Bullish News

Collection

Nifty 50 Support Level Identified at 25,200 Amid Market Correction

Market Brief: February 24, 2026 The Indian equity benchmarks witnessed a sharp sell-off today, with the **Nifty 50** plunging over **385 points** to hit an intraday low of **25,327.60**. This **1.5%** decline follows a period of consolidation, as the index struggled to maintain levels above the **25,700** mark established earlier in the week. Bearish sentiment was fueled by heavy profit booking across most sectors, triggered by weak global cues and persistent concerns regarding artificial intelligence-led disruptions in the technology space. The **Sensex** mirrored this weakness, crashing more than **1,300 points** during the session to trade near the **81,934** level. Technical Support and Resistance The Nifty is currently testing critical psychological and technical floors. Analysts identify a primary support zone at **25,200**, which aligns with the **200-day moving average** and a significant retracement level from previous rallies. If the current selling pressure persists and breaches the **25,200** threshold, the next major demand zone is expected around **25,000**. Conversely, immediate resistance is noted at **25,600**, followed by a heavy supply zone at **25,800**. Sectoral Performance and Divergence Despite the broader market weakness, the banking sector continues to show relative resilience. **Bank Nifty** has outperformed the headline index, supported by domestic buying and stability in private lenders. The **PSU Bank index** notably gained **1.35%** even as the broader market faltered. In contrast, the **IT sector** remains the primary laggard, with the **Nifty IT index** tumbling over **4%**. High-profile stocks like **Infosys**, **TCS**, and **Tech Mahindra** led the declines, mirroring an overnight sell-off in US technology stocks. Stock-Specific Headlines * **MobiKwik:** Shares surged up to **12.6%** following BSE approval for its subsidiary to commence stockbroking operations. * **Bharti Airtel:** Witnessed a decline of nearly **3.8%** after announcing a **₹20,000 crore** capital injection plan for its NBFC arm. * **Bank of Maharashtra:** Scaled a fresh **52-week high** of **₹72.44** amid positive corporate announcements. * **Waaree Energies:** Gained **2.5%** after securing a new **500 MW** solar module supply order. Institutional and Global Context Foreign Institutional Investors (FIIs) have remained net sellers in recent sessions, with outflows recorded near **₹638 crore** last week. However, Domestic Institutional Investors (DIIs) continue to provide a cushion, absorbing much of the selling pressure. Global uncertainty regarding US tariff policies and geopolitical tensions remains a significant overhang, keeping the **India VIX** elevated at approximately **14.36**. Market breadth has weakened, with mid-cap and small-cap indices also dropping by up to **1%** in today’s trade.

Jim Walker on the Potential Decline of US Economic Exceptionalism

US markets are entering a volatile period as the long-standing narrative of American exceptionalism faces a significant reality check. Market participants are currently navigating a chaotic landscape defined by trade tariff instability and fundamental physical constraints that threaten the expansion of the technology sector. The trade environment has shifted into a "Plan B" phase following a landmark Supreme Court ruling that dismantled previous tariff regimes. In an immediate response, a global surcharge of **15%** has been imposed on all imports. This temporary measure, set to expire in late July **2026**, has introduced profound uncertainty, complicating corporate investment plans and contributing to a "K-shaped" economic recovery where consumer spending remains uneven. Investor anxiety is clearly reflected in the commodities and currency markets. Spot gold has surged to approximately **$5,167** per ounce, recently touching record highs as a primary safe haven against policy instability. This rally is mirrored by a weakening of the US Dollar Index, which fell to **97.70**, signaling a decline in global confidence in the currency’s stability. The technology sector, a traditional engine of US growth, is confronting a massive "power crunch." The four largest tech giants have projected a staggering **$650 billion** in capital expenditure for **2026**, a **60%** increase from the previous year. However, these ambitious AI-driven plans are hitting physical walls. Five major data centers are each expected to consume over **1GW** of electricity—equivalent to the output of a nuclear reactor. Projections show a **19GW** shortfall in power capacity by **2028**, suggesting that nearly **40%** of the industry's energy needs may go unmet. Labor shortages are further compounding these issues. Firms are currently competing for a limited pool of skilled labor, with AI-related roles now making up **20%** of all tech job postings. This scarcity, combined with sticky inflation holding near **3%**, is squeezing corporate margins. While the S&P 500 recently breached the **7,000** mark, market leadership is beginning to rotate. Equal-weighted indices are outperforming traditional cap-weighted ones, indicating that investors are moving away from hyper-concentrated mega-cap tech bets. As fundamental constraints on electricity and labor intersect with trade policy chaos, the markets are being forced to re-evaluate the sustainability of current growth models. [Gold Price Breakout Analysis](https://www.youtube.com/watch?v=EUsH3mUInxs) This video provides a deep dive into the recent surge in precious metals and the specific impact of the new 15% global tariff on market volatility. http://googleusercontent.com/youtube_content/0

South India Expected to Drive Growth in Cement Sector

South India’s cement sector is undergoing a strategic transformation, pivoting from aggressive volume competition to a disciplined focus on value and profitability. As of late February 2026, the region is leading a nationwide pricing revival, with manufacturers implementing a series of hikes to recover margins. Recent market data shows that out of the ₹15–20 price increases announced in early February, approximately ₹10 per bag has successfully sustained. In major hubs like Chennai and Bangalore, retail prices for PPC grades are currently hovering between ₹310 and ₹370 per bag, while premium OPC 53 grades are commanding prices upwards of ₹390 to ₹400. Analysts expect further aggressive movement in the coming months, with potential hikes of ₹40–50 per bag projected for the April–May period. This pricing power is supported by a robust demand outlook for the 2026–2027 fiscal year. Industry experts forecast a 7–8% volume growth, primarily fueled by a significant rural revival. This growth is expected to offset potential delays in central and state capital expenditure. Rural housing now accounts for nearly 32–34% of total cement consumption, benefiting from increased farm incomes and government allocations. On the national level, the Union Budget 2026–27 has provided a strong tailwind with a 9% increase in capital expenditure, reaching ₹12.2 trillion. Effective capex, including grants-in-aid, has surged by 11% to ₹17.1 trillion. This infrastructure push, combined with a 3% increase in the road transport budget to ₹2.87 lakh crore, ensures a steady pipeline of projects for the sector. Profitability metrics are also on an upward trajectory. Ratings agencies project industry operating profits to rise by 12–18%, reaching ₹900–950 per metric tonne in the current cycle. This recovery follows a challenging period where profits had dipped to around ₹806 per metric tonne due to intense competition and high input costs. Operational efficiency remains a top priority for major players. Companies are increasingly shifting toward green energy, with leaders targeting 85% renewable energy usage by 2030. While South India still faces a capacity utilization challenge—lingering around 60–65%—the entry of large-scale players and ongoing consolidation are expected to bring much-needed market discipline. The sector is entering a phase of the "operational grind," where cost reduction and asset optimization take precedence over headline-grabbing acquisitions. With input costs like coal showing a 12% year-on-year decline and freight expenses stabilizing, the environment is ripe for sustained margin expansion throughout the second half of the fiscal year.

Ruchir Sharma Shifts to Agnostic Stance on Gold Following Recent Market Surge

Gold prices continue to navigate a landscape of extreme volatility, currently holding firm near the **$5,230** per ounce mark as of late February 2026. While the market recently witnessed an abrupt 10% correction that shook speculative confidence, the broader uptrend remains intact. The metal has reclaimed its position above the critical **$5,000** psychological floor, supported by a renewed "risk-off" rotation following significant instability in global equities. Central bank activity remains the primary structural pillar of this rally. Global reserves have expanded by approximately **15%** compared to last year. Institutions are increasingly prioritizing long-term stability over short-term gains, with **95%** of central banks signaling intent to further increase gold holdings through 2026. Estimated total purchases for the year are projected at **755 tonnes**, nearly double the pre-2022 historical average. China continues to exert a dominant influence on price discovery. Despite the temporary liquidity vacuum caused by the Lunar New Year holiday, Chinese investment demand grew by **28%** over the past year. Retail participation in the region is shifting from traditional jewelry to investment-grade bullion, fueled by property market weakness and a desire for safe-haven assets. In domestic markets, prices have mirrored global surges, reaching record highs of approximately **₹16,178** per gram for 24K gold. This represents a significant late-month recovery from mid-February lows near **₹15,420**. The "debasement trade"—the migration of capital from fiat currencies to tangible assets—is accelerating as investors hedge against rising global debt and trade uncertainties. Traditional valuation models are largely being ignored as gold trades at a historic premium. The current narrative is driven by geopolitical stress and currency diversification rather than interest rate fundamentals. Market analysts have raised year-end targets, with some institutions projecting prices could reach **$5,400** to **$6,300** if current liquidity levels and investor sentiment persist. The path forward depends on the resilience of these global narratives. Key technical levels to monitor include the **$5,100** support zone and the recent intraday peak of **$5,394**. As long as prices stay above the **$5,000** threshold, the momentum is expected to favor buyers, though the market remains sensitive to shifts in the U.S. dollar and cooling geopolitical tensions.

Shree Ram Twistex IPO Receives 2x Retail Subscription and 9% Grey Market Premium on Second Day

The initial public offering of **Shree Ram Twistex Limited** has moved into its final stages, showing a distinct divide in investor sentiment. As of **February 24, 2026**, the **Rs 110.24 crore** issue has seen a total subscription of approximately **30%** on its second day of bidding. Retail investors continue to drive the momentum, with their portion oversubscribed by **2.04 times**. In contrast, institutional interest remains muted, as **Qualified Institutional Buyers (QIBs)** have yet to record any bids for the **79.50 lakh shares** reserved for them. The **Non-Institutional Investor (NII)** segment has seen a coverage of roughly **65%**. The grey market premium (GMP) has shown a slight upward trend, rising to **Rs 9**. This suggests a potential listing price of **Rs 113**, a premium of approximately **8.65%** over the upper price band of **Rs 104**. IPO Structure and Financials The issue is entirely a fresh offering of **1.06 crore shares** with a price band set at **Rs 95 to Rs 104**. Retail participants can enter with a minimum investment of **Rs 14,976** for a lot of **144 shares**. Shree Ram Twistex, a Gujarat-based manufacturer of cotton and specialized yarns, reported a total income of **Rs 256.32 crore** for the fiscal year ended March 2025. This is an increase from **Rs 231.72 crore** in the previous year. Profit after tax (PAT) for the same period rose to **Rs 8 crore**, up from **Rs 6.55 crore**. Use of Proceeds and Market Outlook The capital raised will be directed toward key operational and sustainability goals: * **Rs 46.85 crore** for setting up a 6.1 MW solar and 4.2 MW wind power plant for captive use. * **Rs 44.00 crore** for working capital requirements. * **Rs 14.89 crore** for the repayment or prepayment of existing borrowings. The company's focus on captive renewable energy is a strategic move to lower high power costs, which currently impact spinning operations. While the textile sector benefits from a favorable **2026-27 Union Budget** and a **Manufacturing PMI of 57.5**, analysts note that the IPO’s valuation at **29x-30x P/E** leaves a limited margin of safety compared to industry peers. Key Dates for Investors The bidding window officially closes on **February 25, 2026**. The basis of allotment is expected to be finalized on **February 26**, with the tentative listing on the **BSE and NSE** scheduled for **March 2, 2026**.

Australian Shares Stable Amid Tariff Concerns and Inflation Data

The S&P/ASX 200 index hovered near 9,024 points today, reflecting a market in a holding pattern as investors navigate a complex mix of global trade tensions and domestic economic signals. The benchmark index slipped approximately 0.02%, remaining remarkably resilient despite significant volatility in overseas markets. Inflation and Interest Rate Focus Market participants are largely sidelined ahead of the January Consumer Price Index (CPI) release. This data is critical following the Reserve Bank of Australia’s recent decision to raise the official cash rate to 3.85% in early February. Current projections suggest headline inflation may peak at 4.2% by mid-2026. While inflation expectations eased slightly to 5.2% in mid-February, the RBA remains on high alert for persistent price pressures in the services and housing sectors. Resource Giants at Record Levels The mining and energy sectors continue to act as the market’s primary engine. BHP Group achieved a historic milestone, with its share price surging past $55.00 for the first time. The global mining giant has gained over 50% since its mid-2025 lows, driven by robust demand for copper and gold. Energy stocks also found favor, with Woodside Energy rising 1.6% to reach its highest level since late 2024. Despite a reported 24% dip in annual profit due to lower global oil prices, the company’s record production levels and optimistic 2026 transition outlook provided a boost to investor confidence. Banking and Tech Divergence The financial sector saw a modest recovery of 0.35%, helping to offset deeper losses elsewhere. However, the broader market was weighed down by sharp declines in interest-rate-sensitive sectors. The Information Technology index plummeted 3.1% during today's session, reaching its lowest point since October 2023. Real Estate followed a similar downward trajectory, falling 1.7% to its lowest valuation since April 2025 as the prospect of "higher-for-longer" interest rates continues to pressure property valuations. Trade Policy Uncertainty Global trade dynamics remain a central concern for Australian exporters. Recent announcements regarding a potential 15% baseline tariff on all U.S. imports have triggered a spike in market uncertainty. Trade Minister Don Farrell has labeled these potential levies as "unjustified," and the government is currently assessing countermeasures. While the Australian Dollar has remained steady near 0.71 US cents, the looming implementation of these trade barriers on February 24 has created a cautious atmosphere for companies with high international exposure. Corporate Earnings Performance * **Monadelphous Group:** Surged 7.48% following a strong half-year result and upgraded revenue guidance for the 2026 fiscal year. * **Adore Beauty:** Witnessed a 24.4% collapse in share price as margin pressures and soft consumer trends overshadowed active customer growth. * **ARB Corporation:** Declined 13.4% after reporting a significant 18.8% drop in pre-tax profits. With heavyweight earnings from Fortescue and Woolworths expected in the coming 24 hours, the index is likely to remain reactive to individual corporate health and the impending inflation report.

Indian Corporate Earnings Growth Projected to Support Market Performance in FY27

Market Brief: India FY27 Earnings Outlook Corporate earnings in India are projected to experience a significant revival in **FY27**, moving past the modest growth seen in recent quarters. Market analysts expect a transition from "strong macros but weak micros" to a more synchronized growth phase. Economic Drivers Nominal GDP growth is a primary catalyst for this shift. After bottoming out in the **8% to 9%** range during FY26, nominal GDP is forecast to climb to **10.5%** in FY27. This acceleration is expected to be fueled by a recovery in the GDP deflator and an inflation rate stabilizing around **4%**. Historically, corporate revenue and profit growth show a high correlation with nominal GDP. Consequently, earnings for the Nifty 50 are projected to accelerate from a sluggish **5% to 6%** in FY26 to a robust **15% to 18%** in FY27. Currency and Sectoral Impact The Indian Rupee has recently faced pressure, trading near the **91.10** mark against the US Dollar. While this depreciation reflects global capital account stress, it serves as a tailwind for export-heavy and dollar-earning sectors. Key beneficiaries of a weaker rupee and improved pricing power include: * **Information Technology & Pharma:** Enhanced margins on dollar-denominated contracts. * **Refining & Metals:** Benefiting from dollar-linked pricing and import substitution. * **Banking:** Supported by healthy credit growth and stable asset quality. AI and Market Sentiment While the earnings outlook is improving, market sentiment remains heavily influenced by global uncertainty surrounding Artificial Intelligence. The terminal value of traditional business models, particularly in IT services, is currently under scrutiny. AI disruption is currently weighing on valuations more than immediate earnings. Investors are grappling with shifts in the IT sector toward outcome-based pricing, though long-term adoption may eventually act as a productivity enabler rather than a pure disruptor. Capital Flows and Manufacturing Foreign Institutional Investors (FIIs) have shown signs of returning, with recent single-day purchases exceeding **₹3,480 crore**. This optimism is supported by resilient private sector activity, with Manufacturing PMI readings remaining positive. The domestic manufacturing cycle is further bolstered by record capital outlay. The defense budget for **FY26-27** has seen a **15%** year-on-year increase, with a capital outlay of **₹2.19 lakh crore** aimed at accelerating domestic production.

Bitcoin Stabilizes Around $63,000 Amid Global Market Decline

The cryptocurrency market is currently navigating a high-velocity de-risking event as of late February 2026. Global risk aversion has intensified, driven primarily by significant shifts in U.S. trade policy. The recent announcement of a 15% global tariff has triggered a broad retreat from speculative assets, sending shockwaves through the digital finance sector. **Bitcoin** is currently struggling to maintain its footing, trading at approximately **$64,120**. This follows a sharp **7.02%** decline over the past week. The asset is testing a critical psychological and technical support zone at **$64,000**. Market analysts warn that a failure to hold this level on a daily closing basis could expose the price to a deeper liquidity cluster near **$60,000**. **Ethereum** has mirrored this downward momentum, sliding to **$1,843**. The second-largest cryptocurrency faces additional pressure from notable founder activity, with reports of roughly **8,800 ETH** in disposals throughout the month. This combination of macro headwinds and internal selling has kept the asset pinned below the **$2,000** resistance mark. The broader market reflects a state of "Extreme Fear," with the Fear & Greed Index crashing to a reading of **11**. This is one of the lowest sentiment readings recorded in recent years. The global crypto market capitalization has retreated to approximately **$2.23 trillion**, marking a significant evaporation of value in a short window. Institutional caution is evident in the derivatives and ETF sectors. Over the last seven days, spot Bitcoin ETFs have seen outflows totaling **$724 million**. In the futures market, the rapid unwinding of leveraged exposure has amplified the volatility. Total network liquidations recently exceeded **$458 million** in a single 24-hour period, with over **92%** of those losses coming from long positions. Trading volumes for major assets have spiked by more than **50%** during this local low, a technical signal that often suggests a period of exhaustion. While the high volume indicates heavy contest at support levels, the prevailing negative bias remains dominant. Investors are closely monitoring the **$63,440** low; a reclaim of higher levels could signal a relief rally, but current structures favor continued consolidation. Macroeconomic uncertainty remains the primary anchor for these conversations. With interest rates staying elevated and the U.S. dollar strengthening, capital continues to rotate into perceived safe havens. Until Bitcoin can reclaim the **$68,500** resistance area, retail and institutional conviction is expected to remain low.

Anthropic AI Expansion Concerns Impact Indian Cybersecurity Stocks

The global cybersecurity sector is currently navigating a period of significant volatility. Stocks in both India and the US have experienced sharp declines following the launch of Claude Code Security by Anthropic. This new AI-powered tool has triggered widespread concern over the potential displacement of traditional vulnerability management and legacy security systems. In the US market, the impact was immediate and broad. Major industry players saw their valuations contract as investors reassessed the competitive landscape. CrowdStrike, Datadog, and Zscaler all recorded drops of approximately 11%. Other prominent firms were also affected, with Fortinet and Okta declining by 6%, and Palo Alto Networks slipping 3%. The Indian market faced even more drastic movements. TAC Infosec hit a 20% lower circuit, while TechD Cybersecurity fell more than 14%. Other domestic firms like Quick Heal Technologies and Sasken Technologies also saw declines ranging from 3% to 5%. These movements reflect a growing anxiety that AI-driven tools could compress the entire vulnerability lifecycle—from discovery to remediation—into a single automated workflow. Anthropic's new tool differentiates itself by moving away from traditional rule-based scanning. Instead, it uses advanced reasoning to map application components and identify logic flaws that human researchers might typically find. During internal tests using the Claude Opus 4.6 model, the company reportedly identified over 500 vulnerabilities in production-level open-source codebases that had previously gone undetected for years. Market analysts are divided on whether this sell-off is a rational repricing or a narrative-driven overreaction. While the new tool is highly effective at code auditing and suggesting software patches, it does not yet address core cybersecurity needs such as real-time endpoint protection, identity management, or zero-trust networking. Despite these distinctions, the sentiment remains cautious. The Global X Cybersecurity ETF recently hit its lowest level since late 2023, falling nearly 5% in a single session. This trend is part of a larger shift where software sectors are being tested by the rapid commercialization of agentic AI and automated defense capabilities. The long-term outlook for the sector may eventually stabilize as these AI tools are integrated into existing platforms. However, for now, the speed of innovation continues to create "headline headwinds," keeping investors on edge as they watch for further signs of structural disruption across the global security landscape.

Vijay Kedia portfolio stocks decline up to 20% amid concerns over AI sector disruption

Market volatility has intensified in the cybersecurity sector following the launch of Anthropic’s new AI security tool, Claude Code Security. This advanced autonomous agent, which identifies and remediates vulnerabilities in open-source software, has triggered a wave of concern regarding the disruption of traditional cybersecurity business models. The impact was felt immediately across the portfolio of prominent investor Vijay Kedia. On Tuesday, shares of TAC Infosec, where Kedia maintains a **9.58%** stake, plummeted to a **20%** lower circuit. TechD Cybersecurity also experienced a sharp decline, falling more than **14%** as investors weighed the competitive threat of AI-driven automated patching against legacy security services. Broader markets have echoed this sentiment. Global cybersecurity leaders saw significant corrections, with CrowdStrike and Cloudflare dropping between **8%** and **10%**. Zscaler and Okta also recorded losses exceeding **5%** and **9%** respectively. These movements reflect a growing investor fear that AI tools capable of reasoning like human researchers may eventually replace human-centric vulnerability management and code auditing. Despite the recent sell-off, some analysts suggest the market reaction may be a "mini-flash crash" driven by headlines rather than immediate operational displacement. While Claude Code Security has reportedly identified over **500** vulnerabilities in active production code, industry experts note that enterprise-grade security still requires independent, battle-tested platforms to handle real-time endpoint protection and identity management. Current data shows TAC Infosec trading at approximately **₹515.00**, reflecting a **15%** decline over the last five trading days. TechD Cybersecurity is currently priced near **₹472.65**, with a one-month return of approximately **-12.84%**. These figures underscore the high volatility in the SME cybersecurity space as emerging AI capabilities continue to redefine the technological landscape. Investor focus remains on how traditional providers will integrate AI to scale their own stacks. While the immediate pressure on stock prices is evident, the long-term outlook for the sector will depend on whether these companies can pivot to complement autonomous AI security or if they will be superseded by the next generation of generative AI agents.

Geopolitical and Tariff Uncertainties Expected to Drive Sustained Market Volatility: Amnish Aggarwal

Market Brief: India Strategic Outlook Indian equity markets are navigating a period of sharp volatility as of **February 24, 2026**. The **BSE Sensex** dropped **718 points** to **82,577** in early trade, while the **NSE Nifty 50** slipped below the **25,550** mark. This cautious sentiment follows a brief relief rally triggered by the US Supreme Court striking down certain reciprocal tariffs, which was quickly offset by a new **15% temporary global tariff** framework introduced by the US administration. Geopolitical tensions in West Asia and ongoing nuclear negotiations involving the US and Iran have further pressured domestic sentiment. Despite these headwinds, the **Nifty PSU Bank** index remains a pocket of resilience, gaining **1.36%** in recent sessions, while the **Indian Rupee** has stabilized near **90.66** against the US dollar. IT Services and the AI Pivot The Information Technology sector faces a dual challenge of trade uncertainty and rapid structural evolution. Heavyweights like **TCS** and **Infosys** saw declines of **3-4%** this week as markets weigh the impact of US trade policies. However, the long-term outlook remains centered on high-value transformation. India's IT industry is on track to reach **$350 billion** by the end of **2026**, contributing nearly **10%** to the national GDP. The focus has shifted from experimental AI pilots to large-scale deployment. Significant infrastructure commitments exceeding **$250 billion** have been secured to power data centers and semiconductor facilities, signaling a move toward "AI-native" service models. Digital Lending and Fintech Maturity Digital lending has emerged as a high-growth pillar within financial services. The market size for digital lending platforms is projected to hit **$23.8 billion** in **2026**, growing at a **CAGR of 23.5%**. The ecosystem has matured beyond simple customer acquisition, with companies now prioritizing retention and regulatory compliance. Underwriting has become increasingly AI-driven, utilizing behavioral data to replace traditional document-based scoring. With **UPI** processing over **16 billion** transactions monthly, embedded finance is now a standard expectation, integrating credit and insurance products directly into e-commerce and retail platforms. Auto Sector and Manufacturing Momentum The automotive industry is entering a phase of volume normalization. While the **2025-26** period saw record highs, growth is expected to moderate to **3-6%** in the coming fiscal year. Passenger vehicle volumes are forecasted to grow by **4-6%**, while the two-wheeler segment may see a **3-5%** increase. Sustainability and premiumization are the primary drivers of value. Electric vehicle (EV) adoption is accelerating, with major players like **Maruti Suzuki** launching mass-market models like the **e VITARA**. Despite potential cost increases of **₹9,000 crore** across the supply chain due to global trade factors, export volumes remain robust, growing at a **4.1% CAGR**. Ferrous Metals and Industrial Commodities The outlook for ferrous metals has improved significantly due to domestic policy support and infrastructure demand. Indian steel prices, which faced pressure in **2025**, are recovering following the imposition of a three-year safeguard duty on flat steel imports. Steel mills implemented price hikes of approximately **₹2,000 per tonne** in early **2026**, with further increases of **₹1,500-2,000** expected. Industrial demand is also being bolstered by the massive expansion of AI data centers, which is projected to drive a **165%** increase in power-related metal requirements by the end of the decade.

IBM Shares Fall 13% Following Anthropic Announcement on AI COBOL Modernization

IBM shares experienced a historic collapse on February 23, 2026, plunging 13.15% in a single session. The sell-off, which wiped out over $31 billion in market value, represents the stock's steepest one-day decline since October 2000. This dramatic move followed an announcement from AI startup Anthropic regarding its new "Claude Code" tool. The startup revealed that its latest AI can effectively modernize COBOL, the legacy programming language that has served as a defensive moat for IBM’s mainframe business for decades. The market reaction stems from fears that AI is finally capable of automating the "investigative and analytical" work required to replace old systems. Traditionally, modernizing COBOL was considered too complex and expensive for most enterprises, keeping them locked into IBM's ecosystem. Anthropic claims its AI can complete analysis in days that previously took human developers months. This threat strikes at the heart of IBM’s Infrastructure and Consulting segments, which recently reported a 67% surge in IBM Z mainframe revenue during the last quarter of 2025. The disruption extended beyond IBM, triggering a broader sell-off in the IT services and cybersecurity sectors. Major players saw significant declines as investors reassessed the value of human-led software maintenance: - CrowdStrike fell roughly 8% - Cloudflare dropped 8% - Okta tanked over 9% - The Global X Cybersecurity ETF hit its lowest level since late 2023 Investor anxiety is focused on "AI cannibalization." While IBM recently reported a generative AI book of business exceeding $12.5 billion, the market is now questioning if this new growth can offset the potential loss of high-margin legacy maintenance revenue. Despite the crash, some analysts suggest the reaction may be an overshoot. They note that while Claude Code can identify and fix over 500 high-risk vulnerabilities, enterprise-grade modernization still requires rigorous human oversight, regulatory compliance, and complex integration that cannot be fully automated overnight. IBM entered 2026 with strong momentum, reporting a total annual revenue of $67.5 billion for 2025. However, the stock is now down roughly 27% month-to-date. The company's ability to defend its modernization funnel against increasingly capable AI agents remains the primary focus for Wall Street as the tech landscape shifts.

Factors Influencing Foreign Institutional Investment Trends in India: Outflow Drivers and Recovery Outlook

Indian equity markets are navigating a complex phase where record domestic inflows act as a vital floor against external volatility. As of February 24, 2026, the Nifty 50 is trading near the 25,480 level, reflecting a cautious sentiment following a 0.9% dip in early session trade. The Sensex is mirroring this trend, currently positioned around 82,480 points. The market remains in a delicate holding pattern as it seeks a definitive end to the earnings downgrade cycle. While valuations have corrected from peak levels of 25x forward earnings to approximately 20x, they remain elevated relative to historical averages. Investors are closely monitoring the shift toward FY28 projections, which are expected to drive the next major valuation reset. Foreign Institutional Investor (FII) activity has shown signs of tactical stabilization. After record annual outflows of 18 billion USD in the previous year, February 2026 has seen a tentative return of foreign capital. Most recently, FIIs recorded a net purchase of 3,483 crore INR in a single session, signaling a potential shift as global interest rates begin to trend lower. Domestic Institutional Investors (DIIs) continue to provide the primary cushion for the market. Strong SIP contributions and insurance flows have created a persistent demand for equities, often offsetting foreign selling pressure. However, these steady inflows have also slowed the pace of price corrections, keeping multiples higher than some analysts anticipated for this stage of the cycle. Sector performance is currently diverging. Financials remain a key anchor, estimated to contribute 46% of incremental index earnings growth through 2028. Conversely, the IT sector is under pressure due to global shifts in technology spending and local currency fluctuations, with major players like Infosys and TCS seeing recent pullbacks. The broader macroeconomic environment is supportive, with India’s GDP growth projected at 7.5% for the current fiscal year. Inflation has moderated significantly, averaging near 2.1%, which has allowed the Reserve Bank of India to maintain an accommodative stance after cumulative rate cuts of 125 basis points. Market participants are now focusing on the roll-forward to FY28 earnings and the potential for a business cycle turn. A sustainable upward move will likely require corporate profit growth to outpace nominal GDP, providing the fundamental justification for current market premiums. [India Market Strategy 2026](https://www.youtube.com/watch?v=ML6czGvdp9Y) This video provides an expert analysis of the latest January market recap and the factors influencing Nifty and Sensex trends for 2026. http://googleusercontent.com/youtube_content/0

US Market Outlook: Impact of Policy Crosscurrents on Wall Street Trends

The U.S. Supreme Court’s February 2026 ruling against the International Emergency Economic Powers Act (IEEPA) has invalidated a significant portion of the current administration’s trade policy. This decision effectively strikes down broad reciprocal duties, removing a projected $2 trillion in revenue over the next decade. While this provides immediate cost relief to some sectors, the Federal Reserve remains cautious, signaling that the ruling's impact on monetary policy may be limited. Despite the judicial setback, the administration immediately announced new 10% global tariffs under Section 122 of the Trade Act of 1974, later increasing the proposed rate to 15%. This shift keeps the effective tariff rate near 14.5%, maintaining upward pressure on consumer prices. The New York Federal Reserve estimates that 90% of previous tariff costs were borne by domestic consumers and businesses, contributing to a persistent inflationary floor. Economic growth for 2026 is currently forecast at 2.4%, though the invalidation of IEEPA tariffs may provide a modest boost by reducing long-run GDP drag from 0.3% to 0.1%. Markets are closely monitoring a potential $160 billion in refunds for "illegally" collected duties. If processed, this would act as a substantial fiscal stimulus, further complicating the Federal Reserve's effort to cool demand. The labor market shows signs of a "low-hire, low-fire" stagnation. While January 2026 nonfarm payrolls added 130,000 jobs—beating expectations—the 12-month average monthly gain has plummeted to 30,000. The unemployment rate currently sits at 4.3%, with the ratio of job openings to unemployed persons falling below 1.0. This cooling trend provides some leeway for the Fed, yet wage growth remains sticky at 3.7% year-over-year. The Federal Reserve held the federal funds rate steady at 3.5%–3.75% during its most recent meeting. Futures markets reflect almost zero chance of a rate cut in March, as core PCE inflation is projected to end the year at 2.4%. While some financial institutions predict two 25-basis-point cuts by December 2026, the potential for new trade barriers and volatile energy prices—with Brent crude recently hitting $71.44 per barrel—keeps the path for easing highly uncertain.

Textile Stocks Decline Up to 6% Amid Market Volatility

Market Brief: Textile Sector Faces Policy Headwinds India’s textile and apparel sector encountered a significant hurdle this week as the government implemented a sharp reduction in export incentives. A sudden notification from the Directorate General of Foreign Trade (DGFT) has restricted benefits under the Remission of Duties and Taxes on Exported Products (RoDTEP) scheme. Effective immediately, the applicable duty refund rates and value caps have been slashed by 50%. This policy shift aims to align with tighter fiscal management, as the budgetary allocation for the scheme was lowered to 10,000 crore for the 2026-27 fiscal year, down from over 18,232 crore previously. Equity Markets React Shares of leading textile exporters felt the immediate impact of the news. During the latest trading sessions, several key players saw a marked decline in valuation: - Gokaldas Exports dropped 5.39% to settle at 746.60 - Pearl Global and Trident witnessed sharp intraday corrections - Sector-wide losses ranged between 4% and 6% Market analysts note that the sentiment shift is particularly pronounced because the industry had recently enjoyed a "golden phase" rally following trade optimism with the US and UK. Export Impact and Industry Concerns The RoDTEP scheme is vital for exporters as it refunds non-rebated taxes and levies incurred during production. Before this cut, refund rates ranged from 0.3% to 3.9% of the export value. These have now been effectively halved to a range of roughly 0.15% to 1.95%. Industry bodies, including the Federation of Indian Export Organisations (FIEO), have urged an immediate review. Exporters argue that the timing is critical due to: - Rising operational and logistics costs - Sluggish global demand and protectionist trends - A widening trade deficit, which hit a three-month high of 34.68 billion in January Economic Context Despite these policy challenges, the Indian textile market remains a cornerstone of the economy, valued at approximately 194 billion for the 2025-26 period. While domestic demand continues to drive 80% of the industry, the government’s Vision 2030 target of 100 billion in exports now faces a steeper climb. Exporters are currently navigating a high-stakes environment where even a 1% shift in costs can determine the loss of international orders to regional competitors. The industry now looks toward potential relief through upcoming Free Trade Agreements (FTAs) to offset the increased fiscal burden.

**US Markets Mixed Amid Tariff Uncertainty and Technology Sector Volatility**

Market Brief: February 24, 2026 Wall Street is navigating a period of intense volatility as a collision of trade policy shifts and technology sector fatigue triggers a defensive rotation. Investors are increasingly favoring safety over growth as uncertainty regarding global tariffs and corporate debt stability takes center stage. **Equity Markets and Tech Outlook** The technology sector is under significant pressure, with the software index retreating roughly 20% year-to-date. Concerns are mounting over the long-term viability of traditional software business models as generative AI disruption begins to materialize. Investors have specifically sold off major tech names, leading to a sharp downturn in broader indices. Corporate earnings remain a focal point. While the technology sector is projected to lead annual earnings growth with a 32.3% increase, the high capital expenditure required for AI infrastructure—estimated at $600 billion for the top five hyperscalers in 2026—is raising questions about immediate return on investment. **Trade Policy and Geopolitical Impacts** Global trade remains sensitive to shifting tariff landscapes. Although the U.S. Supreme Court recently struck down certain sweeping global tariffs, the administration’s immediate pivot to a temporary 15% import tariff on all countries has kept markets on edge. These developments have contributed to a "sticky" inflation environment, complicating the Federal Reserve's path toward interest rate cuts. Geopolitical tensions, particularly involving U.S. military postures in the Middle East and South America, are further driving the flight to safety. **Safe-Haven Assets** Gold continues its historic rally, maintaining resilience near the $5,000 per ounce level. Analysts project the precious metal could reach $5,400 per ounce by late 2027, supported by sustained central bank demand and record inflows into gold-backed ETFs. For the first time since 1996, gold has surpassed U.S. Treasuries as a share of global central bank reserves. U.S. Treasuries are also seeing heightened activity. The New York Fed is conducting Treasury security purchase operations to manage liquidity, while 10-year yields fluctuate in response to shifting expectations for a May rate cut. **Credit Market Stress** The private credit market is signaling distress, specifically within U.S. software exposure. Software firms are reportedly delaying debt deals as borrowing costs rise and lenders intensify scrutiny. Approximately 50% of software sector loans now hold a rating of B- or lower, indicating a high risk of default. Defaults in this segment are projected to rise between 3% and 5% if AI-driven market disruptions accelerate through 2026. Refinancing pressure is building, as the capacity of primary bond markets to absorb massive tech issuance is being tested.

Mixed Outlook for IDFC First Bank and IT Sector Amid Near-Term Risks

The Indian equity landscape is witnessing a sharp divergence between traditional tech services and the banking sector. While global anxieties regarding artificial intelligence (AI) and trade tariffs have battered tech stocks, the banking space remains a primary focus for long-term growth, despite recent localized volatility. IT Sector: Assessing the Oversold Territory Market sentiment toward the IT sector has reached a multi-month low. The Nifty IT index has plummeted nearly **21%** over the past month as of late February 2026. This correction is fueled by fears that AI-led automation is rapidly disrupting legacy programming and maintenance roles. Despite the negative headlines, valuations for major tech players have become increasingly attractive. Analysts suggest the current "panic selling" may be overstating the speed of disruption, creating a window for investors to accumulate high-quality tech assets at a significant discount. Banking: A Tale of Two Tiers The banking sector is currently split between high-performing heavyweights and mid-tier lenders facing regulatory and internal hurdles. State Bank of India (SBI) recently made history by becoming India's second-largest bank by market capitalization, overtaking ICICI Bank after a **7%** surge in its share price to an all-time high of **₹1,136.85**. While ICICI and HDFC Bank remain fundamental favorites with strong credit expansion outlooks, mid-tier lenders are under intense pressure. IDFC First Bank and AU Small Finance Bank have seen a combined erosion of over **₹16,000 crore** in market value this week. This follows a **₹590 crore** fraud disclosure at an IDFC First branch, leading to the Haryana government de-empanelling both lenders. IDFC First shares hit a **20%** lower circuit, while AU Small Finance dropped over **7%**. Experts advise a "wait-and-watch" approach for these specific names until forensic audits are complete. Tobacco: Navigating the Tax Shock Cigarette stocks are navigating a volatile transition following the implementation of a new excise duty regime on February 1, 2026. The new structure introduced specific duties ranging from **₹2,050 to ₹8,500** per 1,000 sticks, alongside a **40%** GST rate. Initial market reaction was negative, with stocks like ITC and Godfrey Phillips seeing sharp declines. However, companies have demonstrated significant pricing power. ITC recently implemented price hikes of up to **41%** on premium brands like Gold Flake to protect margins. While this offsets tax costs, the risk of "downtrading" to cheaper alternatives or illicit products remains a primary concern for the sector. Strategic Outlook The broader market is currently range-bound, with Nifty support identified near the **25,000** level. Investors are shifting focus toward large-cap private banks and resilient PSU lenders as a hedge against global tech volatility. The resilience of the "Big Three"—SBI, HDFC, and ICICI—continues to underpin the financial sector, even as global headwinds from U.S. tariff uncertainties and geopolitical tensions keep the overall market atmosphere cautious.

India Targets $19.7 Billion via State-Run Firm IPOs by 2030

India is accelerating its transition toward a high-efficiency economy with the launch of the National Monetisation Pipeline (NMP) 2.0. This second phase, spanning from fiscal year 2026 to 2030, sets an ambitious target to generate 16.72 trillion rupees. This figure represents a massive 2.6-fold increase over the previous pipeline, underscoring the government's aggressive push to unlock value from existing brownfield infrastructure. Approximately 5.8 trillion rupees of this total is expected to come from private sector investments. A critical component of this drive is the 1.79 trillion rupees (approximately $19.7 billion) earmarked for Initial Public Offerings (IPOs) of state-run firms by 2030. The railways sector leads this effort, with plans to divest stakes in seven companies to raise 837 billion rupees. For the upcoming 2026-27 fiscal year alone, the government targets 170 billion rupees from new market listings. The power sector is another heavy lifter, with 310 billion rupees projected from the listing of various subsidiaries. This includes high-profile units like NTPC Green Energy, which is preparing for a significant market entry to fund its 60-GW renewable energy target. Coal India and NLC India are also expected to contribute 483 billion rupees through the public offering of their subsidiaries and green energy assets. Beyond energy and transport, the aviation and petroleum sectors are key pillars of the plan. The Airports Authority of India is scheduled to sell stakes in its subsidiaries and joint ventures, while GAIL GAS is positioned for a 31 billion rupee listing in the 2027-28 window. These moves are designed to shift public enterprises from traditional state management to a "value creation" model. The momentum is supported by a surge in the PSU sector's market performance. The combined market capitalization of listed public firms has soared from 12 trillion rupees in 2020 to nearly 69 trillion rupees as of early 2026. This growth, driven by cleaner balance sheets and improved corporate governance, now accounts for roughly 15% of India’s total equity market value. Investors are keeping a close watch on these developments as the government simplifies processes to make asset monetisation seamless. By reinvesting these proceeds into the National Infrastructure Pipeline, the state aims to maintain a real growth rate near 7% while modernizing core sectors without increasing fiscal strain.

AI Disruption Concerns Impact Debt Financing and US Software Equity Performance

Software companies are entering a period of significant financial recalibration as of February 2026. Higher borrowing costs and intensified lender scrutiny have led many firms to delay or abandon debt fundraising efforts. The software sector is currently facing a sharp divide. While the broader tech industry reached record debt issuance levels in 2025, representing 16.7% of global non-financial corporate bonds, smaller and riskier software firms are hitting a wall. Lenders are increasingly concerned that rapid AI advancements could dismantle existing software-as-a-service (SaaS) business models. This anxiety is manifesting in credit spreads, which have widened by 20 to 50 basis points for software names in recent weeks. Market data shows that approximately 50% of software sector loans now carry B- or lower credit ratings. This concentration of high-risk debt has made lenders cautious, with many demanding stricter covenants and higher yields to protect against potential AI-driven defaults. The "maturity wall" is becoming a critical focus. While only 0.5% of software loans are due for refinancing in 2026, that figure jumps to 6% in 2027 and peaks in 2028. This upcoming surge is forcing companies to preserve cash now rather than seeking new credit in an expensive market. Interest rates for business loans remain elevated, with average rates ranging from 10.75% to 22.50% depending on credit quality. These high costs are particularly difficult for software firms whose products are perceived as easily replicable by new AI coding agents. The private credit market, which holds an estimated $600 billion to $750 billion in software exposure, is under localized strain. This has led to a noticeable slowdown in new financing deals as firms wait for market stability and clearer signs of which business models will survive the AI shift. In contrast, "hyperscalers" and massive infrastructure providers are borrowing heavily to fund AI development, raising over $121 billion in 2025 alone. This massive capital absorption by top-tier firms is further crowding out smaller software borrowers. For mid-sized and smaller software entities, the current strategy is one of "wait and see." Management teams are prioritizing operational efficiency over debt-fueled growth, aiming to strengthen balance sheets before the 2027 refinancing cycle begins.

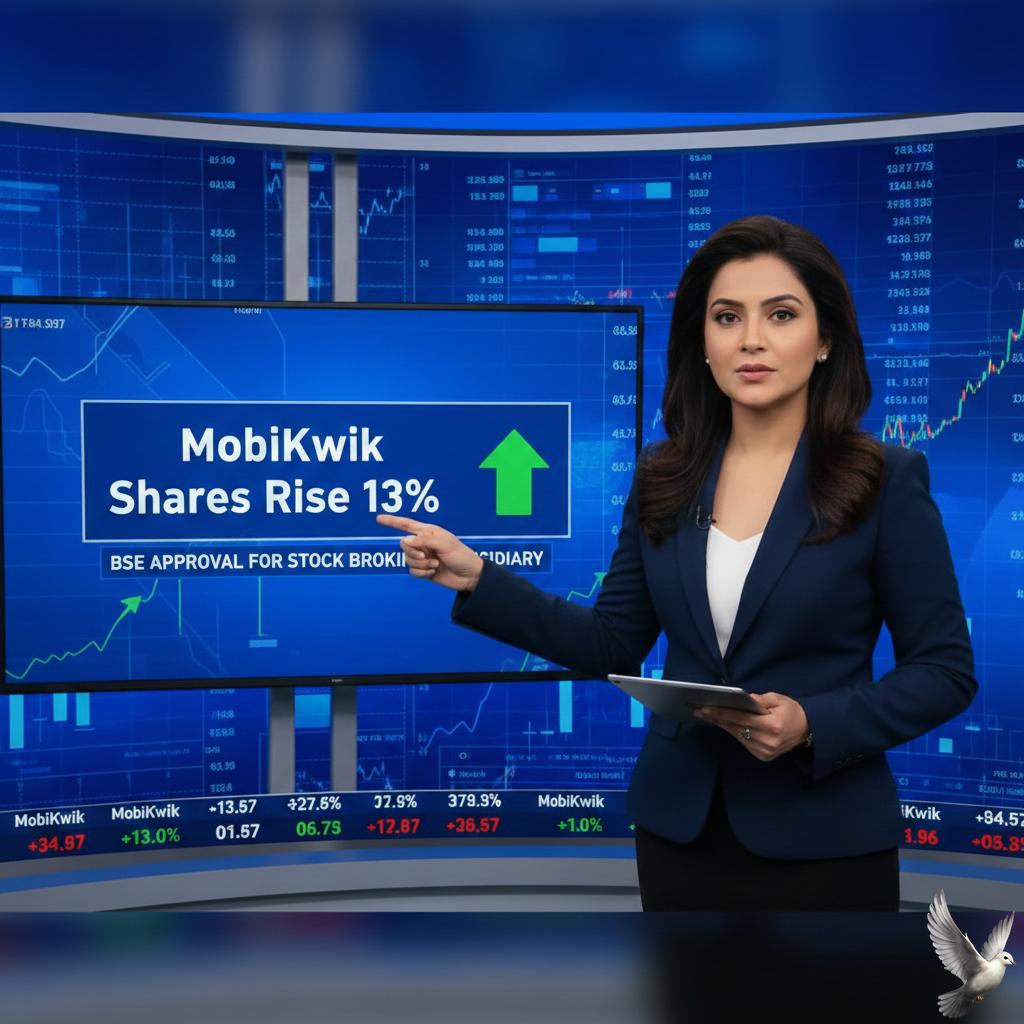

MobiKwik Shares Rise 13% Following BSE Approval for Stock Broking Subsidiary

MobiKwik Market Brief: February 24, 2026 **MobiKwik** shares experienced a significant surge today, climbing as much as **12.6%** to reach an intraday high of **227.37** on the NSE. This rally follows a pivotal regulatory milestone for the fintech firm’s expansion into broader financial services. Strategic Expansion into Stockbroking The primary catalyst for today's price action is the formal approval from the **Bombay Stock Exchange (BSE)** for MobiKwik's wholly-owned subsidiary, **MobiKwik Securities Broking Private Limited**, to commence stockbroking operations. Effective today, **February 24, 2026**, the subsidiary is authorized to facilitate the buying, selling, and settlement of equity trades. This move follows the initial registration granted by **SEBI** in July 2025 and positions MobiKwik to compete directly with established wealth-tech platforms. Financial Turnaround and Valuation The company recently reported a move toward profitability, a key shift for its long-term market sentiment. For the quarter ending December 31, 2025 (**Q3 FY26**), MobiKwik recorded: * **Net Profit (PAT):** 40.48 million, reversing a major loss from the previous year. * **Total Income:** 2,972.20 million, marking an **8%** year-on-year increase. * **Payments GMV:** Hit an all-time high of **481 billion**. * **UPI Transactions:** Grew **3.2x** year-on-year. Despite the recent **13%** surge, the stock continues to trade significantly below its historical levels. The current price near **217** remains well under the initial IPO price band of **265 – 279** and the 2024 listing debut price of approximately **442**. Market Context and Outlook The broader fintech sector in early 2026 is shifting focus from pure user acquisition to high-margin financial services. MobiKwik's entry into stockbroking aligns with this industry-wide trend toward **WealthTech** and credit distribution. While the stock has declined roughly **35%** over the past year, today's volume spike—with over **10 million** shares traded on the NSE alone—indicates renewed investor interest following the completion of these regulatory steps. The company currently maintains a market capitalization of approximately **1,650 crore**, with management focusing on a "risk-first" approach to digital lending and sustainable margin expansion in its new broking vertical.