Bullish News

Collection

CreditAccess Grameen Attracts Increased Investor Interest

CreditAccess Grameen Stake Acquisition Brief The landscape of India’s microfinance sector is shifting as major banking players and global firms eye a significant stake in **CreditAccess Grameen**. Deal Structure and Suitors The Netherlands-based promoter, **CreditAccess India BV**, is moving forward with plans to divest its **66.28%** majority stake. This divestment aims to provide a strategic exit for long-term investors, including **Olympus Capital Asia** and the **Asian Development Bank**. **HDFC Bank** and **Axis Bank** have emerged as the primary domestic contenders. While Axis Bank recently clarified to regulators that no "material event" has been finalized, market reports suggest it remains a frontrunner. Two additional global financial firms have also joined the exploratory phase, potentially sparking a competitive bidding war for the microlender. Financial Health and Valuation The promoter stake is estimated to be valued at approximately **₹14,000 crore**. CreditAccess Grameen remains financially robust, reporting a capital adequacy ratio of **26.4%** as of late 2025—well above the regulatory requirement of **15%**. Current performance metrics include: * **Return on Assets (ROA):** **4.0% – 4.5%** * **Return on Equity (ROE):** **18% – 20%** * **Market Capitalization:** Approximately **₹20,300 crore** * **Current Stock Price:** Trading around **₹1,268 – ₹1,272** (as of Feb 12, 2026) Market Trends and Outlook The microfinance industry is undergoing a recovery phase following recent stress from overleveraged borrowers. Larger, well-capitalized institutions are gaining market share, with the sector expected to grow at a **9.77% CAGR** through 2034. Strategic interest from HDFC and Axis Bank highlights a broader trend of "bank-led microfinance," where large lenders seek high-margin rural portfolios to meet priority sector lending targets. Analysts maintain a **"Buy"** sentiment for the stock, with price targets reaching as high as **₹1,630** based on projected growth in the retail finance mix. Management indicates that future internal accruals are sufficient to support a growth rate exceeding **20%** over the medium term, regardless of the ownership transition.

Potential Impact on Growth of Credit Life Insurance Sales

The Indian financial landscape is undergoing a significant shift as the Reserve Bank of India (RBI) implements stringent new directives to decouple insurance products from retail lending. These measures, integrated into the broader 2025-2026 regulatory framework, aim to eliminate "forced selling" and ensure borrowers are not coerced into high-premium life cover as a condition for loan approval. Market data as of early 2026 shows that the credit life insurance segment, which traditionally thrived on high attachment rates with personal and home loans, is facing a period of recalibration. Regulatory transparency now mandates that lenders provide a standardized fact sheet and an all-inclusive Annual Percentage Rate (APR). This figure must clearly reflect all costs, preventing insurance premiums from being buried within the loan’s perceived interest rate. Despite these hurdles, the broader insurance sector remains resilient. New business premiums for life insurers rose to 37,478 crore INR in January 2026, marking a 21.6% year-on-year increase. While the linking of policies to loans is restricted, the industry is pivoting toward digital-first distribution and voluntary protection models. The growth in the segment is now driven by individual demand rather than institutional bundling. Retail credit expansion continues at a robust pace, with GDP growth projected at 7.4% for the 2025-2026 fiscal year. This economic tailwind has pushed retail loan originations up by nearly 9.4% in recent months. However, the RBI’s focus on consumer protection means that banks must now maintain a clear separation between their lending desks and their insurance subsidiaries. Key structural changes are also influencing the market. The FDI limit for the insurance sector has been raised to 100%, attracting global capital into a market where only 3% of the population currently holds adequate life cover. This influx of capital is expected to fuel innovation in standalone credit protection products that offer better value than the previous bundled versions. For borrowers, the new environment offers lower friction and fewer hidden costs. The prohibition of automatic loan increases and the removal of prepayment penalties on floating-rate loans have further empowered consumers. The market is transitioning from a "push" model, where insurance was a hurdle to clear for credit, to a "pull" model, where protection is sought as a legitimate financial tool. Lenders and insurers are now focusing on the "Bima Sugam" platform and other digital aggregators to reach customers. This shift is expected to stabilize life insurance growth at 10.5% annually through 2035, even as the era of easy, loan-linked commissions comes to an end. The focus has decisively moved toward transparency, ethics, and long-term sustainability.

Major Indian IT ADRs decline amid broader Wall Street technology sector sell-off

Market volatility has intensified for Indian IT giants as global economic cues and structural industry shifts weigh on investor sentiment. Infosys saw its American Depositary Receipts (ADRs) slump by more than 7% in early trading on February 12, 2026, reaching an intraday low of $14.59. This sharp decline mirrored the performance of Wipro, whose ADRs fell 5.4% to $2.26. The downward pressure followed a significant sell-off in the domestic Nifty IT index, which shed 5.5% in a single session, eroding approximately ₹1.3 lakh crore in market capitalization across the sector. External pressures from the U.S. labor market have acted as a primary catalyst for this retreat. Recent employment data showed a stronger-than-expected January, cooling hopes for imminent interest rate cuts by the Federal Reserve. Sustained high interest rates typically compression the valuations of growth-heavy sectors like technology. Consequently, the Nasdaq Composite dropped over 1%, while major tech names like Cisco tanked 11%. Beyond macroeconomic factors, the sector is grappling with a profound structural transition. Artificial Intelligence is fundamentally altering the traditional headcount-based outsourcing model. While AI deals now represent nearly 74% of new contracts, there are growing concerns regarding "outcome-based" pricing and the automation of routine tasks. Analysts warn that while AI-first strategies drive long-term competitiveness, they may create near-term headwinds for revenue growth and recruitment. Despite the current price correction, long-term industry projections remain ambitious. The Indian IT sector is expected to reach $350 billion by the end of 2026, contributing nearly 10% to the national GDP. Global IT spending is also forecasted to grow by 10.8% this year, totaling $6.15 trillion. Investors are now closely monitoring deal flow and margin resilience. Wipro recently reported a stable operating margin of 17.6%, its best in several years, while Infosys continues to leverage a large-deal pipeline, including a $4.8 billion contract value high. However, both firms face a bearish technical outlook in the short term, with stocks trading below key moving averages as the market recalibrates for a higher-for-longer interest rate environment.

10 Key Factors Influencing Friday's Stock Market Performance

Market sentiment shifted to a cautious stance as heavy selling in the technology sector and resilient US employment data cooled expectations for immediate interest rate cuts. The Nifty 50 closed at **25,807.20**, marking a decline of **0.57%** and snapping a four-day winning streak. Similarly, the Sensex dropped **0.66%** to end at **83,674.92**. Key Market Drivers A primary trigger for the downturn was the US non-farm payrolls report, which added **130,000** jobs in January—surpassing the forecasted **70,000**. This unexpected strength in the labor market suggests the Federal Reserve may maintain higher interest rates for longer, reducing the appeal of growth-oriented assets. The IT sector bore the brunt of the sell-off. The Nifty IT index plummeted **5.51%**, with major players like Tech Mahindra and Infosys falling nearly **6%**. Concerns over AI-driven disruptions and a global tech correction added to the pressure, wiping out approximately **₹2.80 lakh crore** in investor wealth in a single session. Technical Outlook Nifty is currently navigating a consolidation phase between **25,800** and **26,000**. While the index managed to hold its immediate support at **25,800**, a breach below this level could lead to a deeper correction toward the **25,500–25,600** range. Resistance remains firm at **26,000**, characterized by heavy call writing that acts as a significant hurdle for any upward momentum. The India VIX rose slightly to **11.73**, indicating a modest increase in market nervousness, though volatility remains relatively low. Sector and Institutional Activity Despite the broader weakness, select sectors showed resilience. The Nifty Financial Services index gained **0.38%**, led by buying interest in ICICI Bank and SBI. Bajaj Finance emerged as a top gainer, rising **3.11%**. Institutional flows remain mixed. On February 11, FIIs were net buyers with **₹943.81 crore**, while DIIs recorded a minor sell-off of **₹125.36 crore**. This tug-of-war between foreign inflows and domestic profit-booking continues to define the current range-bound movement. Analysts recommend a selective approach, focusing on stocks with strong earnings visibility and relative strength. Buying interest is concentrated in banking, auto, and select healthcare counters, even as the overall market breadth remains tilted toward sellers with over **2,500** stocks declining on the BSE.

Restaurant Brands International tops quarterly sales estimates amid global growth and value initiatives

Restaurant Brands International (RBI) released its fourth-quarter and full-year 2025 financial results on February 12, 2026, delivering performance that surpassed market expectations despite a volatile economic landscape. The company reported consolidated system-wide sales growth of 5.8% for the fourth quarter, reaching $12.13 billion. This contributed to a full-year system-wide sales total of $46.76 billion, a 5.3% increase compared to 2024. Global comparable sales rose by 3.1% in the final three months of 2025. Growth was anchored by the International segment, which saw a 6.1% jump in comparable sales. The Burger King International division remains a core pillar of strength, maintaining demand across more than 100 countries and helping to offset domestic challenges. In the United States, Burger King saw a 2.6% increase in comparable sales during the quarter. This performance was boosted by high-profile marketing initiatives, such as the SpongeBob SquarePants meal, and a strategic focus on value menus. However, the U.S. market continues to face significant headwinds. Burger King U.S. franchisee profitability took a "step back," declining to approximately $185,000 per restaurant from $205,000 the previous year. This drop was primarily driven by a 20% surge in beef costs and aggressive price competition within the fast-food sector. Tim Hortons remains a dominant driver of stability, representing about 42% of RBI’s operating profit. The brand recorded its 19th consecutive quarter of positive same-store sales in Canada, with growth of 2.8%. Cold beverages were a standout performer, now making up a record 27% of its total beverage mix. Financial highlights for the quarter included: - Adjusted Diluted Earnings Per Share of $0.96, up 18.7% nominal. - Organic Adjusted Operating Income growth of 15.6%. - Total GAAP revenues of $2.47 billion. - Net Leverage reduced to 4.2x, down from 4.6x a year ago. RBI returned roughly $1.1 billion to shareholders in 2025 through dividends and continued its aggressive modernization plan. The "Royal Reset" initiative has now updated 58% of the Burger King U.S. estate to a modern image, up from 51% in 2024. Looking ahead to 2026, the industry anticipates persistent cost pressures. Food-away-from-home prices are forecast to rise by 4.6%, while wholesale beef prices are expected to remain elevated with a projected 6.9% increase. The stock market reacted sharply to the report on February 12. Shares of RBI (NYSE: QSR) fell 5.56% in mid-day trading to around $66.77, as investors weighed the international growth against the margin compression seen in the U.S. segments. Management remains focused on a long-term goal of 5% net restaurant growth and continues to transition Burger King China toward a new ownership structure to reignite regional expansion.

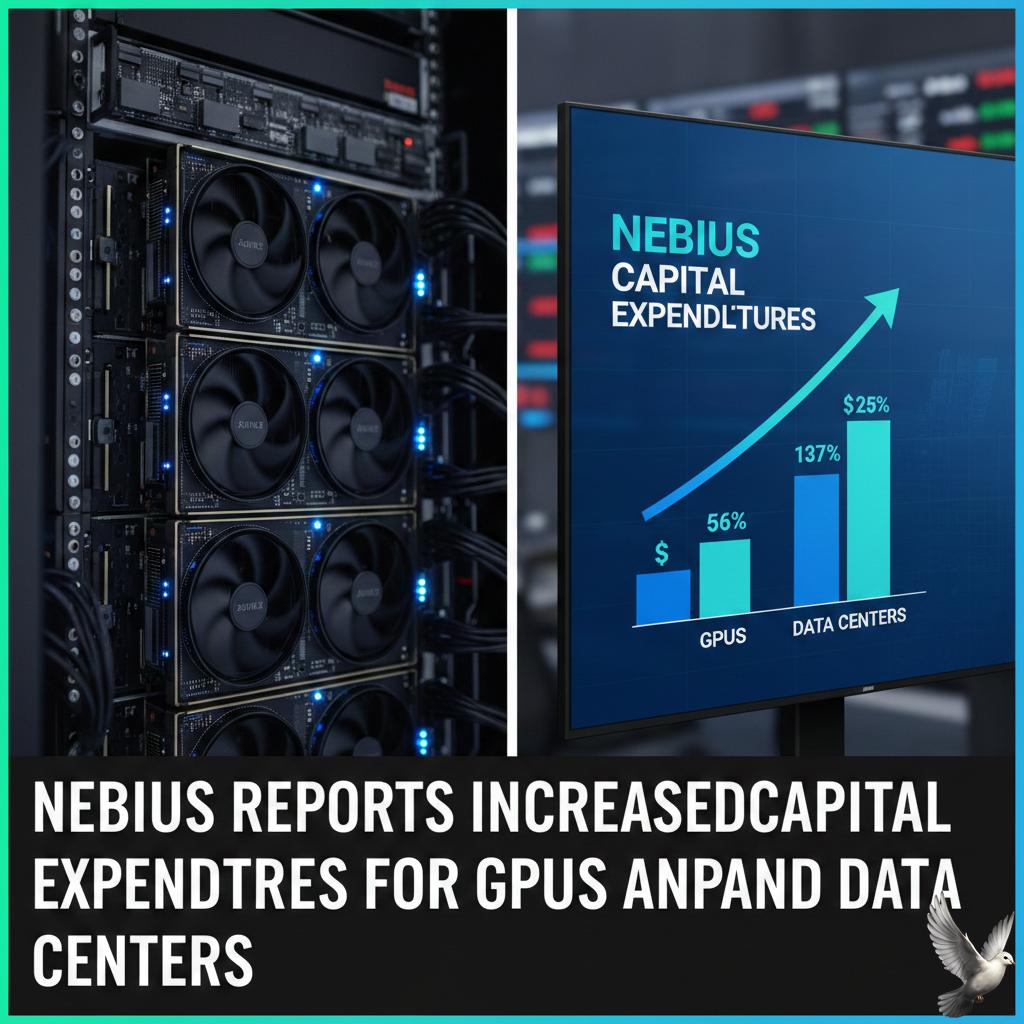

Nebius Reports Increased Capital Expenditures for GPUs and Data Centers

Nebius Group (NASDAQ: NBIS) disclosed a significant acceleration in capital expenditures during its fourth-quarter earnings report on Thursday, February 12, 2026. The Amsterdam-based AI cloud provider is aggressively scaling its infrastructure to address a persistent supply-demand imbalance in the enterprise AI market. Capital spending for the quarter ending December 31 surged to approximately **$2.1 billion**. This represents a massive increase compared to the **$416 million** invested during the same period the previous year. Total capital expenditure for the full year 2025 reached **$4.07 billion**, primarily directed toward securing high-performance Nvidia GPU clusters and expanding data center footprints. Revenue Performance and Outlook Revenue for the fourth quarter reached **$227.7 million**, a staggering **547%** year-over-year increase. Despite this growth, the figure fell short of the **$246.1 million** consensus estimate. For the full year, revenue climbed **479%** to **$529.8 million**. Management has set aggressive targets for the coming year. The company expects to end 2026 with an annualized revenue run-rate between **$7 billion and $9 billion**. This is a substantial leap from the **$1.25 billion** run-rate recorded at the close of 2025. Infrastructure and Capacity Expansion Nebius is currently operating in a "sold out" environment, with demand from AI-native firms and hyperscalers consistently outpacing available capacity. To solve this, the firm is launching nine new data center sites across the U.S., France, Israel, and the UK. Power capacity targets have been revised upward. The company now expects to have more than **3 gigawatts (GW)** of contracted power by the end of 2026, up from previous forecasts of **2.5 GW**. Currently, the firm is on track to have between **800 megawatts and 1 gigawatt** of connected power active by year-end. Strategic Moves and Market Reaction The company recently announced the acquisition of Tavily, a search infrastructure provider, to enhance its "agentic AI" capabilities. This move aims to provide a full-stack platform where enterprises can build and run autonomous AI agents with real-time web access. Despite the explosive growth, the market focused on the quarterly revenue miss and widening losses. Net loss from continuing operations for the quarter stood at **$249.6 million**, compared to **$122.9 million** a year prior. Following the report, shares were down approximately **3%** in volatile trading. Nebius continues to lean on its strategic partnerships with industry giants, including multi-billion dollar cloud deals with Microsoft and Meta, to secure its long-term revenue trajectory.

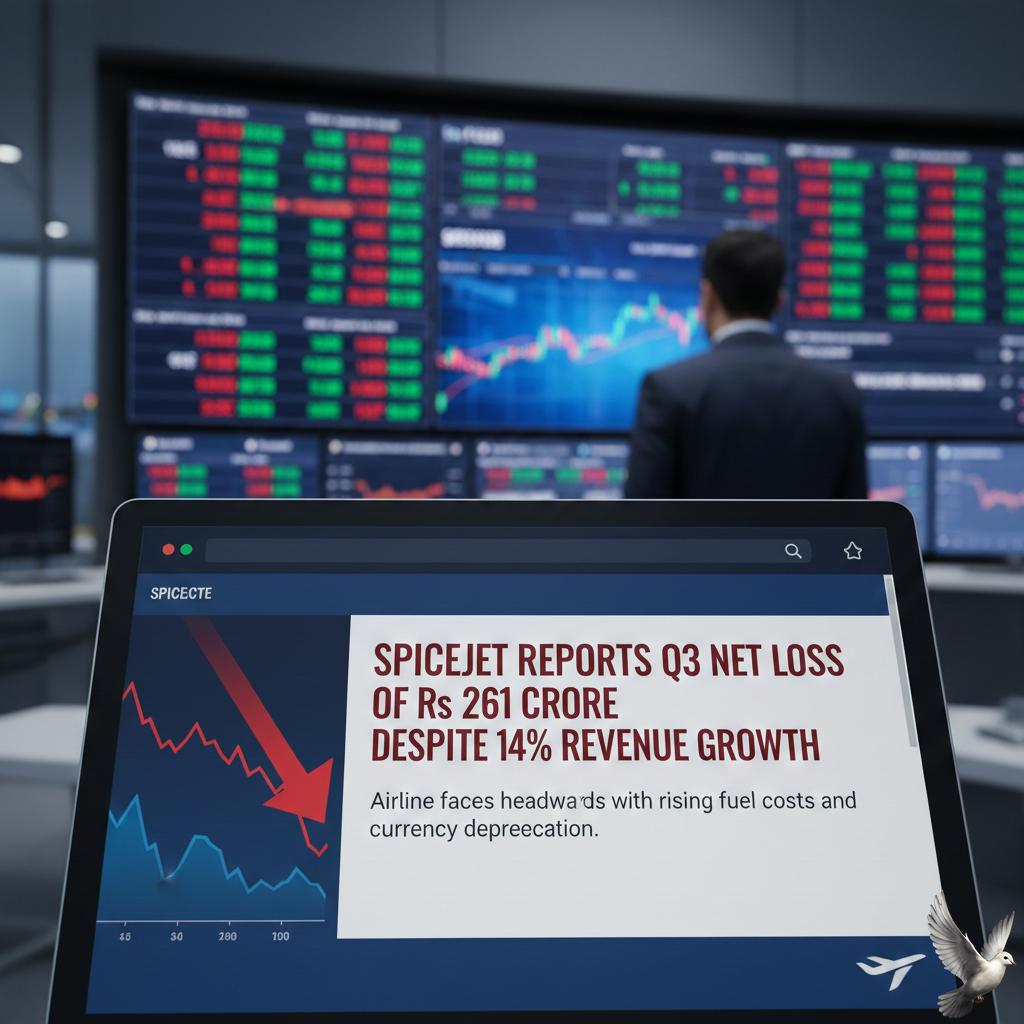

SpiceJet Reports Q3 Net Loss of Rs 261 Crore Despite 14% Revenue Growth

SpiceJet is undergoing a complex financial and operational restructuring as it attempts to move past a period of significant volatility and deep fiscal distress. While the carrier previously reported a consolidated net loss of 261.38 crore for a December-ended quarter, recent data indicates a push toward stabilization through aggressive fund-raising and debt settlement. The airline successfully secured a massive 3,000 crore capital infusion through a Qualified Institutional Placement (QIP) and an additional 500 crore from its promoter group. These funds have been critical in addressing long-standing liabilities, including the full repayment of 200 crore to Credit Suisse and the settlement of statutory dues such as Provident Fund and GST. A major milestone in its balance sheet cleanup was the restructuring of 442 crore in debt with Carlyle Aviation Partners. This deal converted a portion of the airline’s lease debt into equity and unlocked 740 crore in liquidity, providing the necessary cushion to bring grounded aircraft back into service. Operational capacity is scaling rapidly to capture growing domestic demand. SpiceJet aims to double its operational fleet to approximately 35–40 aircraft by the end of 2025. For the current winter schedule, the airline has significantly increased its daily operations to 250 flights, more than double its previous summer schedule. Despite these efforts, the airline faces a competitive market where its share recently fluctuated around 4.3%. For the quarter ending September 2025, the carrier reported a net loss of 635.42 crore, pressured by a weaker rupee, high maintenance costs for reinducting aircraft, and airspace restrictions. Market sentiment remains cautiously optimistic as credit agencies like Acuité and CRISIL have recently upgraded the airline's ratings to BB (Stable) and A4+, citing improved liquidity and the success of its restructuring initiatives. The stock currently trades around 20.40, reflecting the market's ongoing assessment of the carrier's ability to sustain its long-term recovery.

IHCL Reports Q3 Revenue of Rs 2,842 Crore and PAT of Rs 954 Crore

The Indian Hotels Company Limited (IHCL) has achieved a major milestone, reporting its fifteenth consecutive record-breaking quarter for the period ending December 31, 2025. The company demonstrated resilient operational strength with consolidated revenue rising 12% year-on-year to reach 2,900 crore. Profitability saw a significant surge during this period. Net profit (PAT) jumped 55% to 903 crore, supported by robust hotel performance and a one-time exceptional gain of 327 crore from the sale of a joint venture stake. Operating EBITDA reached 1,134 crore, maintaining a healthy margin of 39.1%. The hospitality giant continues to expand its footprint rapidly. The total portfolio has grown to 617 hotels, including 361 currently operational and a massive pipeline of 256 properties. Under its "Accelerate 2030" strategy, IHCL is aggressively diversifying into wellness and boutique leisure, recently acquiring controlling stakes in the Atmantan and Brij brands. New business verticals are proving to be high-growth engines. Revenue from segments like Ginger, Qmin, and amã Stays & Trails grew by 31%, while airline and institutional catering through TajSATS rose by 17%. The Ginger brand alone now features a portfolio of over 250 hotels, signaling a strong push into the mid-scale market. On the operational front, the domestic hotel sector is benefiting from high pricing power. Domestic Revenue Per Available Room (RevPAR) increased by 9% to approximately 13,800 per night. Demand remains particularly strong in major hubs, with Rajasthan seeing a 25% revenue jump and Delhi NCR growing by 8%. The company’s financial health remains a core strength. IHCL maintains a gross cash balance of 3,877 crore as of late 2025, providing ample liquidity for future greenfield and brownfield projects. Capital expenditure for the first nine months of the fiscal year stood at 750 crore, focused on key projects in Frankfurt, Varanasi, and Mumbai. As of February 12, 2026, IHCL stock was trading around 704 on the NSE. While the stock has seen some recent cooling from its 52-week high of 858, the long-term outlook remains supported by a 14.3 million-member loyalty ecosystem and a capital-light growth model, where 94% of the current pipeline is based on management contracts rather than asset ownership.

Muthoot Finance Updates FY26 Growth Guidance Following Quarterly Profit Increase

Muthoot Finance has significantly upgraded its growth outlook for FY26, following a period of exceptional financial performance and favorable market shifts. **Growth Guidance and Strategic Outlook** The company has raised its annual growth forecast to a range of 44%–45% for FY26. This is a substantial jump from the previously revised guidance of 30%–35%. Management attributes this optimism to a surge in gold loan demand and a more supportive regulatory environment. **Q3 Performance Highlights** Standalone net profit for the third quarter nearly doubled, reaching 2,656 crore compared to 1,363 crore in the same period last year. This surge was primarily driven by a 64% increase in total income, which climbed to 7,263 crore. Profitability was further bolstered by a 47% reduction in provisions, which fell to 111 crore. **Market Value and Assets** Assets Under Management (AUM) reached 1.48 lakh crore, representing a robust 51% year-on-year growth. Gold loans specifically accounted for 1.40 lakh crore of this total. The market capitalization of the firm currently stands at approximately 1,63,275 crore. **Branch Expansion and Regulatory Support** Muthoot Finance plans to open 150 to 200 new branches in the coming year, exceeding its current annual target by 50 units. This expansion is supported by new Reserve Bank of India (RBI) norms that remove the requirement for prior approval for branch expansion for lenders with over 1,000 branches. **Gold Price Impact** A historic rally in gold prices, which saw domestic rates hit a 1.6 lakh milestone per 10 grams in February 2026, has fundamentally improved borrowing capacity. Higher collateral values have increased Loan-to-Value (LTV) outputs, allowing customers to access more capital with the same quantity of gold jewelry. **Stock Market Performance** The share price has reflected this momentum, trading near 4,067 as of February 12, 2026. The stock has seen a 52-week high of 4,150, marking a significant recovery and growth trajectory over the past year. **Subsidiary Performance** The company's microfinance arm, Belstar Microfinance, also returned to profitability in Q3 with a net profit of 51 crore, following losses in the first two quarters of the fiscal year. This highlights a broader recovery across the company's diversified lending segments.

RBI Swaps FY27 Bonds for 2040 Securities in Government Debt Exchange

The Reserve Bank of India (RBI) has executed a significant debt management maneuver by completing a bond switch operation with the central government. In this strategic move, the government bought back securities worth **755.04 billion rupees** ($8.34 billion) that were scheduled to mature in the 2026-27 fiscal year. To replace these short-term obligations, the RBI issued longer-dated **2040 securities** totaling **694.36 billion rupees**. The new 8.30% bonds were issued at a price of **110.45 rupees**, while the buyback prices for the shorter-term papers ranged between **100.28 and 102.46 rupees**. This "switch" is designed to ease immediate redemption pressures as the government prepares for a massive borrowing program. New Delhi has set a record gross borrowing target of **17.2 trillion rupees** for the upcoming fiscal year, a **17% increase** over the current year’s 14.61 trillion rupees. By pushing maturities further into the future, officials aim to prevent a surge in yields that could be triggered by such heavy debt supply. Market conditions remain cautious following the RBI’s February monetary policy meeting. The central bank opted to keep the repo rate unchanged at **5.25%**, maintaining a "neutral" stance. This decision came as a surprise to some traders who had hoped for a rate cut to support the heavy bond pipeline. Current indicators show the 10-year benchmark bond yield hovering around **6.69% to 6.72%**. While yields cooled slightly this week, they remain sensitive to persistent supply pressure from both federal and state government auctions. Analysts expect the 10-year yield to stay within a range of **6.60% to 6.80%** in the near term. On the macroeconomic front, the RBI has marginally raised its GDP growth forecast for the current fiscal year to **7.4%**. Inflation projections have also been nudged up to **2.1%**, primarily due to a sharp rally in gold and silver prices which has impacted core inflation. The central bank continues to manage banking system liquidity aggressively. It recently injected over **2 trillion rupees** through a combination of open market operations, foreign exchange swaps, and repo auctions. These measures are intended to ensure that despite record borrowing, the financial system remains stable and capable of supporting productive economic sectors.

Shriram Finance and Max Health Projected for Up to 13% Near-Term Gains

Market Overview The Indian equity market concluded the session on February 12, 2026, with the Nifty 50 ending a four-day winning streak. The index declined by **146.65 points**, or **0.57%**, to settle at **25,807.20**. Despite the intraday volatility that saw a low of **25,752.40**, the benchmark managed to hold above its **20-day moving average**, currently tracked near **25,595**, sustaining the broader recovery narrative. The Sensex mirrored this downward movement, shedding **558.72 points** to close at **83,674.92**. Market sentiment was weighed down by a significant sell-off in the technology sector, while the India VIX rose by **1.52%** to **11.73**, signaling a slight increase in trader anxiety. Sector Performance and Tech Drag The IT sector faced intense pressure as the Nifty IT index plunged **5.51%** to close at **33,160.20**. Investor caution spiked following the launch of new competitive products from global AI firms, which raised concerns over the traditional business models of domestic software giants. Top losers in the space included Tech Mahindra, which dropped **6.40%**, followed by Infosys at **5.97%** and TCS at **5.77%**. Conversely, the Financial Services and Metals sectors showed resilience. Bajaj Finance led the gainers with a **3.31%** rise, while Shriram Finance advanced **2.48%** to reach a new 52-week high of **1,069.50**. Technical Levels and Outlook Technical indicators suggest the Nifty faces immediate resistance at the psychological **26,000** mark. Derivatives data indicates the highest Open Interest in Call options remains at this level. On the downside, immediate support is established at **25,700**, with a more crucial support zone ranging between **25,500** and **25,650**. The market is also processing fresh economic data, as India’s January retail inflation was reported at a lower-than-expected **2.75%** under a revised base year. This cooling inflation may provide a cushion against further aggressive downside, keeping the medium-term outlook cautiously optimistic. Tactical Stock Opportunities **Shriram Finance** The stock has demonstrated strong momentum, currently trading above all major moving averages. It recently hit a 52-week peak of **1,069.50** on the back of nine consecutive quarters of positive results. With a record quarterly net profit of **2,529.67 crore**, analysts see further upside potential as institutional holding remains high at over **68%**. **Max Healthcare** Max Healthcare remains a tactical focus in the healthcare services space. The stock recently witnessed a surge in volume, closing near **1,055.50**. While valuations are considered premium at a P/E of approximately **72**, the company reported a **35.2%** year-on-year growth in net profit for the December quarter, reaching **187 crore**. Support for the stock is currently identified around the **1,020** level.

US Weekly Jobless Claims Fall Less Than Anticipated Amid Labor Market Stabilization

US Labor Market Report: February 2026 The United States labor market is showing renewed signs of stabilization in early **2026**, moving past the significant "soft patch" that defined much of the previous year. Recent data indicates a shift away from the stagnant "low hire, low fire" cycle toward a more balanced environment. Initial applications for unemployment benefits fell to **227,000** for the week ending **February 7, 2026**. This represented a decrease of **5,000** from the previous week’s revised level of **232,000**. While the decline was slightly less than the **222,000** claims expected by economists, the trend suggests that employers are largely maintaining current staffing levels despite broader economic uncertainties. The **4-week** moving average, which provides a clearer view of the trend by smoothing out weekly volatility, rose to **219,500**. This reflects a slight uptick from January lows but remains well within a range consistent with a healthy economy. Key Employment Indicators * **Unemployment Rate:** The national jobless rate currently stands at **4.3%**, a slight improvement from the **4.4%** recorded in **December 2025**. * **Monthly Job Gains:** Total nonfarm payrolls surged by **130,000** in **January 2026**, significantly outperforming the forecast of **70,000**. * **Continuing Claims:** The number of people already receiving benefits rose by **21,000** to **1.862 million**. While this is an increase, it remains below the post-pandemic highs of **2.0 million** seen last fall. * **Labor Participation:** The participation rate edged up to **62.5%**, signaling that more Americans are entering the workforce to seek employment. Sector Performance and Economic Outlook Job growth in the new year has been heavily concentrated in specific sectors. **Healthcare** and **social assistance** led the expansion, adding **124,000** jobs combined in the latest monthly report. **Construction** also showed resilience with **33,000** new positions. Conversely, the **federal government** sector saw a decline of **42,000** jobs, and **manufacturing** remains stagnant due to trade-related uncertainties. Earnings continue to rise, with average hourly pay increasing by **0.4%** month-over-month. On an annual basis, wages are up **3.7%**, providing a necessary cushion for consumer spending. Economists view these figures as evidence that the labor market has found its footing. The combination of falling unemployment and stronger-than-anticipated job creation has led markets to adjust expectations for monetary policy, with many now anticipating that interest rates will remain steady through the first half of the year.

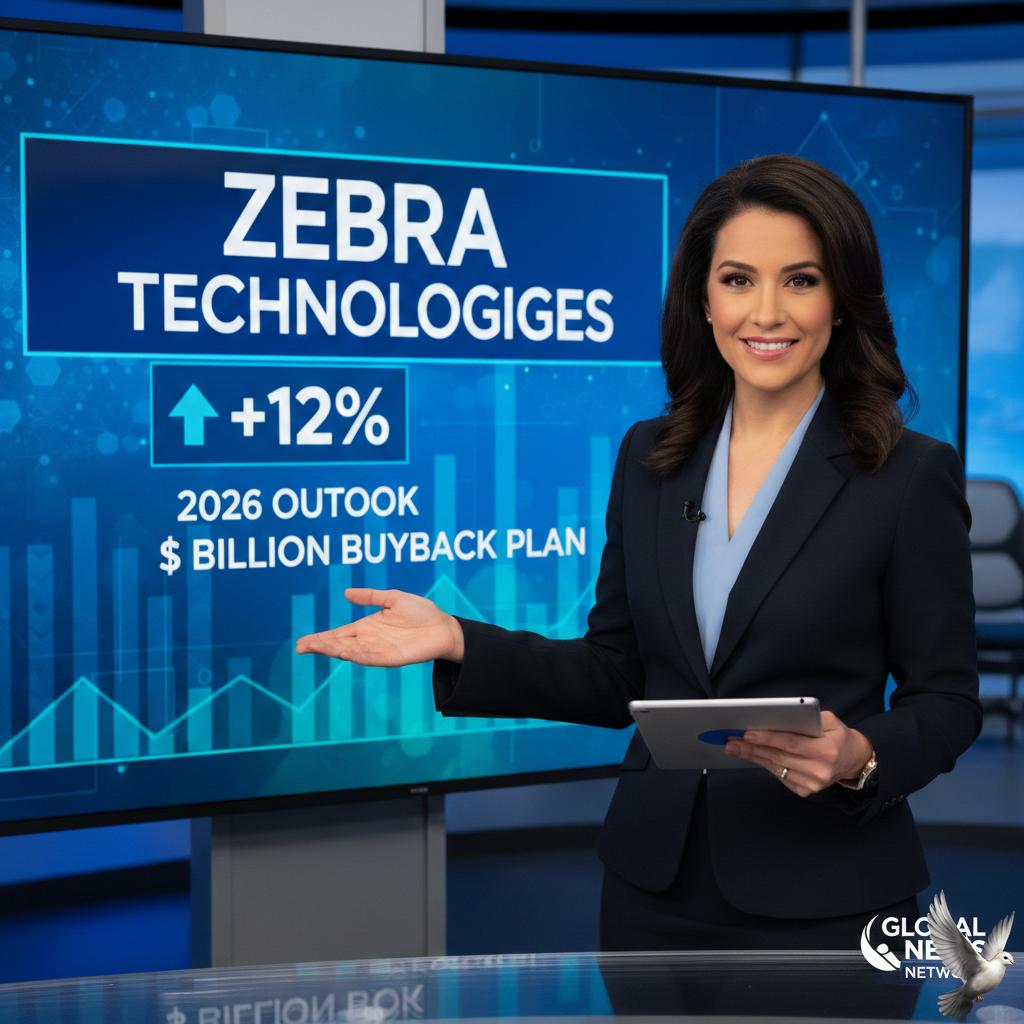

Zebra Technologies Shares Rise on 2026 Outlook and $1 Billion Buyback Plan

Zebra Technologies (ZBRA) experienced a significant market surge on February 12, 2026, with shares climbing more than 17% to reach levels near $296.38. This rally follows a fourth-quarter earnings report that showcased robust revenue growth and an aggressive outlook for the 2026 fiscal year. The company reported fourth-quarter revenue of $1.48 billion, representing a 10.6% increase year-over-year. Adjusted earnings per share reached $4.33, while adjusted EBITDA rose 10.5% to $326 million. These results reflect a recovery in demand for enterprise hardware, particularly in the logistics and retail sectors. For the full year 2026, Zebra has issued guidance that exceeds market expectations. The company anticipates sales growth between 9% and 13%, supported by a healthy order backlog and the integration of recent acquisitions like Elo Touch. Management expects adjusted earnings per share to fall between $17.70 and $18.30 for the year. Strategic financial moves have further bolstered investor confidence. The Board of Directors authorized a new $1 billion share repurchase program, adding to the company's existing buyback capacity. Zebra also projects generating at least $900 million in free cash flow throughout 2026, signaling a strong liquid position. Operationally, the "Connected Frontline" segment has emerged as a key growth driver, posting a 3.6% organic increase. While the company recorded $76 million in restructuring charges related to productivity initiatives, the resulting leaner structure is expected to maintain an EBITDA margin of approximately 22% for the coming year. Sector-wide trends are favoring Zebra’s core portfolio. The 2D barcode reader market is projected to reach $9.72 billion in 2026, driven by a shift toward AI-enabled decoding and mandatory traceability in global supply chains. Zebra’s focus on "Physical AI"—integrating intelligence into handheld scanners and mobile computers—aligns with broader enterprise trends for 2026. Despite broader macroeconomic pressures, the company’s first-quarter 2026 outlook remains optimistic, with projected sales growth between 11% and 15%. This guidance has prompted several analysts to maintain or raise price targets, citing Zebra's leadership in digitizing and automating high-value workflows.

LSEG to Launch Blockchain-Based Digital Asset Settlement Platform

The London Stock Exchange Group (LSEG) has officially announced the development of its Digital Securities Depository (DSD), a transformative on-chain settlement service designed specifically for institutional investors. This move marks a pivotal shift as the 325-year-old exchange operator aims to bridge the gap between traditional and digital securities markets through a unified, blockchain-enabled infrastructure. As of February 12, 2026, the project is advancing under the UK’s Digital Securities Sandbox (DSS) regulatory framework. The DSD is engineered to facilitate the end-to-end trading and settlement of tokenized assets, including bonds, equities, and private market instruments. By operating across multiple blockchain networks while maintaining full interoperability with existing settlement systems, LSEG aims to eliminate the friction typically found between digital assets and legacy financial rails. Market conditions have accelerated this strategic pivot. LSEG’s stock rose 0.9% on the day of the announcement, trading near 7,520 GBX. This recovery follows a challenging period where shares faced a 35% decline over the previous year, partly driven by broader volatility in software stocks. The launch of the DSD is seen as a key response to calls for modernization and improved performance from major stakeholders, including activist investor Elliott Management. The technical foundation for this initiative is bolstered by the recently launched Digital Settlement House (DiSH). This platform enables 24/7 instantaneous settlement using tokenized commercial bank deposits across multiple currencies. Unlike experimental models of the past, this system allows participants to maintain ownership of deposits at commercial banks within the network, providing a "real cash leg" for on-chain transactions. LSEG is collaborating with a strategic partner group and top-tier financial institutions—including Barclays, Goldman Sachs, and HSBC—to ensure the depository meets the rigorous demands of institutional liquidity and risk management. A recent partnership with Apex Group also highlights plans to tokenize private funds, with live distribution expected in the first half of 2026. This evolution signifies more than just a technological upgrade; it represents the institutionalization of the "machine economy." By integrating programmable liquidity and atomic settlement, LSEG is positioning itself to handle a market where digital assets are no longer fringe investments but core components of the global financial system. The first phase of live deliverables for the DSD is targeted for 2026, pending final regulatory approvals.

US Stock Market Fluctuates Following Jobs and Economic Data Releases

Wall Street’s primary indices showed resilient growth on Thursday, February 12, 2026, as investors processed a combination of strong labor market data and a high-volume corporate earnings season. Market sentiment remains optimistic following reports that the U.S. economy added 130,000 jobs in January, significantly outperforming the 75,000 forecast by economists. The Dow Jones Industrial Average climbed to 50,336.68, marking a 0.43% gain. The S&P 500 rose 0.21% to reach 6,955.97, while the Nasdaq Composite hovered near 23,063.37. Volatility, as measured by the VIX, dipped by 2.66% to 17.18, signaling a decrease in investor anxiety despite the rapid pace of financial reporting. Labor market indicators have provided a major tailwind. The national unemployment rate fell to 4.3% in January, down from 4.4% in December. This decline, coupled with a solid 0.4% rise in average hourly wages, suggests that the U.S. consumer remains on firm footing even as the broader market transitions out of the stagnant hiring trends seen in late 2025. Earnings results were mixed but featured standout performances in specific sectors. Micron Technology shares surged nearly 4% due to rising memory-chip prices, highlighting the continued strength of hardware infrastructure. In the utility sector, PG&E Corporation reported 2025 core earnings of $1.50 per share, up from $1.36 the previous year, while Exelon reported adjusted operating earnings of $0.59 per share for the fourth quarter. Conversely, some legacy tech and industrial players faced pressure. Cisco Systems saw its stock tumble 7% after a cautious revenue forecast, despite beating immediate profit estimates. In the consumer space, Crocs outperformed expectations with annual revenue exceeding $4 billion, while US Foods reported quarterly sales of $9.8 billion, a 3.3% year-over-year increase that slightly missed analyst targets. In the commodities and treasury markets, the 10-year Treasury yield eased to 4.15% as traders looked ahead to upcoming inflation data. Crude oil stabilized near $64.31 per barrel, and Gold traded at approximately $5,073.78. The shift in investor focus toward individual corporate fundamentals, rather than broad economic fears, underscores a maturing market cycle. While the AI-driven trade continues to induce localized volatility, the broader stabilization of the job market and consistent double-digit earnings growth across the S&P 500 are providing the necessary support for the current upward trajectory.

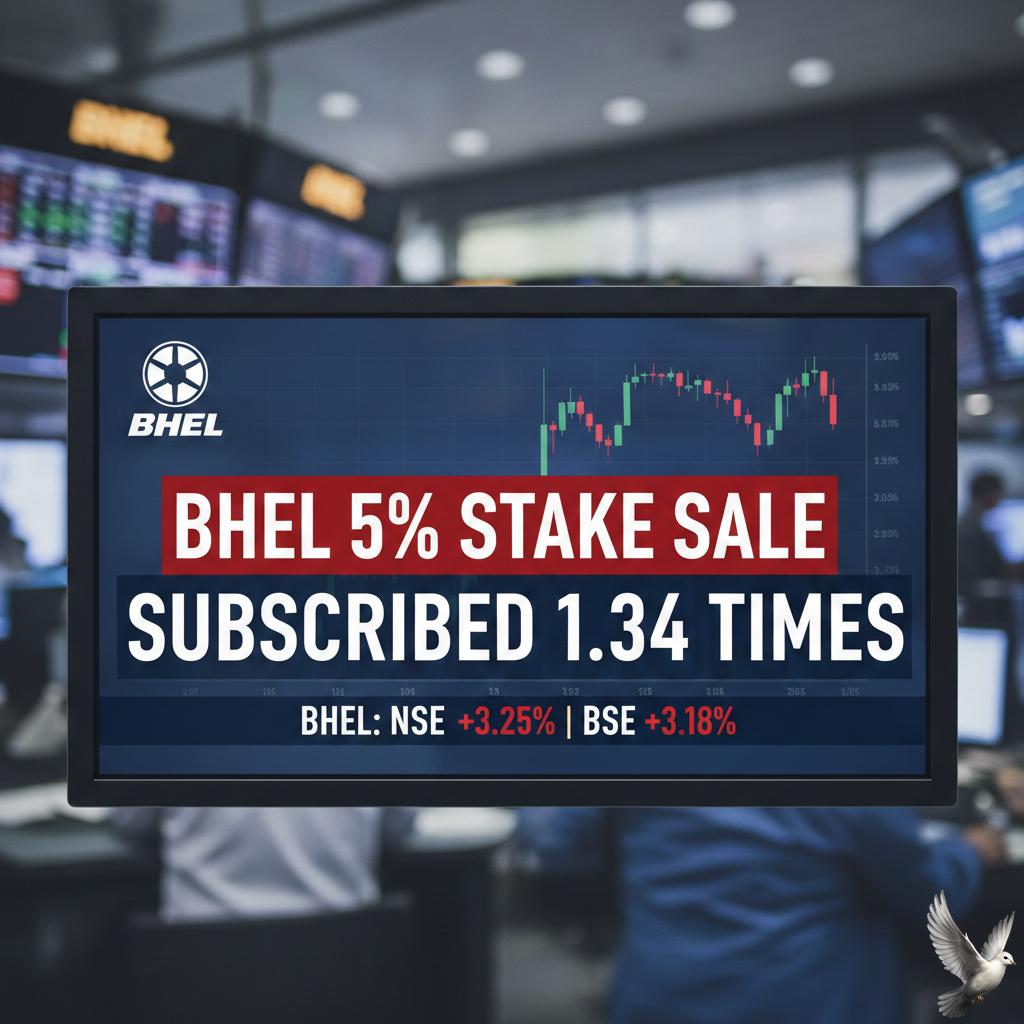

BHEL 5% Stake Sale Subscribed 1.34 Times

The government’s strategic divestment in Bharat Heavy Electricals Limited (BHEL) successfully concluded this week, marking a significant milestone in the current fiscal year's disinvestment program. The Offer for Sale (OFS) for a **5 per cent** stake saw robust participation, ending with an over-subscription of **1.34 times**. The transaction was structured with a base offer of **3 per cent**, which the government expanded by exercising a green-shoe option for an additional **2 per cent** due to high demand. Retail and institutional investors both showed strong interest, despite a volatile market environment. The floor price for the sale was set at **₹254 per share**, representing a tactical discount of approximately **8 per cent** from the pre-announcement closing price. As of February 12, 2026, the stock has stabilized near the **₹260** mark, reflecting a market capitalization of approximately **₹96,122 crore**. The government's total proceeds from this stake sale are estimated at over **₹4,422 crore**. This capital infusion supports the broader fiscal goal of increasing public shareholding in Central Public Sector Enterprises (CPSEs) while enhancing the stock's liquidity and free float in the secondary market. BHEL’s operational recovery has provided a supportive backdrop for this divestment. The company recently reported a massive surge in profitability for the December 2025 quarter, with net profit jumping nearly **190 per cent** year-on-year to **₹390.40 crore**. Revenue from operations also rose by **30.4 per cent**, reaching **₹8,473.10 crore**. Investor confidence remains anchored by a record-high order book, which currently stands at over **₹2.22 lakh crore**. This provides revenue visibility for the next **3 to 4 years**, driven primarily by the power sector, which accounts for **80 per cent** of the total mandates. Recent project wins include major EPC contracts for thermal power plants and supply orders for Vande Bharat sleeper train transformers. Furthermore, the company is positioned as a key player in India’s energy transition, with a strategic focus on scaling nuclear power capacity from **8.8 GW** to a target of **100 GW** by 2047. While the stock has seen a temporary price adjustment toward the OFS floor price, the long-term outlook is supported by improving operating leverage and the accelerating domestic manufacturing cycle. BHEL continues to hold a dominant **90 per cent** market share in the domestic thermal power equipment segment.

Bharat Forge Q3 Net Profit Increases 28% to Rs 273 Crore

Bharat Forge has delivered a resilient performance for the third quarter ending December 2025, reporting a **28.2% year-on-year surge** in consolidated net profit to **Rs 273 crore**. The company’s revenue from operations soared by **25%**, reaching **Rs 4,343 crore**, significantly outperforming street estimates of **Rs 4,045 crore**. This growth was primarily fueled by a massive scale-up in the defense sector and steady domestic automotive demand. **Defense and Industrial Performance** The defense segment has emerged as a major growth engine, with revenue jumping **102%** to **Rs 682 crore**. The company’s total defense order book now stands at a robust **Rs 11,130 crore**. Key highlights include a new contract with the Ministry of Defence for over **250,000 CQB Carbines**. Industrial exports also provided a cushion, growing **11%** sequentially to offset fluctuations in other areas. **Market Reaction and Valuation** Following the results, Bharat Forge shares witnessed strong buying interest on February 12, 2026, climbing over **3%** to trade around **Rs 1,731**. The stock has maintained a powerful trajectory, currently trading near its 52-week high of **Rs 1,757**, up from a low of **Rs 919**. The company’s market capitalization has crossed **Rs 82,500 crore**, reflecting investor confidence in its diversification strategy. **Margins and Costs** While top-line growth was strong, EBITDA margins saw a slight compression to **17.3%**, down from **18%** a year ago. This softening was attributed to: - Persistent de-stocking in the North American commercial vehicle market. - Higher input costs and increased material consumption. - An exceptional loss of **Rs 56 crore** due to updated labor codes affecting gratuity and leave liabilities. **Shareholder Rewards** The board has declared an interim dividend of **Rs 2 per share** (100% on a face value of Rs 2). The record date for this payout is fixed for **February 18, 2026**, with payments expected by mid-March. **Management Outlook** Leadership remains optimistic, stating that the "worst is behind" regarding global export headwinds. Management expects high double-digit top-line growth through 2026 and 2027, driven by the commencement of major defense programs and a recovery in international automotive markets.

Coal India Q3 Net Profit Declines 16% YoY to Rs 7,166 Crore; Dividend of Rs 5.5 Declared

Coal India Limited has reported a decline in its consolidated net profit for the third quarter of the 2025–26 financial year. The state-owned mining giant posted a net profit of 7,166 crore, representing a 16% drop compared to the same period in the previous year. The dip in profitability is largely attributed to a mismatch between record production levels and actual market offtake. While the company has ramped up its output to meet national energy security goals, rising operational expenses and a slight softening in sales volume have impacted the bottom line. Total expenses for the quarter rose as the company faced higher contractual costs and employee-related provisions. Despite the lower profit figures, the Board of Directors has demonstrated a strong commitment to shareholder returns. The company has declared a third interim dividend of 5.50 per share for the 2026 financial year. This follows a consistent payout strategy, including a second interim dividend of 10.25 per share earlier in the cycle. In the stock market, Coal India’s shares are currently trading around 419.15. The stock has seen a minor correction of approximately 1.03% in recent sessions as investors digest the quarterly performance. The company maintains a healthy dividend yield of 6.32% and a market capitalization of approximately 2.58 lakh crore, reflecting its dominant position in India’s energy landscape. Operational data shows that Coal India continues to account for over 80% of the country’s coal output. For the current financial year, production targets remain aggressive at 875 million tonnes. However, the company is managing a significant pithead inventory of over 80 million tonnes, which acts as a buffer for the power sector during peak demand periods but also adds to carrying costs. The broader coal sector in India is navigating a complex transition. While the government is pushing for increased thermal power generation to support industrial growth—with a goal of reaching 1.5 billion tons of coal volume by 2030—there is also a simultaneous shift toward renewable energy. For now, coal remains the backbone of the grid, contributing to nearly 75% of total electricity generation. Investors are keeping a close watch on the company’s ability to manage costs and improve grade conformity. The recent listing of its subsidiary, Bharat Coking Coal, also signals a strategic move toward unlocking value within its different mining arms. Looking ahead, the focus remains on enhancing the evacuation infrastructure to ensure that high production levels translate directly into higher sales revenue.

NSE Appoints Rothschild as Independent Advisor for IPO

The National Stock Exchange of India (NSE) has reached a critical milestone in its decade-long journey toward a public listing. On Thursday, February 12, 2026, the exchange officially appointed Rothschild & Co as its independent advisor. This appointment is a strategic move to streamline the highly anticipated Initial Public Offering (IPO). Rothschild will lead the selection of investment bankers, legal counsel, and other key intermediaries. Their role also includes managing stakeholder communication and ensuring information parity as the exchange prepares for what could be India’s largest-ever market debut. Valuation and Market Impact The NSE is currently commanding a massive presence in the unlisted market. As of February 2026, the exchange is valued at approximately **₹5.27 lakh crore** ($63 billion). Unlisted shares are currently trading near **₹2,130** per share, reflecting strong investor confidence. The IPO is expected to be an Offer for Sale (OFS), where existing shareholders plan to divest between **4% and 4.5%** of their equity. Based on current valuations, this could raise roughly **₹22,500 crore** ($2.5 billion). Major institutional shareholders poised to participate in the stake sale include: * **Life Insurance Corporation of India (LIC):** 10.7% stake * **Aranda Investments (Temasek):** 4.5% stake * **State Bank of India (SBI):** 3.23% stake * **Stock Holding Corporation of India:** ~4% stake Regulatory Momentum The path to listing cleared significantly following a No-Objection Certificate (NOC) from the Securities and Exchange Board of India (SEBI) on January 30, 2026. This followed years of delay due to the co-location case, which the exchange recently resolved through a **₹1,388 crore** settlement. To manage the transition, the NSE board has reconstituted its IPO Committee. The group is chaired by non-independent director Tablesh Pandey and includes CEO Ashishkumar Chauhan. Estimates suggest the shares could hit the primary market within the next **7 to 8 months**. Financial Performance The exchange continues to demonstrate robust operational growth. In the latest financial reports for FY2025, the NSE reported: * **Revenue from Operations:** ₹17,140 crore (up 28% YoY) * **Profit After Tax:** ₹12,187 crore (up 27% YoY) * **Operating Profit Margin:** 75% As the world's largest derivatives exchange by volume, the NSE services over **11.3 crore** unique investors. Its listing comes at a time of market strength, with the Nifty 50 recently closing at **25,935**, hovering just below the psychological **26,000** milestone.

UK Selects HSBC as Platform Provider for Digital Bond Pilot

**UK Market Brief: Digital Gilt Issuance & Strategic Innovation** The UK government has officially selected HSBC to lead its landmark pilot for the issuance of tokenised government bonds. This initiative, known as the Digital Gilt Instrument (DIGIT) pilot, marks a major step in the nation’s Wholesale Financial Markets Digital Strategy. By choosing a blockchain-based platform, Britain has positioned itself at the forefront of the G7 nations in the race to modernise sovereign debt infrastructure. The pilot will utilise the HSBC Orion platform, a distributed ledger technology (DLT) system that has already facilitated over $3.5 billion in digital bond issuances globally. The government’s objective is to test how DLT can streamline the entire lifecycle of a gilt—from issuance to settlement—to enhance transparency and reduce operational costs for financial institutions. **Key Market Data & Indicators** The UK gilt market enters 2026 following a period of significant yield volatility. Throughout 2025, the 10-year gilt yield remained largely within a range of 4.45% to 4.75%. Recent forecasts suggest a gradual easing of interest rates, with the Bank of England’s base rate expected to fall to 3.25% by mid-2026. Current projections indicate that UK gilts offer an annualised return of 5.0% to 6.0% over the next decade. These returns are currently viewed as more attractive than many other developed government bonds, including US Treasuries, which have lower projected Sharpe ratios. **Strategic Impact & Technology** The DIGIT pilot is designed to be digitally native and short-dated. It will operate within the Digital Securities Sandbox (DSS), a regulated environment managed by the Financial Conduct Authority (FCA). This independence from the main debt management programme allows the Treasury to experiment with on-chain settlement without disrupting broader fiscal stability. Beyond the technology, the government has appointed the law firm Ashurst LLP to provide legal services, ensuring the pilot addresses the complex regulatory and tax treatments required for digital assets. The success of this trial is expected to catalyse the development of wider UK-based DLT infrastructure. **Sector Outlook** While tokenised debt still represents a small fraction of the global market, momentum is building. HSBC's platform has previously handled the European Investment Bank’s first digital sterling bond and the Hong Kong government’s $1.3 billion green bond, the world’s largest digital issuance to date. The move signals a clear intent to keep the UK at the centre of global capital markets. As inflation begins to stabilise and interest rate cuts become more likely in 2026, the introduction of more efficient, faster-settling digital instruments could drive higher liquidity in both primary and secondary bond markets.