Bullish News

Collection

Walmart Earnings and Economic Data Headline Upcoming Market Week Amid AI Volatility

Market dynamics are shifting as investors pivot away from high-growth technology toward "old economy" sectors. This transition is fueled by mounting volatility in the AI space, where concerns over massive capital expenditure and the threat of industry-wide disruption have pressured major tech valuations. The energy sector has emerged as the clear leader in 2026, climbing nearly 23% year-to-date. This surge is supported by high free-cash-flow generation and strong dividend yields. Other defensive and value-oriented sectors are also showing significant strength, with consumer staples rising 15.9% and materials gaining 15.6%. Industrials have followed with a robust 11.9% increase. Contrastingly, the technology-heavy Magnificent Seven have struggled, posting a collective decline of approximately 6.2%. This rotation is further reflected in the equal-weighted S&P 500, which has outperformed its market-cap-weighted counterpart by nearly 5% this year. Inflation data released this week provided a slight reprieve for markets. The annual Consumer Price Index (CPI) slowed to 2.4% in January, its lowest level since May 2021. Core inflation, which excludes volatile food and energy costs, also eased to 2.5%. These figures were cooler than the 2.7% recorded in December, though they remain above the Federal Reserve's 2% target. Consumer spending health remains a primary focus as Walmart reports its latest earnings. The retail giant recently surpassed a $1 trillion market capitalization, driven by a 22% growth in global eCommerce and a 46% jump in its advertising business. Walmart’s quarterly revenue reached $177.4 billion, a 4.8% increase, providing a critical benchmark for household resilience. Looking ahead, the market anticipates the release of the personal consumption expenditures (PCE) price index and the minutes from the Federal Reserve’s January meeting. These developments will be vital in determining if the current rotation toward value and defensive sectors will persist through the first quarter.

Trilok Agarwal: Trade Deal Resolves Long-Term Overhang and Supports Multiple Expansion Potential

The landmark interim trade agreement between India and the United States has fundamentally shifted the investment landscape, triggering a decisive risk-on sentiment for Indian equities. This historic reset, formalized in February 2026, has seen the US slash reciprocal tariffs on Indian goods from 25% down to 18%, while total duties on specific categories have plummeted from 50% to zero. The deal unlocks immediate access to a 30-trillion-dollar US market, providing a massive competitive edge for Indian exporters against regional peers. With India’s benchmark Nifty 50 currently trading at a price-to-earnings (P/E) ratio of approximately 22.7, valuations remain below long-term averages. This creates significant headroom for multiple expansion as earnings visibility improves across the board. The pharmaceutical sector is a primary beneficiary of the new framework. Indian generic drugs and active pharmaceutical ingredients (APIs) now enjoy zero-duty access to the US, insulating the 10-billion-dollar export pipeline from previous punitive measures. This clarity is expected to drive higher margins and sustained volume growth for domestic drugmakers. The gems and jewelry industry is also poised for a major rebound. Tariffs on Indian diamonds and jewelry have been reduced from 50% to 18%, while select high-value categories like polished diamonds and platinum now attract zero duty. This shift targets a US market valued at over 61 billion dollars, offering a direct boost to profitability for Indian exporters. Broader economic indicators reflect this newfound stability. Goldman Sachs recently upgraded India’s 2026 GDP growth forecast to 6.9% following the announcement. Furthermore, India’s current account deficit is projected to narrow by 0.25% of GDP, supported by record-high exports that reached 825.25 billion dollars in the last fiscal cycle. Investors are also monitoring a massive 500-billion-dollar purchasing commitment from India for US energy, aircraft, and technology products over the next five years. This strategic alignment is expected to unlock a private investment cycle and strengthen the Indian Rupee, which has already emerged as one of the best-performing emerging market currencies this month. With inflation stabilizing near the 4% target and rural consumption showing resilience, the equity market reset appears well-supported by fundamental data. The combination of lower trade barriers and robust corporate earnings creates a compelling window for capital allocation into India’s manufacturing and export-oriented sectors.

Alphabet Bond Terms Reflect Strong Investor Demand

Alphabet has executed a massive **$31.51 billion** global bond sale, marking a decisive shift toward debt-financed growth to sustain its dominance in the artificial intelligence race. This fundraising effort includes a historic **100-year "century" bond** in the British pound market—the first of its kind from a major technology firm since 1997. Investor demand for these securities has been overwhelming. The century bond tranche alone was nearly **10 times oversubscribed**, signaling profound market confidence in the long-term viability of AI hyperscalers. This surge in borrowing is being mirrored across the sector; major tech peers are projected to collectively spend between **$660 billion and $690 billion** on infrastructure in 2026. Despite the high demand, the structure of these new bonds has triggered warnings within credit markets. Unlike traditional corporate debt, Alphabet’s latest offerings—along with recent issuances from Meta and Oracle—omit standard "change-in-control" covenants. These missing protections mean investors have little recourse if the company’s ownership or credit profile shifts dramatically over the next century. Financially, Alphabet remains in a position of extreme strength. The company holds over **$125 billion** in cash and equivalents, yet the decision to tap debt markets now allows it to lock in long-term capital while maintaining maximum operational flexibility. Management has indicated that capital expenditures could hit **$185 billion** this year, nearly double previous levels, as they scale data centers and specialized AI hardware. The market's willingness to accept fewer protections highlights a "new normal" for Big Tech debt. As these firms transition from asset-light software models to capital-intensive infrastructure owners, they are testing the limits of investor appetite. While credit spreads have remained relatively tight, analysts note that the sheer volume of new debt could eventually pressure valuations if AI returns do not meet expectations. This aggressive financing strategy underscores the "compute capacity" constraint currently facing the industry. By securing multi-decade funding now, Alphabet is positioning itself to navigate land, power, and supply chain bottlenecks that currently limit the growth of its Gemini models and cloud services. [Alphabet century bond analysis](https://www.youtube.com/watch?v=mXqqJGCy-hA) This video provides a breakdown of why Alphabet chose a 100-year bond and what it signals about their long-term strategy for AI funding. http://googleusercontent.com/youtube_content/0

S&P 500 Closes Higher Amid Tech Decline and Easing Inflation Data

Major US indices are navigating a volatile February as the technology sector faces a significant rotation. The Dow Jones Industrial Average, S&P 500, and Nasdaq Composite all posted weekly losses, with the tech-heavy Nasdaq leading the decline at 2.3%. While the Dow recently touched a fresh all-time high of 50,335, it has since retraced by 1.4% as investor sentiment shifts away from growth-oriented sectors. A primary catalyst for this downward pressure is the intensifying scrutiny of artificial intelligence investments. Major "hyperscalers" have committed over $500 billion to AI infrastructure for 2026, including Alphabet’s projected $50 billion and Amazon’s historic $75 billion capital expenditure. Investors are increasingly concerned that the timeframe for these massive investments to generate meaningful profits remains uncertain, leading to a "roller-coaster" performance for technology stocks. The market is witnessing a distinct "mirror image" of 2025’s trends. Software and services indices have slumped 15% since late January, while defensive and "old economy" sectors like Consumer Staples and Utilities have gained 1.4% and 1.2% respectively. This rotation reflects fears of AI disruption in traditional business models, such as insurance and wealth management, as well as high capital costs. Economic indicators are providing a mixed backdrop. January’s Consumer Price Index (CPI) cooled to 2.4% year-over-year, marking a nearly five-year low and beating expectations of 2.7%. Core inflation, excluding food and energy, slowed to 2.5%. While this cooling trend initially boosted hopes for Federal Reserve easing, a robust jobs report—showing 130,000 new positions added in January—has led markets to price in a more cautious approach. Current expectations suggest the Fed may hold rates steady until mid-2026, with approximately 60 basis points of total cuts anticipated by year-end. In corporate highlights, individual stock performance is diverging sharply. Nvidia continues to report record revenues, reaching $57 billion in its most recent quarter, yet the broader "Magnificent Seven" cohort has underperformed the equal-weighted S&P 500 this year. Hardware providers like Cisco have seen double-digit daily drops after missing margin targets, further weighing on the mega-cap space. The 10-year Treasury yield recently dropped 7 basis points to reflect a "flight to quality," while gold prices surged over 2% to reach $5,030 per ounce following the softer inflation data. Markets remain focused on upcoming retail sales figures and further inflation metrics to determine if the current tech-led pullback is a temporary correction or a more permanent shift in market leadership.

Sebi Chair Discusses Dual Role of AI in Fraud Detection and Risk Management

The Indian securities market is undergoing a structural transformation, shifting from a focus on individual institutions to a comprehensive oversight of systems and technology. SEBI Chairperson Tuhin Kanta Pandey recently outlined this "next regulatory frontier," emphasizing that regulation must become anticipatory rather than reactive to keep pace with rapid technological shifts. A central theme of this evolution is the dual role of Artificial Intelligence. While AI offers powerful capabilities for market surveillance and fraud detection, it also introduces significant risks, including algorithmic bias, lack of transparency, and the potential for a dangerous concentration of technological power. To counter these, the regulator is advocating for markets that are resilient by design. The scale of the Indian market now necessitates this high-tech approach. As of February 2026, India’s market capitalization has surged more than fourfold over the last decade, exceeding **Rs 470 trillion**. This represents **138%** of the national GDP, a massive increase from **81%** in FY15. The investor base has also expanded to a record **140 million** unique individuals. Under the 2026 regulatory framework, SEBI has implemented strict mandates for algorithmic trading to ensure market integrity. All trading strategies must now receive mandatory exchange approval before deployment. Each order must carry a unique **Algo ID**, allowing for real-time monitoring and the immediate tracing of errors or suspicious activity. Transparency is being reinforced through the classification of algorithms. "White box" strategies must be fully replicable and transparent, while "black box" providers are now required to register as Research Analysts and maintain exhaustive documentation of their logic. Furthermore, the use of open APIs for retail algorithmic trading is banned; all systems must reside within broker-hosted infrastructure to ensure a clear audit trail. Technological resilience is also being tested by current market volatility. On February 13, 2026, the Sensex experienced a sharp correction, tumbling over **1,000 points** while the India VIX, a measure of market fear, surged by **14%**. During this period, Nifty 50 also slipped below the **25,500** mark, highlighting the importance of robust, automated risk controls like "kill switches" to prevent systemic glitches. Capital mobilization remains strong despite these fluctuations. In the current fiscal year (FY26) through January, **Rs 11.6 trillion** has been raised, including proceeds from **329 IPOs**. India continues to lead globally in IPO activity, reinforcing the need for what the Chairperson describes as the "four Ts": Trust, Technology, Transparency, and Teamwork. The shift toward "SupTech" (Supervisory Technology) and "RegTech" (Regulatory Technology) is intended to reduce the friction of compliance while strengthening data governance. By moving toward dynamic supervision and risk-based monitoring, the regulator aims to protect the growing volume of household capital now flowing into the markets through mutual funds, which currently manage assets equivalent to **23%** of India’s GDP.

AI Impact on Capital Markets: David Schwimmer Perspective

India is rapidly cementing its status as the global nerve center for AI-driven financial innovation. LSEG CEO David Schwimmer recently underscored that the country’s unique combination of digital infrastructure and elite engineering talent has placed it at the heart of the transformation of global capital markets. As of early 2026, the Indian fintech market is valued at approximately **$142.5 billion**. Growth remains aggressive, with experts forecasting a compound annual growth rate of over **17%**, potentially pushing the sector toward a **$595 billion** valuation by 2034. The financial sector's pivot toward artificial intelligence is visible in the numbers. AI adoption within the Indian banking and financial services industry (BFSI) reached **68%** in the last fiscal year. This momentum is supported by the IndiaAI Mission, which operates with a dedicated budget of over **$1.2 billion** (₹10,372 crore) to scale computing power and domestic talent. Investment levels reflect this high-conviction environment. Private equity and venture capital funding for Indian fintech ventures reached **$10 billion** in 2025. Major global players are also doubling down, with recent landmark investments including a **$15 billion** AI hub by Google and an **$11 billion** AI innovation city planned by the Tata Group. Technological readiness is no longer a bottleneck. India now ranks **3rd** globally in AI vibrancy and is the world's second-largest contributor to AI-related projects on GitHub. The country’s digital backbone is equally robust, with internet connections surpassing **100 crore** (1 billion) and a 5G user base exceeding **400 million**. Schwimmer highlights that as AI integrates into complex market functions, the industry’s focus is shifting from data volume to data integrity. With customer demand for financial data rising by roughly **40%** annually since 2019, the risk of "AI hallucinations" or model drift makes precision a non-negotiable requirement. The move into 2026 marks an inflection point where AI moves from experimental pilots to "Agentic AI"—autonomous systems capable of making real-time, governed decisions. This evolution is expected to contribute as much as **$500 billion** to India’s Gross Value Added by the end of this year. For global capital markets, the message is clear: India provides the scale, the skills, and the infrastructure. The success of this new financial era will depend on maintaining high-quality data inputs to ensure the outcomes produced by these advanced models remain trustworthy and responsible.

Madhusudan Kela Suggests Using Market Volatility as a Strategic Entry Point

Market Outlook: Resilience Amid Volatility The Indian equity landscape is currently navigating a period of heightened sensitivity. Recent sessions have seen the **Nifty 50** retreat from the psychological **26,000** mark, settling near **25,471** after a sharp **1.3%** single-day decline. Similarly, the **Sensex** has corrected to approximately **82,627**, reflecting a broader sell-off in heavyweight sectors. Market veteran Madhusudan Kela maintains a grounded perspective, projecting moderate annual returns in the range of **10% to 12%**. This outlook acknowledges that the era of easy, broad-based gains may be transitioning into a phase of stock-specific performance. Strategic Focus and AI Integration Wealth creation in this environment is increasingly tied to the discovery of undervalued companies and emerging structural themes. A primary focus has shifted toward businesses effectively leveraging Artificial Intelligence to drive productivity. India's AI market is undergoing a massive transformation, projected to reach **$131.31 billion** by **2032**. Corporate India is moving beyond experimental phases, with nearly **87%** of enterprises now actively deploying AI solutions. Kela views this technological shift not as a threat, but as a critical catalyst for enhancing the bottom line of forward-thinking companies. Sector Performance and Risks Volatility has been most pronounced in the IT sector, where the **Nifty IT** index recently faced a significant rout amid fears of AI-led disruption to traditional labor models. However, resilience is visible in other pockets: * **Financial Services:** Leading private and PSU banks continue to provide a floor to the market, with **Bank Nifty** hovering around the **60,600** level. * **Manufacturing:** A steady infrastructure push and healthy capital expenditure remain key drivers for industrial growth. * **Consumer Goods:** Defensive buying in FMCG has offered stability during recent intraday swings. Foreign Institutional Investors (FIIs) have shown signs of returning as net buyers, signaling a stabilization of external flows despite a surge in the **India VIX** to **13.29**, indicating elevated near-term nervousness. The Long-Term Discipline Market fluctuations are categorized as entry points rather than deterrents. The current strategy emphasizes backing resilient entrepreneurs who can navigate global headwinds, such as fluctuating crude prices and geopolitical tensions. The principle of compounding remains the most potent tool for wealth generation. By identifying "bottom-up" opportunities in the mid-cap and small-cap space—where valuation gaps often persist—investors can position themselves for the next growth cycle. Current data suggests that while the indices may consolidate in a tight range between **25,400** and **26,000**, the focus remains on high-quality management and sustainable earnings growth over the long term.

Indian Equities Decline Over 1% Led by IT Sector Amid AI Concerns

Market Overview Indian equity benchmarks concluded a volatile week with significant corrections. On Friday, **February 13, 2026**, the **Nifty 50** plummeted **336.10 points (1.30%)** to settle at **25,471.10**. The **S&P BSE Sensex** witnessed a steeper drop, tumbling **1,048.16 points (1.25%)** to close at **82,626.76**. This downward trajectory wiped out approximately **₹7.02 lakh crore** in investor wealth in a single session. For the week, both indices posted a cumulative decline of roughly **1.1%**, marking a sharp reversal from previous gains. The IT Sector Rout The technology sector remained the primary drag on the market. The **Nifty IT index** plunged **8%** over the week, recording its most severe weekly loss in **10 months**. This selloff resulted in a market value erosion of **₹4.69 lakh crore** for the IT pack. Intraday losses on Friday saw the IT index crash over **5%** as major heavyweights faced intense selling. **Infosys** led the decline with a **7.5%** drop, followed by **TCS** at **6%** and **HCL Technologies** at **5.5%**. Catalysts: AI Disruption and US Data Market sentiment was heavily weighed down by "Anthropic Shock." The release of advanced AI tools has intensified fears that traditional IT outsourcing models—including coding, maintenance, and support—could face rapid automation and margin compression. Simultaneously, stronger-than-expected US employment data for January pushed the **US unemployment rate** down to **4.3%**. This signal of labor market resilience has dampened hopes for near-term interest rate cuts by the US Federal Reserve, maintaining high operational costs for Indian firms. Global and Domestic Context The domestic selloff mirrored a global retreat in technology shares. Overnight, the **Nasdaq Composite** fell **2%**, while Asian peers like the **Hang Seng** and **Nikkei** dropped **1.7%** and **1.2%** respectively. Broad-based selling in India extended beyond IT, with **Metals** falling **3.3%** and **Realty** dropping **2.2%**. On the domestic data front, January's retail inflation rose to **2.75%**, further complicating the outlook for local monetary easing. Institutional activity showed a stark divide: **Foreign Institutional Investors (FIIs)** offloaded equities worth **₹7,395.41 crore**, while **Domestic Institutional Investors (DIIs)** provided some cushion by purchasing stocks worth **₹5,553.96 crore**.

Uday Kotak Appointed Chairman of GIFT City

GIFT City has entered a new era of leadership with the appointment of veteran banker Uday Kotak as the Chairman of Gujarat International Finance Tec-City Company Limited. This move, effective as of mid-February 2026, sees the Kotak Mahindra Bank founder succeeding Hasmukh Adhia. The transition comes at a time of aggressive expansion for India’s first International Financial Services Centre. The financial hub has demonstrated significant growth, with over 1,100 entities now operational within the IFSC. The total asset base for the 38 banking units active in the zone has crossed $100.14 billion. This scale is reflected in the ecosystem's rising global profile, as GIFT City recently climbed to the 43rd position in the Global Financial Centres Index. Capital market activity remains a core driver for the hub. The GIFT Nifty continues to serve as a critical liquidity indicator, with monthly turnover figures reaching approximately $102.35 billion. Furthermore, the number of Fund Management Entities has surged to 194, managing total fund commitments of roughly $26.30 billion. Sector performance highlights include a major breakthrough in green finance. ReNew Energy recently issued $600 million in senior secured green bonds through its GIFT City subsidiary, marking the first international bond offering by an entity incorporated within the zone. In the aviation and maritime sectors, the hub now hosts 37 aircraft lessors and 34 ship lessors, supporting over 300 leased aviation assets. Policy updates from the Union Budget 2026 have further bolstered investor confidence. Key reforms include the extension of the IFSC tax holiday from 10 to 20 years and the introduction of a concessional 15% corporate tax rate for units once the holiday period concludes. These measures are designed to attract long-term global treasury operations and asset management firms. Operational milestones are also visible in the city's infrastructure and services. The launch of the Foreign Currency Settlement System now enables real-time transactions between IFSC banking units, bypassing the need for overseas correspondent banks. Additionally, India’s foreign exchange reserves have hit a record $701.4 billion as of early 2026, providing a stable macroeconomic backdrop for the hub's continued integration into global value chains. With the appointment of a Padma Bhushan-awarded leader and a robust regulatory framework under the IFSCA, GIFT City is positioned as a primary conduit for global capital, aiming to compete directly with established financial centers in Dubai, Singapore, and London.

Sebi Approves IPOs for Duroflex and Four Other Companies

SEBI Greenlights Pipeline of Five New IPOs The Securities and Exchange Board of India (SEBI) has cleared the path for five diverse companies to launch their Initial Public Offerings. Premier Industrial Corporation, Virupaksha Organics, Hexagon Nutrition, Om Power Transmission, and Duroflex received the regulator’s "observation" letters on February 13, 2026. This move comes as the primary market targets a massive **₹24,000 crore** fundraising goal for the month. Industrial and Infrastructure Focus **Premier Industrial Corporation** is set to offer **2.79 crore** equity shares. The issue includes a fresh issuance of **2.25 crore** shares and an offer for sale (OFS) of **54 lakh** shares. Capital will be deployed for a new wire manufacturing facility in Raigad, Maharashtra, and expansion at its Palghar site. **Om Power Transmission** is moving forward with a total of **1 crore** equity shares. This consists of **90 lakh** fresh shares and a **10 lakh** share OFS. The Ahmedabad-based firm, which reported a **₹220.85 million** profit in FY25, plans to use the proceeds for equipment purchases and debt reduction. Healthcare and Wellness Expansion **Virupaksha Organics** is seeking to raise **₹740 crore** through an entirely fresh issue. The Hyderabad-based API manufacturer aims to allocate **₹360 crore** toward capacity expansion and **₹195 crore** to repay existing borrowings. The company recorded revenue of **₹811 crore** in the latest fiscal year. **Hexagon Nutrition** has also received the go-ahead for an issue comprised entirely of an OFS of **3.08 crore** shares. As a major player in micronutrient premixes and clinical nutrition, the Mumbai-based firm is positioning itself for a transition to the public markets without raising new primary capital at this stage. Consumer and Retail Growth **Duroflex**, a leader in the mattress and sleep-tech segment, plans an IPO featuring a fresh issue of **₹184 crore** alongside an OFS of **2.25 crore** shares. The company has shown significant recovery, turning a **₹15.5 crore** loss in FY23 into a **₹47.1 crore** net profit by FY25. Funds are earmarked for opening **120** new company-owned stores and general corporate expansion. Market Context and Sentiment The approvals arrive during a period of moderate volatility. As of February 13, 2026, the **S&P BSE Sensex** stood at **82,980.12**, while the **Nifty 50** held the **25,592.65** level. Despite a brief sell-off in technology and metal stocks, retail and domestic institutional participation remains robust. The current 2026 IPO trend highlights a shift toward companies with sustainable cash flows and established profitability. Investors are seeing a broader mix of traditional manufacturing and specialized healthcare sectors over pure-play technology platforms. While listing dates are yet to be finalized, these five companies are expected to launch their bidding processes in the coming weeks.

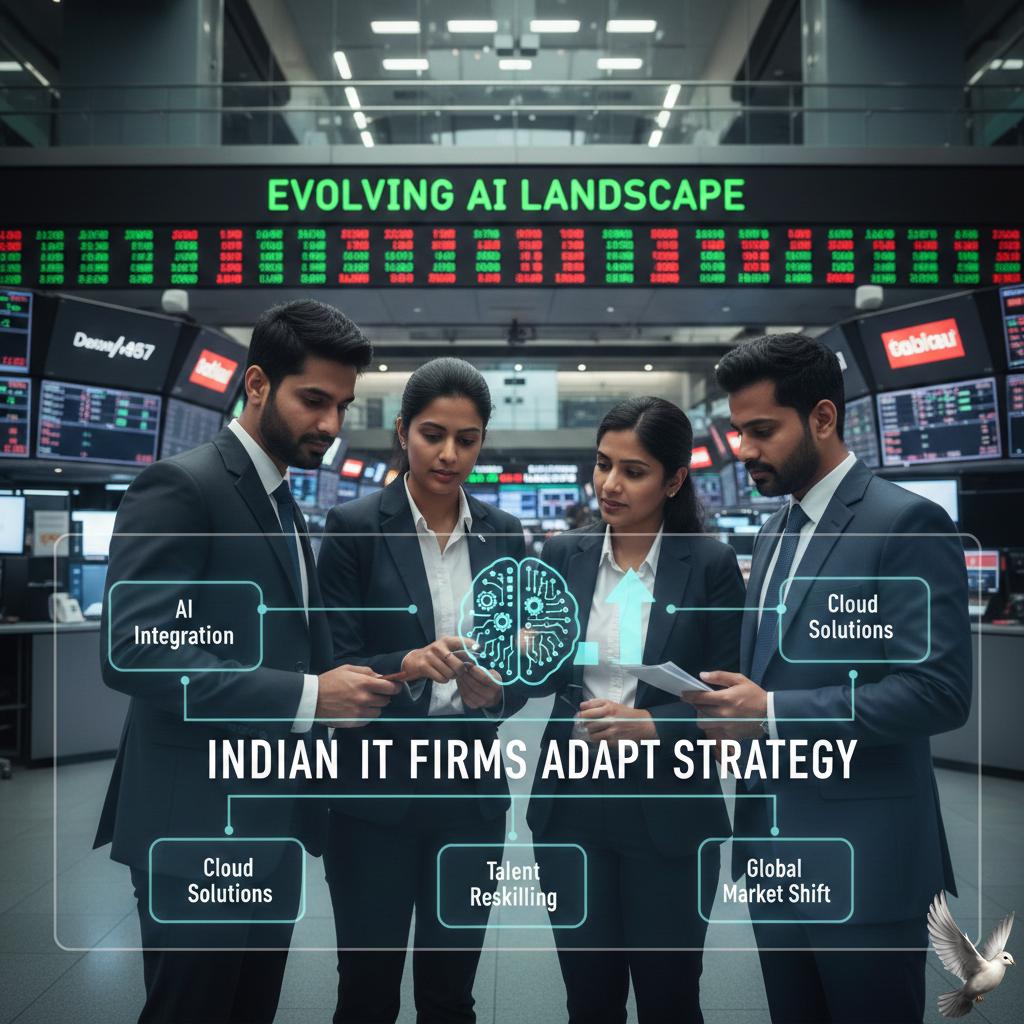

Indian IT Firms Adapt Strategy Amid Evolving AI Landscape

Market Brief: Indian IT Sector Resilience Amid AI Disruption The Indian IT landscape is undergoing a structural reset as of February 2026. While the sector faces immediate valuation pressure, a fundamental shift from labor-driven models to "intelligence arbitrage" is defining the next growth phase. Market Correction and Valuations The **Nifty IT index** witnessed a sharp correction in mid-February, plunging **5.51%** in a single session. This move wiped out approximately **₹1.3 lakh crore** in market capitalization. Heavyweights like **TCS** saw valuations dip below the **₹10 lakh crore** mark for the first time in years. Current trading multiples have moderated significantly. **Infosys** is trading at a P/E of roughly **21x**, while **TCS** sits between **20x and 22x**. These figures represent a notable discount compared to US-based AI-native firms, suggesting that the "AI disruption risk" is now being priced into Indian equities. AI Integration and Revenue Shifts The "Anthropic shock" and the launch of advanced agentic AI tools have fueled fears of revenue deflation in traditional maintenance work. However, tier-1 firms are reporting that AI is moving from experimental pilots to core profit drivers. **TCS** and **HCLTech** recorded nearly **20%** growth in AI-related revenue during the latest quarter. The industry is pivoting toward specialized infrastructure, such as the **$2 billion** "HyperVault" initiative by TCS for AI-ready data centers. **Infosys** is leveraging its Topaz Fabric to industrialize AI delivery for Fortune 500 clients. Deal Momentum and Pipeline The nature of contract wins is evolving. Clients are increasingly moving away from "mega-deals" in favor of smaller, phased, and faster-to-execute projects. **HCLTech** recently reported new bookings of **$2.6 billion**, notably achieving this without a single massive contract. **TCS** maintains a robust total contract value (TCV) pipeline between **$7 billion and $9 billion**. While project cycles have elongated, the demand for "cost takeout" deals and legacy modernization remains a critical cushion against global macroeconomic headwinds. Sector Outlook The sector is navigating a "K-shaped" recovery. While large-cap firms focus on consolidating high-value AI integration, mid-cap players are finding niche opportunities in Engineering Research & Development (ER&D). Operating margins remain resilient, with **TCS** maintaining a leading **25.2%** EBIT margin. Efficiency gains from AI-led productivity are expected to offset the impact of global wage hikes and a cautious spending environment in the US and Europe.

SEBI to Review ETF Pricing Framework to Address Price-NAV Divergence

The Securities and Exchange Board of India (Sebi) has issued a significant consultation paper on February 13, 2026, targeting a comprehensive overhaul of the pricing framework for Exchange-Traded Funds (ETFs). The proposal aims to synchronize ETF trading with real-time market dynamics by addressing structural lags and rigid price constraints. Addressing the Base Price Lag A primary concern highlighted by the regulator is the current use of **T-2 day closing Net Asset Value (NAV)** as the base price for setting daily trading ranges. This two-day lag often causes ETF price bands to become disconnected from the actual value of underlying assets, particularly during volatile sessions. To rectify this, Sebi has proposed shifting the base price calculation to **T-1 day data**. Three specific alternatives are under consideration: the volume-weighted average price from the last 30 minutes of T-1, the average indicative NAV (iNAV) from that same period, or the T-1 closing NAV where operationally feasible. Precision in Price Bands The existing framework applies a uniform **±20% price band** across most ETF categories. However, market data analyzed between April and December 2025 revealed that **99.8%** of equity and debt ETF movements remained within a **10%** range. For commodity-based funds, **98%** of movements stayed within **9%**. Sebi notes that the flat 20% limit is often excessively wide and does not accurately reflect the volatility profile of the underlying assets. Segment-Specific Proposals The regulator is moving toward a more granular, graded approach to circuit filters: * **Gold and Silver ETFs:** Proposed initial bands of **±6%**, which can be flexed up to **±20%** following 15-minute cooling-off periods. This follows recent volatility in precious metals in late January 2026. * **Overnight ETFs:** These will maintain tighter **±5%** bands given their low-volatility nature. * **Equity and Debt ETFs:** Transitioning toward graded bands that better align with the 10% movement threshold observed in the majority of trades. Operational Efficiency and Market Growth The proposed shift to T-1 data is also expected to reduce the need for manual adjustments related to corporate actions like dividends or bonuses. Currently, manual intervention in T-2 calculations increases the risk of operational errors. This regulatory push comes as the Indian ETF market shows massive expansion. Trading turnover surged from **₹51,101 crore** in FY20 to **₹3.83 lakh crore** in FY25. As of early 2026, the sector manages nearly **₹8.75 lakh crore** across approximately **260 funds**. By narrowing spreads and ensuring prices track underlying assets more closely, the regulator seeks to protect investors from "fat-finger" trades and price manipulation while supporting the market's continued liquidity. The public and stakeholders have until **March 6, 2026**, to submit comments on these proposals.

Updated Regulations for M&A Financing and Loans Against Shares

In a significant shift for India’s corporate landscape, the Reserve Bank of India has introduced final guidelines allowing commercial banks to provide acquisition financing. This move, effective April 1, 2026, overturns a long-standing prohibition and provides domestic companies with a more cost-effective alternative to expensive private credit and foreign funding. The new framework specifically permits banks to refinance a target company's existing debt. This is allowed only when such refinancing is considered integral to the acquisition finance. To maintain financial stability, the regulator has set a post-acquisition debt-to-equity ratio cap of 3:1 for the merged entity. Banks are now authorized to finance up to 70% of an acquisition’s total value. The remaining 30% must be funded by the acquirer through equity or internal accruals. To prevent over-leverage across the system, the RBI has raised the bank-level exposure limit for acquisition finance to 20% of eligible capital, up from the initially proposed 10% in draft rules. Eligibility for these loans is restricted to high-performing entities. Acquiring companies must have a minimum net worth of 500 crore INR and must have recorded net profits for the three preceding financial years. If the acquirer is unlisted, they must also hold an investment-grade credit rating before any funds are disbursed. The policy change comes as India’s M&A market experiences a massive surge. In 2025, financial sector deals alone reached 8 billion USD, marking a 127% increase year-on-year. Broad market activity in August 2025 peaked at over 20 billion USD in a single month, driven by strategic consolidations in energy, retail, and technology. Market liquidity remains a key focus as the central bank maintains a repo rate of 5.25%. While global bond yields have shown volatility, Indian macro-indicators remain stable, with GDP growth projected at 6.5% for the 2026 fiscal year. This regulatory easing is expected to further accelerate credit growth, which is forecast to reach 11.5% to 12.5% over the next two years. Strategic control is a central requirement of the new rules. Acquisition financing is permitted only where the buyer seeks to cross material ownership thresholds, ranging from 26% up to 90%. This ensures that bank capital is utilized for genuine business combinations rather than short-term financial engineering. In addition to corporate rules, the regulator has increased the individual borrowing limit against shares to 1 crore INR per person. For capital market activities like IPO and FPO subscriptions, the per-individual limit has been set at 25 lakh INR, requiring a minimum cash margin of 25%.

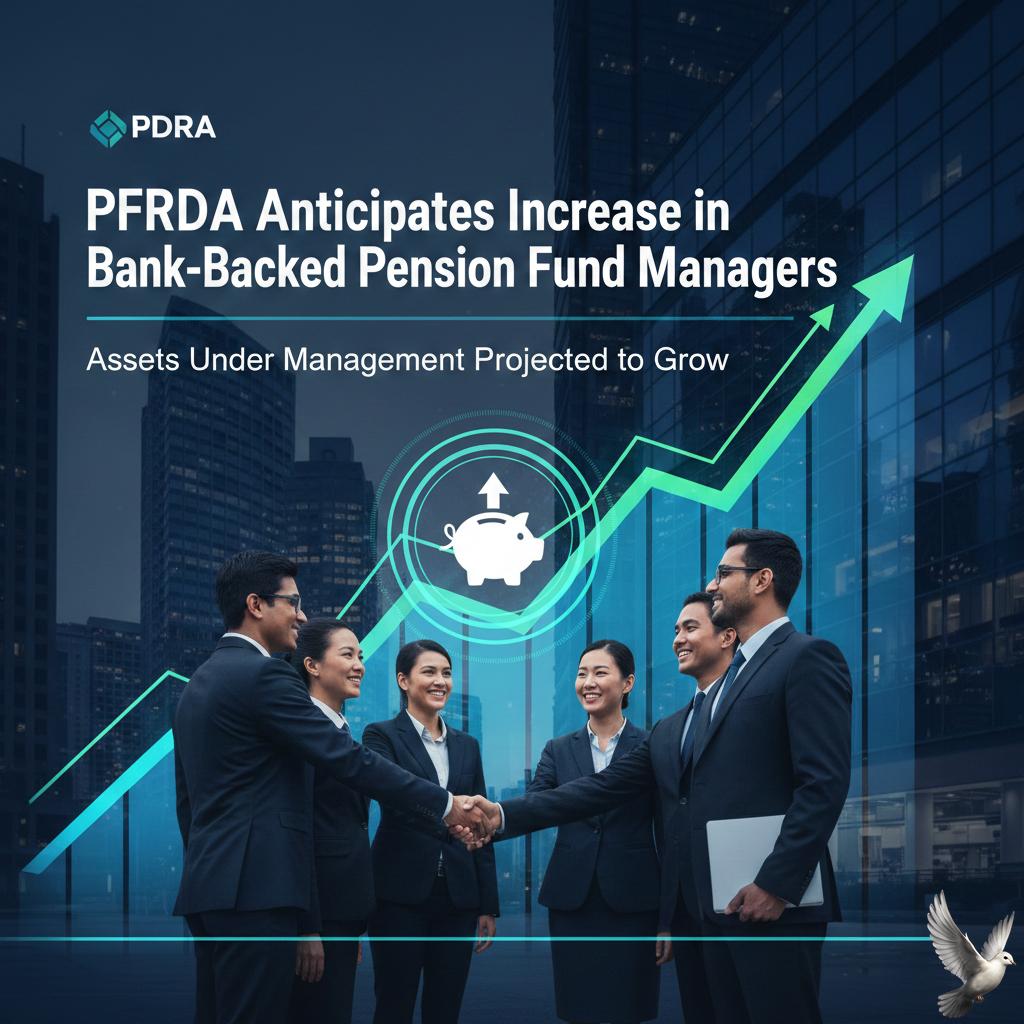

PFRDA Anticipates Increase in Bank-Backed Pension Fund Managers

The Indian pension sector is undergoing a significant structural shift as major financial institutions transition from distributors to fund managers. The Pension Fund Regulatory and Development Authority (PFRDA) has confirmed that Bank of Baroda and ICICI Bank have formally submitted applications to sponsor their own pension funds. ICICI Bank recently completed a **2.035 billion** acquisition of ICICI Prudential Pension Funds Management to bring the business directly under its corporate umbrella as of January 2026. Axis Bank is currently finalizing its application, while a consortium involving Union Bank of India and Dai-ichi Life is actively exploring entry into the space. This wave of institutional interest follows new PFRDA guidelines that allow Scheduled Commercial Banks to independently set up pension funds, provided they meet strict net worth and prudential criteria. Market Momentum and Scale The National Pension System (NPS) and Atal Pension Yojana (APY) continue to show aggressive growth. As of early 2026, the combined Assets under Management (AUM) have surpassed **16 lakh crore**. The total subscriber base has expanded to over **9 crore**, reflecting a successful push into the private and informal sectors. New regulatory frameworks are further driving this adoption. The Multiple Scheme Framework (MSF), launched in late 2025, has already crossed **145 crore** in AUM within just four months. This framework has attracted over **1.5 lakh** new accounts by offering subscribers up to **100%** equity exposure and segment-specific investment strategies. Regulatory and Fee Reforms To accommodate increased competition, the PFRDA has overhauled the fee structure. Effective April 1, 2026, a new slab-based Investment Management Fee (IMF) will be implemented for the non-government sector. The revised IMF rates are as follows: * **0.12%** for AUM up to **25,000 crore** * **0.08%** for AUM between **25,000** and **50,000 crore** * **0.06%** for AUM between **50,000** and **1.5 lakh crore** * **0.04%** for AUM exceeding **1.5 lakh crore** The regulator has also increased the maximum entry age to **85 years** and simplified exit procedures. Non-government subscribers can now withdraw up to **80%** of their corpus as a lump sum, provided they maintain a minimum **20%** annuity purchase. These moves aim to bring **25 crore** private-sector citizens into the pension net over the next five years. Performance and Outlook NPS returns remain competitive despite market volatility. Composite schemes with moderate equity exposure are generating returns above **9%**, while pure equity tiers have seen historical five-year returns ranging between **16%** and **21%**. The entry of major banks as sponsors is expected to deepen the market and improve digital distribution. PFRDA Chairperson Sivasubramanian Ramann has emphasized that distribution must become predominantly digital to reach the target of **100 cities** by March 2026.

Mizuho Financial Group Partners With Avendus to Strengthen Global Corridor Connectivity

**Mizuho-Avendus: The Japan-India Investment Corridor** Mizuho Financial Group is accelerating its expansion into India, positioning the country as a critical pillar of its global growth strategy. Under the leadership of CEO Masahiko Kato and Group CEO Masahiro Kihara, the bank is actively constructing a robust investment corridor to facilitate Japanese capital entry into the Indian market. **Strategic Acquisition of Avendus Capital** In late December 2025, Mizuho Securities reached an agreement to acquire a majority stake in **Avendus Capital** from KKR. The deal involves purchasing between **61.6% and 78.3%** of shares for approximately **$523 million** (¥81 billion). This acquisition transforms Avendus—a leading Indian investment bank and wealth manager—into a consolidated subsidiary. It fills a vital "missing piece" in Mizuho's investment banking portfolio, complementing its 2023 purchase of the U.S. advisory firm Greenhill. **Capital Flows and Sector Focus** Japanese investor interest in India has reached unprecedented levels. Japan has committed to a **10 trillion yen** investment target over the next decade. Mizuho’s strategy focuses on high-growth sectors where Japanese precision meets Indian scale: * **Manufacturing & Auto:** Japanese automakers are leading an **$11 billion** investment push, with Suzuki alone committing **$8 billion** to expand production. * **Semiconductors:** Partnerships like Tokyo Electron and Tata Electronics are establishing a domestic chip-making ecosystem. * **Green Energy:** Collaborative projects in green hydrogen and solar energy are being prioritized to meet net-zero goals. **Market Dynamics and Economic Outlook** The corridor is supported by India’s strong economic performance. India’s GDP growth is projected at **7.2%** for the **2025/26** fiscal year, making it the fastest-growing major economy. Despite global geopolitical shifts and trade tariffs, bilateral trade remains resilient. As of late 2025, Japan's exports to India surged **16.4%** year-on-year to reach **¥227 billion** monthly, while Indian exports to Japan also showed double-digit growth in key categories like electronics and automotive parts. **A Catalyst for Regional Integration** Mizuho aims to act as a "catalyst for change," bridging the two economies. Recent high-level discussions between Masahiko Kato and Indian leadership emphasized deepening financial cooperation in infrastructure and digital innovation. By integrating Avendus’s local market depth with Mizuho’s global institutional network, the bank provides Japanese corporates with a seamless entry point—from conceptual strategy to large-scale capital deployment.

US Stocks Rise as Cooling Inflation Boosts Expectations for June Rate Cut

Market Brief: U.S. Inflation and Fed Outlook U.S. consumer prices cooled significantly at the start of **2026**, with the headline annual inflation rate dropping to **2.4%** in January. This result beat economist expectations of **2.5%** and represents the lowest inflation level since **May 2025**. The month-over-month Consumer Price Index (CPI) rose by a modest **0.2%**. This cooling trend has revitalized expectations for interest rate adjustments, as the Federal Reserve looks for sustainable progress toward its **2%** long-term target. Interest Rate Futures and Fed Odds Financial markets reacted immediately to the cooling data. Interest rate futures now suggest an increased probability of a rate cut by **June 2026**. This follows a "pause" at the January FOMC meeting, which kept the benchmark federal funds rate at a range of **3.50% to 3.75%**. Current market pricing indicates roughly **63 basis points** of total cuts expected for the year. While a move in March remains unlikely with an **82% to 86%** probability of no change, the momentum for a mid-year pivot is growing as labor market signals also begin to stabilize. Sector Performance and Key Indicators * **Core Inflation:** The core CPI, which strips out volatile food and energy costs, edged down to **2.5%** year-over-year from **2.6%** in December. * **Energy and Goods:** Energy prices fell **1.5%** in January, driven by a **3.2%** drop in gasoline. Used car and truck prices also declined by **1.8%**. * **Shelter and Services:** Shelter costs remain a "sticky" component, rising **0.2%** and acting as a primary contributor to the remaining inflation. Airline fares saw a sharp spike of **6.5%**. Market Reaction U.S. equity indices turned positive following the report. The **S&P 500** futures erased earlier losses, reflecting optimism that the Fed may not need to keep rates "higher for longer" through the second half of the year. In the commodities space, gold futures climbed **1.3%** to reach **$4,985** per ounce, while silver surged nearly **5%** to **$78.72**. These moves highlight a shift toward assets that typically benefit from a lower interest rate environment. Economic Context The U.S. labor market continues to show resilience but is no longer "overheated." Monthly job growth is projected to average around **67,000** for the year, with the unemployment rate currently holding at **4.4%**. With the current Fed Chair's term expiring in **May 2026**, the transition in leadership adds a layer of policy uncertainty. However, the current data-dependent approach remains focused on balancing the cooling inflation with a stable employment backdrop.

Fortis Healthcare Q3 Net Profit Declines 22% to Rs 197 Crore

Fortis Healthcare has reported a significant 22% year-on-year decline in its consolidated profit after tax (PAT) for the third quarter ending December 2025. The net profit fell to 197 crore, down from 254 crore in the corresponding period last year. This dip was primarily driven by an exceptional loss of 55.2 crore, largely attributed to the implementation of new labor codes. Despite the bottom-line pressure, operational revenue showed strong resilience. Top-line income grew by 17.5% to 2,265 crore, compared to 1,928 crore in the previous year. This growth was fueled by robust performance in specialized clinical areas, specifically renal sciences and orthopedics, which saw growth of 27% and 20% respectively. Market performance for Fortis stock remains a focal point for investors. As of February 13, 2026, the share price closed at 918.80 on the NSE, reflecting a 1.05% intraday decline following the earnings announcement. The company currently maintains a market capitalization of approximately 69,180 crore, with shares trading between a 52-week high of 1,104.30 and a low of 587.10. Strategically, the group is aggressively pursuing an expansion-led growth model. A key highlight this quarter was the acquisition of the 125-bedded People Tree Hospital in Bengaluru for 430 crore. This move is part of a broader plan to scale its presence in the Bengaluru cluster from 900 beds to over 1,500 beds in the near future. The broader Indian healthcare sector is currently benefiting from a favorable policy environment following the Union Budget 2026. The budget has repositioned healthcare as a vital economic infrastructure, introducing the 10,000 crore Biopharma Shakti program and establishing five regional medical tourism hubs. These initiatives are expected to drive long-term demand for private hospital operators. Current industry trends indicate a steady rise in Average Revenue Per Occupied Bed (ARPOB), which has increased by 10% to 16% across leading networks. This shift is driven by a move toward higher-acuity procedures in oncology and neurology. Furthermore, the diagnostics segment remains a high-margin contributor, with top players reporting EBITDA margins between 25% and 35%. Looking ahead, Fortis aims to mitigate one-time costs through improved operational leverage and network optimization. With a net debt-to-EBITDA ratio sitting comfortably at 0.41x, the company is well-positioned for further inorganic growth and capacity additions across its mature hospital assets.

Rivian Shares Rise 20% Following Updated Delivery Forecast and Smaller SUV Plans

Rivian shares surged 20.07% on Friday, February 13, 2026, reaching approximately $16.85. The rally was fueled by the company’s optimistic outlook for 2026, centered on its pivot toward more affordable mass-market electric vehicles. The automaker reported its first-ever full year of positive gross profit in 2025, a significant $144 million milestone that marks a $1.3 billion improvement over the previous year. This shift toward profitability comes as the company successfully reduced production costs and grew its high-margin software and services revenue, which surged 222% year-over-year to $1.56 billion. Investors are primarily focused on the upcoming R2 SUV, which is positioned as a direct competitor to the Tesla Model Y. Priced at approximately $45,000, the R2 is expected to begin customer deliveries in the second quarter of 2026. Management projects that this new model will drive a 53% jump in total deliveries for the year. Projected delivery figures for 2026 are set between 62,000 and 67,000 vehicles. While production of the flagship R1T and R1S models is expected to remain flat, the R2 is expected to represent nearly half of the total volume. Rivian plans to scale this production by adding a second shift at its Illinois plant by late 2026, targeting a rate of 4,000 units per week. The strategic push toward affordability is a direct response to a challenging market environment. The expiry of federal EV tax credits last year has pressured sales across the industry, forcing manufacturers to lower entry prices to attract a broader buyer base. Despite the positive momentum, 2026 is being framed as a transitional year. The company expects an adjusted EBITDA loss between $1.8 billion and $2.1 billion as it absorbs the high capital costs of launching the R2 platform. Capital expenditures are projected to double this year, reaching roughly $2 billion. Liquidity remains a key strength for the company. Rivian ended 2025 with $6.59 billion in total liquidity, including $6.1 billion in cash and short-term investments. This provides a necessary cushion as the company builds its second factory in Georgia and continues its software joint venture with Volkswagen. Market analysts remain divided on the near-term outlook. Some firms have set price targets as high as $25, citing the success of the R1S as the best-selling premium electric SUV in several U.S. states. Others remain cautious, pointing to the intensive capital requirements and the risk of production hurdles during the R2 ramp-up. The broader sector is watching closely as Rivian attempts to transform from a luxury niche brand into a high-volume player. The success of this transition hinges on the R2's ability to maintain the brand's premium appeal while meeting the price expectations of the mass market.

US Stocks: Consumer Inflation Slows to Lowest Level Since May

US inflation cooled more than expected in January 2026, reaching its slowest annual pace since last spring. According to data released by the Bureau of Labor Statistics on February 13, the Consumer Price Index (CPI) rose 2.4% year-over-year. This figure fell below the 2.7% recorded in December and beat the 2.5% consensus forecast from economists. On a monthly basis, the headline index increased by 0.2%, down from the 0.3% rise seen in the previous month. The slowdown was primarily driven by a significant dip in energy costs. Energy prices fell 1.5% in January alone, with gasoline prices plunging 3.2% for the month and 7.5% over the past year. Core inflation, which excludes volatile food and energy sectors, remained slightly more persistent. The core CPI rose 0.3% in January, matching analyst expectations. On an annual basis, core inflation stood at 2.5%, down from 2.6% in December. This marks the lowest core reading since March 2021, signaling a gradual return toward the Federal Reserve's long-term targets. Sector-specific performance showed a mix of pressures. While shelter costs rose at a more moderate 0.2% monthly pace—down from 0.4% in December—other areas saw sharp increases. Airline fares surged by 6.5%, and personal care services grew by 1.2%. Conversely, used cars and trucks saw a 1.8% decline, providing additional downward pressure on the headline figure. The market response to the data was broadly positive. Equity futures trended higher while the US Dollar weakened against major currencies. Bond yields also retreated as traders adjusted expectations for the Federal Reserve's next move. Current market pricing suggests a 10% probability of a rate cut in March, though the central bank’s recent steady stance at 3.50%-3.75% indicates a cautious approach remains. Financial analysts noted that while the cooling is a welcome sign, potential headwinds remain for 2026. The implementation of new tax cuts and the ongoing pass-through of trade tariffs could impact price stability in the coming quarters. For now, the January report provides a rare bit of relief for consumer wallets and keeps the possibility of future interest rate cuts on the table for mid-year.

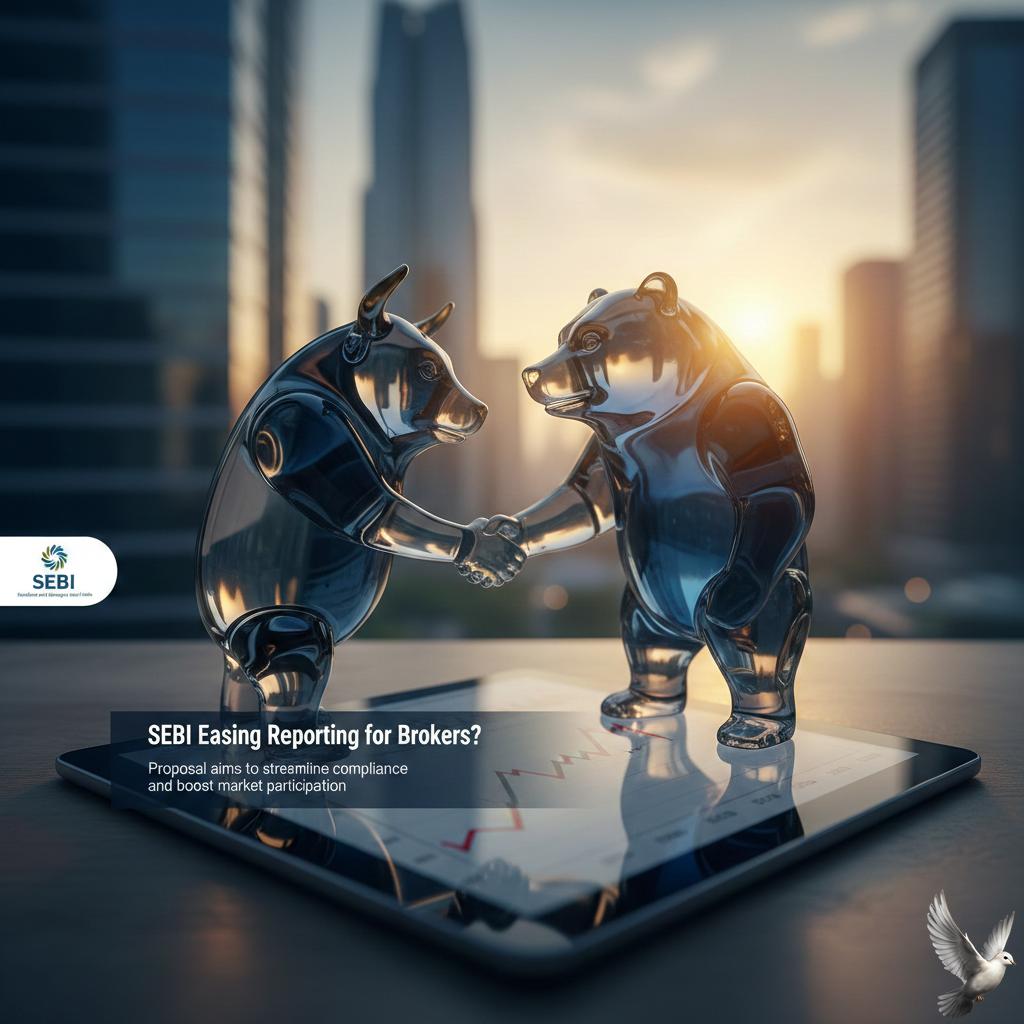

SEBI Considers Easing Reporting Requirements for Stock Brokers

In a major push for the ease of doing business, the Securities and Exchange Board of India (Sebi) has proposed significant relaxations to reporting norms for stock brokers. A key highlight of the proposal is the exemption of specific demat accounts from mandatory "tagging" requirements. This relief is aimed primarily at stock brokers who also operate as primary dealers, reducing the administrative burden of categorizing every account under their management. This regulatory shift coincides with the implementation of the new Sebi Stock Broker Regulations 2026, which officially replaced the 34-year-old 1992 framework on January 7, 2026. The updated code has streamlined compliance by cutting the regulation's length from 59 pages to just 29. It introduces modern provisions such as electronic record-keeping, joint inspections by exchanges and depositories, and a minimum net worth requirement of 1 crore for trading members. Market performance on February 13, 2026, reflected high volatility as these regulatory updates were processed alongside global headwinds. The BSE Sensex plummeted 1,048.16 points to close at 82,626.76, while the Nifty 50 dropped 336.10 points to finish at 25,471.10. This 1.30% decline was largely driven by a sharp selloff in the IT and metal sectors, with investor sentiment dampened by global tech concerns and shifting expectations regarding U.S. interest rates. Total market capitalization for BSE-listed companies fell to approximately 465 lakh crore (5.13 trillion USD), marking a one-day wealth erosion of nearly 7 lakh crore. Despite the broad downturn, specific stocks showed resilience. Bajaj Finance gained 2.57%, while Eicher Motors rose 1.54%. In contrast, Hindalco Industries emerged as a top loser, falling 5.75%, followed by Hindustan Unilever which declined 4.34%. Beyond broker reporting, Sebi has introduced a one-year special window from February 5, 2026, to February 4, 2027, allowing for the transfer and dematerialization of physical securities purchased before April 2019. This initiative addresses long-standing investor grievances and supports the broader transition to a fully digital securities ecosystem. These cumulative measures indicate a shift from reactive enforcement to preventive, digital-first compliance. By allowing brokers to undertake activities under other financial regulators and simplifying reporting for primary dealers, the regulator aims to lower the cost of entry for new fintech players while maintaining a robust safety net for the 465 lakh crore market. Investors and intermediaries are now transitioning to these consolidated standards to ensure market integrity during this period of heightened volatility.