Bullish News

Collection

RBI Approves Bain Capital's Acquisition of up to 41.7% Stake in Manappuram Finance

Manappuram Finance has reached a pivotal milestone with the Reserve Bank of India (RBI) granting final approval for Bain Capital to acquire a significant stake in the company. The private equity giant, through its affiliates BC Asia Investments XXV and BC Asia Investments XIV, is set to acquire up to 41.66% of the company’s paid-up equity capital. Under the definitive agreement initially established in March 2025, Bain Capital committed an investment of approximately 4,385 crore. This capital infusion involves an 18% stake through the preferential allotment of equity shares and warrants at a price of 236 per share. The transaction triggers a mandatory open offer for an additional 26% stake from public shareholders at the same 236 price point. Following the completion of this deal, Bain Capital will be classified as a joint promoter, sharing control with the existing promoter group, which is expected to retain a 28.9% holding on a fully diluted basis. This strategic partnership arrives as the gold loan sector experiences a historic surge. Domestic gold prices in India recently touched a milestone of 1,60,540 per 10 grams in February 2026. This 18% rally has significantly enhanced the borrowing capacity of households, as the 75% Loan-to-Value (LTV) cap now allows for higher capital disbursals against the same quantity of collateral. Financially, Manappuram Finance reported a consolidated Asset Under Management (AUM) of 52,125 crore for the December 2025 quarter, reflecting a 17.9% year-on-year growth. The gold loan segment remains the primary engine, with its specific AUM jumping 58.2% annually to reach 38,754 crore. While top-line growth remains steady, the company is managing margin pressures. Consolidated net profit for the latest quarter stood at 239 crore, a 14.3% decline compared to the previous year. To reward shareholders, the board recently declared an interim dividend of 0.50 per share. The stock market has responded to these developments with notable activity. As of February 13, 2026, Manappuram’s share price closed at 302.15 on the NSE. Despite recent volatility, the stock has delivered a 56.32% return over the last 12 months, significantly outperforming broader indices. The entry of Bain Capital is expected to accelerate the company’s digital transformation and branch expansion. Management aims to leverage the new capital to enhance risk management and scale its non-gold portfolios, including vehicle finance and MSME lending, which currently contribute roughly 43% of total operations.

Indian Market Outlook: 7 Key Factors Influencing Sensex and Nifty Performance This Week

Market Overview: Volatility Grips Dalal Street The Indian equity market is navigating a period of intense turbulence as benchmark indices faced a significant retreat this week. A sharp sell-off in the technology sector, fueled by global anxieties, has dampened recent optimism. The **BSE Sensex** plummeted **1,048.16 points** (1.25%) to close at **82,626.76** on Friday, while the **NSE Nifty 50** sank **336.10 points** (1.30%) to settle at **25,471.10**. Investor wealth saw a massive erosion, with nearly **₹2.8 lakh crore** wiped out in a single session. IT Sector Under Siege The Information Technology sector remains the primary drag on the market. The **Nifty IT index** plunged over **8%** this week, marking its steepest weekly decline since April 2025. Heavyweights like **TCS** and **Infosys** saw their valuations pressured by emerging concerns over artificial intelligence disruption. The market capitalization of TCS dipped below the **₹10 lakh crore** mark for the first time since late 2020. Market sentiment turned sour following reports of new generative AI tools that could challenge traditional IT outsourcing models. Analysts note that while domestic buyers are attempting to support prices, the tech-led rout on Wall Street continues to spill over into Indian software exporters. Macroeconomic Indicators and Global Cues Economic data presents a mixed picture for the coming weeks. Domestic growth remains a bright spot, with the **RBI** recently raising its **FY26 GDP growth projection** to **7.4%**. In contrast, global macroeconomic triggers are creating headwinds: * **US Inflation:** The latest US Consumer Price Index (CPI) came in at **2.4%** for January, slightly lower than the expected 2.5%. While this hints at cooling inflation, strong labor data has led markets to price in a delay for US interest rate cuts. * **Currency Pressure:** The **Indian Rupee** settled at **90.64** against the US Dollar, reflecting broader currency market volatility. * **Foreign Inflows:** Institutional activity showed a "tug of war." Foreign Portfolio Investors (FPIs) were marginal net buyers of **₹108 crore** on Thursday, whereas Domestic Institutional Investors (DIIs) provided stronger support with purchases of **₹276 crore**. Technical Outlook and Risk Factors Technical chart patterns indicate a bearish shift as the Nifty 50 slipped below the crucial **25,500** support level. The **India VIX**, often referred to as the "fear gauge," surged by **15%**, signaling that traders expect heightened price swings in the immediate future. Geopolitical tensions and fluctuations in **Brent crude**, currently trading near **$67.80 per barrel**, add further layers of risk. While banking and FMCG stocks showed some resilience, the broader market remains cautious as it digests the final phase of corporate earnings and prepares for the upcoming US economic calendar.

Dalal Street Week Ahead: Nifty tests key support levels amid rising volatility

Market Overview Indian equity markets concluded a challenging week on February 13, 2026, as benchmark indices faced sharp selling pressure. The Nifty 50 slumped by **336.10 points** or **1.30%** to close at **25,471.10**. Similarly, the Sensex dropped **1,048.16 points** to end the session at **82,626.76**. The decline was largely driven by a massive sell-off in IT and FMCG heavyweights. High-profile stocks like Infosys, TCS, and HUL faced significant pressure, with HUL reporting a **30%** year-on-year decline in net profit for the December quarter. The IT sector was further rattled by rapid advancements in automation tools in the US, leading to concerns over traditional outsourcing models. Technical Indicators and Volatility Market sentiment turned jittery as the India VIX, a key gauge of expected volatility, surged by **13.36%** to reach **13.29**. While the index remains below the high-stress threshold of **20**, the sudden spike indicates a rise in investor fear following a period of relative calm. The Nifty 50 is currently testing crucial support levels near the **25,400** mark. Although the broader medium-term uptrend is technically intact, the failure to sustain levels above **25,900** earlier in the week confirms a corrective phase. Traders noted that the Relative Strength Index (RSI) is hovering in the mid-**50s**, suggesting neutral momentum with a slight downward bias. Institutional Activity Foreign Institutional Investors (FIIs) were aggressive sellers in the final session of the week, offloading equities worth **₹7,395.41 crore**. Domestic Institutional Investors (DIIs) attempted to cushion the fall by purchasing shares worth **₹5,553.96 crore**, but this was insufficient to offset the global exit. The divergence in institutional flows highlights a cautious stance from global funds, likely influenced by stronger-than-expected US employment data. This has increased the probability of the Federal Reserve maintaining higher interest rates for longer, with the likelihood of a June rate hold rising to **41%**. Economic Outlook On the domestic front, the new Consumer Price Index (CPI) series with a 2024 base year recorded retail inflation at **2.75%** for January 2026. This remains well within the Reserve Bank of India’s target range of **2% to 6%** for the 12th consecutive month. Despite benign inflation, the RBI maintained the repo rate at **5.25%** in its recent meeting, signaling a "neutral" but cautious stance. The central bank has revised the GDP growth outlook to **7%** for the upcoming quarters, reflecting confidence in India's structural resilience despite temporary market turbulence. Investors are currently prioritizing a stock-specific approach. Defensive positioning is recommended until the Nifty demonstrates a decisive close above the **25,800** resistance level. Fresh long positions are generally being deferred as the market waits for clearer global cues and the stabilization of institutional selling.

DeepSnitch AI Markets Gain Attention Amid Aster and LayerZero Consolidation

The intersection of institutional finance and artificial intelligence is reshaping the digital asset landscape as of February 2026. Two major developments are currently driving market sentiment: the expansion of tokenized private credit and the rise of AI-driven market intelligence. **Institutional RWA and Private Credit Evolution** OKX Ventures has formalized its move into the Real-World Asset (RWA) sector through a strategic investment in STBL. This partnership, which includes industry leaders Securitize and Hamilton Lane, centers on the launch of an ecosystem-specific stablecoin on the X Layer network. The project utilizes a sophisticated dual-token architecture designed for regulatory compliance. This model separates the stable settlement unit from the yield-generating layer. The stablecoin is backed by tokenized exposure to Hamilton Lane’s Senior Credit Opportunities Fund (SCOPE), effectively bringing institutional private credit onto the blockchain. **Market Indicators for RWAs** The broader RWA market is entering a high-growth phase. Current estimates place the total value of on-chain real-world assets at approximately $35 billion, supported by over 539,000 global holders. Analysts project a significant inflection point throughout 2026, with some forecasts suggesting the market could grow 3 to 5 times its current size as demand shifts from tokenized Treasuries toward private credit and commodities. Institutional participation is the primary driver, with 69.1% of the market share currently held by large-scale entities. The total asset tokenization market is expected to reach $3.01 trillion by the end of 2026, maintaining a compound annual growth rate of over 37%. **DeepSnitch AI and the Intelligence Layer** Parallel to institutional infrastructure, the "intelligence layer" of Web3 is seeing record capital inflows. DeepSnitch AI has emerged as a dominant player in this niche, developing what is being termed a Web3-native Bloomberg Terminal. The project has recently surpassed $1.58 million in its presale phase. The native token, $DSNT, is currently priced at $0.03906, representing a 165% increase for early participants. This momentum is fueled by significant "whale" participation and a unique information-arbitrage model. **Growth Catalysts for 2026** The DeepSnitch ecosystem is gaining traction by offering live AI analytics and tools that track whale wallets and on-chain flows in real time. Investors are moving toward projects that offer immediate utility and "staking scarcity" to mitigate supply inflation before public exchange listings. Market analysts are positioning these two sectors—RWA-backed stablecoins and AI-powered market terminals—as the primary breakout narratives for 2026. While the former provides the foundational liquidity and yield for institutions, the latter offers the data infrastructure necessary for retail and professional traders to navigate an increasingly complex on-chain environment.

Anupam Rasayan Q3 Net Profit Increases 12% Amid Revenue Growth

Anupam Rasayan India has demonstrated strong top-line growth in its third-quarter results for the 2025-26 fiscal year, reported on February 14, 2026. The specialty chemicals manufacturer saw total revenue jump by 31.35% to 512.44 crore, compared to 390.14 crore in the same period last year. Profitability remained on an upward trajectory with a 12% increase in consolidated net profit, reaching 61 crore. The company's standalone performance was notably stronger, with net profit surging 150% to 47.9 crore. For the nine-month period ending December 2025, consolidated revenue grew by 84% to 1,744.5 crore. Despite the revenue surge, operating margins faced pressure from rising expenses, which climbed to 454.59 crore during the quarter. EBITDA margins stood at 24.9%, reflecting a shift toward higher sales volumes amidst a complex global cost environment. A transformative milestone for the company is the definitive agreement to acquire 100% of US-based Jayhawk Fine Chemicals for 150 million dollars. This strategic move establishes a direct manufacturing presence in North America and integrates Jayhawk’s expertise in high-purity technologies and Suzuki Coupling with Anupam’s cost-efficient India-based manufacturing. The acquisition is being financed through 50 million dollars in new credit facilities and internal accruals. It is expected to be immediately earnings-accretive, opening doors to high-value markets including semiconductors, automotive electronics, and advanced pharmaceuticals. In the equity markets, Anupam Rasayan shares closed at 1,335.70 on February 13, 2026. The stock has delivered exceptional returns over the past year, rising approximately 93% and significantly outperforming the broader benchmark indices. The Indian specialty chemicals sector continues to evolve from volume-based growth to value-oriented innovation. Companies are increasingly focusing on custom synthesis and sustainable chemistry to meet rising demand in the electric vehicle, digital infrastructure, and healthcare segments. With a robust order book and newly signed contracts valued at 14,646 crore, Anupam Rasayan is positioned to leverage its expanded global footprint. The integration of US operations is set to provide a dual-site manufacturing model, offering global customers greater supply chain flexibility and localized production capabilities.

SEBI and NSDL Launch Investor Verification Awareness Campaign via Auto Rickshaws

Market Brief: SEBI-NSDL Investor Protection Drive The Securities and Exchange Board of India (SEBI) and National Securities Depository Limited (NSDL) have launched a high-visibility outreach campaign to safeguard retail investors. The initiative uses over **1,000 branded auto-rickshaws** as mobile awareness hubs across major cities, including Mumbai, Delhi, Pune, and Patna. These vehicles feature prominent QR codes that link directly to the **SEBI Check** portal and the **Saathi** mobile app. Fighting Digital Fraud The campaign addresses a sharp rise in sophisticated financial crimes. Recent data highlights that banking fraud values surged **30% year-on-year** in the first half of the current fiscal, reaching **₹21,515 crore**. By encouraging a "SEBI Check" before any transaction, the regulator aims to normalize the verification of UPI IDs and bank details of the **4,940 registered stock brokers** and other market intermediaries. Market Context This push for vigilance comes during a period of intense market volatility. On February 13, 2026, the **BSE Sensex** plummeted by **1,048 points**, closing near **82,850**, while the **Nifty 50** fell below the **25,500** mark. Investor wealth saw a single-day erosion of approximately **₹7.02 lakh crore**, primarily driven by a sell-off in the IT and metal sectors. Foreign Institutional Investors (FIIs) offloaded equities worth over **₹7,395 crore** during the session. Verification Tools Investors are urged to use official channels to confirm the "Fit and Proper" status of entities. The digital payment ecosystem continues to expand rapidly, with UPI volumes hitting **19 billion transactions** monthly and daily values nearing **₹90,000 crore**. To further this cause, SEBI has also introduced a multilingual, AI-enabled calling pilot. Authenticated calls for this program originate exclusively from the number **1600-313-384** to prevent spoofing and ensure investor security.

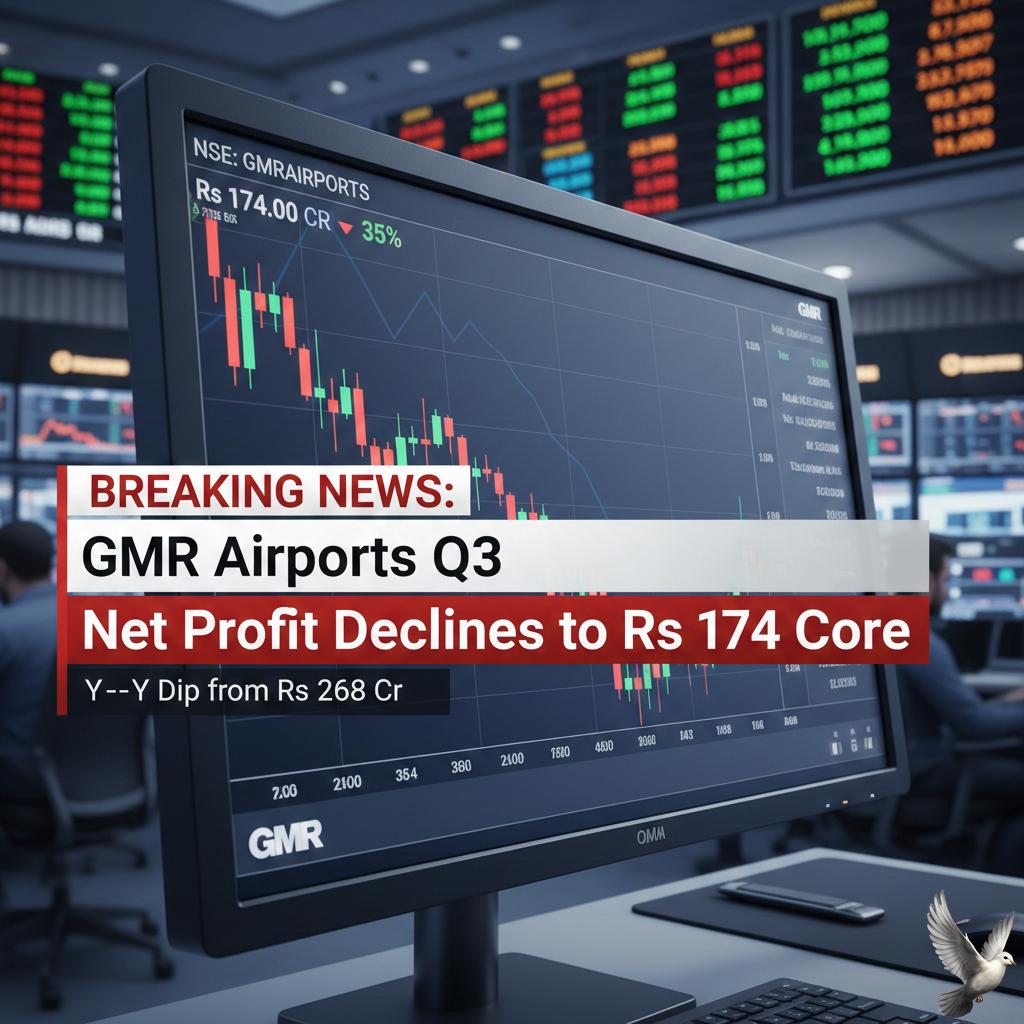

GMR Airports Q3 Net Profit Declines to Rs 174 Crore

GMR Airports Ltd (GAL) has released its financial and operational performance for the quarter ended December 2025, revealing a complex landscape of surging revenues and record passenger traffic tempered by significant one-time financial burdens. The company reported a 14% year-on-year decline in consolidated profit after tax, which fell to 173.96 crore. This dip was primarily driven by 183.12 crore in exceptional expenses. These one-time costs were linked to the termination of a cargo agreement with Celebi and the implementation of new labor laws. Despite the bottom-line pressure, total income saw a massive jump, reaching 4,082.77 crore compared to 2,748.22 crore in the same period last year. This revenue surge reflects the broader recovery and expansion of the Indian aviation sector. Operationally, GMR achieved record-breaking milestones. Total passenger traffic across its portfolio grew to 31.9 million for the December quarter. Delhi International Airport (DIAL) led this growth, handling 20.8 million passengers—its highest quarterly figure ever. DIAL also successfully swung back into the black, reporting a profit after tax of 231 crore. Hyderabad Airport also maintained a strong trajectory, with total income rising 23% to 6.1 billion for the quarter. The Mopa Airport in Goa reported a 77% income surge, highlighting its rapid scaling as a key tourism gateway. Non-aeronautical revenue remains a critical growth driver. In Delhi, this segment grew by 13%, while Hyderabad and Mopa saw increases of 17% and 45% respectively. Spending per passenger in duty-free zones also improved, with Delhi reaching 1,063 and Hyderabad hitting 879. The company’s debt profile continues to be a point of focus. Consolidated net debt rose by 10 billion to a total of 297 billion. This increase is attributed to ongoing investments in the new Bhogapuram airport and currency fluctuations affecting USD bonds. Management expects debt levels to peak between 30,000 and 31,000 crore by the end of fiscal year 2026. Market sentiment remains cautious but generally positive. As of February 2026, GMR Airports' share price has stabilized around 94.00 to 96.00 levels. Analysts maintain a "Buy" rating on the stock in over 85% of recent reports, citing long-term growth in international transit and the expansion of the Delhi Aerocity into a global business district. The broader Indian aviation industry is now the third-largest globally, with total passenger traffic projected to hit 303.63 million for the full fiscal year 2025. GMR is strategically positioned to capture this demand as it moves toward becoming a consumer-first platform with diversified revenue streams beyond traditional aeronautical services.

Southern Petrochemical Industries Corporation Q3 Consolidated Net Profit at Rs 54.07 Crore

Southern Petrochemicals Industries Corporation Ltd (SPIC) has reported a robust financial performance for the third quarter of the 2025-26 fiscal year. The company recorded a net profit of 54.07 crore for the October-December period, representing a significant jump from the 38.50 crore posted in the same quarter the previous year. Total income for the nine-month period ending December 31, 2025, rose to 2,419.36 crore, up from 2,340.82 crore in the prior year. Net profits for these nine months reached 182.01 crore. These results include a 20.10 crore insurance claim settlement related to previous flood-related operational shutdowns, which bolstered "other income" figures. The fertilizer sector is currently navigating a complex landscape. While India recorded its highest-ever monthly production of phosphatic and potassic fertilizers in January 2026 at 15.76 lakh metric tonnes, international supply chains remain under pressure. Geopolitical tensions in the Red Sea have rerouted shipments, increasing freight costs and voyage times for raw materials like DAP. Market data as of February 13, 2026, shows SPIC shares trading at approximately 69.47 on the NSE. The stock is currently positioned near its 52-week low of 68.50, contrasting with a yearly high of 128.20. Despite recent price volatility, the company maintains a price-to-earnings (P/E) ratio of roughly 9.03 and a dividend yield of 2.82%. Strategic growth remains a primary focus for the group. SPIC is nearing the completion of a major urea plant revamp, with operations expected to scale up by April 2026. This project aims to increase annual urea production capacity from 6.24 lakh tonnes to 9.12 lakh tonnes. The initiative also focuses on improving gas efficiency to 5.5 Gcal/tonne, aligning with new government environmental norms. The company has successfully transitioned to 100% gas-based production, reducing its historical reliance on naphtha. This shift is intended to optimize production costs and stabilize margins. Additionally, the group is investing in a new 150-tonne-per-day green ammonia unit to further its commitment to sustainable and eco-friendly agri-inputs. Recent management changes include the elevation of K R Anandan to the role of Whole-Time Director (Finance) and Chief Financial Officer. The leadership continues to emphasize alignment with national initiatives such as the "One Bharat One Fertiliser" scheme to support the domestic farming community through research-driven nutrient solutions.

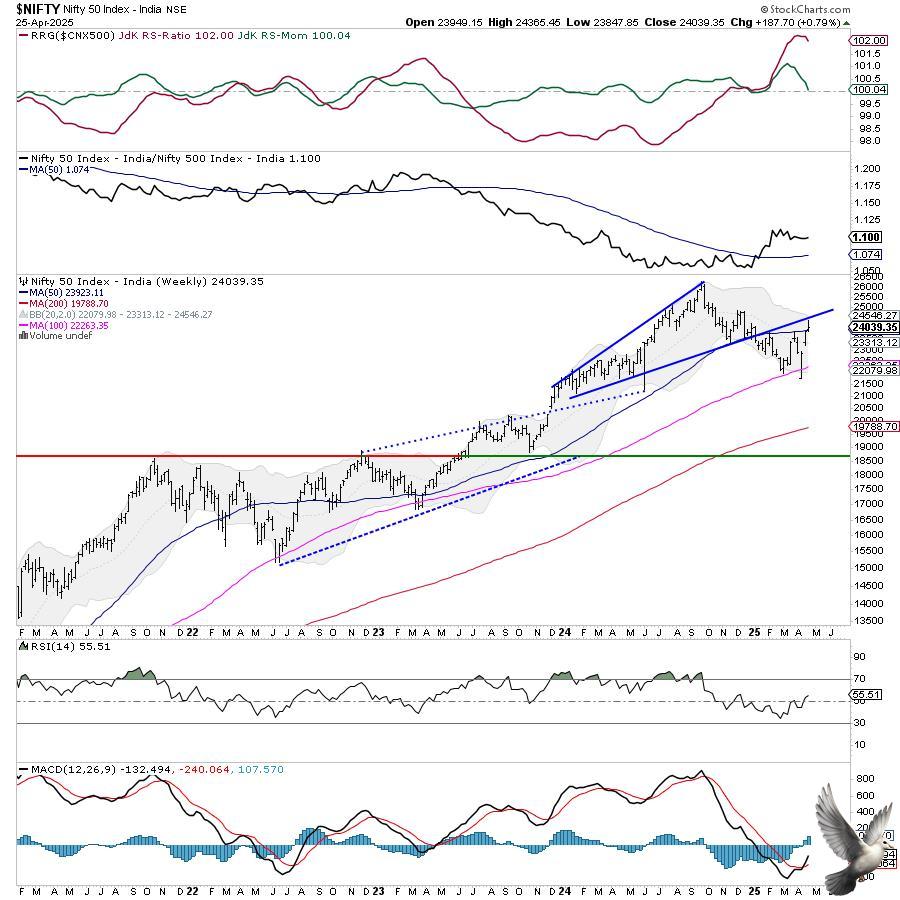

Nifty Breaks Key Moving Averages Amid VIX Spike as Analysts Track Coforge and Weekly Market Leaders

Nifty 50 Market Brief: February 14, 2026 The Indian equity market has entered a phase of heightened volatility, with the **Nifty 50** experiencing a significant structural breakdown. After back-to-back corrections, the index closed its latest session at **25,471.10**, marking a sharp single-day decline of **1.30%** or **336 points**. This move is technically significant as the index has slipped below its **20-day Moving Average (20DMA)**, which currently sits near **25,461**. Trading below this short-term anchor suggests a shift from a "buy-on-dips" environment to a more cautious "sell-on-rise" setup. Support and Resistance Zones The psychological support of **25,500** has been breached, turning the near-term bias weak. Immediate structural support is now identified at **25,060**, followed by a deeper floor at **24,801**. On the upside, **25,895** acts as the first major hurdle. A sustained recovery above the **26,000** mark is required to neutralize the current bearish momentum and invite fresh buying interest. Market Drivers and Volatility A "risk-off" sentiment has gripped the floor, evidenced by the **India VIX** jumping over **13%** to cross the **13.00** level. This spike reflects growing investor nervousness regarding global and domestic triggers. The recent sell-off was broad-based, resulting in a loss of approximately **₹7 lakh crore** in investor wealth in a single session. The total market capitalization of BSE-listed companies has retreated to **₹465 lakh crore**. Sectoral and Institutional Trends Sectoral performance remained largely negative. The **Nifty Metal** index led the decline with a **3.31%** drop, while **Realty** and **FMCG** fell by **2.23%** and **1.90%** respectively. Despite the benchmark's struggle, select heavyweights like **Bajaj Finance** and **SBI** showed resilience, gaining **3.09%** and **0.33%** respectively in the face of the broader downturn. Institutional activity remains mixed. While **Foreign Institutional Investors (FIIs)** were marginal net buyers of **₹108 crore** in the latest session, **Domestic Institutional Investors (DIIs)** provided stronger support with net purchases of **₹276 crore**. Global Context External pressures continue to weigh on domestic sentiment. Stronger-than-expected **U.S. jobs data** has dimmed hopes for near-term rate cuts by the Federal Reserve, while global tech volatility has pressured the Indian **IT sector**, which saw a **1.44%** decline. The **GIFT Nifty** is currently trading near **25,440**, suggesting a muted or flat start for the upcoming sessions as the market attempts to find a stable floor above recent lows.

**10 Stocks With Highest Retail Shareholding Increase in Q3 Including Coal India and Adani Power**

Retail participation in the Indian equity market reached a historic milestone in early 2026, with the total number of unique investor accounts on the National Stock Exchange surpassing **24 crore**. This rapid expansion highlights a significant shift in domestic wealth, as retail investors now hold an **18.75%** share of the total NSE market capitalization. This figure represents a 22-year high, reflecting a total value of approximately **₹84 lakh crore**. In the most recent quarter ending December 2025, specific companies emerged as magnets for small-scale investors. Leading the surge in retail shareholder growth were public sector giants and energy leaders. **Coal India** and **Adani Power** were among the top 10 stocks recording the sharpest increase in individual shareholding during this period. Other notable names included **Suzlon Energy**, **Reliance Power**, and **Yes Bank**, which continue to maintain high public ownership levels. Market performance in February 2026 has been defined by volatility and a cautious interest rate environment. The Reserve Bank of India recently lowered the repo rate to **6.25%**, seeking to support a GDP growth forecast of **6.7%** for the upcoming fiscal year. Despite this, the **BSE Sensex** and **Nifty 50** faced downward pressure, with the Sensex trading near the **82,626** level and the Nifty hovering around **25,471**. Investor wealth saw a significant contraction of over **₹7 lakh crore** in mid-February due to heavy selling in the IT and Metal sectors. **Hindalco** and **Hindustan Unilever** were among the top laggards, while **Bajaj Finance** and **State Bank of India** showed resilience with marginal gains. The shift toward indirect participation remains a dominant trend. Systematic Investment Plans (SIPs) hit a record monthly inflow of **₹31,000 crore** in December 2025. This consistent capital flow from households has acted as a crucial buffer against the **$8.7 billion** in net outflows from foreign portfolio investors (FPIs) recorded during the first half of the fiscal year. Demographic data confirms that the investor base is becoming more diverse. Women now account for **25%** of all NSE-registered investors, and over **50%** of retail holdings are now managed directly by individuals rather than solely through mutual funds. States like Maharashtra and Uttar Pradesh continue to lead, together accounting for over **6.7 crore** investor accounts. While blue-chip stocks like **Reliance Industries** and **HDFC Bank** remain the foundation of most portfolios, the growth in retail shareholders is increasingly visible in mid-cap and small-cap segments. This segment’s ownership reached a 19-year high of **16.7%**, as investors look beyond the top 10% of companies for higher growth opportunities. This [Retail Investor Performance Overview](https://www.youtube.com/watch?v=J3_ZZYCdJ5w) provides a visual breakdown of how these top companies are rewarding their growing shareholder base through consistent wealth creation. http://googleusercontent.com/youtube_content/0

RBI Tightens Funding Norms for Stock Brokers

The financial landscape for stockbrokers is undergoing a fundamental structural shift as the Reserve Bank of India (RBI) implements sweeping amendments to credit and capital market exposure. Effective **April 1, 2026**, the industry must pivot to a strictly regulated liquidity model that prioritizes systemic stability over high-leverage growth. The core of this transformation is the mandate for **100% secured funding**. Moving forward, unsecured credit lines and flexible guarantee structures will be largely eliminated. Historically, brokers could utilize bank guarantees where only **50%** was backed by fixed deposits, with the remainder supported by personal or corporate guarantees. This flexibility is now ending. Under the new framework, any bank guarantee issued in favor of exchanges or clearing corporations must meet a **50% minimum collateral** threshold. Crucially, at least **25%** of that collateral must be held in cash. For those using equity shares as collateral, the regulator has increased the minimum haircut to **40%**, significantly reducing the "borrowing power" of existing stock portfolios. The impact on proprietary trading is equally significant. Banks are now prohibited from providing funding for a broker's own trading activities. Exceptions are extremely narrow, limited only to essential market-making functions and specific debt warehousing. This move is designed to ring-fence bank capital from speculative market movements. Brokers must also adapt to continuous collateral monitoring. The era of periodic checks is being replaced by real-time oversight. Facility agreements must now include explicit clauses for immediate margin calls. If collateral value dips, brokers must replenish funds instantly or face automated deactivation of trading terminals. This tightening of liquidity arrives alongside SEBI’s **2025 Stock Broker Regulations**, which replace decades-old rules. The focus has shifted toward "Qualified Brokers" and real-time digital audits. While these changes increase the cost of compliance, they aim to eliminate the risk of "pooling" client funds and ensure that every trade is backed by verified, liquid assets. For market participants, these numbers signal a new era of "capital-heavy" operations. The reduction in leverage—combined with stricter upfront margin requirements for options—means that brokers will need deeper cash reserves to maintain the same volume of business. While this may pressure smaller firms, the result is a significantly more resilient financial ecosystem.

Reliance Infrastructure and SpiceJet Among 10 Smallcap Stocks Falling Up to 23% This Week

Small-Cap Market Brief: February 2026 The small-cap segment is currently defined by a sharp contrast between an index-level recovery and persistent volatility in specific stocks. While the **Nifty Smallcap 100** has surged over **6%** in the first half of February, broader market breadth remains fragile. On **February 13, 2026**, the **BSE Smallcap index** declined by **0.63%**, closing at **6,350.84**. This dip was accompanied by a weak advance-decline ratio, where only **240** stocks advanced while **970** declined. This suggests that while a few high-weight names are pushing indices higher, the majority of smaller firms are still navigating a corrective phase. Key performance data reveals significant divergence within the sector. Individual gains remain highly concentrated. **GE Power** recently delivered a **19.99%** return, and **Jay Bharat Maru** saw a similar surge of **19.99%** based on robust order books. Conversely, **SpiceJet** plunged **16.71%**, and **Vindhya Telelink** fell **6.20%**, highlighting the risks in companies facing operational or sectoral headwinds. Several factors are supporting the potential turnaround for the broader segment. Valuation resets following a difficult **2025** have made the space more attractive, with nearly **Rs 16 lakh crore** of small-cap market capitalization now estimated to be at fair or undervalued levels. The average P/E ratio for small caps stands at approximately **17x**, significantly lower than the **29x** seen in large-cap benchmarks like the **S&P 500**. Sentiment has been further bolstered by the recent **India-US trade deal**, which has triggered a reversal in foreign institutional investor (FII) activity. FIIs turned net buyers in **seven out of nine** sessions in early February. Additionally, corporate earnings for the third quarter have largely met expectations, with small-cap earnings growth projected to reach **19%** for the full year. Despite these positive triggers, market experts warn that the correction may be prolonged for businesses with weaker fundamentals. Approximately **321** stocks in the small-cap universe have seen price declines of **30%** or more recently. Investors are increasingly rotating capital into quality names in industrials, chemicals, and auto components, while avoiding "junk" stocks that lack clear revenue streams. Upcoming earnings reports from companies like **Prakash Industries** and **Ahluwalia Contracts** will be critical in determining if the current recovery can broaden beyond a handful of top performers. For now, the market remains a "stock-picker’s" environment where index gains mask underlying pressure on the majority of constituents.

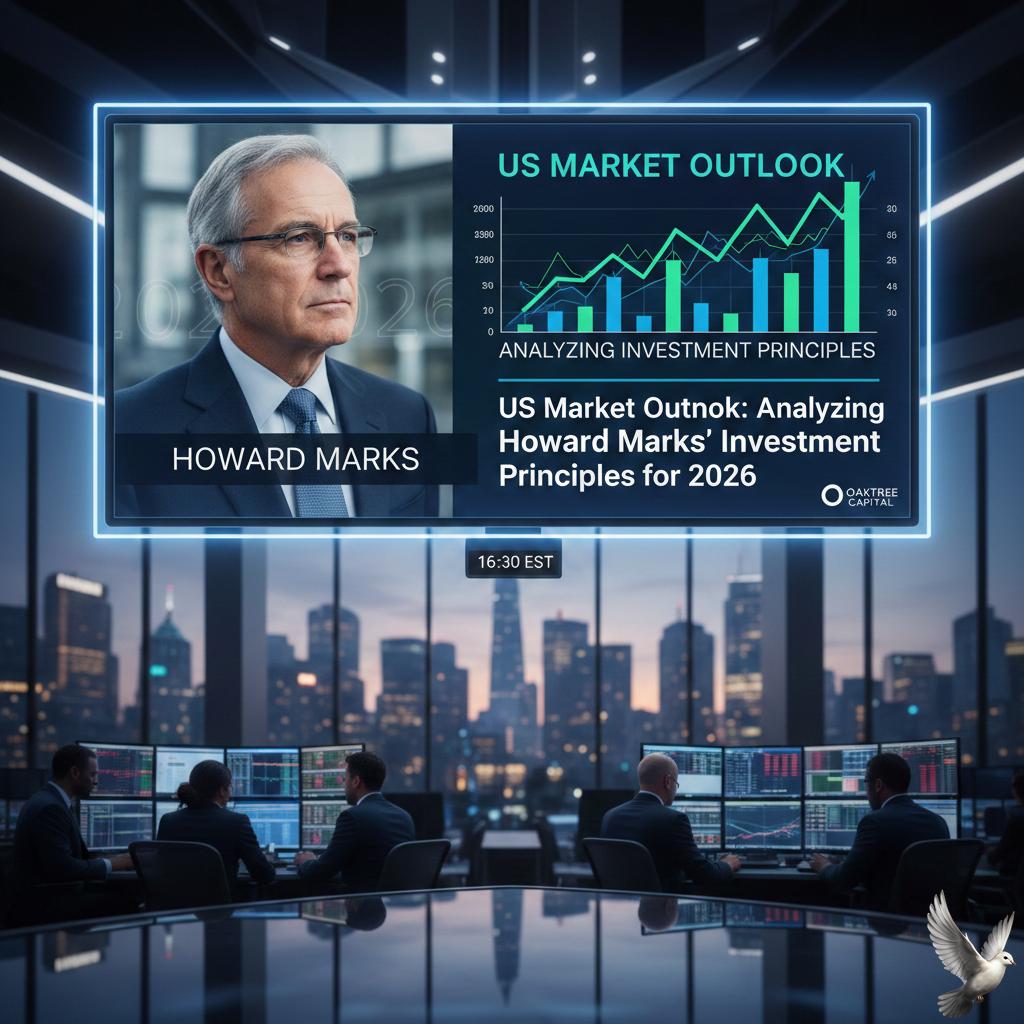

US Market Outlook: Analyzing Howard Marks’ Investment Principles for 2026

In today's landscape of high-tech optimism and elevated valuations, veteran investor Howard Marks emphasizes that understanding market cycles is more critical than predicting exact turning points. Rather than making drastic moves, he advises calibrating risk by gradually adjusting portfolios based on prevailing market signals. Global sentiment remains in a state of fragile equilibrium. In the U.S., equity indices like the S&P 500 have maintained a buoyant tone, yet risk appetite has recently moderated. The Risk Appetite Index dropped to 13% in February 2026, down significantly from 41% in January. This shift reflects growing caution over high-stakes macroeconomic data, including resilient wage growth and sticky inflation, which continue to challenge expectations for Federal Reserve rate cuts. A massive surge in capital expenditure defines the current cycle. The top five U.S. "hyperscalers" are projected to spend over 700 billion USD in 2026, a 60% increase driven by the race for infrastructure. While this signals confidence, the sheer scale of investment is beginning to strain free cash flows, forcing a transition toward external financing for tech giants that were previously self-funded. The Indian market is mirroring this need for caution. On February 13, 2026, the Nifty 50 experienced a sharp decline of 336 points, or 1.30%, to close at 25,471.10. Similarly, the BSE Sensex plummeted over 1,048 points to end at 82,626.76. This sell-off wiped out approximately 2.80 lakh crore INR in investor wealth in a single session, largely driven by a retreat in IT heavyweights like TCS and Infosys, which fell as much as 6%. Valuation discipline is now the primary tool for Indian investors. While structural growth remains intact, the "value" theme is outperforming "growth" strategies as the market punishes stocks with excessive premiums. Recent volatility has pushed the India VIX up by 13% to reach 13.29, signaling an expectation of continued near-term turbulence. In this environment, Howard Marks suggests that while no one can definitively label the current trend a bubble, going "all-in" poses an unnecessary risk of ruin. The strategy for 2026 shifts toward a barbell approach: maintaining exposure to long-term structural winners while increasing allocations to high-quality value stocks that can weather periods of high dispersion and market cooling.

Sir Martin Sorrell on AI Adoption, Global Risk, and India’s Market Position

The global advertising landscape is undergoing a structural shift as it crosses the **$1 trillion** threshold for the first time in 2026. Sir Martin Sorrell, Executive Chairman of S4 Capital, identifies external competitive threats and internal pressure from CFOs as the primary catalysts driving this rapid transformation. While technological curiosity exists, the urgent need for efficiency is what is truly forcing industries to integrate AI into their core operations. In the automotive and financial services sectors, AI adoption has moved from a peripheral experiment to a central requirement. In the automotive industry, AI is now indispensable for optimizing **800V** electric vehicle architectures and predictive thermal systems. Meanwhile, financial services are leveraging agentic AI to automate complex workflows and risk assessments. These shifts are fueled by a pivot toward performance-driven metrics, as brands move away from long-term building in favor of immediate activation. India has emerged as the most resilient growth hub within this fragmented global market. The Indian advertising sector is projected to reach **$20.7 billion** in 2025, maintaining a growth rate of **9.2%**. Digital platforms are set to command **55%** of the total market share, driven by a surge in retail media and short-form video. India is now consistently positioned as the fastest-growing market globally, with a middle class expected to reach **715 million** by the start of the next decade. Young professionals are advised to prioritize adaptability over traditional skill acquisition. Sir Martin Sorrell notes that as AI automates coding and language translation, the value of human labor will shift toward strategic positioning and the management of AI ecosystems. The democratization of knowledge is flattening corporate hierarchies, removing middle-management layers and allowing information to flow in real time across departments. Business structures are evolving from static messaging to dynamic, "always-on" environments. Brands are increasingly treated as living systems rather than fixed narratives, utilizing AI to maintain a consistent "soul" across millions of automated touchpoints. In this new era, success is no longer defined by the size of the advertising budget, but by the ability to build responsive, trustworthy systems that deliver personalization at a global scale. The global economy currently faces persistent inflation and slower globalization, yet sectors that combine technological scale with growth continue to outperform. India remains at the center of this trajectory, offering a blueprint for how digital ecosystems can thrive despite geopolitical uncertainty. Organizations that fail to restructure their workforces for an AI-native world risk being displaced by more agile competitors. [How AI is changing marketing](https://www.youtube.com/watch?v=Z9m-yZiFtmE) This video provides Sir Martin Sorrell’s direct insights on how AI-driven job churn and India's rising influence are fundamentally shifting the economics of the advertising industry. http://googleusercontent.com/youtube_content/0

Bitcoin and Ethereum Stabilize Near $68,000 and $2,050 Amid Cautious On-Chain Outlook

The global digital asset market is currently navigating a period of sharp recovery. Following a session of heightened volatility, the total market capitalization has stabilized at approximately **$2.43 trillion**. While the broader market recently experienced a minor contraction of **3.52%**, current intraday movements show a strong bullish reversal led by the largest assets. Bitcoin has climbed **3.84%** in the last 24 hours, trading at approximately **$68,936**. This rebound occurs as the market processes a significant options expiry totaling **$3 billion**. Institutional interest remains a primary driver, evidenced by the recent filing of new Bitcoin and Ethereum Spot ETFs by major funds. Bitcoin continues to hold a dominant market share of **56.60%**. Ethereum is outperforming the benchmark with a **5.67%** surge, bringing its price to **$2,052.52**. The asset is benefiting from positive sentiment surrounding its technical scaling roadmap and the potential for increased institutional inflows through new exchange-traded products. The altcoin sector is witnessing even more aggressive gains. Solana has emerged as a top performer with an **8.19%** increase, reaching a price of **$85.04**. Other major tokens are following this upward trajectory: * **XRP** gained **3.90%** to reach **$1.41** * **Cardano (ADA)** rose **5.40%** * **Dogecoin** moved up **4.21%** * **Binance Coin (BNB)** saw a more modest increase of **1.48%** * **Hyperliquid (HYPE)** and **Monero (XMR)** posted gains of **3.65%** and **7.58%** respectively Despite these price recoveries, investor sentiment as measured by the Fear & Greed Index remains at an "Extreme Fear" level of **9**. This suggests a significant disconnect between the current price action and the cautious outlook held by many retail participants. Trading volume remains robust at over **$103 billion** for the 24-hour period. This liquidity is supported by the convergence of traditional finance and digital assets, with established institutions increasingly integrating blockchain-based settlement systems and tokenized treasuries into their core operations.

Silver Prices Rise to Near Rs 2.50 Lakh Ahead of Monday Trade

Precious metals are demonstrating notable resilience as the market enters mid-February 2026. On the Multi Commodity Exchange (MCX), silver and gold are stabilizing following a period of intense volatility and technical corrections. Silver futures for March 5, 2026, are currently trading near 2,95,100 rupees per kg. This follows a significant recovery from recent lows, with the metal reclaiming ground after a sharp "liquidity flush" earlier in the month. The market is establishing a firm base around the 2,95,000 mark, supported by steady industrial demand from the solar and 5G sectors. Gold futures for April 2 delivery are holding steady near 1,55,780 rupees per 10 grams. While prices have retreated from the psychological 1,60,000 peak seen at the start of February, strong underlying support remains at the 1,52,000 level. Retail prices for 24-carat gold across major Indian cities like Mumbai and Delhi are mirroring this trend, consolidating as traders digest recent economic data. The gold-to-silver ratio remains high at approximately 84:1. This indicator suggests that silver continues to be undervalued relative to gold, a factor that is attracting selective restocking and bargain hunting from long-term investors. The broader macroeconomic environment is heavily influenced by shifted expectations regarding US Federal Reserve policy. Recent robust labor data and a 2.5% inflation reading have pushed projected interest rate cuts further into the second half of the year, likely July 2026. This has provided strength to the US dollar index, which is currently hovering near 97.05, acting as a temporary headwind for dollar-priced commodities. Industrial consumption remains a primary driver for silver. Despite record-high prices curtailing some jewelry demand in India, the expansion of data centers and artificial intelligence technologies is expected to maintain a structural supply deficit for the sixth consecutive year. Market sentiment is currently categorized as cautious but optimistic. Analysts are monitoring the 3,00,000 level for silver and the 1,58,000 resistance for gold as the next potential triggers for a momentum shift. For now, the focus remains on physical demand and the impact of global currency fluctuations on domestic bullion rates.

Infosys and Wipro ADRs Rise 4% Following Two-Day 14% Decline

Market Brief: Indian IT Sector Liquidity Crisis The Indian Information Technology sector is grappling with an unprecedented wave of capital erosion, as more than **Rs 7.4 lakh crore** in investor wealth vanished over the most recent trading sessions. The benchmark Nifty IT index has plummeted **19%** in a rapid descent, reaching its lowest valuation levels since October 2023. A combination of global structural shifts and domestic regulatory pressures has triggered this intensive sell-off. The primary catalyst, termed the "Anthropic Shock," stems from the launch of advanced AI automation agents capable of completing complex tasks—such as SAP migrations and legal compliance—in weeks rather than the years traditionally required by the outsourcing model. Key Performance Indicators The Nifty IT index currently trades near **32,681**, reflecting a sharp year-to-date decline of over **12.5%** for 2026. Market capitalization for the sector has shrunk to approximately **Rs 26.87 lakh crore**, as institutional investors pivot away from traditional software services. * **TCS:** The industry bellwether hit a fresh 52-week low of **Rs 2,579**, down nearly **32%** from its yearly high. * **Infosys:** Shares plunged over **7.5%** in a single session, with its market value falling below **Rs 5.41 lakh crore**. * **Wipro:** Trading at **Rs 213**, the stock has seen a **30.7%** decline over the past year. * **Tier-2 Pressure:** Mid-cap players like Coforge and Mphasis experienced intraday slippages of up to **6%**, highlighting a lack of safe havens within the tech pack. Structural and Macro Pressures Beyond AI-driven disruption, the sector is facing a "margin squeeze" from a new labor code implementation, which resulted in a one-time cost impact of **Rs 1,289 crore** for Infosys alone in the December quarter. Global macro headwinds are further complicating the recovery. Stronger-than-expected US jobs data has dampened hopes for imminent Federal Reserve rate cuts, maintaining high borrowing costs for the global enterprise clients that provide the bulk of Indian IT revenue. Market Outlook While the Nifty IT price-to-earnings (P/E) ratio has dropped to **22.03**—well below its 10-year average—volatility remains high. Analysts note that 30% to 40% of traditional IT service revenues remain at risk from AI-led deflation. Investors are currently prioritizing companies with high visibility for FY27 growth and those proactively integrating AI-led operating models to counter shrinking project timelines and reduced billing hours.

12 Stocks Record Five-Session Losing Streak

Market Brief: Global Outlook and Performance **February 14, 2026** The global economic landscape for 2026 is defined by steady but divergent growth, currently projected at **3.3%**. While technology investment and private sector adaptability provide a buffer, trade policy shifts and geopolitical tensions remain the primary risks to stability. Central banks continue to navigate a delicate path, balancing cooling inflation with resilient labor markets. Equities and Sector Performance Major U.S. indices faced significant pressure this week as concerns intensified over the return on investment in the technology sector. The **S&P 500** finished at **6,832.76**, recording a **1.6%** decline. The **Dow Jones Industrial Average** dropped **1.3%** to close at **49,451**, while the tech-heavy **Nasdaq** tumbled **2.0%** to end at **22,597.15**. The selloff was most pronounced in the **Information Technology** sector, which fell **2.6%**, and **Financials**, down **2.0%**. Investors shifted capital into defensive positions, providing a boost to **Utilities** (**+1.5%**) and **Consumer Staples** (**+0.9%**). This rotation reflects growing caution regarding the pace of earnings growth in high-valuation growth stocks. Fixed Income and Monetary Policy Treasury markets saw a relief rally following the latest inflation data. The **two-year Treasury yield** slid to **3.41%**, its lowest level since 2022. Markets are currently pricing in a federal funds rate target range of **3.0% to 3.75%** for the year, as the Federal Reserve maintains a patient approach following previous rate cuts. Current projections suggest the **10-year Treasury yield** may settle near **3.75%** by year-end. However, long-term fiscal concerns persist, with budget deficits expected to remain elevated, potentially exerting upward pressure on yields in the latter half of the decade. Commodities and Energy Precious metals experienced a sharp "liquidity flush" this week. **Gold** prices fell **2.59%** to **$4,966** per ounce, breaking below the psychological **$5,000** support level. **Silver** saw a more dramatic plunge of **9.71%**, trading near **$75.78** after a period of extreme volatility. Energy markets showed modest gains despite broader market weakness. **WTI Crude Oil** for March delivery rose to **$67.95** per barrel, marking a **3%** increase for the month of February. While global demand remains steady, supply chain adjustments and trade restrictions continue to influence local pricing dynamics. Trade and Economic Indicators New trade measures are actively reshaping global export competition. Tariff shifts have notably impacted specific sectors, with South African wine imports becoming **17 percentage points** more expensive relative to competitors, while Italian rice imports have become **12 percentage points** cheaper. Domestic labor data remains a bright spot, with jobless claims totaling **227,000** and an unemployment rate holding steady at **4.3%**. Consumer spending also remains resilient, advancing **0.4%** in the most recent monthly report, providing a necessary floor for continued economic expansion.

Upcoming IPO Activity: Gaudium IVF, Fractal, and Aye Finance Prepare for Market Entry

Gaudium IVF and Women Health Limited is set to enter the primary market with its initial public offering on February 20, 2026. This mainboard issue represents a significant move in the specialized healthcare segment, particularly as the Indian In Vitro Fertilization market is projected to grow from 1.32 billion USD in 2024 to 4.54 billion USD by 2034. The offering consists of a fresh issue of 1.14 crore equity shares and an offer for sale of 94.93 lakh shares by promoters. Investors can participate during the subscription window from February 20 to February 24. Allotment is expected to be finalized on February 25, followed by the official listing on the BSE and NSE on February 27. The company has demonstrated robust financial health ahead of the debut. For the fiscal year ending March 2025, Gaudium reported a total income of 70.96 crore INR and a profit after tax of 19.13 crore INR. This marks a sharp increase from the previous year’s profit of 10.32 crore INR. The firm currently operates through a hub-and-spoke model with 30 locations across India, including 7 central hubs. Capital raised from the fresh issue is earmarked for several key objectives. Approximately 18.93 crore INR will address total borrowings, while remaining funds will support the establishment of new IVF centers and general corporate purposes. The IPO is structured with 35% of the offer reserved for retail investors and 15% for non-institutional bidders. The healthcare sector continues to show resilience in a volatile market environment. While broader indices like the Nifty 50 and Nifty Midcap have faced recent pressure, the Nifty Healthcare Index has maintained relatively stable valuations with a P/E ratio around 34.21. Investor sentiment for specialized medical services remains strong, driven by a domestic infertility rate estimated at 10% to 15% among couples. This listing coincides with a broader expansion in the Indian capital markets, where fundraising through IPOs is expected to exceed 2 trillion INR in 2026. The issue is managed by Sarthi Capital Advisors, with Bigshare Services serving as the registrar. Market participants are closely watching the healthcare sector as it provides a low-volatility alternative during periods of macroeconomic uncertainty.

**Weekly Global Market Outlook: Five Key Themes**

Global Market Outlook: Retail, Commodities, and Policy Shifts The global financial landscape enters a high-stakes week as major retail results and economic data provide a health check on the consumer and industrial sectors. Walmart and the Global Consumer Walmart is scheduled to release its fourth-quarter results on **February 19, 2026**. Markets are watching closely after the retail giant recently crossed a **$1 trillion** market capitalization. Analysts expect earnings of **$0.73** per share on revenues of **$188.4 billion**, a potential **9.8%** increase year-over-year. These figures will serve as a primary indicator of consumer resilience, especially after U.S. retail sales remained unexpectedly flat in recent months. Commodity Volatility and European Mining European miners face a complex environment as commodity prices show extreme divergence. Metals and precious metals saw a sharp rise of **9.3%** and **17%** respectively at the start of the year. However, the broader outlook for 2026 remains cautious. The World Bank forecasts an overall **7%** drop in global commodity prices this year due to weak global growth and a growing oil surplus. Earnings from major miners will reflect these fluctuating input costs and the impact of the EU's new carbon border charges. UK Economic Indicators The UK economy is navigating a cooling labor market and easing price pressures. Headline CPI inflation was recorded at **3.4%** in December and is projected to fall toward **2.1%** by the second quarter of 2026. The Bank of England recently held interest rates at **3.75%**, though a narrow **5-4** vote suggests a shift toward easing is possible. Market participants are now focused on upcoming wage growth data, which is expected to slow from **5%** to **3.5%** this year. Central Bank and Business Activity Indonesia’s central bank, Bank Indonesia, has maintained its benchmark BI-Rate at **4.75%** to ensure Rupiah stability. With inflation currently at **3.55%**, the bank's next decision remains a critical pivot point for emerging market sentiment. On a global scale, business activity is showing signs of a "lower gear" recovery. The J.P. Morgan Global Composite PMI rose to **52.5** in January, up from **52.0**. While this indicates expansion, it remains below the long-term trend. Business confidence is currently hampered by geopolitical uncertainties and new trade policies, with many firms reporting intensified price pressures despite the acceleration in manufacturing output.