Neutral News

Collection

Foreign Portfolio Investors Withdraw ₹27,000 Crore from Indian Equities in May as Total 2026 Outflows Reach ₹2.2 Lakh Crore Mark

Foreign capital outflows from Indian equity markets have accelerated sharply, signaling systemic risk aversion among offshore fund managers. According to data from the National Securities Depository Limited, Foreign Portfolio Investors have pulled out a net **₹27,048 crore** from domestic shares during May. This latest wave of liquidation pushes the cumulative foreign capital outflow from Indian equities to a substantial **₹2.2 lakh crore** for the current calendar year. This aggressive selling cycle has completely outpaced the total liquidation observed during the preceding calendar year, when overseas investors withdrew a total of **₹1.66 lakh crore**. Market tracking shows that foreign institutional participants have maintained a net selling posture across almost every month of the year. The year opened with a net equity liquidation of **₹35,962 crore** in January. A short-lived trend reversal occurred in February, yielding a temporary net inflow of **₹22,615 crore**, which marked a **17-month** peak for monthly foreign capital deployment. However, that momentum dissolved rapidly. March witnessed a historic capital migration with a record **₹1.17 lakh crore** exiting Indian shares. This aggressive offloading was closely followed by a further **₹60,847 crore** net reduction in equity exposure during April, establishing the groundwork for the ongoing capitulation through May. According to market research analysts at Morningstar Investment Research India, this continuous disinvestment cycle reflects deeply entrenched anxieties regarding global macroeconomic growth stability. The institutional pulling back is heavily driven by lingering concerns over global inflation trajectories, which continue to muddy the timing and magnitude of future interest rate interventions by major western central banks. Furthermore, persistent geopolitical instability in critical energy corridors has introduced structural volatility into global crude oil pricing. With crude values maintaining an upward bias, risk appetite toward energy-dependent emerging markets has experienced a sharp contraction. Compounding these structural challenges are two significant global fixed-income factors. Robust developed-market sovereign bond yields and a notably stronger US dollar index have meaningfully altered capital allocation mathematics. Higher, risk-adjusted yields available in developed credit jurisdictions are prompting large macro funds to implement defensive asset reallocation strategies. The continuous outflow of foreign portfolio capital has also altered domestic currency dynamics. Large-scale capital repatriation has widened the current account deficit, triggering a visible depreciation in the domestic currency. The Indian rupee recently experienced downward pressure, touching an all-time low of **95.80** against the US dollar, which has materially reduced dollar-denominated returns for international fund managers.

Analysis of 5 Small-Cap Stocks Reaching 52-Week Highs with Monthly Gains Up to 50%

The global energy sector enters late February 2026 defined by a "double-track" momentum: a persistent supply surplus in traditional fossil fuels and an unprecedented acceleration in electricity demand driven by the digital economy. Crude Oil and Liquid Fuels The crude oil market is currently navigating a period of downward price pressure. Brent crude is trading near **$69.67** per barrel, while WTI sits at **$64.34**. This reflects a year-on-year decline of approximately **5% to 8%**. A significant supply surplus is the primary driver of this trend. Global inventories reached a four-year high of **8.03 billion barrels** at the start of the year. Analysts project this surplus could expand by **2 million to 3.7 million barrels per day** throughout 2026. Despite this bearish outlook, prices remain sensitive to a "geopolitical premium." Tensions in the Middle East and supply disruptions in Kazakhstan have prevented a steeper collapse. However, major financial institutions have lowered their year-end forecasts, with some expecting Brent to settle in the **$55–$60** range by the fourth quarter. Natural Gas and LNG Natural gas markets are showing signs of stabilization following the volatility of early winter. US Henry Hub futures are trading around **$2.79 per MMBtu**, down nearly **60%** from the peaks seen during January’s winter storms. In Europe, TTF prices have softened to approximately **$11.30 per MMBtu**. This is supported by healthy storage levels, which currently sit at **34.4%**—an improvement over previous crisis years but still below the five-year average. The long-term outlook for gas is defined by a massive expansion in liquefaction capacity. Global LNG supply is expected to rise by **7%** this year alone. This influx of "new molecules" is projected to drive European and Asian prices below **$10 per MMBtu** by late 2026. Power Markets and Grid Infrastructure The International Energy Agency has labeled 2026 the beginning of the "Age of Electricity." Global power demand is rising at **3.6%** annually, outstripping general economic growth for the first time in decades. This surge is fueled by three factors: the rapid build-out of AI data centers, record electric vehicle sales, and rising cooling needs in emerging economies. China and India are the primary engines of this growth, with India’s peak load rising by over **50%** compared to mid-decade levels. To meet this demand, the world is adding roughly **664 GW** of solar and wind capacity this year. Renewable generation now accounts for more than **one-third** of the global power mix. Key Economic Indicators Market participants are closely watching several critical metrics that define the current landscape: * **125 GW**: The amount of new energy storage capacity being added annually. * **13.7 million bpd**: Current US weekly crude oil production, maintaining record highs. * **20%**: The projected increase in transmission and distribution costs by 2030 due to grid upgrades. * **$4.31**: The forecasted average Henry Hub spot price for the full year 2026. The transition is creating a "molecule competition" where traditional gas infrastructure is being rapidly repurposed. New policy frameworks are accelerating the conversion of pipelines for hydrogen transport, while carbon capture networks are moving from pilot stages to industrial-scale reality in the North Sea and North America.

Anthropic’s AI Suite Launch Correlates with Significant Monthly Market Cap Decline in IT Sector

The Indian IT sector is navigating a period of intense volatility as of February 26, 2026. The Nifty IT index experienced a historic **21%** decline throughout the month, marking its steepest monthly contraction since the 2008 global financial crisis. This massive selloff was primarily ignited by rapid advancements from AI startup Anthropic. The launch of specialized tools capable of automating legal workflows and streamlining legacy **COBOL** code has raised urgent questions regarding the long-term viability of traditional IT service models. Market Performance and Valuation The Nifty IT index reached a significant low of **30,053** earlier this week, representing a **30-month** bottom. While the index showed a slight recovery of **0.89%** today to trade around the **30,797** level, the structural outlook remains cautious. Valuations for the sector have retreated to an eight-year low relative to the broader Nifty 500. Major firms are currently trading at price-to-earnings (P/E) multiples between **14** and **18** times, offering free cash flow yields of **4%** to **6%**. Disruption Risks and Stock Impact The primary catalyst for the "Software-mageddon" was Anthropic’s ability to target the high-margin maintenance of legacy systems. With an estimated **95%** of US ATM transactions still relying on **COBOL**, the automation of these processes threatens a core revenue stream for global and Indian providers. The impact on individual heavyweights has been severe: * **HCLTech** declined nearly **22%** over the past month. * **Infosys** and **TCS** saw single-day losses ranging from **4%** to **7%** following major AI announcements. * **Persistent Systems** and **Coforge** led intraday losses of up to **8%** during the height of the selloff. Strategic Shifts and Outlook Despite the downturn, some institutional analysts have shifted to an "Overweight" stance, viewing the correction as an entry point for long-term investors. They argue that the market has already priced in anemic growth scenarios, with potential three-year returns projected between **13%** and **25%** in a recovery case. The sector's resilience now depends on how quickly firms can pivot. Infosys recently announced a strategic partnership with Anthropic to develop enterprise AI solutions, a move that briefly triggered a **3%** relief rally. However, the broader trend shows foreign portfolio investors remaining net sellers of Indian IT stocks as they recalibrate for an AI-first economy. The industry is at a crossroads where legacy contract deflation must be offset by new AI transformation projects. Until clear strategies for AI enablement are proven, the sector is expected to face continued pricing pressure and scrutiny over billable hours.

US Stock Market Remains Steady as Investors Await Fed Interest Rate Decision

U.S. monetary policy remains at a critical juncture as of February 2026. Federal Reserve officials are currently navigating a "low-hire, low-fire" economic environment, characterized by a cooling labor market and inflation that remains stubbornly above the long-term target. The effective federal funds rate is currently holding steady at **3.64%**. This follows a period of significant adjustments, including **175 basis points** of cumulative rate cuts since late 2024. The target range established in late January sits between **3.50% and 3.75%**. St. Louis Fed President Alberto Musalem maintains that current policy is well-positioned. He describes a state of "tension" between the Fed’s two primary goals. While the labor market appears to have stabilized with an unemployment rate of **4.3%**, Musalem notes that inflation is still running nearly a full percentage point above the **2%** target. Recent data places headline inflation at **2.4%**, while core inflation—which excludes volatile food and energy costs—is slightly higher at **2.5%**. Musalem identifies recent tariffs as a key driver, contributing roughly **0.5%** to current excess inflation. He expects these pressures to fade as the year progresses. Kansas City Fed President Jeffrey Schmid remains more cautious. As a prominent dissenter in previous rate-cut decisions, Schmid emphasizes that overly high inflation remains the central bank's most pressing problem. He acknowledges the health of the employment sector but insists that more work is required to ensure price stability. The labor market showed unexpected resilience in January 2026, adding **130,000 jobs**, which significantly outpaced economist forecasts of **70,000**. Despite this jump, the broader trend is one of moderation; average monthly gains over the last year have slowed to approximately **30,000**, a sharp decline from the **103,000** average seen in early 2025. Policymakers are also monitoring the Fed's balance sheet, which has been reduced to approximately **$6.5 trillion** from its peak of nearly **$9 trillion**. While the pace of reduction has halted, officials continue to debate the appropriate level of liquidity needed to maintain stability in the banking system. Market expectations are currently divided. While some officials favor a prolonged pause to monitor the effects of previous cuts, others suggest that further reductions of **25 basis points** could be on the table by mid-2026 if labor market risks intensify or if inflation continues its slow descent toward the target.

Fed Official Cites AI Impact on Labor Market and Productivity

Federal Reserve Governor Lisa Cook highlighted a generational transformation in the U.S. labor market this Tuesday, driven by the rapid adoption of artificial intelligence. Cook warned that this shift could create a structural rise in unemployment that traditional monetary policy might struggle to resolve. The U.S. unemployment rate currently sits at **4.3%** as of January 2026. While this remains low by historical standards, the central bank is monitoring "churn" in specific sectors. Entry-level hiring and professional fields like coding are already seeing reduced demand as firms deploy AI for routine tasks. A key concern for the Fed is that AI-driven job displacement may occur before new roles are created. If the unemployment rate rises because of a productivity-driven reorganization of work rather than a drop in consumer demand, lowering interest rates could prove ineffective. Standard demand-side tools—like cutting the federal funds rate, which is currently held between **3.5%** and **3.75%**—might actually stoke inflation if the labor market issues are structural rather than cyclical. This presents a difficult "trade-off" for policymakers trying to balance employment with the Fed’s **2%** inflation target. Current data shows that while overall hiring has cooled, AI-related job postings have grown to represent **4.2%** of all listings. Employers are increasingly willing to pay a premium for AI skills, with some roles commanding salaries **8.5%** to **23%** higher than non-AI counterparts. Investment in AI infrastructure remains aggressive despite elevated borrowing costs. Business spending on data centers and advanced chips has surged, suggesting that the "neutral" interest rate—the level that neither stimulates nor slows the economy—may be higher than in previous decades. Governor Cook noted that the "most significant reorganization of work in generations" is underway. In this environment, non-monetary solutions such as workforce retraining and education policy may become more critical than interest rate adjustments in supporting displaced workers.

Nifty IT Index Records Largest Monthly Decline Since 2008 Amid Market Volatility

The Nifty IT index has entered a phase of historic volatility, plunging over 21% in February 2026. This mark represents the sector’s worst monthly performance since the 2008 global financial crisis. On February 24 alone, the index tanked another 6%, wiping out approximately 5.05 lakh crore in investor wealth within a single month. The primary catalyst for this rout is a "perfect storm" of AI-driven disruption and global trade uncertainty. Fears intensified after tech startup Anthropic demonstrated its Claude tool’s ability to modernize legacy COBOL code. This breakthrough has raised alarms that long-standing revenue streams from managed services—the backbone of Indian IT—could be rapidly automated or made obsolete. Market heavyweights have faced significant selling pressure. On the latest trading day, HCLTech and Tech Mahindra dropped as much as 6% to 7%. Infosys and Tata Consultancy Services (TCS) also recorded steep declines of 4% to 6%, pushing their stock prices to multi-year lows. Beyond AI concerns, a new wave of global macro pressure has hit the sector. Renewed global trade tensions and fresh tariff remarks from the U.S. administration have sparked fears of reduced discretionary spending. Since Indian IT firms derive the majority of their revenue from the U.S. and Europe, any threat to international trade flows directly impacts their growth outlook. Valuations for the sector have now dropped to an eight-year low relative to the Nifty 500. While some contrarian investors see this as a value opportunity, institutional sentiment remains cautious. Foreign Institutional Investors (FIIs) have been net sellers, pulling out over 10,950 crore from the IT sector in early February alone. Analysts suggest that while the sector is trading at a more attractive Price-to-Earnings (P/E) ratio of approximately 21.5x—near its 10-year average—cheap valuations may not be enough. The industry is facing a structural shift where traditional application maintenance is expected to shrink, potentially denting overall revenues by 10% to 12% over the next few years. Market experts emphasize that the next phase for Indian IT will depend on how quickly these companies can pivot to AI-led consulting and innovation. For now, the lack of a clear execution roadmap to protect revenue moats is keeping the outlook cloudy. Investors are advised to seek clarity on long-term growth before making decisive moves into the sector.

Gold and Silver Prices Decline Amid US Dollar Strength and Tariff Uncertainty

MCX Metals Brief: February 24, 2026 Precious metals are navigating a landscape of intense volatility. Gold and silver prices on the MCX saw a modest pullback in early Tuesday trade as investors balanced a resilient U.S. Dollar against escalating global trade uncertainties and geopolitical friction. Current Market Rates MCX Gold futures for April delivery are trading near **₹160,615** per 10 grams, a slight dip of **0.55%** from the recent peak. Despite this morning's minor correction, gold remains in a powerful uptrend, having recently surged past the psychological barrier of **₹161,000**. Silver has mirrored this volatility, with MCX futures trading near **₹264,327** per kg. This follows a dramatic 24-hour window where spot silver prices in major Indian cities like Delhi and Mumbai surged by nearly **₹25,000** to hit the **₹3,00,000** per kg milestone. Core Market Triggers The primary driver remains the shifting U.S. trade policy. Recent court rulings against emergency tariffs were quickly met with new executive orders proposing a **10% to 15%** global tariff. This "tariff chaos" has sent investors rushing toward safe-haven assets. In Asia, the reopening of Chinese markets after the Lunar New Year break is providing a "sentiment reset." China's return to the market typically increases liquidity, though it has also introduced a "liquidity vacuum" that exaggerated price swings over the last week. International Context On the global stage, Spot Gold is hovering around **$5,150** per ounce, cooling slightly from a one-month high of **$5,200**. The U.S. Dollar Index (DXY) remains a critical factor; while it has shown recent resilience, it is trading near four-year lows, providing a long-term floor for bullion prices. Technical Outlook and Targets Analysts maintain a "buy on dips" stance. For gold, immediate support is identified at **₹154,200**, with upside targets fixed at **₹155,500** and **₹156,300** for short-term traders. A stop loss is recommended at **₹153,300**. Silver exhibits a wider trading range. Support is currently pegged at **₹237,000**, while resistance stands at **₹252,000**. If momentum breaks above **₹290,000** again, a retest of higher levels is anticipated. The gold-silver ratio has recently compressed from **100x** to approximately **64x**, signaling that silver is attempting a catch-up rally relative to gold’s consistent performance throughout February.

Insurance-Linked Securities Under Development for Risk Diversification

The International Financial Services Centres Authority (IFSCA) is advancing a specialized regulatory framework to institutionalize Insurance-Linked Securities (ILS) and catastrophe bonds within the GIFT-IFSC jurisdiction. Chairman K. Rajaraman recently confirmed that the authority will approach the central government within the next two months to operationalize Special Purpose Vehicle (SPV) structures. This initiative is designed to bridge a significant protection gap for climate and natural catastrophe risks in Asia. Current data indicates that approximately 84% of economic losses in the region remain uninsured, leaving only 16% covered by traditional means. By introducing Special Purpose Insurers (SPIs), the IFSCA aims to tap into global institutional capital, moving beyond the limits of traditional reinsurance. The global appetite for these instruments is currently at an all-time high. The catastrophe bond market closed 2025 with a record-breaking $24 billion in new issuances. Market projections for 2026 suggest total volumes could reach $70 billion as $13.8 billion in existing bonds mature and are reallocated. Investors are seeing competitive performance in this sector. The Swiss Re Cat Bond Index posted gains of 11% in the past year, matching the performance of the MSCI World Index and significantly outperforming U.S. corporate bonds. Spreads currently sit at approximately 6.5% over U.S. Treasury rates, remaining well above the historical average of 5%. Key drivers for this surge include rising inflation, which has increased property rebuilding costs by roughly 50% over the last five years. This has forced insurers to seek alternative risk transfer mechanisms. The market is also diversifying its risk mix, with 16 first-time issuers entering the space recently to cover unconventional perils like cyber risks and wildfires. To support this ecosystem, the IFSCA has notified the Fund Management (Amendment) Regulations 2026. These updates simplify compliance for intermediaries and offer a 24-month transition window for appointing IFSC-based custodians. The goal is to create a future-ready jurisdiction that allows private equity firms and institutional investors to diversify portfolios while stabilizing the broader insurance industry.

IDFC First Bank Reports Branch Fraud Involving Employees and External Parties

Market Brief: IDFC First Bank Branch Fraud Discovery **IDFC First Bank** has disclosed a significant fraudulent incident involving unauthorized transactions totaling **590 crore**. The activity was localized at a single branch in **Chandigarh** and primarily targeted accounts belonging to the **Haryana Government**. The fraud came to light when a government department requested an account closure, revealing a discrepancy between the department’s records and the actual bank balance. Mechanics of the Breach The bank’s initial assessment points to a sophisticated manual breach rather than a digital system failure. Transactions were executed using **forged cheques** and fraudulent authorization letters. The bank has characterized this as an isolated case of **collusion** between certain branch employees and external third parties. This internal connivance allowed the perpetrators to bypass standard "maker-checker" protocols and manual verification steps. Response and Recovery Efforts * **Personnel Action**: Four bank officials have been suspended pending a detailed investigation. * **Audits**: The bank has appointed **KPMG** to conduct an independent forensic audit to determine the full scope of the breach. * **Asset Recovery**: Recall requests have been sent to beneficiary banks to mark liens on suspicious accounts. * **Legal Action**: Strict criminal and civil proceedings are being initiated against all involved internal and external parties. Financial and Market Context Despite the **590 crore** impact, the bank maintains that the event is manageable given its current capital position. For **Q3 FY26**, IDFC First Bank reported a standalone net profit of **502.5 crore**, representing a **48% year-on-year increase**. The bank's **Gross NPA** has improved to **1.69%**, while its **CASA ratio** remains strong at **51.6%**. As of **February 23, 2026**, the stock is trading near **83.51**, reflecting a **1-year return of approximately 36%**. Market capitalization remains robust at over **71,800 crore**. Strategic Outlook Management emphasizes that this is not a systemic technology issue. The bank continues its transition from a wholesale-heavy book to a retail-focused model, with **80%** of its portfolio now diversified across retail and MSME segments. Future focus will likely intensify on **behavioral biometrics** and enhanced internal surveillance to prevent manual overrides of security protocols at the branch level.

Supreme Court Decision Overturning U.S. Tariffs May Influence Treasury Market Volatility

In a landmark 6-3 decision on **February 20, 2026**, the U.S. Supreme Court struck down a central pillar of the administration's trade policy. The court ruled that the **International Emergency Economic Powers Act (IEEPA)** of 1977 does not grant the president authority to levy duties, as the power to tax remains a strictly congressional prerogative. The ruling immediately nullified several sweeping measures, including the **25%** tariffs on Canadian and Mexican goods and the "reciprocal" tariffs that reached as high as **50%** for certain trading partners. Chief Justice John Roberts clarified that while the president can regulate imports during emergencies, the law is silent on the specific power to impose taxes or surcharges. The fiscal implications are substantial. Current estimates suggest the government may be required to refund between **$150 billion** and **$200 billion** to importers who paid these illegal duties. Independent budget groups warn that without the projected IEEPA revenue, federal debt could climb to **125%** of GDP by 2036, adding roughly **$2.4 trillion** to the long-term national deficit. Within hours of the decision, the White House announced a shift in strategy. The president signed a new executive order to impose a **10%** global baseline tariff under **Section 122** of the Trade Act of 1974. This authority allows for a temporary "import surcharge" during balance-of-payments emergencies for a period of **150 days**. Market reactions remained cautious yet resilient. The **S&P 500** closed up **0.69%** following the news, buoyed by the prospect of corporate refunds for automakers and consumer goods retailers. However, tech and industrial sectors—heavily reliant on global supply chains—face renewed uncertainty as the administration launches fresh trade investigations under **Section 301** to find more permanent legal footing for duties. Treasury Secretary Scott Bessent has downplayed the long-term fiscal damage. In recent statements, he projected that the pivot to a **10%** blanket tariff and other legal alternatives will result in "virtually unchanged" revenue for **2026**. Bessent maintains a growth forecast of at least **3.5%** for the coming year, arguing that domestic tax breaks and falling energy prices will offset the trade-related volatility. For households, the landscape remains complex. While the removal of illegal tariffs could offer relief, the new **10%** surcharge is expected to result in an average tax increase of approximately **$1,300** per household in 2026. Global trading partners, including India and China, are now recalibrating as the average effective U.S. tariff rate is projected to settle at roughly **4.5%** under the new legal framework.

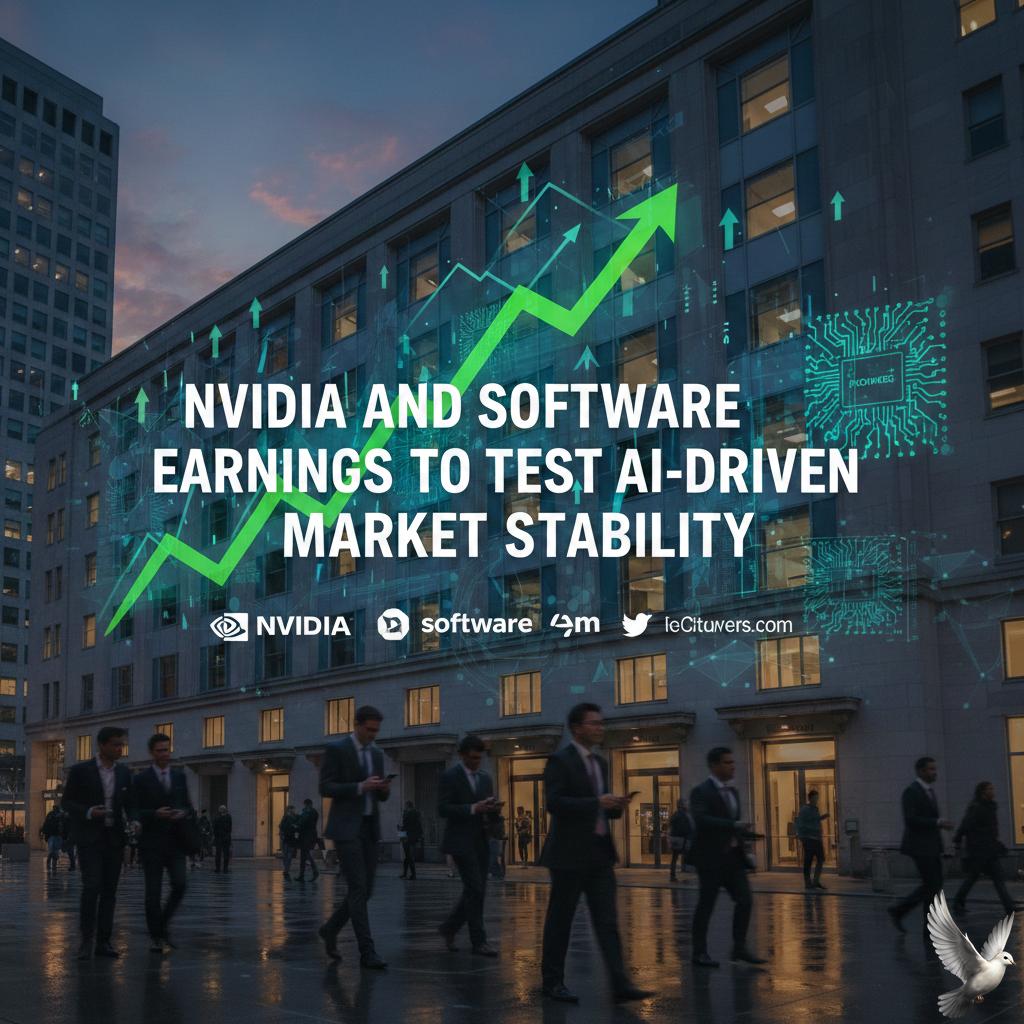

Nvidia and Software Earnings to Test AI-Driven Market Stability

Nvidia and the AI Benchmark Global markets are currently locked in a waiting pattern as **Nvidia** prepares to release its fourth-quarter fiscal 2026 results on **Wednesday, February 25**. As the world’s most valuable company and a primary engine for AI infrastructure, its performance is seen as a survival signal for the broader tech sector. Analysts expect a significant report, with revenue projected to reach **$65.5 billion**—a massive jump from the **$35.1 billion** recorded just one year ago. Earnings per share (EPS) are forecasted at approximately **$1.52**. The options market is currently pricing in a price swing of **7% to 8%** in either direction following the announcement. Software Sector Turmoil While chipmakers remain in high demand, the software industry is navigating a brutal transition. The **MSCI Software Index** has dropped nearly **21%** year-to-date. Investors are increasingly worried about "seat compression," where autonomous AI agents replace the need for traditional per-seat software licenses. Market sentiment has shifted from celebrating AI features to fearing the total disruption of legacy business models. This has triggered a rotation of capital away from high-multiple software firms and into "Old Economy" value stocks in the financials and industrials sectors. Macroeconomic and Policy Drivers The U.S. stock market has faced a choppy February, with the **Nasdaq Composite** recently sliding **2.1%** in a single week. Despite this, broader economic data remains resilient. Headline inflation cooled to **2.4%** in January, and fourth-quarter GDP growth is being tracked at a robust **5.4%**. President Trump’s recent policy updates have added a new layer of complexity to the trade environment. While strict tariffs remain a focus, a recent shift allowing the resumption of high-end chip sales to **China**—subject to an export tax—is being viewed as a potential multi-billion dollar catalyst for the 2027 fiscal year. Key Metrics to Watch * **Data Center Revenue:** Expected to hit **$59.9 billion**, representing the core of Nvidia's growth. * **Blackwell Demand:** CEO Jensen Huang has described demand for the new Blackwell AI platform as "insane," and investors want confirmation of production scaling. * **Capital Expenditure:** Tech giants like Amazon and Alphabet have signaled combined AI spending exceeding **$350 billion** for 2026, which directly benefits the semiconductor pipeline. * **Market Volatility:** The **VIX** (fear gauge) has moved up to **20.60**, reflecting heightened nervousness ahead of next week's policy and earnings catalysts. The immediate focus remains on whether Nvidia can exceed the "price-to-perfection" standards the market has set. Its ability to maintain gross margins near **75%** will be the primary indicator of whether the AI infrastructure boom still has room to run or if the cycle is beginning to normalize.

Pre-Market Analysis: Financial Outlook and Trade Setup for the Current Session

Market Brief: Geopolitical Tensions Spark Sharp Correction Indian equity markets faced a significant downturn during the latest session, abruptly halting a three-day rally. The **BSE Sensex plummeted 1,236.11 points (1.48%)** to close at **82,498.14**, while the **NSE Nifty 50 dropped 365 points (1.41%)** to settle at **25,454.35**. The sell-off erased approximately **₹7.55 lakh crore** in investor wealth as risk aversion swept through almost all sectoral indices. Energy Crisis and Imported Inflation The primary catalyst for the decline is the escalating tension between the United States and Iran. Concerns over potential military action and disruptions in the **Strait of Hormuz**—a critical passage for 20% of global oil—pushed **Brent crude** to a year-to-date high above **$71 per barrel**. For India, which imports over **85%** of its crude requirements, the surge raises immediate alarms regarding imported inflation and a widening trade deficit. While upstream explorers like **Oil India (+5.2%)** and **ONGC (+3.6%)** gained on higher realizations, oil marketing companies like **HPCL (-5%)** and **BPCL (-3.4%)** faced heavy selling due to anticipated margin compression. Institutional and Currency Activity Market sentiment was further weighed down by cautious institutional flows. In the cash segment, **Foreign Institutional Investors (FIIs)** were net sellers of **₹880.49 crore**, joined by **Domestic Institutional Investors (DIIs)** who offloaded **₹596.28 crore**. The **Indian Rupee** remained under pressure, trading near the **91.07** level against the US Dollar. The combination of high oil prices, a weakening currency, and rising US bond yields has created a challenging macro environment for domestic equities. Sectoral Performance and Outlook The selling was broad-based, with **Realty, Auto, and Power** sectors each shedding nearly **2%**. Large-cap heavyweights including **Reliance Industries, HDFC Bank, and ICICI Bank** led the downward move as investors locked in profits following the recent streak of gains. Technically, the **Nifty 50** has breached immediate support levels. Analysts suggest the index may test the **25,370 - 25,230** range if the geopolitical situation does not stabilize. Investors are now closely monitoring the US Federal Reserve’s upcoming policy signals for clues on the global interest rate trajectory.

Market Outlook: 10 Key Factors for Friday’s Trading Session

Indian equity markets faced a significant downturn on **February 19, 2026**, as escalating tensions between the United States and Iran triggered a wave of risk aversion. The benchmark **Nifty 50** plummeted **365 points**, or **1.41%**, to close at **25,454.35**. Simultaneously, the **S&P BSE Sensex** crashed **1,236 points**, ending the session at **82,498.14**. This sharp reversal wiped out approximately **₹7 lakh crore** in investor wealth in a single day. The primary catalyst for the sell-off was the breakdown in diplomatic negotiations, with US officials warning that military options remain on the table. This geopolitical friction sent **Brent crude** prices surging toward **$70.53 per barrel**, raising concerns about imported inflation and fiscal pressure for India. Consequently, the **India VIX** spiked by **7.40%** to reach **13.13**, signaling a sharp rise in market nervousness and the potential for continued volatility. Sectoral performance was almost entirely negative, with all 16 NSE sectoral indices ending in the red. The **Auto** sector was among the hardest hit, with **Mahindra & Mahindra** falling **2.93%**. **Aviation** and **Cement** also saw heavy liquidations; **IndiGo** dropped **3.28%** while **UltraTech Cement** declined **2.97%**. Despite the broader gloom, **ONGC** bucked the trend to rise **3.65%**, benefiting from the spike in global oil prices. From a technical perspective, the Nifty has drifted toward its **20-day moving average** near the **25,300** zone. This level is now considered a crucial support floor. A breach below **25,200** could accelerate the correction toward the psychological handle of **25,000**. On the upside, immediate resistance is established at **25,600**, followed by a more significant supply wall at **25,800**. Market breadth was decisively bearish, with roughly **2,900** stocks declining against only **1,200** advances on the BSE. Foreign Institutional Investors (FIIs), who had shown interest earlier in the week, appeared to move to the sidelines as the "buy on dips" strategy was tested by the weight of global uncertainty. Mid-cap and small-cap indices mirrored the large-cap decline, falling **1.54%** and **1.16%** respectively, as valuations in those segments remain under scrutiny.

**Oil prices fluctuate amid ongoing US-Iran geopolitical developments**

Energy Market Brief: February 19, 2026 Crude oil markets are navigating a volatile session as significant geopolitical escalations in the Middle East collide with shifting inventory data. Prices have moderated slightly following a sharp rally, with traders balancing immediate supply risks against broader economic forecasts. Price Action As of today, **Brent Crude** is trading near **$70.32** per barrel, marking a steady climb from earlier February lows around **$65.97**. **West Texas Intermediate (WTI)** has mirrored this strength, currently holding around **$65.24**. This follows a volatile 24-hour period where prices surged by over **$3.00** in a single session due to heightened risk premiums. Geopolitical Flashpoints The primary driver of the recent price spike is a dramatic expansion of military posturing in the Persian Gulf. Reports indicate the **United States** has moved an armada including two aircraft carriers and over **150** military cargo planes into the region. Market participants are pricing in a roughly **90%** chance of "kinetic action" involving **Iran**. This has placed the **Strait of Hormuz**—a chokepoint for **20%** of global oil shipments—under intense scrutiny. While diplomatic talks continue, progress remains slow, and the shift from deterrence to active war footing has sent global energy markets into a tailspin. Inventory and Supply U.S. oil inventories fell unexpectedly last week, defying analyst predictions of a build. Private sector data recently indicated a headline crude draw, adding upward pressure to prices ahead of the official government report. The **Energy Information Administration (EIA)** is scheduled to release official data later today. Analysts are watching for confirmation of these tightening stocks, as total global builds in **2025** reached a staggering **477 million barrels**, providing a significant buffer that may currently be eroding. Production and Demand Outlook **OPEC+** has reaffirmed its commitment to market stability, maintaining flat production targets through the first quarter of **2026**. However, the alliance has signaled a potential output increase starting in **April** to meet anticipated summer demand. Global demand is currently forecast to grow by **1.4 million** barrels per day (bpd) in **2026**, led primarily by non-OECD economies. **India** and **China** remain the critical engines of this growth, with Indian demand surging by over **300,000 bpd** in recent monthly prints, driven by industrial and transport fuel needs. Despite the current geopolitical spike, the **IEA** and **EIA** maintain a cautious long-term outlook, citing that global supply is still on track to rise by **2.4 million bpd** this year, which could lead to a cooling of prices later in **2026**.

**Rohit Srivastava Notes Defensive Growth Potential in Value Stocks and NBFCs**

Market Brief: India Equities Stability Check Indian equity benchmarks maintained a neutral stance on Wednesday, February 18, 2026, as the **Nifty 50** struggled to find direction, hovering near the **25,700** mark. The **Sensex** tracked a similar path, trading marginally lower around **83,390** levels. This sideways movement follows a period of heightened volatility where the market is balancing between local earnings strength and global uncertainty. Critical Technical Zones Technical analysts identify the **25,780** to **25,800** range as a formidable resistance barrier for the Nifty. A sustained move above this level is required to trigger a fresh rally toward the **26,000** psychological milestone. On the flip side, immediate support is established at **25,550**. If the index fails to hold this cushion, a deeper correction toward **25,300**—the 200-day exponential moving average—remains a distinct possibility. Divergent Sectoral Performance The market is currently characterized by high "churn," with capital rotating rapidly between sectors. * **Metals and PSU Banks:** Leading the gainers today, with the Nifty Metal index jumping over **1.30%** as commodity prices stabilize. PSU Banks saw a surge of more than **2%**, continuing their recent outperformance. * **Information Technology:** Facing persistent pressure due to uncertainty surrounding global software disruptions. Large-cap IT names like Infosys and TCS remain volatile as institutional investors seek more attractive valuations. * **Energy and Services:** These sectors underperformed in today's session, with energy stocks sliding as global crude benchmarks fluctuate near **$67.48**. Liquidity and Sentiment Foreign Institutional Investors (FIIs) have shown early signs of a strategy shift. While they were net sellers of over **₹41,000 crore** in January, they turned net buyers in mid-February, recording an inflow of **₹995.21 crore** in a single recent session. Domestic Institutional Investors (DIIs) continue to provide a floor to the market, supported by steady SIP inflows. The India VIX, a gauge of market nervousness, has cooled significantly by nearly **5%** to settle around **12.27**. This drop suggests that while the indices are flat, the immediate fear of a sharp crash is receding. Investors are advised to move away from broad index bets and focus on bottom-up stock selection. Value is currently emerging in sectors with high earnings visibility, such as pharmaceuticals, telecom, and select automobiles, while momentum remains focused on the mid-cap and small-cap space, which outperformed the frontline indices today.

Upstream oil stocks decline up to 4% amid market shifts

Upstream oil and gas stocks experienced a sharp sell-off on Wednesday, February 18, 2026, as global crude prices retreated toward two-week lows. The decline was primarily fueled by reports of diplomatic progress between the United States and Iran, which raised the possibility of increased supply entering an already well-stocked market. Crude Prices and Geopolitical Shifts Benchmark Brent crude fell to **$67.39** per barrel, while West Texas Intermediate (WTI) hovered around **$62.28**. This downward movement reflects a reduction in the "geopolitical risk premium" that had previously propped up prices. Recent talks in Geneva have led to a "general agreement" on guiding principles regarding Iran’s nuclear program, signaling a potential path for the removal of sanctions. Market sentiment has also been impacted by rising output at the Tengiz field in Kazakhstan and a projected global supply surplus of nearly **4 million barrels per day** for the first quarter of 2026. This oversupply remains a dominant theme, even as OPEC+ considers whether to resume production hikes in April. Impact on Indian Upstream Majors The drop in global prices directly pressures the realizations and profit margins of domestic producers. In Mumbai, shares of major upstream players saw significant corrections: * **ONGC** and **Oil India** shares tumbled by as much as **4%** during intraday trading. * **Seamec Ltd** also faced pressure, compounded by news that its vessel, *SEAMEC Diamond*, was off-hired for mandatory drydocking maintenance. For these companies, lower crude prices translate to reduced revenue per barrel and may lead to a more cautious approach toward capital expenditure on new exploration projects. Shifting Trade Dynamics The domestic energy landscape is also adapting to changing import patterns. Data from early 2026 shows that Indian refiners have significantly reduced purchases of Russian crude, with imports plunging over **40%** in January compared to the previous year. This shift follows increased international pressure and new tariff structures, forcing a diversification of supply sources. While upstream producers face a softer pricing environment, the broader sector is increasingly looking toward natural gas and digital optimization to defend profitability in a volatile market.

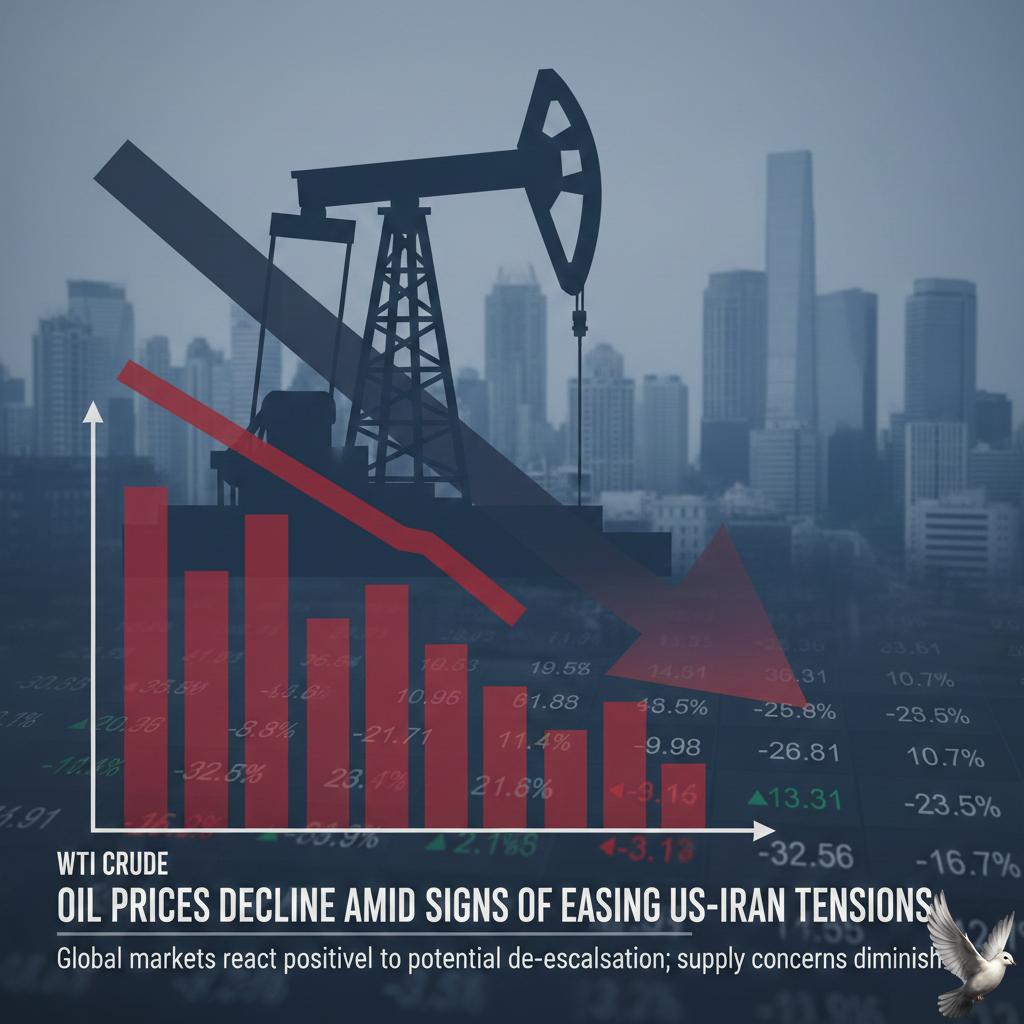

Oil Prices Decline Amid Signs of Easing US-Iran Tensions

Energy markets are experiencing a cautious pull-back as geopolitical shifts and rising production capacity alter the supply-demand balance. As of February 18, 2026, Brent crude is trading near **$67.45** per barrel, down approximately **0.10%**. Simultaneously, WTI crude has slipped to **$62.24**, marking a **0.14%** daily decline. Both benchmarks are currently hovering near two-week lows as traders digest a complex mix of diplomatic progress and physical supply growth. A primary driver for the current softening is the second round of indirect talks between the U.S. and Iran held in Geneva. While "guiding principles" for a potential nuclear dispute resolution have been discussed, officials emphasize that a final deal is not imminent. Despite the lack of an immediate breakthrough, the mere "steady drip" of diplomatic optimism has significantly eased fears of sudden supply disruptions in the Persian Gulf. Supply-side pressure is also mounting from Central Asia. Kazakhstan's Tengiz field—one of the world's largest—has successfully ramped up output following recent expansion projects. Production at the field exceeded **39 million tons** in 2025, a significant jump from previous years. This surge in Kazakh crude, combined with a broader recovery from winter-related production shut-ins in North America, is contributing to a growing global inventory cushion. Market participants are now pivotally focused on upcoming U.S. inventory data. Recent figures showed a massive surge in U.S. crude stocks by **13.4 million barrels** in a single week, reversing previous draws and signaling a potential domestic glut. Wider trends for 2026 suggest a "market reset" may be underway. Global supply is projected to rise by **2.4 million barrels per day** this year, while demand growth is expected to slow to roughly **850,000 barrels per day**. This widening surplus of over **1.5 million barrels per day** is keeping a firm lid on price rallies, even amidst ongoing regional tensions. Short-term volatility remains high, with the market alternating between bearish supply data and bullish geopolitical headlines. For now, the combination of diplomatic engagement and robust output from non-OPEC+ sources like Kazakhstan continues to weigh on the price floor.

Indian Sovereign Bonds Advance Amid Lower Treasury Yields and Surplus Liquidity

Indian government bonds gained momentum this Monday, as the 10-year benchmark yield stabilized near three-week lows. The move reflects a broader cooling in global yields and resilient domestic liquidity, even as the market navigates long-term supply pressures. The 10-year benchmark 6.48% 2035 bond yield settled at 6.6670%, a slight decline from the 6.68% level seen in previous sessions. This steadying performance follows a period where yields slipped to their lowest levels in nearly a month, driven by strategic government debt management. Sentiment was bolstered by a significant drop in U.S. Treasury yields. The 10-year U.S. note fell to 4.05%, its lowest since November, following softer-than-expected inflation data. This has heightened global market bets on potential rate cuts, providing a supportive backdrop for Indian debt. Domestically, inflation remains a key driver. January’s consumer price inflation was reported at 2.75%, remaining well within the Reserve Bank of India’s 2% to 6% tolerance band. This benign inflation environment has allowed the RBI to maintain a neutral stance, recently holding the repo rate steady at 5.25%. Liquidity conditions in the banking system have stayed comfortable, with a daily surplus averaging approximately 70,000 crore. This follows aggressive open market operations (OMO) by the RBI, which conducted purchases amounting to 3,50,000 crore in the preceding months to ensure market stability. Despite the recent rally, some caution remains due to future supply concerns. The government recently conducted a debt switch, buying back 75,500 crore of bonds maturing in 2027 while issuing 69,400 crore of longer-dated 2040 securities. While this eased near-term redemption pressure, the market is bracing for a gross market borrowing target of 17.2 trillion in the next fiscal year. The fiscal deficit for the 2026-27 period is estimated at 4.3% of GDP, a slight reduction from the 4.4% projected for the current year. Investors are balancing this fiscal consolidation path against the increased interest burden and the need for the market to absorb a record volume of government paper. Short-term volatility may also stem from new regulatory measures. The RBI has introduced stricter collateral rules for proprietary trading firms, effective April 1. This move, aimed at curbing speculative leverage, is expected to raise capital costs for major market participants and influence overall trading volumes in the coming months.

Global Markets: BOE Rate Decisions Hinged on Upcoming UK Inflation Data

The Bank of England maintains a cautious stance on monetary policy after a narrow 5–4 vote on February 4, 2026, to hold the benchmark interest rate at 3.75%. Despite the hold, policymakers signaled a shift toward future easing, with four members already pushing for an immediate 0.25% reduction. This internal division highlights a critical pivot point for the UK economy. Inflation remains the central focus for the Monetary Policy Committee. The headline rate was recorded at 3.4% as of late 2025, which remains above the 2.0% target. However, projections suggest inflation will return to target levels by June 2026, aided by a projected 5% drop in energy price caps and government price-cutting measures. The labor market is showing significant signs of cooling, providing the Bank with more room to maneuver. The unemployment rate has risen to 5.1%, the highest level since 2021. Furthermore, private sector wage growth has slowed to 3.9%, its lowest in nearly five years. This "loosening" of the jobs market is a key indicator that inflationary pressures from earnings are receding. Economic growth remains fragile with the UK economy expanding by only 0.1% in the final quarter of 2025. Annual GDP growth for 2026 is forecast at a modest 0.9% to 1.0%. Business investment rose by 3.5% over the past year, but activity is heavily concentrated in the energy and technology sectors, leaving the broader economy stagnant. Financial markets are currently pricing in an 80% probability of two further rate cuts by the end of 2026, which would bring the Bank Rate down to 3.25%. A dovish shift in the Bank’s recent communications has led many analysts to expect the next 25-basis-point cut as early as the March meeting, provided upcoming inflation and labor data continue their downward trajectories. The coming weeks are essential for determining if the UK can achieve a "soft landing." Success depends on balancing the risk of persistent services inflation against the threat of a weakening economy that could slip into stagnation without further stimulus. [Bank of England interest rate decision](https://www.youtube.com/watch?v=SPZDIPMmht0) This video provides a professional breakdown of the latest Bank of England meeting, explaining the 5–4 split vote and what the current economic data means for future interest rate cuts. http://googleusercontent.com/youtube_content/0

Indian IT Stocks and Nine Others Reach 52-Week Lows Following Monthly Declines of Up to 20%

Dalal Street witnessed a significant retreat as the benchmark **BSE Sensex** crashed **1,048.16 points**, or **1.25%**, to close at **82,626.76** on Friday, February 13, 2026. This sharp decline was mirrored by the **NSE Nifty 50**, which plunged **336.10 points** to settle at **25,471.10**, slipping below the critical **25,500** mark. The downturn was primarily fueled by a massive sell-off in the technology sector, following a rout in global tech markets and renewed fears over artificial intelligence disrupting traditional business models. The **Nifty IT index** cracked over **5%** during intraday trade, marking a cumulative loss of nearly **12%** in just three sessions. Key blue-chip IT stocks bore the brunt of the selling pressure. **Infosys** tumbled **7.5%**, while **Tata Consultancy Services (TCS)** and **HCL Technologies** dropped **6%** and **5.5%** respectively. **Wipro** and **Tech Mahindra** also faced steep declines of approximately **4.5%**. Broader market sentiment remained fragile as nine stocks within the **BSE 200** index hit fresh **52-week lows**. Among the notable names touching their lowest prices in a year were **Wipro**, **TCS**, **Infosys**, **L&T Technology Services**, and **Info Edge India**. Market capitalisation of BSE-listed companies was eroded significantly, falling to approximately **₹465 lakh crore** ($5.13 trillion). The market breadth was overwhelmingly negative, with **2,960** shares declining compared to only **1,253** gainers on the BSE. Volatility spiked as the **India VIX** surged **15.18%**, reflecting increased investor anxiety ahead of upcoming U.S. inflation data. External pressures, including a stronger **U.S. Dollar Index** at **97.07** and the Indian rupee edging lower to **90.65** against the dollar, further weighed on domestic equities. In other sectors, metal and FMCG stocks also saw heavy profit-booking. **Hindustan Unilever (HUL)** dropped **4.34%** following weak quarterly results, while **Hindalco** emerged as a top loser, sliding **5.75%**. Only a few counters managed to defy the trend. **Bajaj Finance** rose **2.57%** and **State Bank of India (SBI)** gained **0.52%**, standing out as rare bright spots in an otherwise sea of red. The current correction reflects a structural recalibration as investors reassess growth assumptions for the IT services industry. With the traditional headcount-based model facing scrutiny, the market is likely to remain volatile until clearer guidance on deal flows and AI integration emerges.