with some institutional forecasts targeting **$6,000** per ounce by the second half of the year. The market is currently entering a phase of healthy profit-taking and consolidation. Liquidity is expected to normalize as major Asian markets return to full activity following the Lunar New Year holidays, potentially providing the necessary volume to test higher resistance levels.

US Dollar Strengthens Amid Expectations of Sustained Federal Reserve Interest Rates

The U.S. dollar climbed to its highest levels in weeks following the release of the January Federal Open Market Committee minutes. The report signaled a hawkish shift in policy sentiment, cooling expectations for immediate rate relief and pushing the U.S. Dollar Index (DXY) to approximately 97.71. The greenback's strength is fueled by a Federal Reserve that appears divided but largely cautious. While the benchmark interest rate remains in the 3.5% to 3.75% range, the minutes revealed that several policymakers are open to discussing rate hikes if inflation does not continue its descent toward the 2% target. This "two-sided" policy outlook has anchored the dollar as a preferred asset. Recent economic data has supported this stance, with durable goods orders and industrial production both exceeding consensus expectations. The January inflation print arrived at 2.4%, down from 2.7%, but the Fed remains wary of price volatility driven by potential trade shifts and labor market stability. In the bond market, the 10-year Treasury yield rose to 4.08%, snapping a three-day streak of declines. This upward movement in yields reflects a market recalibrating for a "higher for longer" interest rate environment. The spread between the 10-year and 2-year yields remains at 0.62%, indicating a persistent curve dynamic as investors weigh long-term growth against near-term policy restrictions. The surge in the dollar has placed significant pressure on major currency pairs. The Euro dropped toward the 1.178 level, struggling against the backdrop of a more aggressive U.S. rate outlook. Simultaneously, the Japanese yen weakened further, with the USD/JPY pair trading near 154.97 as the yield differential between the U.S. and Japan continues to favor the greenback. Regional currencies are also feeling the impact. The Malaysian ringgit eased to 3.89 against the dollar, and other Asian currencies remained on the defensive. Markets are now pivoting their focus toward the upcoming Core PCE report, which serves as the Fed's preferred inflation gauge. The current sentiment suggests that while two rate cuts may still be on the table for later in 2026, the window for a March reduction is rapidly closing. Investors are now pricing in a more resilient U.S. economy, which provides the Fed with the necessary cushion to maintain current rates until clearer evidence of a sustained 2% inflation path emerges.

US Stocks Close Higher on Growth in AI Sector

Indian equity markets maintained a bullish trajectory on Wednesday, February 18, 2026, as the Nifty 50 climbed **0.37%** to close at **25,819.35**. The BSE Sensex followed suit, gaining **283.29 points** to settle at **83,734.25**. This third consecutive session of gains was fueled by a robust recovery in financial and metal sectors, offsetting temporary weakness in the IT index. Domestic sentiment was bolstered by news of potential easing in U.S. steel tariffs, which sent the Nifty Metal index up **1.33%**. Banking stocks also surged, with the PSU Bank index rising **1.31%** to reach a fresh record high of **9,647**. Individual standouts included Godfrey Phillips, which skyrocketed **20%** following cigarette price hikes, and Netweb Technologies, which gained **9%** after announcing a "Make in India" AI supercomputer powered by Nvidia. On Wall Street, major indices opened with renewed vigor as concerns over artificial intelligence valuations began to ease. The Dow Jones Industrial Average rose **0.53%** to **49,796.62**, while the S&P 500 gained **0.72%** to reach **6,892.35**. The tech-heavy Nasdaq Composite outperformed with a **1.20%** jump to **22,850.41**, as investors rotated back into megacaps. Nvidia shares rose **1.9%** after securing a massive multi-year AI chip deal with Meta Platforms. Amazon also advanced **1.6%** as the market reacted positively to its **$50 billion** investment plan for AWS AI capabilities. These gains provided a much-needed reprieve after a volatile period where Big Tech lost over **$1.3 trillion** in market value since the start of the year. The U.S. Federal Reserve’s January meeting minutes, released Wednesday, indicated a significant policy split. While officials unanimously held interest rates at **3.50%–3.75%**, "several" participants suggested that rate hikes could return if inflation remains sticky. Current market pricing suggests a **63%** probability that the first rate cut of at least **25 basis points** will not occur until June 2026. Energy markets experienced a complex day. While global Brent crude is forecasted to average **$58 per barrel** throughout 2026 due to rising inventories, domestic Indian energy stocks faced sharp midday pressure. In contrast, the U.S. energy sector saw gains as investors rewarded companies showing durable cash flow and infrastructure growth over speculative software plays.

Indian Market Set for Positive Start Amid Strong Global Cues

Global Market Brief: February 2026 The global economy is currently navigating a path of divergent growth and shifting trade landscapes. Global output is projected to expand by **2.7%** in 2026, a slight cooling from the **2.8%** seen last year. While major economies are largely avoiding recession, growth remains below the pre-pandemic average of **3.2%**. Equity Markets and Sector Performance Equity markets have entered 2026 with a "winner-takes-all" dynamic, particularly in the United States. The S&P 500 is buoyed by an AI supercycle, with earnings growth in the technology sector forecasted between **13% and 15%**. However, concentration risks remain high as capital flows predominantly into market leaders. In India, the BSE Sensex recently reached levels around **83,734**, marking a resilient start to the year. Strength is concentrated in metals, banking, and FMCG sectors. The Nifty 50 is trading near **25,819**, supported by robust domestic flows. Conversely, IT services have faced pressure as the market transitions from AI experimentation to demanding measurable impacts. Commodities and Energy Energy markets are seeing a downward trend in prices as global production begins to outpace demand. Brent crude is currently trading near **$67.50** per barrel, with forecasts suggesting an average of **$58** for the full year. European natural gas has stabilized below **€30/MWh**, easing inflationary pressure on industrial sectors. Precious metals continue to serve as a hedge against geopolitical volatility. Gold prices have seen significant interest, recently retreating slightly from peaks but maintaining a strong position as investors monitor central bank signals. The World Bank anticipates an overall **7%** drop in commodity prices through 2026, marking a multi-year decline. Monetary Policy and Inflation Central banks are shifting from the aggressive easing cycles of 2025 to a "simultaneous hold" strategy. In the United States, the Federal Reserve is expected to target a policy rate of **3%** by year-end, while the European Central Bank maintains rates around **2%**. Inflation is cooling globally but remains "sticky" in certain regions. India's inflation rate was recorded at **2.75%** for January 2026, allowing the RBI to maintain a relatively accommodative stance with interest rates at **5.25%**. Trade and Technology Trends Global trade is undergoing a significant remapping due to new tariff structures. U.S. trade policies have shifted competitive advantages, making imports like Italian rice **12%** cheaper while South African wine has become **17%** more expensive relative to competitors. The technology sector has moved into the "Year of Truth for AI." Enterprises are shifting focus from experimental pilots to "Agentic AI" and "Cloud 3.0" infrastructures. Investment is moving toward hybrid architectures that balance cloud elasticity with on-premises data sovereignty. This shift is expected to drive a **17%** increase in solar energy generation to meet the rising power demands of new data centers.

Axis Securities Maintains 'Accumulate' Rating on Bank of India

Market Brief: Global Equity and Commodity Overview **February 19, 2026** Global financial markets are navigating a period of heightened sensitivity as investors balance corporate earnings resilience against shifting central bank expectations and geopolitical tensions. Following the release of the latest Federal Open Market Committee (FOMC) minutes, market participants are reassessing the timing of potential interest rate adjustments, with attention firmly fixed on upcoming inflation data. Equity Market Performance U.S. benchmarks demonstrated a cautious upward trajectory in the most recent sessions. The **Dow Jones Industrial Average** remains positioned near the **49,662.66** level, while the **S&P 500** has climbed to approximately **6,881.31**. The **Nasdaq Composite** has shown particular strength, rising to **22,753.64**, driven by a sustained rebound in large-cap technology shares. In India, the **NIFTY 50** closed at **25,819.35**, gaining **93.95 points** (0.37%). This growth was supported by strong performance in the metal and insurance sectors. Conversely, the technology sector faced headwinds, with major players like Wipro and Infosys seeing declines. The **BSE Sensex** recently ended its losing streak, recovering to close above the **83,277** mark. Economic Indicators and Monetary Policy The global economic outlook for 2026 remains steady with a projected growth rate of **3.3%**, according to the latest IMF updates. In the United States, January headline inflation eased to **2.4%**, marking its lowest level since 2021. Despite this cooling trend, the Federal Reserve maintained interest rates at **3.75%** in February. Markets currently price in a **60%** probability of a rate cut by March, though some analysts suggest July is a more likely timeframe given the resilience of the labor market. Commodities and Currencies Energy markets are experiencing volatility due to ongoing tensions in the Middle East. **Brent Crude** is currently trading around **$67.72** per barrel, while **WTI Crude** saw a recent rally to **$64.04**. These fluctuations are closely tied to security developments in the Strait of Hormuz. Precious metals continue to serve as a hedge against uncertainty. **Gold** prices are hovering near **$5,047.14** per ounce, reflecting a modest year-to-date gain of **14.71%**. In domestic Indian markets, gold (24-carat) is priced at approximately **₹1,27,152** per 8 grams in major metros. The currency landscape shows the **USD/INR** pair stabilizing at **₹90.56**, providing a level of macroeconomic comfort for Indian exporters despite broader global volatility. Sector Trends and Key Events Technology continues to be the primary driver of market sentiment. While innovation remains a catalyst, concerns over the high cost of infrastructure and sector-wide disruptions have led to increased selectivity among investors. In the banking and financial services sector, private and public sector banks have shown resilience, with **Bank Nifty** rallying over **760 points** to reach **60,949.10**. Investors are also monitoring the impact of the **Union Budget 2026**, which introduced targeted tariff reductions to bolster domestic manufacturing and clean energy. Looking ahead, the market will focus on the **Personal Consumption Expenditures (PCE)** price index and advanced **GDP** growth estimates to gauge the next directional move for global equities.

Pre-Market Analysis: Trading Outlook for the Current Session

Market Brief: Indian Equities Extend Recovery Indian equity benchmarks maintained their upward trajectory for a third consecutive session on **February 18, 2026**, reinforcing a steady recovery from recent lows. The **Nifty 50** climbed **94.35 points** or **0.37%** to settle at **25,819.35**, while the **BSE Sensex** gained **283.29 points** or **0.34%** to close at **83,734.25**. Early signals for **February 19** from **Gift Nifty** suggest a positive opening, with the index trading near **25,842.00**, up approximately **85 points**. This indicates continued domestic strength despite a mixed global backdrop. Sector Performance and Key Drivers Market momentum was primarily fueled by a surge in **Metal** and **Public Sector Bank** stocks. The **Nifty Metal** index rose **1.33%**, led by a **2.9%** jump in **Tata Steel** following reports of potential U.S. tariff easing. **PSU Banks** also outperformed, gaining **1.31%** as institutional interest gravitated toward state-owned lenders. In contrast, the **Information Technology** sector remained a drag, declining by **1.2%**. Heavyweights like **Infosys** and **HCL Tech** faced selling pressure ahead of key industry summits, while **TCS** also recorded losses. Institutional Activity and Currency Domestic resilience was supported by a notable shift in institutional flows. On the latest reporting day, **Foreign Institutional Investors (FIIs)** turned net buyers, injecting **1,154.4 crore** into the cash segment. **Domestic Institutional Investors (DIIs)** provided additional support with a net purchase of **440.4 crore**. On the currency front, the **Indian Rupee** appreciated slightly by **6 paise** to close at **90.66** against the US Dollar. This stability is attributed to sustained foreign inflows and a cooling volatility index, with **India VIX** dropping to **12.67**, signaling reduced market nervousness. Outlook and Technical Levels The market maintains a "buy-on-dips" bias as it approaches the **26,000** psychological barrier. Analysts identify immediate resistance for the **Nifty 50** at the **25,850 – 25,900** zone. On the downside, strong support is established at **25,650**, backed by significant put writing in the options market. Global cues remain a critical factor, with investors closely monitoring **U.S. Federal Reserve** meeting minutes and movement in **Brent crude**, which recently drifted below **$82 per barrel**. This softening of energy costs is expected to benefit oil-importing economies like India. While broader market sentiment is positive, profit-booking at higher levels remains a possibility given the rapid three-day rally. Selective stock-picking in the **FMCG** and **Banking** sectors continues to be the preferred strategy for market participants.