Bullish News

Collection

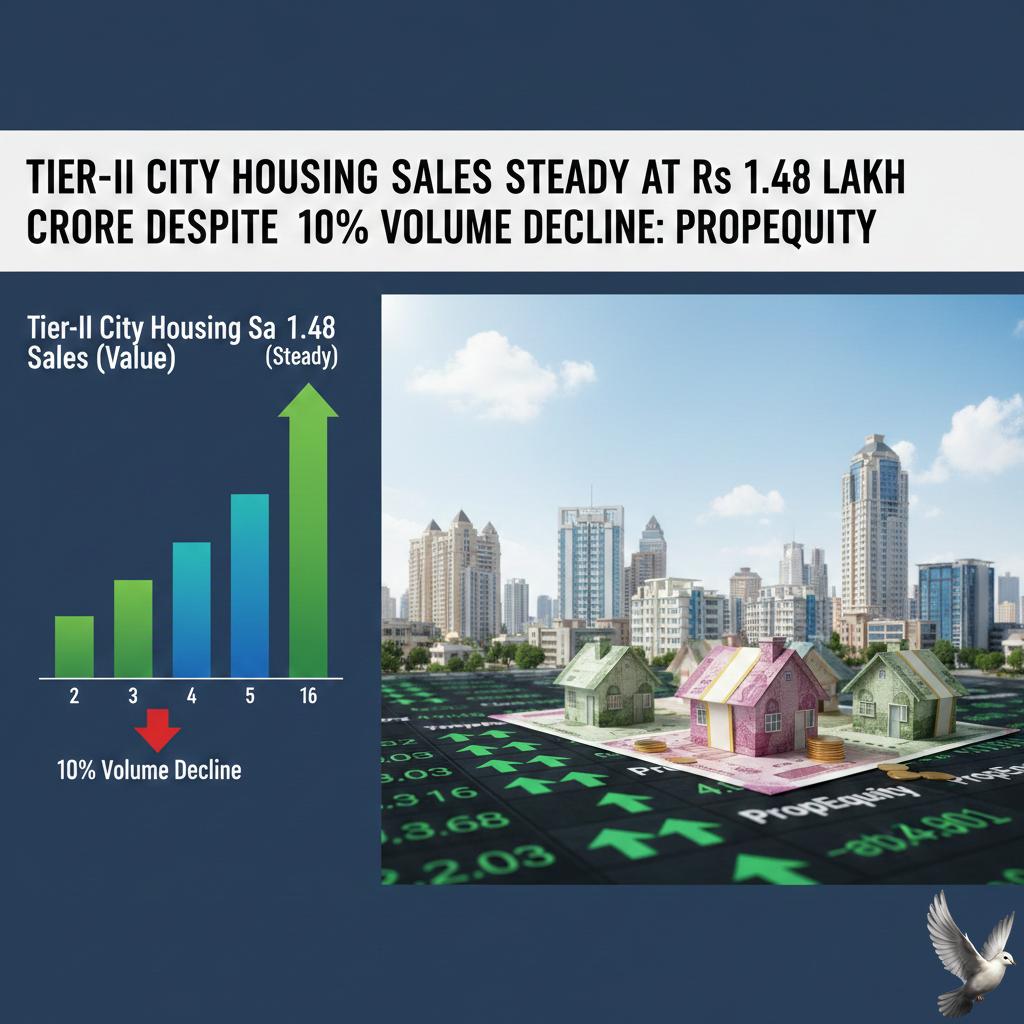

Tier-II City Housing Sales Steady at Rs 1.48 Lakh Crore Despite 10% Volume Decline: PropEquity

Housing sales across India’s top 15 tier-II cities experienced a 10 per cent decline in volume during 2025, with total transactions falling to 1,56,181 units. Despite this drop in the number of homes sold, the market remained resilient in value terms, holding steady at 1.48 lakh crore. This trend highlights a significant shift in buyer behavior and market dynamics as secondary urban centers begin to mirror the premiumization seen in major metropolitan hubs. The stagnation in sales value amidst falling volumes is primarily driven by a surge in property prices. Average housing costs have risen due to escalating land acquisition expenses and a 40 per cent increase in construction costs over the last five years. Labor costs alone have jumped nearly 150 per cent since 2019, while essential materials like steel and cement have seen price hikes of up to 57 per cent. A critical factor in the volume decline is the shrinking supply of affordable housing. Projects priced below 1 crore, which historically anchored the tier-II market, saw a 15 per cent drop in sales volume. The market share for this segment fell from 77 per cent in 2024 to 72 per cent in 2025. Conversely, the premium segment is thriving. Homes priced above 1 crore witnessed a 9 per cent growth in sales, now accounting for 28 per cent of the total market. City-wise performance shows a stark contrast across regions. Visakhapatnam recorded the steepest decline in sales at 38 per cent, followed by Bhubaneswar at 25 per cent and Vadodara at 19 per cent. Ahmedabad remains the largest contributor to the tier-II landscape, representing 33 per cent of total sales with over 51,000 units sold. Notably, Mohali and Lucknow bucked the broader downward trend, posting sales growth of 34 per cent and 6 per cent, respectively. The investment outlook is supported by a more favorable interest rate environment. The Reserve Bank of India has actively reduced the repo rate throughout 2025, bringing it down to 5.25 per cent as of December. These cuts have started to lower borrowing costs, with home loan rates from major banks now hovering around 7.90 per cent to 8.25 per cent. Looking ahead, infrastructure development remains a primary catalyst for growth. Government initiatives like the Smart Cities Mission and the expansion of industrial corridors are enhancing the liveability of these cities. Ahmedabad is already being positioned for a transition to tier-I status by 2026 due to its massive scale of new launches and absorption. While affordability pressures are mounting, the move toward lifestyle-led upgrades and integrated community living is expected to define the next phase of the residential market.

Hindalco Q3 Net Profit Falls 45% YoY to Rs 2,049 Crore as Revenue Increases 14%

Hindalco Industries, the flagship metal company of the Aditya Birla Group, has released its financial results for the quarter ending December 31, 2025 (Q3 FY26), showing a substantial recovery in profitability. The company reported a consolidated Net Profit of 2,049 crore, representing a 45% increase compared to the previous year. This surge in profit comes on the back of resilient operational performance across its global and domestic businesses. Consolidated Revenue for the quarter rose by 14% year-on-year to reach 66,521 crore. The company's consolidated EBITDA stood at 8,762 crore, a 6% increase from the same period last year. In the Indian market, Hindalco’s operations delivered significant growth. The India Business saw its revenue climb 21% to 29,858 crore, while its Net Profit jumped 24% to 3,581 crore. The Copper segment was a standout contributor to the top line, with revenue growing 33% to 18,233 crore, driven by robust domestic demand and higher volumes. Novelis, Hindalco’s U.S.-based subsidiary and the global leader in aluminum rolling and recycling, reported revenue of $36.6 billion for the quarter, up 9%. Despite global macro-economic pressures and higher scrap costs, Novelis maintained a steady performance with an Adjusted EBITDA of $3.1 billion, excluding one-time impacts. As of February 12, 2026, Hindalco’s stock is trading at approximately 961.80 on the National Stock Exchange. The company’s market capitalization remains strong at roughly 2,17,015 crore. Over the last year, the share price has seen a significant appreciation of 62.11%, reflecting investor confidence in its strategic growth projects and cost leadership. The global aluminum market continues to face a complex environment. On the London Metal Exchange (LME), aluminum prices have shown volatility, recently trading in the 2,800 to 2,900 USD per tonne range. Supply constraints in China and high energy costs in Europe are expected to keep prices elevated, with some analysts forecasting a test of the 3,000 USD mark in the near term. Hindalco remains focused on its expansion strategy, with key projects in alumina refining, aluminum smelting, and copper expansion on track. The company’s Net Debt to EBITDA ratio remains disciplined at 1.33x, providing a solid foundation for future capital expenditure and sustainability initiatives.

Experion Developers to Invest 1,500 Crore in Noida Housing Project

Experion Developers is expanding its footprint in the National Capital Region with a significant investment of 1,500 crore to develop Saatori, an ultra-luxury housing project in Noida’s Sector 151. The project is spread across 5 acres and will feature approximately 450 premium units. This development follows the company’s recent launch of Experion Elements in Sector 45, where 3 and 4 BHK residences are currently commanding prices between 5.74 crore and 7.59 crore. The total built-up area for the new Sector 151 venture is estimated at 16 lakh square feet, with a targeted completion timeline of four to five years. The Noida real estate market is currently witnessing a robust upward cycle, with average property rates in 2026 reaching approximately 12,773 per square foot. High-demand sectors like Sector 150 and the Expressway corridors are seeing even higher valuations, frequently ranging between 10,000 and 15,000 per square foot. Strategic infrastructure remains the primary catalyst for these valuations. The Noida International Airport at Jewar is nearing operational readiness, which experts project will trigger a 15% to 35% growth in property values across nearby sectors. Additionally, the expansion of the Noida Metro into Greater Noida West and upgrades to the FNG Expressway are significantly reducing commute times, further fueling residential demand. Market data for early 2026 indicates a clear shift toward premiumization. While overall housing sales volumes in the Delhi-NCR region saw a 13% dip last year, the luxury segment remains resilient. Homes priced above 1 crore now account for 28% of total market share, up from 23% in 2024. This trend highlights a maturing market where buyers are increasingly prioritizing low-density layouts, wellness-centric amenities, and sustainable architecture. Rental yields in the region have also seen a sharp uptick. Prime residential corridors in Noida recorded a 19% annual appreciation in rents throughout 2025, driven by return-to-office mandates and a limited supply of high-end inventory. As the city continues to contribute nearly 10% to Uttar Pradesh's GSDP, the combination of corporate expansion and infrastructure growth is expected to maintain a steady 6% to 9% annual appreciation for the foreseeable future.

Spring House Opens 1,200-Seat Coworking Space in Noida

Noida Flex Market Brief: Spring House Expansion Noida has solidified its position as a primary hub for flexible office solutions in early **2026**. Realty firm Spring House Workspaces has launched a new managed office center in the city to capture this momentum. The facility spans **60,000 square feet** and adds **1,200 desks** to the local inventory. This expansion follows a broader trend where the Indian flexible office sector is projected to cross **100 million square feet** by the end of this year. Delhi-NCR remains the second-largest market in the country for flex stock, trailing only Bengaluru. Market Dynamics and Pricing Corporate demand for managed spaces has surged, with international enterprises accounting for **72%** of recent leasing activity. Global Capability Centres and large IT firms are shifting away from traditional long-term leases to prioritize speed-to-market and reduced capital expenditure. Average desk prices in Noida currently range from **₹6,000** to **₹9,500** per month in key IT corridors like Sector 62 and Sector 63. Premium Grade A buildings in micro-markets such as Sector 16 and the Noida Expressway are commanding higher rates, often exceeding **₹14,000** per desk. Commercial property values in Noida have seen a steady climb, with average rates reaching approximately **₹9,200 per square foot** in **2026**. Infrastructure milestones, including the progress of the Jewar Airport and Film City, continue to drive capital appreciation in the commercial segment at an average rate of **15% to 20%** annually. Supply and Demand Trends Flexible workspace now represents roughly **13%** of the total office space demand nationwide. In Noida, the "flight to quality" is evident as occupiers seek out Grade A assets that offer modern amenities and sustainable designs. Managed office and enterprise solutions currently dominate the post-pandemic landscape, making up **70% to 80%** of all flex space transactions. This shift is mirrored in the Spring House expansion, which focuses on providing high-capacity, fully managed environments for corporate clients rather than just traditional individual coworking seats. Vacancy rates in core business hubs across Delhi-NCR are expected to tighten through **2026** as absorption rates outpace new completions. Strategic corridors like the Noida-Greater Noida Expressway are seeing the highest concentration of these new developments, supported by improved metro connectivity and a growing ecosystem of service industries.

Smartworks Leases 1.82 Lakh Sq Ft Office Space in Mumbai

Smartworks Coworking Spaces Ltd has significantly expanded its footprint in Mumbai, securing 182,300 square feet of prime office space at "The Square" in Andheri East. This strategic move, finalized in February 2026, pushes the company’s total portfolio in India's financial capital past the 2 million square foot mark. The new facility is situated in a Grade A project developed by Lloyds Realty Developers. Located just 0.5 km from the Mumbai International Airport, the center is designed to meet the intensifying demand for managed office solutions from large-scale enterprises and Global Capability Centers. The Indian flexible office market is currently operating at a historic peak. National net absorption reached 61.4 million square feet in 2025, a 25% year-on-year increase. Mumbai specifically contributed 17 million square feet in gross leasing volume during this period. Demand remains robust as 78% of Indian businesses in the IT and finance sectors have now transitioned to permanent hybrid work models. Smartworks’ recent financial data highlights a successful growth trajectory. The company reported a 34% year-on-year revenue increase to 4,721 million INR in Q3 FY26. Notably, the firm achieved a milestone by turning PAT positive under Ind-AS standards for the first time, supported by a healthy 17.9% EBITDA margin. Enterprise clients now drive 90% of the company's rental revenue. A significant shift in the market is the rise of the "1,000+ seat" cohort, which now accounts for 36% of total revenue. These large-scale corporate occupiers prefer managed campuses over traditional leases to reduce capital expenditure and benefit from tech-enabled amenities. Market supply for flexible workspaces in India is projected to exceed 100 million square feet by the end of 2026. In Mumbai, average office rentals have firmed up, rising nearly 2% quarter-on-quarter. Prime micro-markets like Andheri East and BKC continue to lead this growth due to superior connectivity and infrastructure like the new Metro Line 3. Smartworks currently manages a national portfolio of 15.3 million square feet across 63 centers in 15 cities. With a committed occupancy rate of 92%, the firm is well-positioned to capitalize on the ongoing "flight to quality" as corporates consolidate fragmented offices into premium, managed environments.

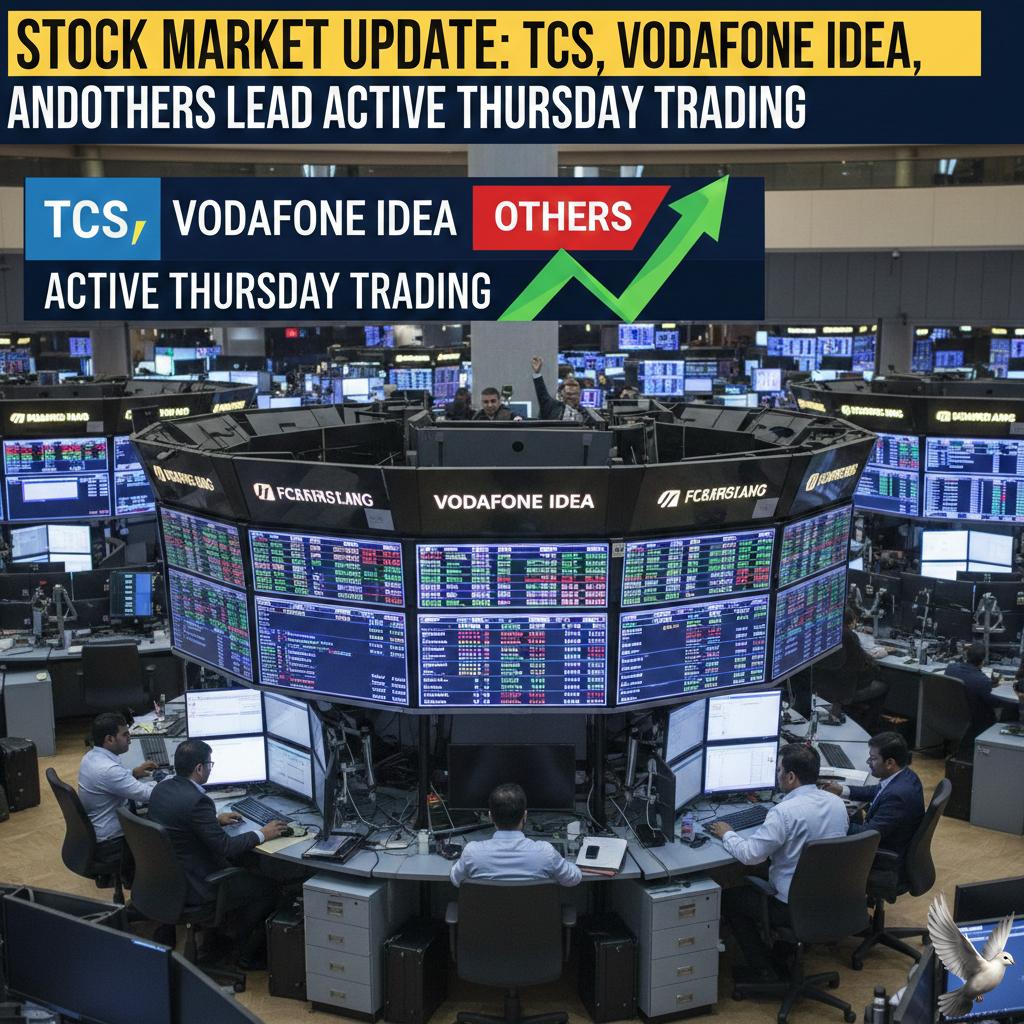

Stock Market Update: TCS, Vodafone Idea, and Others Lead Active Thursday Trading

Market Overview Indian benchmark indices faced a significant retreat on **Thursday, February 12, 2026**, as a massive sell-off in the technology sector overshadowed broader market sentiment. The **BSE Sensex** plummeted **558.72 points**, or **0.66%**, to settle at **83,674.92**. Similarly, the **NSE Nifty 50** snapped its four-day winning streak, declining **146.65 points** or **0.57%** to end at **25,807.20**. The broader market also felt the heat, with the Nifty Midcap 100 dropping **0.47%** and the Smallcap 100 falling **0.64%**. IT Sector Crisis The **Nifty IT index** was the day's primary laggard, tumbling a massive **5.51%** to close at **33,160**. This sharp decline was triggered by escalating fears that new, advanced artificial intelligence agents—specifically recent releases from firms like Anthropic—could automate core services traditionally handled by Indian software firms. **Tata Consultancy Services (TCS)** saw its market capitalization slip below the psychological **₹10 lakh crore** mark for the first time since late 2020. The stock hit a fresh 52-week low of **₹2,752.75**, down over **5%** during the session. Other major technology losers included: * **Tech Mahindra**: Down **6.40%** * **Infosys**: Down **5.97%** * **Coforge**: Down **6.61%** * **HCL Technologies**: Down **5.20%** Economic Headwinds Sentiment was further dampened by stronger-than-expected **U.S. jobs data** for January. The robust labor market has led investors to believe the **U.S. Federal Reserve** will keep interest rates higher for longer, fading hopes for a near-term rate cut. Domestically, the **Reserve Bank of India (RBI)** recently kept the repo rate unchanged at **5.25%**, maintaining a neutral stance while monitoring global volatility and the impact of international trade deals. Sectoral Highlights and Gainers While most sectors ended in the red, the **Consumer Durables** index managed a modest gain of **0.50%**. Despite the sea of red, specific stocks showed resilience: * **Bajaj Finance**: Surged **3.31%** * **Shriram Finance**: Rose **2.48%** * **Eicher Motors**: Gained **2.13%** * **ICICI Bank**: Up **1.84%** **Hindustan Copper** also saw trading interest following recent board approvals for interim dividends and firm global copper pricing trends, even as the broader metals space remained volatile. Technical Outlook The **Nifty 50** slipped below its immediate support levels during the session, hitting an intraday low of **25,750**. Analysts noted that the **Nifty IT index** has now fallen approximately **12%** in 2026 so far, reflecting a deep-seated recalibration of valuations within the tech industry due to structural shifts in the global software landscape.

SAIL, Sharda Cropchem Among Four Commodity Stocks Reaching 52-Week Highs Following Monthly Rallies

Commodity Market Pulse: Feb 2026 The Indian metals and agrochemicals sectors are demonstrating exceptional strength. Key players in the steel and commodity space have surged to significant milestones, with several reaching all-time highs as of **February 12, 2026**. This rally occurs despite a cautious broader market where the Sensex has faced intermittent pressure, trading near the **83,700–84,200** range. Sharda Cropchem: Performance Leader Sharda Cropchem has emerged as a top performer in the agrochemical space. The stock hit an all-time high of **₹1,254.00** during today's session. * **One-Month Rally:** Approximately **51%** gain * **One-Year Return:** Over **112%** * **Technical Status:** Trading above all major moving averages (5-day to 200-day) * **Current Momentum:** The stock has decoupled from the broader market, driven by a zero-debt balance sheet and strong intellectual property registrations. Steel Sector Milestones The ferrous metals sector is benefiting from disciplined mill output and robust domestic infrastructure demand. Leading producers have reported substantial price appreciation. **JSW Steel** The company hit a fresh record high of **₹1,263.85** on February 12. * **Market Cap:** Approximately **₹3.04 lakh crore** * **Quarterly Growth:** Net profit surged to **₹2,527 crore** in the latest quarter * **Year-to-Date:** Up **7.07%**, significantly outperforming the Sensex's **1.66%** decline in the same period. **Jindal Steel (JSPL)** Jindal Steel touched a new 52-week peak of **₹1,207.00**. * **Annual Appreciation:** Up **44.9%** over the last 12 months * **Recovery:** The stock has climbed over **56%** from its 52-week low of **₹770** * **Sector Rank:** Outperformed the broader ferrous metals index by **0.32%** in recent sessions. **Steel Authority of India (SAIL)** SAIL reached a milestone high of **₹162.90** this week. * **Sales Volume:** Rose **16%** year-on-year to **5.15 million tonnes** * **Annual Return:** Approximately **62%** * **Market Outlook:** Analysts point to aggressive inventory liquidation and January price hikes as primary drivers for the current valuation. Sector Catalysts The upward trajectory in these commodities is supported by specific industrial shifts: * **Demand Projections:** India's steel demand is expected to grow by **8%** for the **2025/2026** fiscal year. * **Price Adjustments:** National Mineral Development Corporation (NMDC) recently hiked iron ore prices by **₹100 per tonne**, signaling firm input costs. * **Import Protection:** Government safeguard duties of **11-12%** on select imports have provided domestic mills with enhanced pricing power. * **Infrastructure Spend:** Sustained government capital expenditure continues to underpin volume growth for long-steel products. The technical alignment of these stocks remains bullish. Most are currently positioned above their **200-day moving averages**, a standard indicator of long-term upward trends. While global iron ore prices are forecast to stabilize between **$95 and $100 per tonne**, domestic operational efficiency and inventory management are currently the dominant factors driving share prices.

Mamaearth Q3 Results: Net Profit Rises 93% to Rs 50 Crore as Revenue Increases 16% YoY

Honasa Consumer, the parent company of Mamaearth, has reported a robust financial performance for the third quarter of FY26. Revenue from operations climbed to 602 crore, marking a 16% increase compared to the 518 crore recorded in the same period last year. This growth is supported by a strong return to profitability. In the preceding quarter, the company posted a net profit of 39 crore, a significant turnaround from previous losses. Half-yearly profits for FY26 have spiked to 80.5 crore, showcasing a 3.7x increase year-on-year. The company's stock is currently reflecting this positive momentum. As of mid-February 2026, Honasa shares are trading near 295.60 on major exchanges, gaining approximately 3% over the last month. The market capitalization stands at approximately 9,616 crore. Strategic expansion remains a key driver for the group. Honasa recently completed the acquisition of a 95% stake in the men’s grooming brand Reginald Men for 195 crore. This move is designed to capture a larger share of the South Indian market and the rapidly growing men’s personal care segment. The company also continues to diversify its portfolio through a 25% stake in Couch Commerce, the owner of Fang Oral Care. These investments align with a broader shift in the Indian beauty and personal care market, which is projected to reach 40 billion dollars by 2030. Operational efficiency is improving as the company scales. Gross profit margins have stabilized around 71%, supported by a 35% increase in direct offline distribution outlets. Younger brands in the portfolio, such as The Derma Co, are growing at rates exceeding 20% annually. Market sentiment is bolstered by recent internal moves, including a 50 crore share purchase by the company’s promoter. Analysts maintain a generally positive outlook, with average price targets for the stock hovering around the 320 mark. The broader industry trend in 2026 highlights a shift toward dermatology-backed skincare and "clean" beauty. Honasa’s strategy of leveraging Gen Z and Gen Alpha consumer bases through influencer-led marketing continues to sustain its digital-first leadership in the FMCG sector.

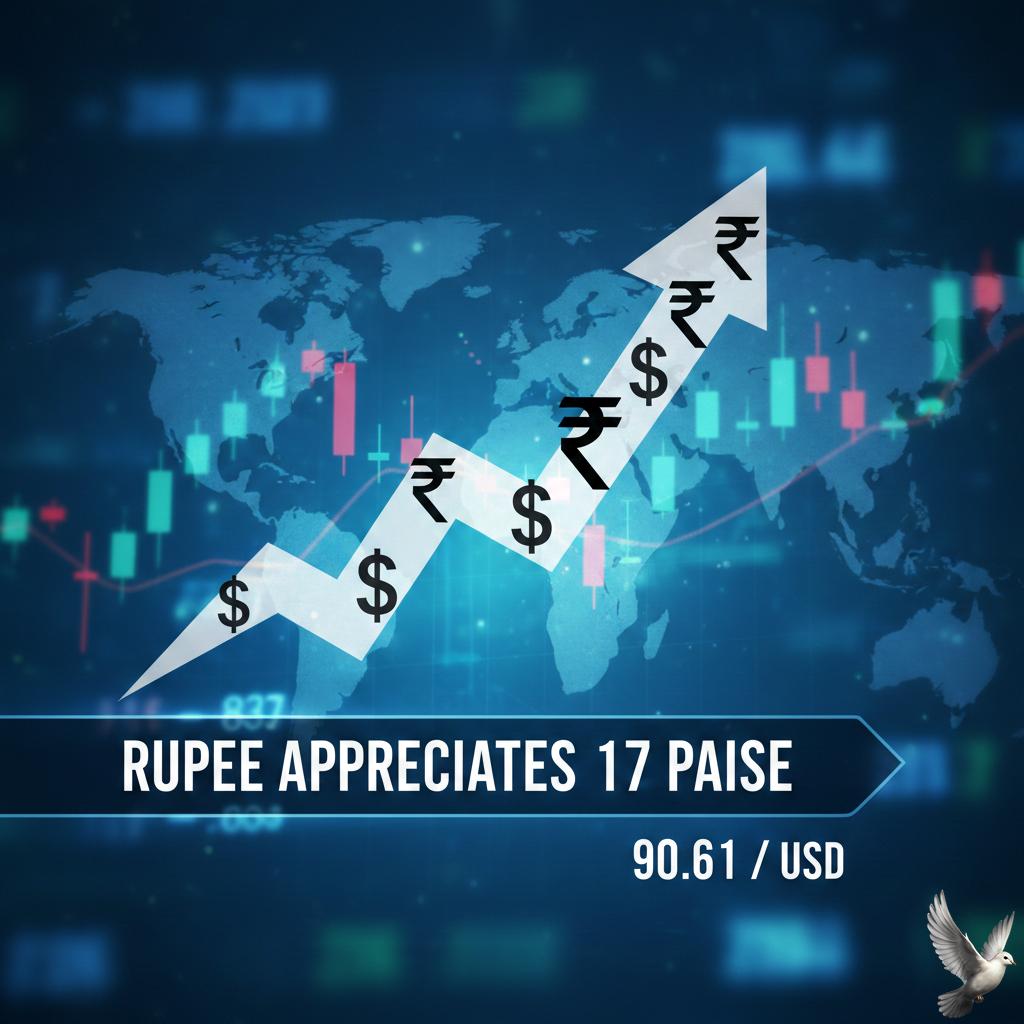

Rupee Appreciates 17 Paise to 90.61 Per US Dollar

The Indian rupee strengthened on Thursday, February 12, 2026, gaining **17 paise** to close at **90.61** against the US dollar. This recovery follows a volatile session on Wednesday where the currency had slipped to **90.78**. Market sentiment was primarily bolstered by a steady return of foreign fund investments and a landmark trade development with the United States. At the interbank foreign exchange market, the rupee exhibited strong momentum early in the day. It opened at **90.55** and surged to an intraday high of **90.40** before settling at its final provisional mark. This performance highlights a shift in risk appetite, as foreign portfolio investors (FPIs) turned net buyers in early February, infusing over **Rs 8,100 crore** into Indian equities after months of heavy selling. The broader economic landscape is currently shaped by the recent India-US interim trade agreement. Under this deal, reciprocal tariffs on Indian goods have been reduced from **25%** to **18%**, a move expected to provide structural support to exports. Consequently, major financial institutions like Goldman Sachs have upgraded India’s real GDP growth forecast for 2026 to **6.9%**, citing the positive impact of lower trade barriers. Inflation data released today shows a transition to a new CPI base year (**2024=100**). Under this revised series, retail inflation for January 2026 climbed to **2.75%**, up from the previous month's adjusted figures. Despite this uptick, the Reserve Bank of India (RBI) remains in a neutral stance, keeping the repo rate unchanged at **5.25%**. The central bank has been active in the background, ensuring banking system liquidity remains in surplus—recently averaging around **Rs 70,000 crore** per day. External factors provided a supportive cushion as the dollar index, which tracks the greenback against six major currencies, eased slightly to **96.79**. Additionally, Brent crude prices softened to **$69.20** per barrel, reducing the "silent tax" on India's import-heavy economy. While the domestic equity markets saw some profit-booking, with the Sensex closing lower, the underlying currency stability reflects growing confidence in India’s macroeconomic fundamentals and its narrowing current account deficit, now projected at **0.8%** of GDP for 2026.

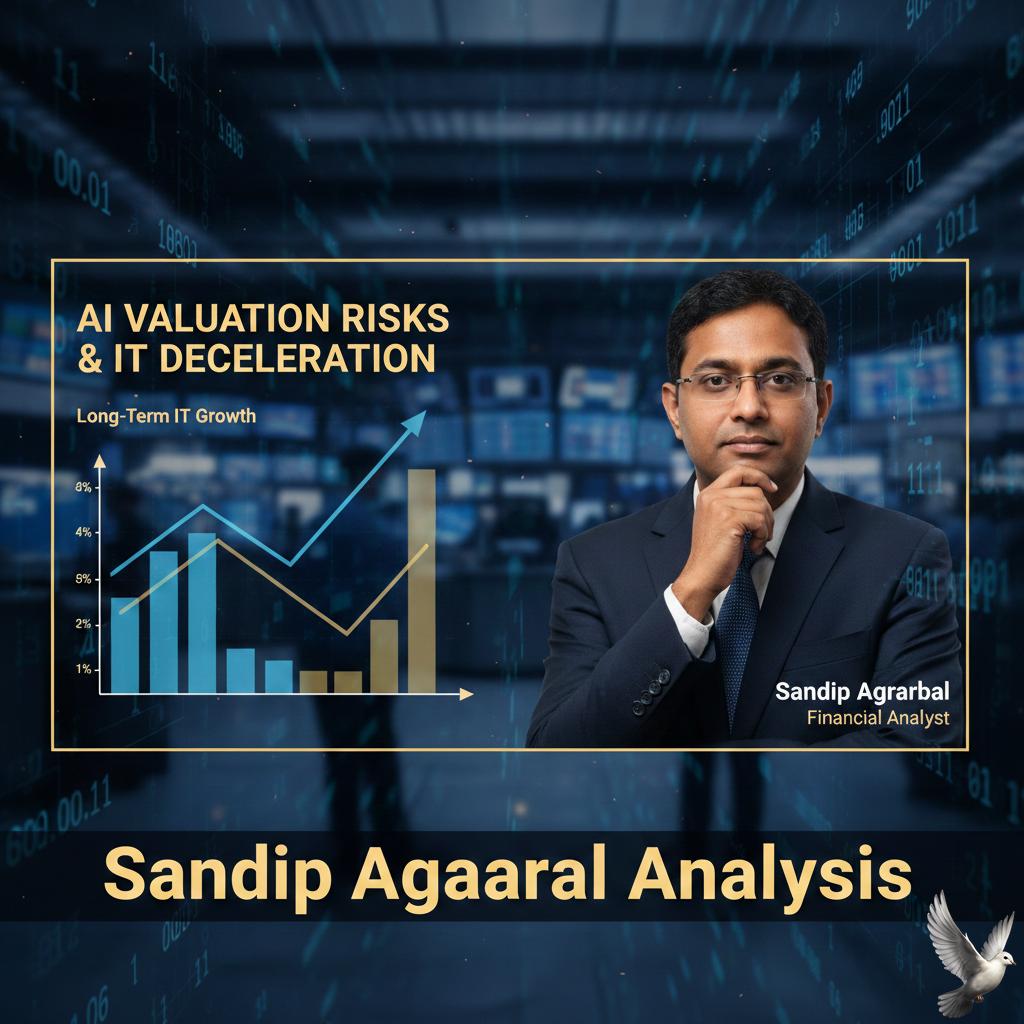

AI Valuation Risks and Long-Term IT Growth Deceleration: Sandip Agarwal Analysis

The Indian IT services sector is navigating a significant structural pivot as Artificial Intelligence moves from experimental phases into large-scale production. While the industry is on track to hit a **$300 billion** revenue milestone by FY26, the transition is creating a visible divide in growth trajectories and market valuations. Market data for early 2026 reveals a sharp divergence in performance. Large-cap IT firms are currently modeling revenue growth in the **5% to 6%** range, reflecting a cautious outlook as traditional maintenance and manual-intensive projects face automation pressure. In contrast, mid-cap firms and those specializing in Engineering Research & Development (ER&D) are maintaining a more aggressive pace, with growth projections between **10% and 12%**. The "AI tax" on billing models is becoming a tangible reality. Generative AI tools are drastically reducing the human effort required for coding and testing, forcing a shift from traditional time-and-material billing to output-based or outcome-based models. Industry reports indicate that AI-centric engagements now represent approximately **74%** of all new contracts signed over the last six quarters. Investor sentiment has turned sharply cautious in February 2026. The Nifty IT index has witnessed a correction of over **10%** since the start of the year. Significant volatility was recorded on February 12, 2026, as major players like Tech Mahindra and Infosys saw intraday drops of nearly **6%**. Tata Consultancy Services (TCS) saw its market capitalization slip below the **₹10 lakh crore** mark for the first time in years, losing its position as India’s fourth most valuable company to banking giants. Despite these valuation adjustments, India’s status as a global technology hub remains firm. The sector now contributes roughly **10%** to the national GDP. Global Capability Centers (GCCs) and a surge in domestic tech spending—growing at **7%** annually—are providing a necessary cushion against the slowdown in traditional export services. The long-term outlook suggests a "sharp recovery" by 2027 as firms successfully integrate agentic AI and intelligent automation into their core delivery. For now, the focus remains on upskilling the **5.8 million** strong workforce and renegotiating contracts to capture value from AI-driven efficiency rather than just volume of hours.

Institutional Holdings Decreased in 10 Large-Cap Stocks During Q3

Institutional investors adjusted their positions across major large-cap stocks in **Q3 FY26**, marking a period of strategic rebalancing. As of **February 2026**, market data shows a distinct shift toward selective profit-taking in sectors that saw significant run-ups, particularly in IT and private banking. Foreign Institutional Investors (FIIs) have moved toward a more cautious stance, while Domestic Institutional Investors (DIIs) have stepped in to absorb liquidity. On **February 11, 2026**, FIIs recorded a net purchase of **₹69.45 crore**, a sharp contrast to DIIs who remained aggressive net buyers at **₹1,174.21 crore**. The **Nifty 50** currently trades near the **25,950** mark, reflecting a year-to-date gain of approximately **11.1%**. Despite the general upward trend, institutional desks have trimmed stakes in high-weightage names to manage concentration risk. Key large-cap movements include: * **Reliance Industries**: Currently valued at a market cap of **₹19,87,514 crore**, the stock saw marginal institutional trimming as investors locked in gains following a steady climb to **₹1,468.70**. * **HDFC Bank**: Traded at **₹932.60** with institutions re-evaluating weightages amid a **0.50%** intraday dip and broader private bank sector pressure. * **TCS & Infosys**: Both tech giants faced selling pressure in Q3. TCS saw its price adjust to **₹2,983.00**, while Infosys traded at **₹1,495.00**, down **0.15%** in recent sessions. * **ITC**: Institutional holdings were slightly reduced as the stock price stabilized around **₹321.25**, reflecting a defensive shift in FMCG allocations. Market activity in early **February 2026** confirms that while the broader indices remain resilient, the "buy everything" phase has transitioned into a "stock-specific" regime. Professional desks are increasingly moving capital toward PSU banks and the auto sector. **State Bank of India (SBI)** emerged as a primary beneficiary of this rotation, surging **7.6%** in recent activity to reach **₹1,142.20**. Similarly, **Maruti Suzuki** gained institutional favor, trading at **₹15,136.00** as earnings outlooks improved. This rebalancing is driven by the **Securities Markets Code 2025**, which has tightened governance and transparency, prompting institutions to favor companies with the strongest corporate shells. Total unique investors in the Indian market have now surpassed **12 crore**, providing a domestic cushion that offsets global FII volatility. Current sentiment remains balanced but vigilant. The yield on the **10-year benchmark federal paper** stands at **6.71%**, influencing the shift from high-growth tech toward value-oriented infrastructure and energy stocks.

SBI Overtakes TCS and Infosys in Market Capitalization Amid PSU Bank Turnaround

In a historic reshuffle on the Indian bourses, State Bank of India (SBI) has overtaken Tata Consultancy Services (TCS) to become the country's fourth most valuable listed company. This shift marks a significant rotation in investor preference. For the first time in approximately **15 years**, the state-owned lender's valuation has exceeded that of the IT bellwether. As of February 12, 2026, SBI's market capitalization reached approximately **₹10.92 lakh crore**, while TCS's valuation slipped to nearly **₹10.52 lakh crore**. SBI now trails only Reliance Industries, HDFC Bank, and Bharti Airtel in the national rankings. Banking Surge and Record Profits The ascent of SBI is underpinned by its strongest-ever quarterly performance. For Q3 FY26, the bank reported a **24%** year-on-year rise in net profit, hitting **₹21,208 crore**. Key metrics driving this rally include: * Net Interest Income (NII) growth of **9%** to **₹45,190 crore**. * Gross Non-Performing Asset (NPA) ratio improving to **1.57%**. * Credit growth maintaining a healthy pace of **15.6%**. Management has indicated confidence in sustaining net interest margins above **3%** through the remainder of 2026, supported by robust loan demand and improved asset quality. IT Sector Headwinds In contrast, the IT sector is grappling with a de-rating fueled by global uncertainty. TCS shares have declined nearly **4%** in the last week alone, while Infosys has seen its value drop over **21%** on a year-on-year basis. Investors are currently pricing in the potential for artificial intelligence to disrupt traditional IT service models. This has led to heavy selling across the Nifty IT index, which has faced significant pressure as global tech spending remains cautious. Sectoral Divergence The market gap between these sectors continues to widen. While SBI has surged **21%** year-to-date in 2026, major IT counters have largely traded in the red. The Nifty PSU Bank index has consistently outperformed the broader market, gaining nearly **5%** in recent weekly cycles, driven by institutional buying and a fundamental turnaround in public sector balance sheets. This structural shift reflects a broader bet on India's domestic credit cycle and infrastructure recovery, contrasting with the export-oriented challenges facing the technology sector.

Six Stocks With Over 100 Mutual Fund Investors Gain Up to 130% Annually

Global Market Brief: February 12, 2026 The global equity landscape is currently navigating a period of high-stakes transition. While the tech-driven rally of the past year has reached historic milestones, recent sessions show a market attempting to balance massive capital investment in artificial intelligence with a shifting interest rate outlook. NVIDIA and the Intelligence Economy NVIDIA remains the primary architect of the current market cycle. As of today, the company maintains a market capitalization of approximately **$4.5 trillion**, securing its position as the world’s most valuable enterprise. Investor focus has moved from the Blackwell architecture to the newly announced **Rubin platform**. This next-generation system, built on a **3nm** process, is designed to reduce AI inference costs by **10x**. While the stock has seen a **43%** gain over the last **12 months**, current trading around **$188.54** reflects a "normalization" phase as the industry prepares for the Rubin production ramp-up in the second half of **2026**. Analysts maintain an overwhelmingly bullish outlook, with over **92%** issuing a Buy rating. The average price target has moved to **$253.62**, suggesting a potential upside of **25%** from current levels. Semiconductor Sector Dynamics The broader chip industry is on track to reach **$975 billion** in total revenue by the end of **2026**, representing a **26%** year-over-year acceleration. This growth is heavily concentrated in logic and memory chips, which are both projected to expand by more than **30%** this year. A significant structural shift is underway as the market moves from "Training" to "Inference." Demand for High Bandwidth Memory (**HBM4**) is expected to drive the memory market to **$68 billion** by year-end. However, this concentration of value creates a paradox: while AI chips drive nearly **50%** of industry revenue, they account for less than **0.2%** of total unit volume. Global Indices and Economic Indicators Major indices are showing signs of consolidation following the recent surge. The **Dow Jones** recently crossed the **50,000** milestone, though it slipped slightly to **50,121** in the latest session. The **S&P 500** is hovering near **6,941**, while the **Nasdaq Composite** stands at **23,066**. Economic sentiment is currently being shaped by stronger-than-expected U.S. labor data. January non-farm payrolls rose by **130,000**, well above the consensus of **70,000**. This labor market resilience has pushed the **10-year Treasury yield** up to **4.17%**, causing traders to scale back expectations for imminent Federal Reserve rate cuts. Regional Highlights and Commodities * **India:** The **Nifty 50** is holding steady at **25,953**, buoyed by a **9.4%** rise in net direct tax collections and improving foreign institutional flows. * **Energy:** **Brent Crude** is trading at **$69.60** per barrel, while **WTI** is at **$64.86**. * **Metals:** **Spot Gold** has retreated slightly to **$5,065** per ounce as yields firm up. The central theme for the remainder of the quarter is the "Agentic AI" revolution. As enterprises move from experimental chatbots to autonomous agents, the demand for specialized hardware and high-performance networking like **Spectrum-X**—now a multi-billion dollar business—will likely dictate the next leg of the sector's performance.

Rajesh Bhosale's Top Two Stock Recommendations

Market Overview The Indian equity benchmarks are currently navigating a phase of consolidation. The **Nifty 50** is trading in a restricted band, closing recently at **25,953.85**. The index faces a formidable psychological and technical hurdle at the **26,000** mark. Aggressive call writing at this strike price suggests that a decisive breakout is required to trigger the next leg of the rally. Market volatility remains subdued, with the **India VIX** falling to **11.56**. This indicates a lack of panic among investors despite the rejection at higher levels. Immediate support is established at **25,800**, while a deeper structural base is forming near **25,500**. Sector Performance and Stocks to Watch Selective stock picking remains the primary strategy as sector rotation continues. Financials: Bajaj Finance **Bajaj Finance** continues to draw positive sentiment with an average analyst target price of **₹1,090**. The company is benefiting from robust loan book expansion and its strong association with the Bajaj brand. Over **61%** of analysts maintain a buy rating, viewing the current consolidation as an accumulation opportunity. Automobiles: Hero MotoCorp **Hero MotoCorp** is showing significant resilience, trading near **₹5,788**. The stock has outperformed the broader market with a **36%** gain over the past year. Technically, it is maintaining a position above its major long-term moving averages. Analysts have set a consensus target of **₹6,183**, supported by a healthy dividend yield of **4.84%** and optimism surrounding rural demand recovery. Consumer Goods: Hindustan Unilever (HUL) The outlook for **Hindustan Unilever** remains cautious following its latest quarterly results. While the company reported a headline net profit of **₹6,603 crore**, this was heavily inflated by a one-time exceptional gain of **₹4,611 crore** from its ice cream business demerger. Core operating profit actually saw a **30%** decline, reflecting significant margin pressure and a challenging input cost environment. The stock is currently trading around **₹2,440**. Economic Context The broader economic backdrop remains supportive of long-term equity valuations. * **GDP Growth:** Projected at **7.4%** for the current fiscal year. * **Inflation:** Easing price pressures have allowed for a more accommodative monetary stance. * **Institutional Activity:** Foreign Institutional Investors (FIIs) turned net buyers recently with an inflow of **₹943 crore** in a single session. Investors are advised to maintain discipline and focus on quality businesses as the market "catches its breath" before the next directional move.

EMS Sector Reports 30% Growth Driven by Amber and Syrma Amid Margin Expansion

Market Brief: India’s Electronics Manufacturing Surge India’s electronics manufacturing sector is currently navigating a high-growth phase, with production values surging from **₹1.9 lakh crore** in 2014 to over **₹11.3 lakh crore** in 2025. This six-fold expansion is now accelerating toward a **$300 billion** production target by the end of 2026. Recent policy shifts have solidified this momentum. The Union Budget 2026-27 recently doubled the outlay for the Electronics Components Manufacturing Scheme (ECMS) to **₹40,000 crore**. This strategic pivot aims to move India beyond simple assembly into high-value component manufacturing, such as multilayer PCBs and camera modules. The sector's export performance has been equally transformative. Electronics have climbed to become India’s third-largest export category, reaching **$22.2 billion** in the first half of the 2025-26 fiscal year. In a landmark shift, India recently overtook China to become the top smartphone exporter to the United States. Sector Leaders and Financial Performance Key players like **Amber Enterprises** and **Syrma SGS Technology** are demonstrating the profitability of this shift toward high-margin segments. **Amber Enterprises** is witnessing strong market traction, with its share price surging **26%** in the last 30 days. Analysts have issued a "Buy" rating with target prices reaching **₹8,962**. The company is successfully diversifying into the railways and defense sectors, with railway business revenue expected to double within the next two years. **Syrma SGS Technology** reported a blockbuster third quarter for FY26, with revenue jumping **45%** to **₹1,274 crore**. Its profit after tax (PAT) more than doubled, increasing by **108%** year-on-year. This growth is underpinned by an order book currently standing at **₹6,400 crore**, reflecting robust demand in high-growth verticals. The Shift to Industrial and Automotive Electronics A significant trend in 2026 is the rapid adoption of electronics in the automotive and industrial sectors. The Indian automotive electronics market is valued at **$12.6 billion** and is projected to reach **$27.8 billion** by 2032. The transition to Electric Vehicles (EVs) is a primary catalyst. EV retail sales recently surged by **16%**, with electric passenger car sales jumping **77%**. This shift is creating massive demand for power electronics, battery management systems, and advanced driver assistance systems (ADAS). Syrma SGS has capitalized on this, reporting **44%** growth in its automotive vertical and **45%** in industrial segments. Meanwhile, industrial automation and medical electronics are growing at rates exceeding **30%**, as companies prioritize sophisticated, high-tech production over traditional consumer durables. Investment Outlook and Strategic Drivers The investment climate remains highly favorable, supported by over **$4 billion** in FDI inflows since 2021. Nearly **70%** of this capital is linked to Production Linked Incentive (PLI) scheme beneficiaries. Investors are increasingly focused on companies that demonstrate: * **Strong Order Visibility:** Backlogs extending into 2027 and 2028. * **Vertical Integration:** Moving into PCB and semiconductor packaging. * **Margin Expansion:** Shifting from low-margin assembly to design-led manufacturing. With the India-US trade deal providing preferential access for automotive components and the India-EU FTA offering new tailwinds, the sector is positioned for sustained double-digit growth. Industry GVA grew at **9.13%** in the latest quarter, signaling that the "Make in India" initiative has reached a critical, self-sustaining scale.

HAL Declares Rs 35 Interim Dividend and Announces Record Date

Hindustan Aeronautics Ltd (HAL) has delivered a standout financial performance for the third quarter of FY26, signaling robust operational health and a strong commitment to shareholder returns. The company reported a 29.7% year-on-year surge in consolidated net profit, reaching ₹1,866.66 crore for the quarter ended December 31, 2025. Revenue from operations grew by 10.7% to touch ₹7,698.87 crore, supported by steady execution across its manufacturing and service segments. This growth follows a positive nine-month trajectory, where net profit climbed 12.1% to ₹4,919.48 crore on a total revenue of ₹19,146.47 crore. In a move to reward investors, the Board of Directors declared a first interim dividend of ₹35 per equity share for the current fiscal year. This represents a significant payout on the face value of ₹5 per share. The record date to determine eligibility is set for February 18, 2026, with the actual payment scheduled to be completed by March 14, 2026. Market sentiment remains focused on HAL's massive order book, which currently stands at over ₹94,000 crore. This provides long-term revenue visibility, though execution timelines for key projects like the Tejas Light Combat Aircraft (LCA) remain under scrutiny. HAL recently clarified that five Tejas Mk-1A aircraft are fully ready for delivery, while nine more have been built and flight-tested. The handover is currently awaiting the arrival of F404 engines from GE Aerospace. To secure future production, HAL signed a landmark $1 billion deal with GE in late 2025 for 113 additional jet engines to power the 97 LCA Mk-1A aircraft ordered by the Ministry of Defence. The broader defense sector is operating within a favorable policy environment. The Union Budget 2026-27 has earmarked ₹2.19 lakh crore for defense capital expenditure, a 21.8% increase over the previous year. With the government reserving 75% of the capital acquisition budget for domestic industry, HAL is positioned as a primary beneficiary of India’s self-reliance initiatives. On the bourses, HAL shares have shown resilience following the earnings release, rebounding from recent lows to trade near the ₹4,100–₹4,170 range. Analysts maintain a generally positive outlook on the stock, citing a healthy 24.3% EBITDA margin and the company’s near debt-free balance sheet. Market capitalization remains robust at approximately ₹2.76 trillion, reflecting HAL's dominant position in the aerospace and defense landscape.

Vodafone Idea Shares Decline 4% Following JPMorgan Rating Downgrade

Telecom Sector Brief: Vodafone Idea Market Update Vodafone Idea (Vi) continues to navigate a high-stakes recovery period as of **February 12, 2026**. The company’s stock price has recently faced downward pressure, settling near **₹11.50**, a decline of approximately **3.04%** in a single session. This volatility follows a sharp divergence in market sentiment: while technical indicators showed the stock trading above long-term moving averages, fundamental skepticism from major institutional players has intensified. JPMorgan has issued a notable downgrade on the stock to **Underweight**, setting a target price of **₹9.00**. This valuation suggests a potential downside of more than **20%** from recent highs. The brokerage explicitly described Vodafone Idea’s internal goal of tripling its cash EBITDA over the next three years as "aggressive" and "potentially overestimated." Operational and Competitive Challenges The primary concern remains the company's ability to arrest subscriber churn. Recent data for December 2025 reveals that Vodafone Idea lost **940,731** wireless users, bringing its total base to **198.7 million**. In contrast, Bharti Airtel saw a massive gain of **5.43 million** users, while Reliance Jio added **2.96 million**. Consequently, Vodafone Idea’s market share has slipped to approximately **15.98%**. Financial health indicators highlight a significant disparity between Vi and its peers: * **Average Revenue Per User (ARPU):** Vi reported a sequential growth of **3%** to **₹172**, but still trails significantly behind Airtel’s **₹259** and Jio’s **₹213.7**. * **Leverage:** The company faces a staggering debt-to-EBITDA ratio of **9.60 times**, with total debt excluding spectrum dues estimated at over **₹2 lakh crore**. * **Cash Flow:** Quarterly cash EBITDA (excluding IndAS 116) stood at **₹2,358 crore**, a slight dip from the previous year. Funding and Network Strategy The execution of a **₹45,000 crore** three-year capital expenditure plan is heavily reliant on securing **₹25,000 crore** in bank funding. Analysts note that concrete commitments from lenders remain limited, creating a "capex conundrum." Without this capital, the company struggles to scale its 5G rollout, which currently covers **43 cities** across **17 circles**, compared to the near-nationwide 5G coverage of its competitors. While the broader Indian telecom sector saw revenues rise **9%** year-on-year to **₹72,700 crore**, growth is slowing as the impact of previous tariff hikes fades. Vodafone Idea has called for further "price repairs" to improve returns on investment, but market analysts suggest that any significant tariff intervention is likely to be led by market leaders rather than challengers. Investors are currently monitoring the company's progress in securing institutional funding and the potential for regulatory relief regarding AGR dues, which remain critical markers for its long-term survival.

HAL Reports 30% YoY Profit Increase to Rs 1,867 Crore and Declares Rs 35 Dividend per Share

Hindustan Aeronautics Limited (HAL) continues to demonstrate robust financial health, underpinned by India’s accelerating focus on indigenous defense production. As of the third quarter of the 2024-25 fiscal year, the state-run aerospace giant reported a significant 15% year-on-year increase in revenue from operations, reaching 6,957 crore. This growth is a clear reflection of the company's expanding role in the national security ecosystem. The company’s profitability has followed a similar upward trajectory. Net profit for the December quarter rose by 14% to 1,433 crore, compared to 1,253 crore in the previous year. Operational efficiency remains a highlight, with EBITDA margins improving to 24.2%. In a move to reward shareholders, the board declared a first interim dividend of 25 per equity share for the current financial year. HAL’s forward-looking indicators remain exceptionally strong. The current order book stands at a massive 1.33 lakh crore, providing high revenue visibility for several years. Strategic projections suggest this figure could climb to 2.5 lakh crore by the 2025-26 fiscal year. Key drivers for this anticipated surge include pending contracts for 97 Light Combat Aircraft (LCA) Tejas Mk1A and 156 Light Combat Helicopters (LCH) Prachand, which together are valued at approximately 1.3 trillion. The broader market environment is equally supportive. The Ministry of Defence has been allocated a record 6.81 lakh crore in the latest budget, marking a 9.5% increase aimed at modernization and self-reliance. While HAL has faced some scrutiny regarding the delivery timelines of the Tejas Mk1A jets, the company is actively ramping up production capacity to 24 aircraft per year across its Bengaluru and Nasik facilities. Recent strategic developments include the successful inaugural flight of the Dhruv New Generation (NG) helicopter and a long-term contract with Safran for the development of critical engine parts. These milestones, combined with India's record defense production of 1.51 lakh crore in the 2024-25 period, position HAL as a primary beneficiary of the country’s structural shifts toward a "Make in India" defense framework. Despite recent price volatility, the stock has maintained a one-year rally of approximately 26%. Market analysts note that while short-term corrections are evident, the long-term outlook is bolstered by a manufacturing pipeline that is fully occupied until 2030. HAL’s elevation to Maharatna status further enhances its operational autonomy as it targets new export opportunities in Southeast Asia and South America.

SoftBank Returns to Profitability Driven by OpenAI Investment Gains

SoftBank Group has returned to profitability for the third fiscal quarter of 2025, signaling a decisive turnaround fueled by a massive bet on artificial intelligence. The Japanese investment giant reported a net profit of 248.6 billion yen (approximately $1.62 billion) for the October–December period. This result marks the company’s fourth consecutive profitable quarter, a sharp recovery from the 369 billion yen loss recorded during the same period a year ago. The primary driver of this growth is the surging valuation of OpenAI. SoftBank’s investment in the ChatGPT creator has generated a staggering 2.8 trillion yen ($19.8 billion) in gains over the first nine months of the fiscal year. SoftBank has currently invested over $30 billion in OpenAI, securing an 11% ownership stake. Reports indicate the group is in talks to invest up to an additional $30 billion in a new funding round that could value OpenAI between $750 billion and $830 billion. The Vision Fund segment, once a source of significant losses, recorded a profit of 735.49 billion yen this quarter. This reversal was bolstered by OpenAI’s appreciation, which helped offset weaker performance in other parts of the portfolio. Beyond its direct startup bets, SoftBank’s subsidiary, Arm Holdings, is playing a critical role in its financial narrative. Arm recently reported record quarterly revenue of $1.24 billion, driven by a 27% increase in royalty revenue as its architecture becomes central to AI data centers. To maintain its aggressive investment pace, SoftBank has been liquidating other major assets. Between June and December 2025, the group sold its $5.8 billion stake in Nvidia and a portion of its T-Mobile holding for $12.73 billion. The company is also pivoting toward infrastructure. In late 2025, SoftBank committed to acquiring Swiss robotics firm ABB for $5.4 billion and land from Sharp for 100 billion yen to build large-scale AI data centers. Despite the positive momentum, SoftBank missed the average analyst profit estimate of 336.7 billion yen. Investors remain focused on the company’s rising leverage, as it continues to secure loans against its Arm holdings to fund its ambitious AI "all-in" strategy.

HUL Q3 Results Reflect GST Rate Cut Benefits: Kaustubh Pawaskar

Hindustan Unilever Limited (HUL) has showcased resilient performance in its latest quarterly results for the period ending December 31, 2025. The company reported a consolidated revenue of 16,235 crore, marking a 6% year-on-year increase. This growth was supported by early signs of a demand recovery and a steady 4% underlying volume growth, suggesting that consumer appetite is stabilizing despite a complex economic backdrop. The most striking figure in the report was a 121% surge in consolidated Net Profit, which reached 6,603 crore. This significant jump was primarily driven by a one-time gain following the successful demerger of the company's ice cream business. Excluding these exceptional items, the underlying profit after tax grew at a more modest pace of 1%, totaling 2,562 crore. Operating margins remained a point of strength for the firm. EBITDA for the quarter rose 3% to 3,788 crore, with the EBITDA margin holding firm at 23.3%. This profitability level aligns with management’s guided range and reflects disciplined cost management and a strategic focus on premiumization across key product categories. Sector-wise performance showed a clear tilt toward premium brands. The Beauty & Wellbeing segment delivered a 6% increase in underlying sales, powered by double-digit growth in high-end hair care brands like Dove and TRESemmé. The Home Care division recorded a 3% sales increase, with liquid detergents continuing their double-digit growth momentum. However, the segment faced some pricing pressure due to strategic price cuts implemented during the year to remain competitive. On the stock market, HUL shares faced immediate volatility following the announcement on February 12, 2026. Despite the massive headline profit, the stock dropped approximately 4% to trade near the 2,394 level. Investors appeared to react to the 30% decline in profit from continuing operations and the impact of a 576 crore exceptional loss related to the implementation of new Labour Codes. The broader FMCG environment is showing signs of a shift. While rural demand is proving resilient, urban markets are navigating a "conscious consumption" phase where health and value take center stage. The rise of quick commerce has emerged as a critical growth engine, and HUL has established a dedicated organization to scale its presence in these "channels of the future." Looking ahead, the outlook for the sector is cautiously optimistic. Moderating inflation—with retail figures recently hitting multi-year lows—and a favorable monsoon forecast are expected to bolster consumer spending. HUL remains focused on building brand desirability and accelerating market development in high-growth spaces to sustain its leadership position through 2026.