Bullish News

Collection

Paytm Market Performance: Sustained Profitability vs. Stock Valuation Returns

Paytm has solidified its financial turnaround, reporting its third consecutive profitable quarter as of the December 2025 period (Q3 FY26). The company successfully transitioned from a loss-making phase to a steady profit trajectory, driven by robust growth in core payments and financial services. **Key Financial Milestones** For Q3 FY26, Paytm reported a Net Profit (PAT) of **225 crore**, a significant reversal from the **208 crore loss** recorded in the same period the previous year. Operating revenue rose **20% year-on-year** to reach **2,194 crore**. The company’s EBITDA (before ESOP) surged to **156 crore**, reflecting a 7% margin and showcasing strong operational leverage. **Core Business Performance** The payments division remains the primary engine of growth, with revenue from payment services climbing **21% to 1,284 crore**. Merchant adoption continues to scale rapidly. The subscriber base for payment devices reached **1.44 crore**, adding **27 lakh** new devices over the past year. Total Gross Merchandise Value (GMV) processed through the platform remains high, with UPI consumer market share gaining for three consecutive quarters. Consumer UPI GMV specifically grew **35%** over the last nine months, doubling the industry average growth rate of **16%**. **Financial Services and Lending** The distribution of financial services, including merchant loans and wealth products, saw a revenue jump of **34%**, reaching **672 crore**. The number of customers availing these services increased to **7.1 lakh**, up from **5.9 lakh** a year ago. Despite regulatory shifts in certain lending segments, the company has maintained healthy contribution margins, which currently stand at **57%**. **AI-First Strategy and Innovation** Paytm is pivoting toward an "AI-first" operational model to drive efficiency. The company recently launched a redesigned flagship app featuring over **15 AI-driven tools**. New features include "Paytm Checkin" for travel planning and AI-powered expense tags that automatically categorize monthly spending. On the merchant side, AI is being used for real-time risk monitoring and automated onboarding, helping reduce indirect expenses, which fell **8%** this quarter to **1,092 crore**. **Market Position and Outlook** As of early February 2026, Paytm’s market capitalization stands at approximately **74,122 crore**. The stock has demonstrated a recovery of over **49%** over the last 12 months, reflecting renewed investor confidence. The company maintains a strong liquidity position with a cash balance of **12,882 crore**. This capital provides the flexibility to continue investing in new growth drivers while navigating the evolving regulatory landscape for digital payments in India.

Small-cap Stocks Gain Momentum Following Positive Q3 Earnings Growth

Small-cap stocks have emerged as the early leaders of 2026, marking a decisive shift in market leadership after a grueling previous year. Investors are rotating capital out of mega-cap technology and into domestically focused smaller companies, driven by improving fundamentals and more attractive valuations. The Russell 2000 has surged 6.5% year-to-date as of early February 2026, significantly outperforming the S&P 500's 1.1% gain and a 0.9% decline in the Nasdaq Composite. This follows a historic 15-session winning streak for small caps against large caps, the longest such period of dominance since 1996. Earnings for the small-cap segment are projected to grow by 17% to 22% throughout 2026, outpacing the 14% growth expected for large-cap peers. In the financial sector specifically, small-cap earnings are forecasted to jump by 33.9% in the first quarter of 2026. Valuation remains a primary catalyst for this "great rotation." Small caps are currently trading at a forward price-to-earnings ratio of approximately 17x, a deep discount compared to the 29x seen in the S&P 500. Analysts describe the segment as a "coiled spring" for value seekers. Specific sectors are showing robust momentum. The aerospace and industrials categories are leading the way, with aerospace earnings expected to rise over 40% in early 2026 as supply chain pressures ease. Domestic-focused firms are also benefiting from a stronger dollar and reduced exposure to global trade volatility. While the broader recovery appears to be a turning point, market breadth remains narrow and selectivity is essential. Approximately 70% of certain small-cap index components are still recovering from previous corrections, though sentiment has been boosted by recent international trade deals and cooling geopolitical tensions. Ongoing economic resilience, including a 2.5% GDP growth forecast and a balanced labor market, provides a stable backdrop for this transition. Investors are increasingly viewing small-cap quality and value stocks as the primary engines for growth in the coming months as the "artificial intelligence" premium in mega-caps begins to face scrutiny. [Small Cap Market Outlook 2026](https://www.youtube.com/watch?v=akn48UBqyDk) This video provides a professional breakdown of the 2026 market outlook, including the specific sector shifts and domestic growth engines driving the small-cap recovery. http://googleusercontent.com/youtube_content/0

Impact of Budget 2026 on Global Portfolios: Analysis of Tax Amnesty and Trade Deals by Bhaskar Hazra

Budget 2026 has introduced a pivotal one-time compliance window for undisclosed foreign assets, marking a significant shift toward a more structured cross-border investment framework. This six-month voluntary disclosure scheme allows taxpayers to regularize overseas holdings with specific immunity from prosecution. For assets and income up to 1 crore, a 60% total tax and penalty is applicable. For previously taxed income where only the asset remained unreported, a flat fee of 1 lakh is set for holdings up to 5 crore. Assets valued under 20 lakh are now granted immunity from prosecution, simplifying life for small investors and students. Trade dynamics have shifted following the landmark Free Trade Agreement with the European Union. Dubbed the mother of all deals, it aims to eliminate tariffs on 99.5% of Indian goods. In a rapid domino effect, a subsequent deal with the US has lowered reciprocal tariffs from 25% to 18%, providing a 0.2% boost to annual GDP. Market valuations remain a primary focus as the Nifty 50 hovers near the 26,000 mark. While indices have consolidated for over 16 months, earnings growth is accelerating, particularly in the BFSI and auto sectors. Real GDP growth for the current fiscal year is estimated at a robust 7.4%, supported by a stable repo rate held at 5.25%. Currency stability is vital for global portfolios as the Rupee trades near 90.35 against the US Dollar. India’s forex reserves have climbed to a record 723.8 billion, providing a cushion against global volatility. This liquidity buffer, combined with a narrowing current account deficit of 0.8% of GDP, supports a resilient investment outlook. Investors are encouraged to prioritize quality and growth as the market enters a new phase of transparency. The alignment of tax amnesty, favorable trade pacts, and strong domestic demand positions India as a key destination for disciplined capital allocation.

MCX Gold and Silver Prices Rise Amid Falling US Treasury Yields

Market Brief: February 11, 2026 Global financial markets are navigating a period of measured optimism today as Asian equities hover near record highs and Indian benchmarks extend their winning streak for a fourth consecutive session. Equity Market Performance The domestic market continues its upward trajectory following a positive close on Tuesday. The **Nifty 50** ended at **25,935.15**, gaining **67.85 points**, while the **BSE Sensex** rose **208.17 points** to settle at **84,273.92**. **GIFT Nifty** futures indicate further momentum, trading near **26,053.50**, a premium of approximately **92 points**. Broad-based buying in the auto and metal sectors has been the primary driver of recent gains. Volatility remains low, with the **India VIX** slipping **4.30%** to **11.67**, suggesting a significant cooling in market nervousness. Global Economic Climate Central banks in Europe and the UK are maintaining a cautious stance. The **European Central Bank** has kept interest rates unchanged, with the deposit facility at **2.00%** and the main refinancing rate at **2.15%**. In the UK, the **Bank of England** maintained its rate at **3.75%** in a tight **5–4 vote**, though headline inflation has slowed to **3.4%**. Markets are now pricing in a higher probability of **three Federal Reserve rate cuts** this year following soft US retail data. Commodities and Currencies Gold is maintaining a strong position near a two-week high, trading at **$5,055.26 per ounce**, a **0.62%** increase. Silver has seen more aggressive movement, jumping **2.29%** to **$82.63**. In the energy sector, **Brent Crude** is trading at **$69.32**, up **0.76%**, while **WTI** sits at **$64.52**. The currency market shows the **USD/INR** pair at **90.40**, reflecting a slight decline of **0.07%**. The **Euro** and **British Pound** have also softened against the Rupee, trading at **106.55** and **123.03** respectively. Technology and Innovation A significant rotation is occurring within the tech sector. While "Magnificent Seven" stocks like Microsoft and Alphabet have faced pressure due to massive AI capital expenditure—projected to exceed **$660 billion** this year—**Apple** has emerged as an outlier, gaining over **5%** in the past week. Investors are shifting focus from pure growth to capital efficiency and free cash flow. This has triggered a defensive rotation toward sectors like Energy and Agriculture, propelling the **Dow Jones** above the **50,000** milestone for the first time. Digital Assets The cryptocurrency market remains in a volatile recovery phase. **Bitcoin** is trading near **$67,878**, attempting to stabilize after a sharp drawdown from its **$126,000** peak in late 2025. **Ethereum** continues to underperform relative to Bitcoin, trading at **$1,989** after a **6.2%** slump. Bitcoin’s market dominance holds steady at **60%**, while Ethereum's share has contracted to roughly **10%** amid lower institutional liquidity.

Swiggy Among Four Stocks Identifying Bullish RSI Trends

Market dynamics for early February 2026 reveal a complex landscape defined by shifting central bank policies, regional divergence in equity performance, and heightened volatility in the commodities sector. Global Equity Performance Global markets are currently navigating a phase of fragmented leadership. The Japanese Nikkei 225 has emerged as a frontrunner with a year-to-date gain of **12.0%**, bolstered by recent political stability and a commitment to expansionary fiscal policies. In contrast, the Indian markets have faced a period of consolidation. The Nifty 50 and Sensex hover near **25,935** and **84,273** respectively. While domestic sentiment remains supported by a resilient economy, the BSE Sensex has recorded a year-to-date decline of **1.4%**, pressured by foreign institutional selling and a significant repricing in the technology sector. Monetary Policy and Economic Indicators The Reserve Bank of India maintained the repo rate at **5.25%** during its February meeting, adopting a neutral stance. This decision is underpinned by a projected real GDP growth of **7.4%** for the **2025–26** fiscal year and a benign inflation outlook of **2.1%**. In the West, the European Central Bank held its deposit rate at **2.00%**, noting a decline in headline inflation to **1.7%**. The Bank of England also maintained rates at **3.75%**. Investors are now closely monitoring upcoming US and Chinese inflation data for signals on the next phase of global liquidity. Commodities and Currency Gold has reclaimed the **$5,000** per ounce milestone, trading near **$5,070** on the back of weak US economic data and expectations of future rate cuts. Domestic gold prices in India have rebounded to approximately **₹15,878** per gram for 24-karat. Silver has entered an overbought phase, currently trading near **$82.35** per ounce after experiencing a sharp correction from recent highs. Crude oil remains volatile due to geopolitical tensions in the Middle East. Brent crude futures rose above **$69** per barrel, while WTI crude trades around **$64.57**. The Indian Rupee remains steady against the US Dollar, trading at approximately **90.52**. The Dollar has shown signs of weakening as global investors reassess allocations amid rising US debt servicing costs, which now consume nearly **5%** of US GDP. Sector Trends and Corporate Outlook The technology sector has faced significant pressure, with the Nifty IT index experiencing its sharpest decline since mid-2025 due to concerns over AI-driven disruption. Conversely, the automotive and energy sectors have shown strength, with the Nifty Auto index gaining over **5%** in recent sessions. Defensive sectors like FMCG and Pharma continue to provide a cushion against volatility. Large-cap attention is currently fixed on upcoming earnings releases from heavyweights such as Mahindra & Mahindra and Divi’s Laboratories, which are expected to provide clarity on consumer demand and industrial margin pressures.

Fractal Analytics IPO: Day 3 Subscription Status and Gray Market Premium

Fractal Analytics concludes its **₹2,834 crore** initial public offering today, February 11, 2026. As the first pure-play AI firm to list in India, the issue represents a landmark moment for Dalal Street, though investor response remains measured. The price band is set between **₹857 and ₹900** per share. The offering is a combination of a fresh issue worth **₹1,023.50 crore** and an offer for sale of **₹1,810.40 crore** by existing shareholders. Retail investors can participate with a minimum investment of **₹14,400** for a lot of 16 shares. Subscription data as of the final day shows a cautious trend. Retail interest leads the categories, having reached approximately **60%** of its quota by the previous evening. However, Qualified Institutional Buyers (QIBs) and Non-Institutional Investors (NIIs) have shown significant restraint, with subscription levels at **2%** and **29%** respectively heading into the final hours. Grey market sentiment has softened throughout the bidding period. The Grey Market Premium (GMP) is currently hovering around **₹3 to ₹8**, translating to a modest **1%** upside over the upper price band. This suggests an estimated listing price near **₹903 to ₹908**. Financial performance highlights a major turnaround. In FY25, Fractal reported revenue of **₹2,765 crore**, reflecting a **26%** year-on-year increase. More importantly, the company swung to a net profit of **₹221 crore** following a loss in the prior fiscal year. EBITDA margins have also improved to roughly **14%**. Proceeds from the fresh issue are earmarked for strategic growth. The company plans to deploy **₹264.90 crore** for debt repayment in its US subsidiary and **₹355.10 crore** for research, development, and marketing within its Fractal Alpha division. Additional funds will support new office infrastructure in India and inorganic growth. Analysts maintain that while the valuation is premium—trading at a P/E multiple of approximately **70x**—the company offers unique exposure to the global AI market. India’s AI sector is projected to reach **$22 billion** by 2027, providing a strong tailwind for firms specializing in decision intelligence and agentic AI. Final allotment is expected to be finalized by **February 12, 2026**, with the official listing on the BSE and NSE scheduled for **February 16, 2026**. Experts advise a long-term perspective for those entering at these levels, given the volatility typical of high-growth technology sectors.

Eicher Motors Q3 Results: Net Profit Up 21% and Revenue Up 23% YoY

Eicher Motors has delivered a standout performance for the third quarter of the 2025-26 fiscal year, cementing its position as a leader in the global middleweight motorcycle and commercial vehicle sectors. **Group Financial Highlights** The company reported a consolidated net profit of **1,421 crore**, marking a sharp **21%** increase from **1,170 crore** in the same period last year. This performance significantly exceeded market estimates. Total revenue rose by **23%**, supported by record operational efficiency. EBITDA jumped **30%** to reach an all-time high of **1,557 crore**. Operating margins also saw a notable improvement, climbing **130 basis points** to settle at **25.46%**. **Royal Enfield Expansion** Royal Enfield remains the primary growth engine, recording quarterly sales of **325,773 motorcycles**, a **21%** jump year-on-year. Demand has been particularly strong for the 350cc and 650cc portfolios. To sustain this momentum, the board has approved a major capacity expansion plan. The company aims to increase its annual production capacity from the current **14.6 lakh units** to **20 lakh units** across its manufacturing facilities. Product innovation continues to drive brand interest. The recent debut of the **Flying Flea C6**, Royal Enfield’s first all-electric motorcycle, marks a strategic entry into the EV space. Upcoming launches like the **Bullet 650** and new **750cc prototypes** are expected to further broaden its market appeal. **Commercial Vehicle Performance** The joint venture with Volvo, **VE Commercial Vehicles (VECV)**, outpaced the industry despite a generally sluggish market for heavy vehicles. VECV reported a **44%** surge in net profit, reaching **301 crore**. Monthly sales data for December 2025 showed a volume of **10,384 units**, representing **24.7%** growth. Domestic Eicher trucks and buses saw a **26.3%** rise, while exports grew by an impressive **32.7%**. **Market and Technical Outlook** Eicher Motors' stock currently trades near the **7,200–7,300** range with a market capitalization exceeding **2,00,000 crore**. Technically, the stock maintains a neutral to positive momentum. While it has faced some pressure from rising competition and interest rate hikes, its fundamental health remains robust. The company is virtually debt-free and has maintained a consistent **21%** profit CAGR over the last five years. With a strong product pipeline and expanded production capacity, Eicher Motors is well-positioned for continued dominance in both the premium motorcycling and commercial transport segments.

Apollo Hospitals Q3 Net Profit Rises 35%; Analysts Evaluate Stock Outlook

Apollo Hospitals has delivered a robust performance for the third quarter of the 2025-26 fiscal year, showcasing double-digit growth across its primary business verticals. The Chennai-based healthcare major reported a 35% year-on-year surge in consolidated net profit, reaching 502 crore. Revenue for the quarter grew by 17%, climbing to 6,477 crore compared to 5,527 crore in the previous year. This growth was driven by a strong showing in healthcare services and a significant turnaround in the digital and pharmacy segments. The core Healthcare Services division remains the primary engine of growth, contributing 3,183 crore in revenue, a 14% increase. Operational efficiency in this segment reached a high note with EBITDA margins expanding to 24.8%. This performance was supported by a 67% occupancy rate across its facilities and an increase in high-end surgical volumes. Apollo HealthCo, which includes the pharmacy distribution and the Apollo 24/7 digital platform, reported a 20% increase in revenue to 2,827 crore. Notably, its EBITDA more than doubled to 128 crore as the company successfully optimized its digital health spending. The segment's net profit rose sharply to 87 crore from 32 crore a year earlier. The retail and diagnostic arm, Apollo Health and Lifestyle, also saw a 20% revenue jump to 467 crore. The segment significantly narrowed its losses to 6 crore, moving closer to the break-even point through improved scale and operating leverage across its clinic network. Reflecting this financial strength, the Board of Directors declared an interim dividend of 10 per share. The record date for this payout is fixed for February 16, 2026. Strategic expansion remains a key priority. During the quarter, the company launched a new 250-bed quaternary care hospital in Pune, equipped with advanced surgical robotics and precision oncology tools. Apollo is currently on track to add over 3,500 beds across 11 locations over the next few years. Market analysts maintain a positive outlook on the stock. Citi has reiterated a Buy rating with a target price of 9,600, citing the company's clinical depth and the value-unlocking potential of its digital restructuring. Currently, the stock trades near 7,220, reflecting a market capitalization of approximately 1,03,800 crore. This performance aligns with broader trends in the Indian healthcare sector, which is projected to reach 638 billion USD by 2025. Rising medical tourism and a domestic shift toward organized tertiary care continue to provide strong tailwinds for integrated providers like Apollo.

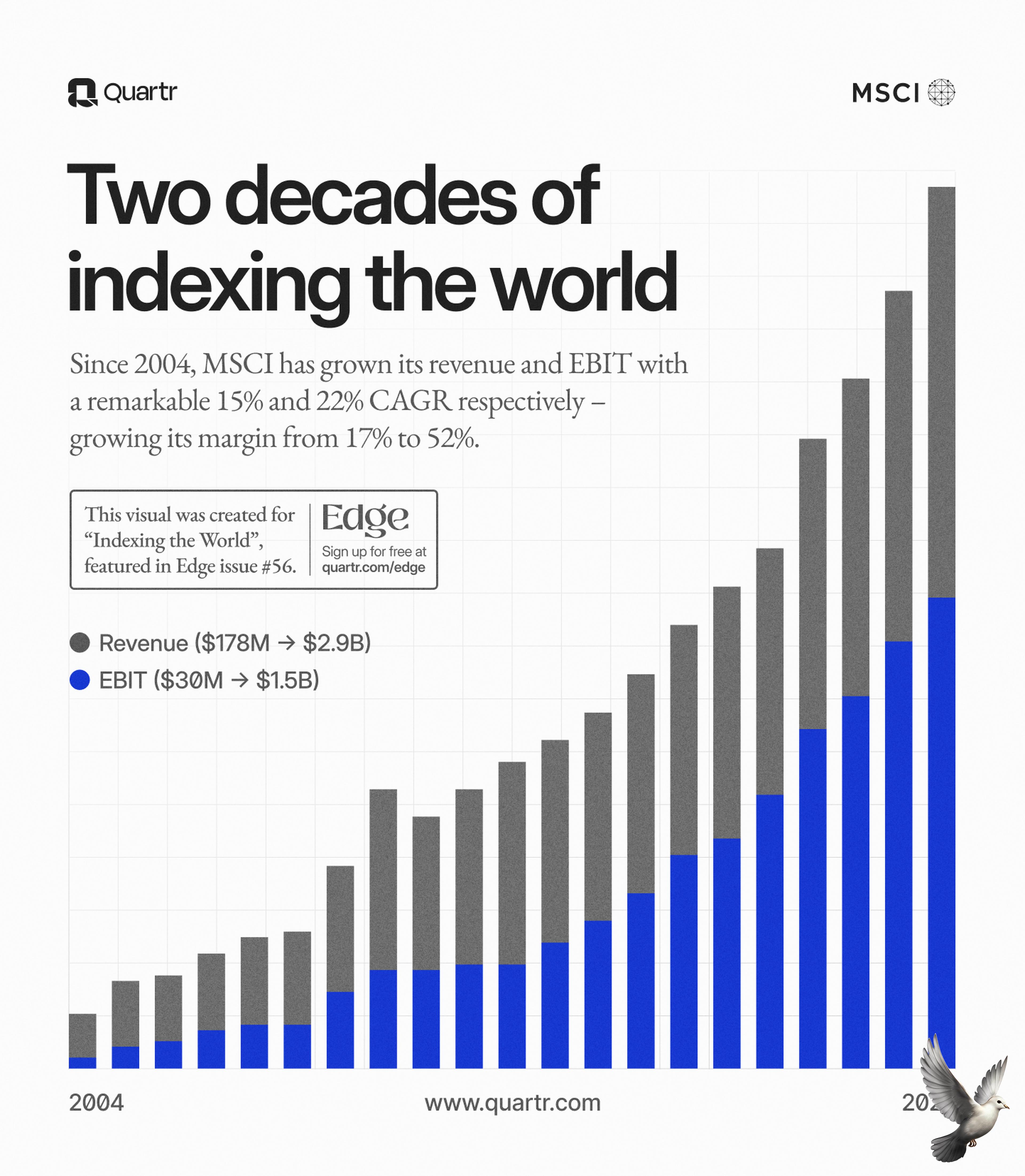

MSCI Index Review: Aditya Birla Capital and L&T Finance Added; IRCTC Excluded

MSCI has announced the results of its February 2026 index review, introducing notable shifts in the composition of Indian equities within its global benchmarks. These changes, which take effect after the market close on February 27, 2026, highlight a continued rotation toward financial services and select industrial players. Global Standard Index Updates Aditya Birla Capital and L&T Finance have been successfully added to the MSCI Global Standard Index. This inclusion is expected to trigger significant passive investment. Aditya Birla Capital is projected to see inflows of approximately **$257 million**, while L&T Finance could attract roughly **$238 million**. Conversely, the Indian Railway Catering and Tourism Corporation (IRCTC) has been removed from the Standard Index. This exclusion is likely to result in estimated capital outflows of **$142 million**. Despite these changes, India’s aggregate weight in the MSCI Emerging Markets Index remains stable at **14.1%**. The total number of Indian constituents in the Standard Index will rise slightly from **164 to 165**. Weight Adjustments and Small Cap Revisions AU Small Finance Bank is set for a weight increase following an adjustment in its free-float status. This revision is anticipated to bring in nearly **$172 million** in additional passive flows. The MSCI Small Cap Index experienced more drastic revisions. While **7** new stocks were added—including Premier Energies, NSDL, and Emcure Pharmaceuticals—a total of **34** stocks were removed. This heavy pruning reduced the number of Indian companies in the Small Cap Index from **508 to 480**. Key names exiting the small-cap category include Gokaldas Exports, Sterlite Technologies, and KNR Constructions. Market Impact and Timing The rebalancing is expected to generate a combined inflow exceeding **$500 million** for the newly added and upweighted companies. Traders expect heightened volatility and increased volumes during the final minutes of the February 27 trading session as index-tracking funds align their portfolios with the new weightings. Investors are monitoring these shifts as they reflect broader trends in liquidity and market capitalization across the Indian financial landscape for early 2026.

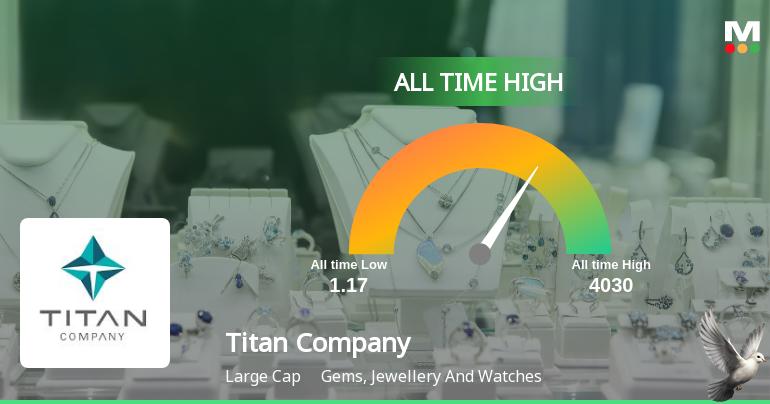

Titan Company Q3 Net Profit Increases 61% Year-over-Year

**Titan Market Brief: Q3FY26 Surge** Titan Company shares reached an all-time high of **4,329.95** on February 10, 2026, following a blockbuster third-quarter performance. The stock has delivered a **28.09%** return over the past year, significantly outperforming the broader Nifty and Sensex indices. The company reported a consolidated net profit of **1,684 crore**, marking a **61%** year-on-year increase. Total income for the quarter surged by **43%** to reach **25,567 crore**, driven by an exceptionally strong festive and wedding season. **Jewellery Segment Performance** The jewellery division remains the primary growth engine, contributing **22,517 crore** in revenue, a **42%** jump from the previous year. This growth was achieved despite gold prices hitting record highs, with 24K gold trading near **1,58,000 per 10 grams** in February 2026. Domestic brands Tanishq, Mia, and Zoya saw a combined growth of **40%**. International jewellery revenue witnessed a massive **83%** spike to **1,058 crore**, supported by aggressive expansion in the GCC region and the United States. **Watches, Wearables, and EyeCare** The Watches and Wearables division recorded a total income of **1,295 crore**, up **14%**. While analog watches saw a healthy **17%** rise due to premiumization and gifting, the smartwatch segment faced a **27%** volume decline as consumer preferences shifted. The EyeCare vertical delivered steady results with a **18%** rise in income to **231 crore**. This growth was supported by double-digit expansion in the sunglasses and lenses categories, alongside network optimization of Titan Eye+ outlets. **Operational Highlights** Titan's operational efficiency saw significant improvement, with EBIT advancing **63%** to **2,657 crore**. The EBIT margin expanded by **155 basis points** to reach **10.8%**, reflecting strong pricing power and a better product mix. The company expanded its retail footprint by adding **56 net new stores** during the quarter, bringing its total global presence to over **3,430 outlets**. Emerging businesses, including fragrances and women’s bags, grew **15%**, with the bags category alone surging by **111%**. **Strategic Outlook** Post-quarter, Titan completed the acquisition of a **67%** stake in Damas Jewellery. This move is expected to drastically scale the company’s international operations and consolidate its leadership in the Middle East market. Management continues to focus on high-value exchange programs and brand equity to navigate the current high-gold-price environment. Market capitalization now stands at approximately **3.78 trillion**, representing over **76%** of India's organized gems and jewellery sector.

11 Stocks Cross Above 200-Day Moving Average

Indian equity markets maintained positive momentum on February 10, 2026, with benchmark indices rising for a third consecutive session. The Nifty 50 advanced 67.85 points to close at 25,935.15, while the Sensex surged 208.17 points to end at 84,273.92. Optimism regarding a potential trade agreement between India and the United States, alongside strong foreign institutional investor (FII) inflows of approximately 2,254 crore, fueled the rally. In the Nifty 500 universe, technical data revealed a significant bullish shift as 15 stocks closed above their 200-day moving average (DMA). This indicator is widely used to confirm long-term uptrends. Among these, 11 stocks recorded gains exceeding 2%. Key performers included Sun TV Network, which closed at 614.35 against a 200 DMA of 576.41, and Amber Enterprises, which surged 6.2% to 7,510.50 following robust quarterly profit growth. Other notable breakouts included PVR Inox at 1,076.05 and General Insurance Corporation at 398.35. Broader market participation was evident as the Nifty Midcap 100 rose 0.49% to 60,736. Sector-wise, Nifty Media led the gains with a 2.40% jump, while the Auto and Steel sectors also showed strength. Eternal was the top gainer on the Nifty 50, rising 5.18% to 393.85, followed by Tata Steel with a 2.9% increase. The macroeconomic backdrop remains supportive with the repo rate holding at 5.25% and India's real GDP growth projected at 6.4% to 7.2% for the upcoming fiscal year. While the rupee faced slight pressure, closing at 90.77 against the US dollar, the overall market sentiment is buoyed by steady domestic demand and stabilizing global cues. Traders are now focusing on the final phase of third-quarter earnings and upcoming inflation data. Immediate support for the Nifty is identified at the 25,550–25,600 level, while the recent 200 DMA breakouts suggest a rotation toward stocks beginning new long-term growth cycles.

Grover Jewells SME IPO to Debut on NSE Today; Grey Market Premium Analysis

Grover Jewells Debuts on NSE SME Platform **Grover Jewells Limited** is set to commence trading on the **NSE SME** platform today, **February 11, 2026**. The company’s initial public offering, which closed on February 6, was priced at the upper cap of **₹88 per share**. The **₹33.83 crore** issue consisted entirely of a fresh issue of **38.44 lakh** equity shares. Market data indicates a neutral reception in the secondary market, with the **Grey Market Premium (GMP)** holding at **₹0** leading up to the bell. This suggests a flat debut, likely listing close to the original issue price. Investor Participation and Allotment The IPO witnessed robust demand across various investor categories, resulting in an overall subscription of **19.16 times**. * **Non-Institutional Investors (NII):** Subscribed **37.57 times**, showing the highest interest. * **Retail Individual Investors:** Subscribed **15.74 times**. * **Qualified Institutional Buyers (QIB):** Subscribed **11.32 times**. Prior to the public bidding, the company successfully secured **₹9.62 crore** from anchor investors on February 3, 2026, at the same offer price of **₹88**. Financial Profile and Use of Funds Grover Jewells specializes in manufacturing wholesale gold jewellery, including plain and studded products. Based in Delhi with showrooms in **Karol Bagh** and **Chandni Chowk**, the firm has expanded its B2B footprint to **20 states** and international markets like **Australia** and the **UAE**. Financially, the company has shown rapid scale. For the seven-month period ending **October 31, 2025**, it reported a total income of **₹473.22 crore** and a Profit After Tax (PAT) of **₹10.45 crore**. This follows a full-year FY25 PAT of **₹7.62 crore**. The company intends to utilize approximately **₹21.35 crore** of the proceeds for **working capital requirements**. This is critical for maintaining inventory and purchasing bullion in a high-value manufacturing environment. The remaining funds are earmarked for general corporate purposes. Sector Trends and Market Context The listing arrives at a time of significant volatility in the gold market. As of **February 11, 2026**, gold prices have remained near historic peaks, with **24K gold** trading around **₹1,58,930 per 10 grams** in Delhi. While high prices can strain demand, the broader gems and jewellery sector continues to contribute roughly **7% to India's GDP**. Recent trade developments have also improved the outlook, including a landmark reduction in U.S. tariffs on Indian jewellery exports from **50% to 18%**, which may benefit manufacturers with established export channels like Grover Jewells. Post-listing, the stock's performance will be measured against its peer group, which includes companies like **Shanti Gold International** and **RBZ Jewellers**. Investors will be monitoring if the company can maintain its **38.52% Return on Net Worth (RoNW)** while managing the **₹28.30 crore** in total borrowings reported in late 2025.

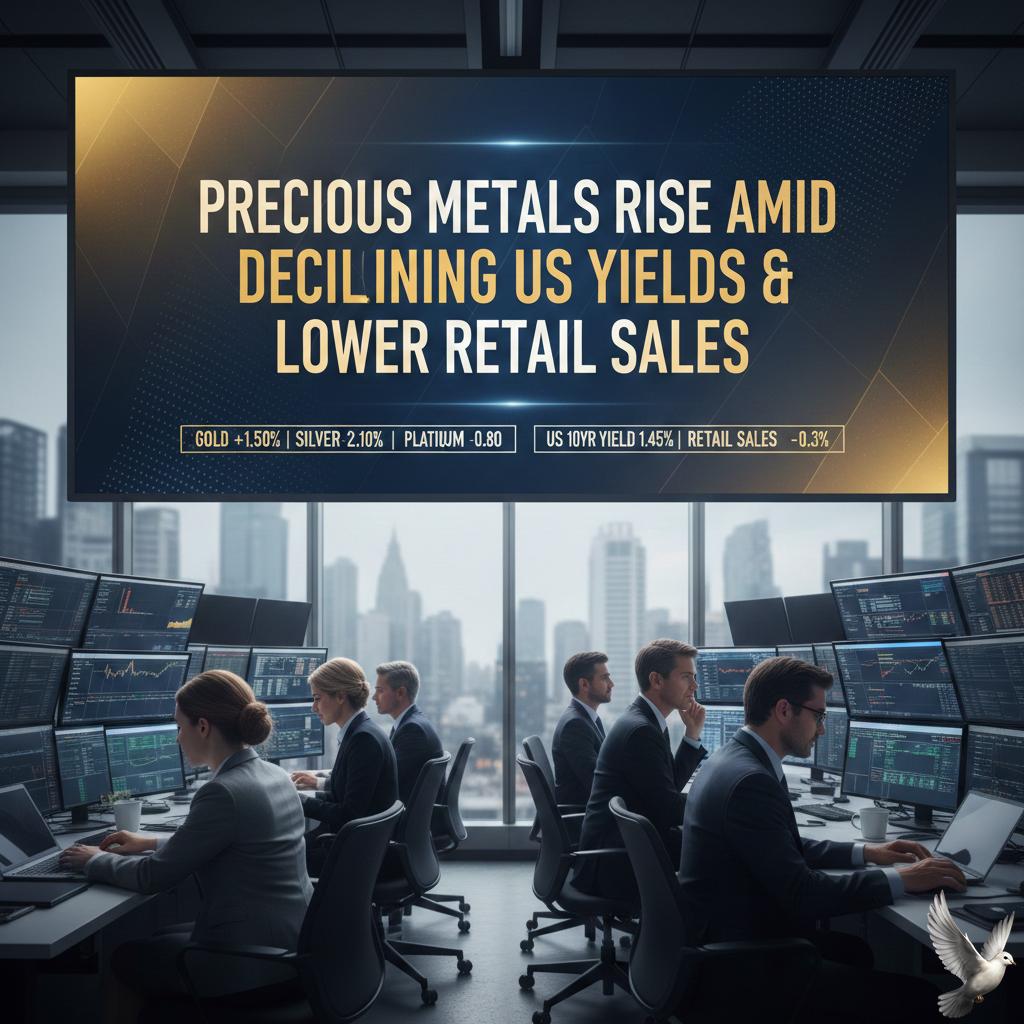

Precious Metals Rise Amid Declining US Yields and Lower Retail Sales

Market Brief: Precious Metals and Economic Indicators Precious metals demonstrated resilience on Wednesday, February 11, 2026, as gold prices held firm above the **₹1.58 lakh** mark per 10 grams in the domestic market. This stability follows a period of significant volatility where 24-karat gold peaked at **₹16,058** earlier in the month before undergoing a healthy correction. International gold prices are currently navigating a broad range between **$5,000** and **$5,100** per ounce. Analysts maintain a bullish long-term outlook, with some institutional forecasts projecting a move toward **$5,400** by late 2027, supported by consistent central bank accumulation and its status as a primary hedge against geopolitical uncertainty. Silver Market Correction and Industrial Demand Silver is experiencing a more pronounced correction following a historic rally in January. After briefly surging past the **₹4 lakh** per kg milestone on the MCX, the white metal has retraced to approximately **₹2.90 lakh** per kg. This **17%** monthly decline is viewed by many as a necessary digestion of recent gains rather than a shift in long-term fundamentals. Despite the price dip, industrial demand for silver remains robust, particularly in renewable energy and electronics. Global silver mine production is expected to rise by only **1%** in 2026, reaching **820 million ounces**, which may not be enough to close the projected sixth consecutive annual market deficit. U.S. Economic Softness and Yield Movements Recent U.S. economic data has introduced fresh cooling signals. Retail sales for December were unexpectedly flat, missing the forecasted **0.4%** increase. Even more telling was the **0.1%** drop in the core control group, which feeds directly into GDP calculations, suggesting a sharp slowdown in consumer spending. This economic softness pushed the **10-year U.S. Treasury yield** down to approximately **4.15%**, its lowest level since mid-January. Markets are now adjusting expectations for Federal Reserve policy, with a growing probability that the central bank will deliver up to three rate cuts during 2026 to support the softening labor market. Shift in Indian Investment Sentiment A significant structural shift occurred in the Indian investment landscape this January. For the first time, inflows into Gold ETFs surpassed those of equity mutual funds. According to AMFI data, Gold ETFs attracted **₹24,040 crore**, more than doubling the figures from the previous month. * Total Precious Metal ETF Inflows (Jan 2026): **₹33,503 crore** * Total Equity Mutual Fund Inflows (Jan 2026): **₹24,013 crore** * Silver ETF Monthly Inflow Growth: **139%** Investors are increasingly prioritizing portfolio diversification as equity markets face persistent foreign institutional outflows. The surge in Silver ETFs, which saw their assets under management grow by **61%** in a single month, underscores a rising appetite for high-beta assets that offer both industrial utility and inflation protection.

Brandman Retail IPO: GMP Signals Potential Listing Gains Ahead of Today's Market Debut

Brandman Retail shares have officially debuted on the NSE SME platform this Wednesday, February 11, following a highly successful initial public offering. The stock entered the market with significant momentum, backed by overwhelming subscription numbers and a steady premium in the unofficial grey market. The **Rs 86.09 crore** IPO was priced at the upper cap of **Rs 176 per share**. Investor interest was exceptionally high, with the issue being oversubscribed by more than **114 times** by the close of the bidding period. Demand was particularly aggressive among Non-Institutional Investors (NIIs), who booked their portion nearly **203 times**. Retail individual investors followed with a subscription of approximately **93 times**, while Qualified Institutional Buyers (QIBs) saw a booking of roughly **85 times**. Listing Day Performance Grey market indicators ahead of the opening bell suggested a listing gain of approximately **10% to 15%**. Unofficial premiums hovered around **Rs 15 to Rs 28**, pointing toward a debut price in the range of **Rs 191 to Rs 204**. This positive reception reflects confidence in the company’s role as a key distributor and retailer for international lifestyle and sports brands, notably its non-exclusive partnership with New Balance. Financial Snapshot and Growth The company has demonstrated rapid scaling since its inception in 2021. For the nine-month period ending December 31, 2025, Brandman Retail reported a profit after tax of **Rs 19.67 crore** on a total income of **Rs 97.21 crore**. This follows a robust fiscal year 2025, where net profit reached **Rs 20.95 crore**, a sharp increase from the **Rs 8.27 crore** recorded in fiscal 2024. Profit margins have remained strong, consistently exceeding **20%** in recent reporting cycles. Capital Utilization The fresh capital raised will be deployed to aggressively expand the company’s physical footprint. Key allocations include: * **Rs 27.90 crore** for launching 15 new Exclusive Brand Outlets (EBOs) and Multi-Brand Outlets (MBOs) across Tier-I and Tier-II cities. * **Rs 11.78 crore** for incremental working capital needs of these new stores. * **Rs 26.72 crore** to support the inventory and operational requirements of existing outlets. The company currently operates 11 exclusive brand outlets and two multi-brand outlets, primarily in Northern India. Its omni-channel strategy also leverages major e-commerce platforms like Flipkart, Ajio, and Tata Cliq to drive digital sales volume. Market observers note that while the expansion strategy is ambitious, the company faces high revenue concentration with its top ten customers and a significant reliance on the footwear segment. However, the current listing performance indicates that investors are prioritizing the company’s growth trajectory in India’s expanding premium athleisure market.

Bitcoin Accumulation Increases Among Large-Scale Holders Amid Broader Market Divestment

Market Brief: Bitcoin Stabilization & Whale Activity Bitcoin has shown tentative signs of stabilization near the **$70,000** mark as of February 11, 2026. This follows a high-volatility period where the asset briefly plunged toward **$60,000** on February 5. The market is currently navigating a transitional phase, characterized by a tug-of-war between aggressive institutional accumulation and persistent retail-driven selling pressure. Whale Accumulation Peaks Large-scale holders, or "whales," have staged their most significant buying spree since late last year. In the past week alone, mid-tier and large whale entities absorbed approximately **53,000 BTC**. This surge in demand provided a critical floor after weeks of heavy distribution. On-chain data highlights that wallets holding between **1,000 and 10,000 BTC** were instrumental in absorbing panic supply in the **$60,000–$65,000** zone. By removing coins from exchanges and moving them into cold storage, these participants are effectively tightening the tradable supply. Price Performance and Technical Levels Bitcoin is currently trading roughly **45%** below its October 2025 peak of **$126,210**. Despite the recent recovery to the **$70,000** range, technical indicators remain cautious. The asset recently broke below its 365-day moving average for the first time in nearly four years, a signal that often suggests a shift in long-term momentum. Key levels to monitor include: * **$72,000–$75,000**: Immediate resistance. Reclaiming this zone is essential to confirm a local bottom. * **$60,000**: Critical psychological and technical support, aligned with the 200-week moving average. * **$84,000**: A major resistance band that previously acted as a support floor during the late 2025 rally. Institutional Flows and Macro Context The market sentiment is currently described as "Extreme Fear," with the Fear & Greed Index sitting at **14**. This follows a challenging January that saw net outflows from U.S. spot ETFs totaling **$1.49 billion**. However, the tide may be turning. In early February, ETF flows showed signs of stabilization with a recorded net inflow of **$385.9 million** in a single week. This suggests that while retail sentiment remains fragile, institutional interest is beginning to capitalize on the lower price entries. Macroeconomic factors, including shifts in Federal Reserve leadership and anticipation of upcoming CPI data, continue to keep volatility high. Bitcoin’s recent correlation with high-growth software stocks indicates that it is currently being traded more as a "risk-on" growth asset than a traditional "digital gold" hedge. Market Outlook The current accumulation appears to be a structural reset. While whales have stepped in to prevent a deeper collapse, broader market conviction remains thin. Total open interest in the derivatives market has cooled to **$16 billion**, down from **$19 billion** the previous week. This deleveraging process has reduced the risk of cascading liquidations, but it also means the market lacks the immediate speculative fuel needed for a rapid return to previous highs. The near-term focus remains on whether Bitcoin can flip the **$75,000** resistance into a new support floor.

US Asset Management Stocks Decline Amid Artificial Intelligence Concerns

US wealth management stocks suffered a sharp decline Tuesday following the launch of a disruptive AI tool by Altruist Corp. The new technology, designed to automate complex tax strategies and personalize client planning in minutes, sparked immediate fears that traditional human-led advisory models are reaching a tipping point of obsolescence. The market reaction was swift and severe. **Charles Schwab** closed down **7.4%** after an intraday plunge of **9.5%**. **Raymond James Financial** fell nearly **9%**, while **LPL Financial Holdings** saw a drop of over **8%** by the closing bell. **Stifel Financial** also finished the session **3.8%** lower, despite attempts to recover from deeper midday losses. The sell-off underscores a growing "AI panic" across the financial services sector. Investors are increasingly concerned about long-term fee compression and the potential for tech upstarts to capture significant market share. This anxiety mirrors recent turbulence in the insurance brokerage space, where the **S&P 500 Insurance Index** fell **3.9%** just 24 hours prior. This volatility is part of a broader trend affecting the "trust industries." Last week, similar AI-driven fears wiped out **$611 billion** in market value across 164 stocks in the software and asset management sectors. High-profile firms like **Thomson Reuters** and **Morningstar** experienced their worst weekly performances in over a decade as automated research tools gain traction. Market analysts suggest that while these AI applications may currently act as efficiency boosters for human advisors, investors are pricing in a future where automated "agentic" systems handle end-to-end financial workflows. The shift suggests that the historical link between revenue growth and headcount in the wealth sector may be permanently decoupling. Industry leaders are now under pressure to prove the ongoing value of human empathy and nuanced judgment. With AI budgets rising across the board, the focus has shifted toward how established firms can integrate these tools to protect their margins before low-cost automated competitors erode their core business.

Yen Gains and Dollar Weakens Ahead of US Payroll Data

Market Brief: Yen Strengthens as Takaichi Mandate Fuels Tokyo Rally The Japanese yen staged a significant recovery on Wednesday, February 11, 2026, breaking below the **155.00** level against the US dollar. This reversal comes as the "Takaichi Trade" gains momentum following a decisive electoral victory for Prime Minister Sanae Takaichi’s party. The yen reached an intraday high near **153.85**, marking a sharp turn from the weakness seen earlier in the week. Nikkei Hits Historic Peaks Investor confidence in Japan has surged, propelling the Nikkei 225 to record territory. The index recently eclipsed the **57,800** mark, with intraday peaks testing **57,960**. The rally is driven by expectations of Takaichi’s "Resilient Japan" economic framework. Key policy goals include a planned two-year suspension of the consumption tax on food and a **¥10 trillion** public support package for the semiconductor and AI sectors. Analysts anticipate that foreign inflows into Japanese equities could reach **¥10 trillion** over the next three months, potentially dwarfing previous historical records. Dollar Under Pressure Ahead of Payrolls While Tokyo celebrates a new political mandate, the US dollar is showing signs of fatigue. The US Dollar Index (DXY) has drifted toward the **98.00** support level as traders reposition ahead of a critical, delayed employment report. The January Non-Farm Payrolls (NFP) report, rescheduled to today due to a previous government shutdown, is the primary focus for global markets. * **Consensus Forecast:** **+70,000** jobs * **Previous Month:** **50,000** jobs * **Unemployment Rate:** Projected at **4.4%** Markets are particularly sensitive to the annual benchmark revisions included in today’s release. Early estimates suggest that 2025 payroll data could be revised downward by as much as **900,000** jobs, which would signal a much cooler labor market than previously thought. Shift in Yields and Policy Outlook US Treasury yields have softened in anticipation of the data, with the 10-year yield falling to approximately **4.15%**. This narrowing yield gap between the US and Japan is providing additional support for the yen. Financial markets are currently pricing in a higher probability of a Federal Reserve rate cut in the coming months. If the NFP print falls below **50,000**, expectations for a March rate cut could become the dominant market theme. In Japan, the focus remains on the "virtuous cycle" of growth promised by the new administration. The government’s official outlook forecasts a nominal GDP growth rate of **3.4%** for 2026, supported by the first real wage increase of over **1.0%** in two decades. However, the aggressive fiscal expansion planned by Takaichi may eventually lead to increased volatility in the Japanese Government Bond (JGB) market if deficit concerns resurface.

S&P 500 and Nasdaq Decline Amid Economic Data and Corporate Earnings Focus

The US stock market currently presents a sharp contrast for global investors. While the Dow Jones Industrial Average has reached a historic new peak, the tech-heavy Nasdaq and the broader S&P 500 have retreated. The Dow Jones recently climbed 0.10% to close at 50,188.14 points. This marks a significant milestone as the index solidified its position above the 50,000-point threshold for the first time. In contrast, the S&P 500 fell 0.33% to 6,941.81, and the Nasdaq Composite dropped 0.59% to 23,102.47. Market psychology is currently dominated by massive capital expenditure in the artificial intelligence sector. Tech giants are estimated to spend over $400 billion on AI infrastructure this year alone. However, this aggressive spending is a double-edged sword. While it fuels growth for chipmakers, it is creating pressure on the profit margins of major software and internet companies. Among the "Magnificent Seven" tech leaders, Tesla was the sole gainer in the latest session, rising nearly 2%. Other giants, including Microsoft, Alphabet, and Meta, saw declines as investors weighed the high costs of AI development against immediate returns. Attention is now firmly fixed on upcoming economic data. Retail sales figures showed consumer spending remained flat in December, missing expectations. This has shifted the focus to the next set of labor statistics. Analysts expect January job growth to be a critical indicator of whether the current economic rally can be sustained. The labor market appears to be in a period of stabilization. Recent reports show the US economy added 151,000 jobs, with the unemployment rate holding steady at 4.1%. While these figures suggest a healthy environment, the concentration of job growth in only a few sectors like healthcare and finance is causing some caution. Yields on 10-year Treasuries have dipped to their lowest level in nearly a month, currently around 4.54%. This shift reflects a cautious outlook on future interest rate cuts, as the Federal Reserve remains in no hurry to ease policy until further progress on inflation is evident. For investors, the current environment is defined by rotation. Funds are moving away from stretched technology valuations and into sectors seen as less vulnerable to AI-related volatility. Gold remains a preferred hedge, maintaining its position above the $2,600 mark despite recent short-term consolidation.

Warren Buffett Quote on Market Patience and Wealth Transfer

Market performance in February 2026 continues to reward the disciplined approach championed by long-term strategists. While short-term fluctuations often dominate the headlines, current data underscores the significant premium placed on patience and fundamental stability. Global equity benchmarks have shown notable divergence in early 2026. The S&P 500 advanced 16% over the last 12 months, driven by heavy concentration in the technology and AI sectors. In contrast, the Berkshire Hathaway portfolio, which historically prioritizes steady compounding, saw a more modest 6% rise. This gap highlights a broadening market where high-growth technology often competes with traditional value-driven assets. In India, the BSE Sensex reached 84,274 points as of February 10, 2026, marking a 0.25% daily gain. The NSE Nifty 50 followed suit, closing above the 25,900 mark. Broader markets outperformed these benchmarks, with mid-cap and small-cap indices climbing 3.8% and 4.6% respectively. These figures suggest that while major indices provide stability, the real momentum is currently found in quality companies within the mid-market tier. The investment landscape remains anchored by dominant "moat" companies. Apple continues to lead major institutional portfolios, representing 40% of public stock holdings for some of the world's most successful funds. This $135 billion position is supported by a global user base of 2 billion active devices, generating nearly $100 billion in annual free cash flow. Financial institutions also remain a pillar of long-term strategies. American Express now accounts for roughly 18% of major value-oriented portfolios, with a market valuation hovering around $247 billion. Its affluent customer base and premium positioning provide a buffer against broader economic shifts. Similarly, Bank of America maintains a strong presence, making up nearly 10% of top-tier holdings due to its favorable valuation and growth projections. The macroeconomic outlook for 2026 remains resilient. Real GDP growth in India is projected at 7.4% for the 2025-26 fiscal year, with expectations for it to stay near 7% into 2027. This growth is increasingly driven by domestic demand and a surge in public infrastructure spending. Investors are currently navigating a "K-shaped" economy, where higher-income segments benefit from rising asset prices while other sectors face pressure from sticky inflation, currently trending near 2.8%. Despite these pressures, the core strategy of holding quality assets through volatility remains the most reliable path to wealth generation. Compounding continues to favor those who avoid the trap of frequent trading. For example, a 20-year lookback shows that disciplined value portfolios have rallied 756%, significantly outpacing the 456% return of the broader S&P 500. This data reinforces the principle that success is not about timing the market, but about time in the market.

Pre-Market Analysis and Trading Outlook for Today's Session

Indian equity markets demonstrated resilience on Tuesday, February 10, 2026, extending a winning streak to three consecutive sessions. The Nifty 50 advanced 67.85 points to settle at 25,935.15, while the BSE Sensex gained 208.17 points to finish at 84,273.92. Despite reaching intraday highs that neared the 26,000 and 84,500 psychological resistance levels, the indices saw gains capped by late-session profit booking in heavyweights. Sectoral performance was markedly divided as the market navigated a peak third-quarter earnings season. Media and Auto sectors led the gains, with Nifty Media surging 2.40% and Nifty Auto rising 1.37%. In contrast, the Healthcare and PSU Bank indices faced selling pressure, sliding 0.27% and 0.19% respectively. Banking stocks remained a significant drag on the broader market, with the Nifty Bank closing slightly lower at 60,626.40. Institutional activity highlighted a growing reliance on domestic support. Domestic Institutional Investors (DIIs) acted as primary shock absorbers, recording net purchases of 1,174.21 crore. Foreign Institutional Investors (FIIs) remained cautious, contributing a marginal net positive flow of 69.45 crore. This divergence underscores a shift where domestic liquidity increasingly dictates market stability against global volatility. Macroeconomic indicators provide a stable backdrop for the current consolidation. The Reserve Bank of India recently maintained the repo rate at 5.25% with a neutral stance, balancing a 7.4% GDP growth forecast for the fiscal year against controlled retail inflation, which stood at 1.33% in December. While domestic growth remains robust, the weak rupee, trading near 90.77 against the US dollar, continues to keep investors watchful. Commodity markets are currently witnessing a sharp correction. Silver prices crashed 17% in early February to reach 2,90,000 per kg, following a massive surge in the previous month. Global oil benchmarks also showed signs of softening, with Brent crude declining to 68.89 per barrel, providing some relief regarding India’s import bill and inflationary pressures. The near-term outlook remains cautiously optimistic with a clear consolidative bias. Analysts suggest that while the 26,000 mark for Nifty 50 remains a formidable barrier, the underlying momentum is supported by double-digit profit growth in the auto and power sectors. Traders are closely monitoring the 12.0 range of the India VIX, which indicates low immediate volatility despite ongoing global trade and tariff concerns.