Negative

Oil Prices Up 3% Amid Extended US-Iran Negotiations

Oil prices surged nearly 3% on Friday as energy markets reacted to a high-stakes extension of nuclear negotiations between the United States and Iran. Traders are increasingly concerned that a potential breakdown in diplomacy could trigger immediate supply shocks in the Middle East.

WTI crude futures climbed toward $67 per barrel, reaching a seven-month high. Brent crude also saw significant movement, trading around $72.78. These gains were fueled by reports that while Iran described talks in Geneva as progressive, U.S. officials expressed disappointment, signaling a widening gap between the two sides.

Geopolitical risk premiums are currently estimated between $4 and $10 per barrel. The market is pricing in the possibility of a disruption to Iran’s 3.3 million barrels per day of production. Concerns are also mounting over the security of the Strait of Hormuz, a critical maritime artery that handles approximately 20% of the world's global oil supply.

Regional tensions have escalated further following the U.S. decision to authorize the departure of non-emergency staff and families from Mission Israel. This atmosphere of uncertainty has overshadowed recent data showing a massive 15.9 million barrel build in U.S. crude stocks, which would typically exert downward pressure on prices.

Supply dynamics remain complex as OPEC+ prepared for its Sunday meeting. The group is widely expected to maintain its cautious stance, with analysts anticipating a modest production increase of 137,000 barrels per day for April. This comes as Saudi Arabia reportedly nears a three-year high in exports as part of a contingency plan to stabilize the market in the event of regional conflict.

For the month of February, oil prices have risen approximately 2.5%, extending a sharp 13.6% rally recorded in January. While long-term forecasts from the IEA and major banks suggest a global supply surplus for 2026, the immediate focus of the market remains fixed on the March 1–6 deadline for a nuclear agreement.

Technical indicators show WTI has broken above its 200-day moving average, confirming a reversal of the previous bearish trend. Investors are now watching the $70 mark as the next psychological resistance level for WTI, provided geopolitical frictions remain unresolved.

Read Story

Positive

XED to Launch GIFT City’s First IPO of $12 Million on March 6

Executive education provider XED Executive Development has confirmed the pricing and timeline for its landmark Initial Public Offering at GIFT City. This transaction represents a historic shift for India’s International Financial Services Centre (IFSC) as it hosts its first-ever equity share sale.

The company has set a price band of **USD 10 to USD 10.5** per share. The issue aims to raise a total of **USD 12 million** to fuel global expansion. The subscription window is scheduled to open on **March 6, 2026**, and will remain active for nine working days, closing on **March 18, 2026**.

This dollar-denominated offering marks a significant evolution for the Gujarat International Finance Tec-City ecosystem. While the zone has previously focused on debt and derivatives, this move introduces a primary equity market for globally oriented companies. The shares will be listed on both the **NSE International Exchange (NSE IX)** and the **India International Exchange (India INX)**.

Participation is restricted to eligible investors under the International Financial Services Centres Authority (IFSCA) framework. This includes Non-Resident Indians (NRIs), foreign portfolio investors (FPIs), and institutional participants. Because the instrument is traded in US dollars, it provides international investors with a hedge against currency volatility and aligns with global valuation standards.

XED currently operates across more than **25 countries**, with a strong presence in the Middle East, Southeast Asia, North America, and India. The capital raised is earmarked for deepening university partnerships and scaling delivery infrastructure across these high-growth regions.

The launch comes at a time of high activity for GIFT City. The International Financial Services Centre has seen banking assets exceed **USD 100 billion**, while monthly exchange turnovers average **USD 90 billion**. Market experts view this IPO as a critical test for the IFSC’s offshore capital-raising platform, which could pave the way for other cross-border enterprises.

The broader market context remains cautious but resilient. The **GIFT Nifty** has recently traded in a range-bound zone near **25,500–25,700**, reflecting a phase of consolidation. Despite global tech volatility, domestic institutional buying remains a strong support pillar for the ecosystem.

Key entities managing the issue include **Global Horizon Capital Advisors** as the lead manager and **KFin Technologies** as the registrar. Banking operations for the IPO are being handled by **DBS Bank** and **RBL Bank**.

Positive

Barclays Shares Decline Amid Market Concerns Following UK Specialist Lender Collapse

**Market Brief: Barclays and the UK Private Credit Sector**

Barclays shares faced significant pressure during Friday's trading session following reports of a 600 million pound exposure to the collapse of Market Financial Solutions (MFS). The specialist UK mortgage provider and bridging lender entered administration this week amid allegations of financial irregularities and fraud.

The bank's stock price slid 4.2% on Friday to close at approximately 451.35p. This decline occurred despite the broader FTSE 100 index reaching a record high of 10,910.55 points. The sell-off reflects investor anxiety regarding the quality of underwriting standards in the fast-growing private finance and "shadow banking" sectors.

**Exposure and Financial Impact**

The collapse of MFS has triggered immediate scrutiny of institutional lending lines. Court proceedings revealed allegations of "double pledging" of assets, a practice where the same collateral is used to secure multiple loans. Barclays and Atlas SP Partners are identified as major creditors, having arranged portions of a lending facility that once supported an MFS loan book valued at 2.4 billion pounds.

While Barclays has recently reported strong annual earnings and a 1 billion pound share buyback program, this latest development introduces a potential 600 million pound loss. Analysts are currently evaluating how much of this exposure is already provisioned or held on the bank's balance sheet versus external investment vehicles.

**Wider Sector Concerns**

The fallout has impacted other lenders with similar private credit exposures. Shares in Jefferies dropped 10%, while Santander also saw declines as the market reassessed risk positions in structured mortgage funding. This incident follows the recent insolvency of another bridging lender, Century Capital, suggesting a localized tightening in the specialist finance market.

The UK bridging sector, which provides short-term property loans, operates with less regulatory oversight than mainstream retail banking. These high-profile failures have validated recent warnings from industry leaders regarding "cockroaches" in the credit market and the risks associated with non-bank lenders stretching standards to maintain income growth.

**Market Outlook and Indicators**

The broader UK economic environment remains complex. The Bank of England recently maintained the base rate at 3.75%, though market expectations lean toward further cuts later this year. While mortgage lending growth is forecast to slow to 2.5% in 2026, the demand for higher-yield private credit had remained robust until these recent defaults.

Investors are now pivoting toward a more cautious "interpretation game." While Barclays’ Common Equity Tier 1 (CET1) ratio remains healthy at 14.1%, the MFS collapse serves as a critical test of the bank’s risk management frameworks within its investment and corporate banking divisions. Expect increased focus on collateral verification and more stringent due diligence across all private lending facilities in the coming months.

Positive

Sunway Healthcare Files Prospectus for IPO of Up to $736 Million

Sunway Healthcare Holding launched its initial public offering (IPO) prospectus on Friday, February 27, 2026. The group aims to raise up to 2.86 billion ringgit, approximately 736 million dollars. This move positions the company for the largest market debut in Malaysia since 2017.

The offering consists of 1.97 billion shares priced at 1.45 ringgit each. The retail subscription window is officially open from today until March 5, 2026. Trading is expected to commence on the Main Market of Bursa Malaysia on March 18, 2026.

Upon listing, the company’s market valuation is projected to reach 16.7 billion ringgit. This listing will increase the total market capitalization of the Sunway Group’s four listed units to over 70 billion ringgit. The IPO has secured backing from 20 cornerstone investors, including the Employees Provident Fund and JPMorgan Asset Management.

Proceeds from the listing are earmarked for major infrastructure and clinical enhancements. Approximately 66.5 percent, or 554 million ringgit, will fund the expansion of existing hospitals over the next 36 months. Another 29.9 percent is allocated to the redemption of sukuk wakalah.

Sunway Healthcare enters the market following a record financial performance. In 2025, the parent group reported a net profit of 1.3 billion ringgit, a 13 percent increase from the previous year. The healthcare division specifically saw a 44.7 percent jump in pre-tax profit to 96.9 million ringgit, fueled by rising patient volumes and higher bed occupancy.

The timing of the IPO coincides with a broader push for larger listings in Malaysia. Bursa Malaysia is targeting a total IPO market capitalization of 28 billion ringgit for 2026. This follows a robust 2025 where 60 companies went public, raising 2.36 billion dollars.

The regional healthcare outlook remains a primary driver for the expansion. Malaysia’s medical inflation is projected to reach 16 percent in 2026, the highest rate since 2021. This trend is attributed to an aging population, the adoption of advanced medical technologies, and a growing demand for private healthcare services.

Sunway Healthcare currently operates 1,805 licensed beds as of early 2026. The group aims to double this capacity by 2032. It also maintains a 30 percent dividend payout policy, positioning itself as a high-conviction play for investors seeking both growth and recurring income in a defensive sector.

Positive

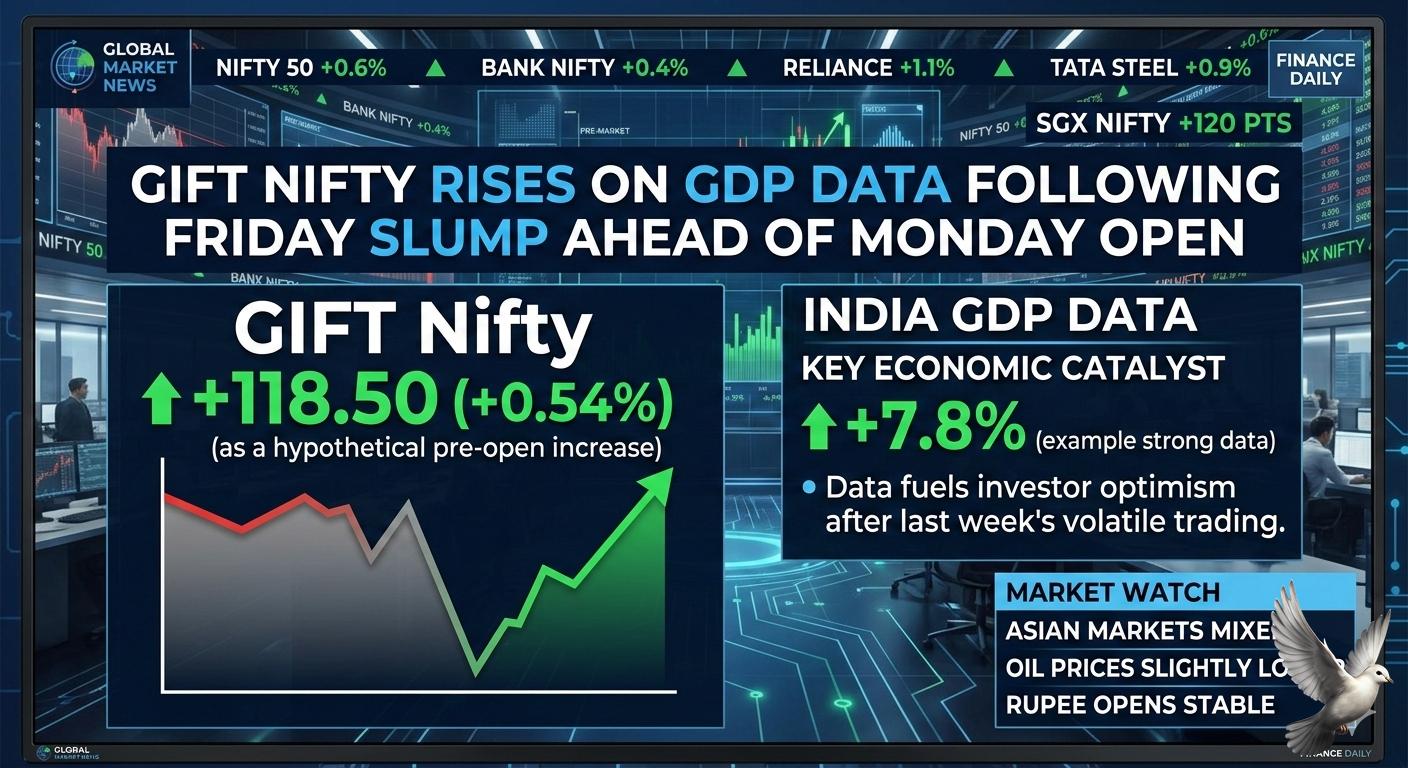

GIFT Nifty Rises on GDP Data Following Friday Slump Ahead of Monday Market Open

Indian equity markets faced a significant sell-off today, February 27, 2026, as the BSE Sensex plummeted 961 points to close at 81,287.19. The NSE Nifty 50 also suffered a sharp decline, sliding 318 points to settle at 25,178.65. This downward move represents a drop of over 1.2% for both benchmark indices.

The correction was fueled by fresh foreign fund outflows and mounting geopolitical risks. Investor confidence wavered as U.S.–Iran nuclear talks stalled, raising fears of escalated tensions in the Middle East. Additionally, uncertainty surrounding AI-sector valuations in the U.S. triggered a global "risk-off" sentiment, dragging down Asian and European peers.

Foreign Institutional Investors (FIIs) remained in selling mode, offloading equities worth 3,465 crore in the latest session. However, the impact was partially cushioned by Domestic Institutional Investors (DIIs), who showed resilience by purchasing stocks worth 5,031 crore. This domestic support remains a critical anchor for Indian markets during global turbulence.

Despite the market volatility, India’s fundamental economic indicators remain robust. The latest government data shows that the economy grew at a better-than-expected 7.8% in the third quarter of the current fiscal year. This performance has led to an upward revision of the full-year GDP growth projection for 2025-26 to 7.6%.

The manufacturing and services sectors have emerged as the primary engines of this resilience, both recording growth rates above 9%. While the broader market cap saw a erosion of nearly 5 lakh crore today, the upbeat GDP signals suggest a solid domestic foundation that could support a recovery once global headwinds subside.

Sectoral performance was largely negative, with heavy selling observed in the Auto, Banking, and Realty spaces. Major laggards included Sun Pharma, Mahindra & Mahindra, and Bharti Airtel. Conversely, the IT sector provided a rare bright spot, with stocks like HCL Tech and Infosys ending in the green as investors rotated into defensive plays.

Volatility, as measured by the India VIX, remains around the 13.06 level, indicating that while there is pressure, there is no immediate panic. Market participants are now closely watching the 25,100–25,200 support zone for the Nifty, as technical indicators suggest the index is entering a critical consolidation phase.

Positive

Robert G. Allen on the Limited Wealth Potential of Savings Accounts Compared to Market Investing

Building wealth in 2026 requires a decisive shift from passive saving to strategic investing. While traditional savings accounts offer a sense of security, they currently struggle to protect purchasing power.

As of late February 2026, global core inflation remains stubborn at approximately 2.8%, with U.S. figures projected to hover around 3.2%. In this environment, cash held in standard accounts often yields a negative real return, effectively eroding wealth over time.

Successful wealth creation now centers on assets that historically outpace these inflationary pressures. The S&P 500 continues to serve as a primary engine for growth, with Wall Street analysts forecasting a total return of nearly 12% for the full year 2026. This significantly exceeds the 30-year historical average of 8.1%, driven by strong corporate earnings which saw a 13.6% year-over-year increase in early 2026.

Real estate remains a critical pillar for financial independence. The global market is showing renewed strength as interest rates stabilize. In early 2026, the Bank Rate in major economies like the UK sits at 3.75%, with expectations for gradual easing. Global investment volumes in real estate have rebounded by 19% compared to previous cycles, as investors seek the stability of tangible assets and rental growth, which averaged 6.4% in high-demand sectors recently.

Modern portfolio construction has evolved beyond simple diversification. High-net-worth strategies now frequently incorporate private markets to reduce reliance on public volatility. Approximately 83% of advisors now consider private credit and private equity essential for a resilient portfolio. These alternative assets offer a cushion against the "shock weeks" seen in public markets, where indices can occasionally drop 5% or more due to geopolitical or trade-related events.

The path to financial independence involves embracing calculated risk. Wealth is no longer just preserved; it is engineered through active participation in the global economy. By moving capital from low-yield savings into growth-oriented investments like large-cap equities and commercial real estate, individuals can ensure their fortunes grow faster than the cost of living.

Diversification remains the most effective tool for managing uncertainty. As regional inflation gaps widen between the U.S. and Europe, a global approach to asset allocation helps capture growth while mitigating localized risks. Strategic investors are currently rotating into sectors like energy and industrials, which have shown double-digit leadership in the opening months of the year.

Ultimately, saving preserves what you have, but investing creates what you need for the future. In a market characterized by rapid technological shifts and evolving fiscal policies, the disciplined deployment of capital into productive assets is the only proven method for long-term wealth accumulation.

[Investment vs. Savings: Which is Better?](https://www.youtube.com/watch?v=0_jF7q5N1D8)

This video provides a foundational comparison between saving and investing, illustrating how different asset classes contribute to long-term wealth growth as discussed in the brief.

Positive

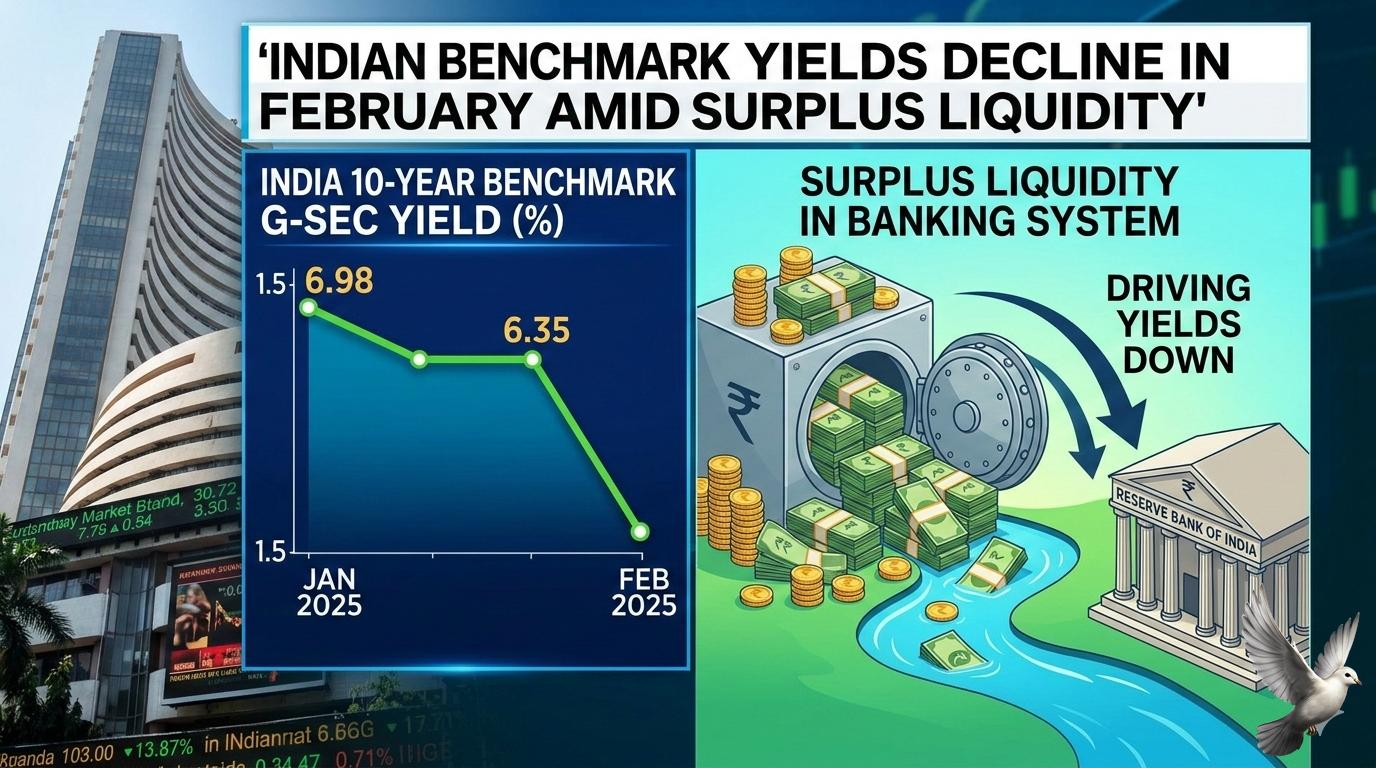

Indian Benchmark Yields Decline in February Amid Surplus Liquidity

The Indian government bond market is navigating a complex period of shifting yields and liquidity adjustments as of late February 2026. While benchmark rates have shown signs of softening, the broader market is reacting to heavy supply pressures and a cautious central bank stance.

The 10-year benchmark bond yield is currently hovering around the 6.68% to 6.70% range. This follows a volatile month where yields initially spiked to 6.73% after the Reserve Bank of India (RBI) maintained a neutral policy stance. Recent auctions have seen stronger demand, particularly for state government debt, helping to pull the benchmark down from its monthly highs.

Banking system liquidity has emerged as a critical support pillar. The RBI has been exceptionally active, purchasing approximately 47% of the government's total bond issuances so far in the current fiscal year. These Open Market Operations (OMOs) have injected over 6.39 trillion rupees into the system, maintaining a surplus of nearly 3 trillion rupees and preventing a sharper rise in borrowing costs.

Despite this surplus, the yield curve is steepening. This is driven by a divergence between short-term rates, which are stabilizing due to high liquidity, and long-term yields, which face pressure from upcoming supply. The government has announced a record gross borrowing target of 17.2 trillion rupees for the next fiscal year (FY27), a figure that exceeded many market projections and continues to weigh on investor sentiment.

The RBI's Monetary Policy Committee recently held the repo rate steady at 5.25%. While inflation remains within the comfort zone at approximately 4%, the central bank’s decision to maintain a "prolonged pause" has dampened hopes for immediate rate cuts. This has shifted investor focus toward short-term instruments, while ultra-long bonds—specifically 30-year and 40-year papers—continue to see sustained interest from insurance and pension funds.

Credit-to-deposit dynamics remain a structural challenge for the banking sector. With credit growth at 14.6% outpacing deposit growth at 12.5%, many banks are seeing their liquidity coverage ratios shrink. This has forced increased reliance on certificates of deposit (CDs), which have seen their rates climb above 7.30%, reflecting persistent funding competition despite the overall system surplus.

Market participants expect the 10-year benchmark to remain within a range of 6.65% to 6.80% in the near term. The primary focus remains on how the market will absorb the final auctions of the current fiscal year and the transition into the heavy borrowing schedule of April.

Positive

Credent Global Finance Raises Rs 30 Crore via QIP

Credent Global Finance has successfully executed a capital raise of 30 crore through a Qualified Institutional Placement (QIP) to accelerate its strategic expansion. The company allocated 1.00 crore equity shares to institutional investors at an issue price of 30 per share. This move has increased the total paid-up equity share capital to 12.29 crore, providing the necessary liquidity to fund microfinance opportunities and enhance market presence.

The fundraising coincides with an exceptional financial performance for the third quarter of 2026. The company reported a 775% year-on-year surge in revenue, reaching 25.74 crore. Net profit for the same period skyrocketed by 3,773%, touching 18.02 crore compared to the previous year. This growth reflects the company’s aggressive disciplined execution and its focus on high-potential credit segments.

Market data as of late February 2026 shows the stock trading near 31.90, maintaining a steady uptrend. The company currently holds a market capitalization of approximately 194 crore. Shares have fluctuated within a 52-week range of 20.70 to 35.06, supported by strong institutional interest and an improving price-to-earnings ratio of roughly 7.27.

To drive this next phase of growth, the leadership team has been significantly strengthened. The board recently appointed Vikas Kataria as Executive Director and Samir Agarwal as CEO. These strategic additions are intended to enhance corporate governance and operational oversight as the firm scales its lending and advisory operations across new regions, including a recent branch expansion into Delhi.

The company remains positioned as a non-banking financial company with a diversified portfolio spanning money lending, asset management, and investment banking. With a strengthened balance sheet and fresh capital, the firm is now focusing on counter-cyclical investing and selective credit opportunities in Eastern India's microfinance sector to deliver long-term stakeholder value.

[Credent Global Finance QIP and Earnings Review](https://www.youtube.com/watch?v=FjC3L469h_I)

This video provides a detailed breakdown of the recent QIP results and quarterly financial highlights mentioned in the report.

Positive

Steel HRC Prices Reach Two-Year High of ₹54,000 per Tonne Amid Ongoing Market Rally

India’s steel market has staged a dramatic recovery, with hot-rolled coil (HRC) prices climbing to a two-year high of ₹54,000 per tonne. This marks a sharp reversal from November lows of ₹47,000, driven by a combination of policy protection, surging input costs, and a frontloaded infrastructure cycle.

The government’s decision to impose a 12% safeguard duty on imported HRC has effectively insulated the domestic market. This duty, set to taper slightly to 11.5% in April 2026, has already caused a 13% year-on-year drop in total steel imports. With imported steel currently landing at approximately ₹57,000 per tonne, domestic producers hold a clear pricing advantage.

Coking coal remains the primary cost driver, with prices rising 30% year-on-year. Since coking coal accounts for roughly 35% of production costs, Indian steelmakers have successfully passed these expenses downstream. Market analysts have recently raised the 2026 coking coal price forecast to $190 per tonne, suggesting that cost-led price floors will remain elevated throughout the year.

Demand fundamentals are robust, with a projected growth of 8% to 9% for the current fiscal year. This surge is fueled by the pre-monsoon construction window and large-scale government projects under the Bharatmala and PM-AWAS schemes. Infrastructure and construction now absorb nearly 65% of India’s total steel output.

Steel producers are seeing a significant inflection in financial performance. EBITDA per tonne is now ranging between ₹5,000 and ₹13,600 across major manufacturers. Experts anticipate a further margin expansion of ₹3,000 to ₹4,000 per tonne in the coming quarter as higher realizations take effect and raw material volatility begins to stabilize.

The long-term outlook remains aggressive as India targets a production capacity of 300 million tonnes by 2030. While global markets face stagnation, India stands out as the fastest-growing steel consumer. Sustained domestic demand and a disciplined pricing environment are expected to maintain this favorable momentum through the first half of 2026.

Positive

Block Shares Rise 20% Following Workforce Reduction of 4,000 Employees

Shares of Block, Inc. surged nearly 20% in late February 2026 trading following a transformative fourth-quarter earnings report. CEO Jack Dorsey announced a massive structural reset, reducing the company's workforce by 40%. The headcount will drop from over 10,000 to approximately 6,000 employees as the firm pivots toward an AI-native operational model.

Markets responded with high conviction to this efficiency-driven strategy. Block reported a Q4 gross profit of $2.87 billion, marking a 24% year-over-year increase. Monthly active users on Cash App reached 59 million, while primary banking actives grew 22% to 9.3 million. This performance pushed the company's 2025 annual gross profit to $10.36 billion, with December alone crossing the $1 billion milestone for the first time.

The pivot to artificial intelligence is central to Block's new growth thesis. Management cited that intelligence tools are now advanced enough to allow significantly smaller teams to outpace larger, traditional workforces. Internal productivity gains from AI integration are expected to accelerate product development cycles and expand operating margins, which reached 20% in the final quarter of 2025.

For the 2026 fiscal year, Block has issued aggressive guidance. The company expects gross profit to reach approximately $12.2 billion, representing 18% growth. Adjusted operating income is projected at $3.2 billion, which would signify a 54% increase over the previous year. This outlook underscores a shift in investor sentiment, where lean, AI-driven profitability is now prioritized over total workforce scale.

Despite the positive market reaction, the broader fintech sector remains in a state of flux. While Block's shares rallied on the news, the stock had faced a 22% decline earlier in the year due to persistent economic headwinds. The current rally reflects a "Rule of 40" reckoning, as the company balances growth with disciplined cost management.

The structural changes at Block serve as a bellwether for the industry. Other major fintech players are increasingly adopting "agentic AI" and automated compliance systems to reduce overhead. As the sector moves through 2026, the focus has shifted entirely to high-margin lending, primary banking engagement, and AI-powered operational leverage.

[Block Q4 2025 earnings review](https://www.youtube.com/watch?v=eml2imnhwZg)

This video provides a professional breakdown of Jack Dorsey's decision to cut half of Block's staff to focus on AI productivity.

http://googleusercontent.com/youtube_content/0

Positive

Brigade Group and Primus Senior Living Partner for Three Senior Housing Projects

**Senior Living Market Brief: Brigade Group Expansion**

**Strategic Partnership and Financial Impact**

Brigade Group has entered into a strategic alliance with Primus Senior Living to develop three specialized housing projects in South India. This collaboration is set to unlock a combined Gross Development Value of 750 crore. The projects will deliver over 600 residential units specifically designed for the elderly, marking a significant move by the developer to diversify its residential portfolio beyond conventional formats.

**Project Integration and Infrastructure**

Two of the three upcoming communities will be integrated within larger existing township developments. This "senior-first" design approach allows residents to access shared social infrastructure while maintaining age-specific amenities. Key features include wellness centers, medical bays, hobby lounges, and fully accessible pathways. The model emphasizes inter-generational connectivity, bridging the gap between independent living and professional care.

**Regional Market Dominance**

South India currently accounts for nearly 60% of the organized senior living market in the country. This dominance is driven by advanced medical infrastructure, higher social acceptance of retirement communities, and a significant NRI base with aging parents in the region. Bengaluru and Chennai remain the primary hubs for these developments, with Chennai recently recording a 55% year-on-year surge in housing sales during the 2025-2026 period.

**Sector Growth and Investment Trends**

The Indian senior living market, valued at approximately 11.16 billion dollars in 2025, is projected to grow at a compound annual rate of 10% to 25% through 2031. This expansion is fueled by a doubling of the elderly population, which is expected to reach 347 million by 2050. Changing family structures and rising disposable incomes have shifted the segment from a niche "need-based" category to an aspirational lifestyle choice.

**Pricing and Portfolio Outlook**

Current market data indicates that senior living units in major South Indian metros typically range from 45 lakh to 75 lakh for standard configurations, with premium luxury projects exceeding 2 crore. For Brigade Group, this partnership builds on the success of their Parkside at Brigade Orchards project, which has been operational since 2017. As of early 2026, the developer continues to maintain a strong presence in the broader residential market, recently launching separate landmarks in Chennai with an estimated value of 1,700 crore.

Positive

Stock Market Top Gainers and Losers: Redington, Tejas Networks, and Others in Focus on Friday

Market Brief: Late February Volatility

Indian equity markets witnessed a sharp downturn as of **February 27, 2026**, with benchmark indices erasing recent gains in a broad-based sell-off. The **BSE Sensex** plunged **961.42 points**, or **1.17%**, to settle at **81,287.19**. Similarly, the **NSE Nifty 50** tumbled **317.90 points**, or **1.25%**, closing at **25,178.65**.

The crash wiped out approximately **₹5 lakh crore** in investor wealth in a single session. Total market capitalization of BSE-listed firms slipped to nearly **₹463 lakh crore** as risk aversion gripped the floor.

Sectoral Pressure Points

The decline was led by heavyweights in the **Auto**, **Financial Services**, and **FMCG** sectors. Foreign Institutional Investors (FIIs) intensified the pressure by offloading equities worth **₹3,465.99 crore** in the preceding session.

Banking and financial counters were particularly hit. Private lenders faced persistent selling amid concerns over valuation comfort and margin stability. Furthermore, sentiment in the microfinance space soured following the passage of the **Bihar MFI Bill 2026**, causing stocks like **Utkarsh Small Finance Bank** and **Fusion Finance** to tank between **6%** and **11%**.

Global and Macro Triggers

Geopolitical uncertainty acted as a primary catalyst. Inconclusive **U.S.–Iran nuclear talks** raised fears of escalation in the Middle East. Simultaneously, **Wall Street** faced its own pressures, with the **Nasdaq** bracing for its steepest monthly drop since early 2025 due to cooling sentiment around high-growth technology and AI sectors.

Domestically, while **GDP data** remained a point of underlying strength, the immediate focus shifted toward a "risk-off" tone as the earnings season concluded. Rising **U.S. bond yields** and a stronger dollar further incentivized FII outflows from emerging markets.

Resilient Counters and Deal Drivers

Despite the general gloom, specific stocks rallied on significant corporate developments. **Tejas Networks** emerged as a top gainer, surging **17.50%** to close at **₹436.00**. This rally followed a strategic agreement with **NEC Corporation** to manufacture and supply **5G Massive MIMO radios** for global telecom operators.

**XTGlobal Infotech** also defied the market trend, hitting its upper circuit with a **19.98%** gain. The stock reached an intraday high of **₹39.99** on the back of strong buying momentum and an unfilled demand for small-cap IT services.

Other notable performers included **Sanofi Consumer**, which advanced **14%** following a robust quarterly report showing a **50%** rise in net profit, and **KSB**, which gained **9%** post-earnings.

Market Outlook

The session left the **Nifty 50** testing immediate support levels near **25,100–25,150**. While the broad market remains volatile, selective buying persists in counters with clear regulatory or deal-driven triggers. Investors are maintaining a cautious stance, monitoring global macro factors and FII activity as the new trading month approaches.

Positive

Redington Shares Surge 17% Following Apple Product Launch Teaser

Redington shares experienced a significant surge, gaining as much as 17% in a single session to reach an intraday high of ₹286.00 on the BSE. This rally followed a strategic teaser from Apple CEO Tim Cook, who hinted at a "big week" of product announcements starting Monday, March 2, 2026.

The stock closed approximately 13% higher at ₹276.00, pushing Redington’s market capitalization above ₹22,000 crore. Trading activity was notably aggressive, with volume reaching 8.5 million shares, significantly outpacing the two-week average.

Investor sentiment is centered on Redington’s role as a primary distributor for Apple in India and international markets. Apple products now account for roughly 33% of the company's total revenue, up from 30% in previous quarters.

The anticipated "big week" is expected to feature a refresh across multiple Apple categories. Markets are specifically watching for the debut of the iPhone 17e, positioned as a high-volume, affordable entry-level smartphone.

Other rumored launches include new MacBook Pro models powered by M5 Pro and M5 Max chips, a refreshed MacBook Air, and updated iPad models. Reports also suggest the introduction of a low-cost MacBook, which could broaden the brand’s reach in the education and value sectors.

Financially, Redington reported a strong Q3 FY26, with global revenue reaching ₹30,959 crore, a 16% year-on-year increase. Its core SISA (Singapore, India, and South Asia) region saw a 24% revenue jump to ₹16,600 crore.

Despite robust top-line growth, profit margins in the region grew more modestly at 3%, signaling some cost pressures even as demand for premium electronics remains high. The company is actively diversifying through its "Unlock Next" strategy, focusing on cloud and enterprise solutions to balance its hardware distribution.

Market analysts note that Redington's 1-year performance has now moved to approximately 11.5%, largely aligning with broader benchmark indices like the Nifty 50. However, today's breakout highlights the stock's high sensitivity to Apple’s product cycles and launch momentum.

Industry trends for 2026 suggest a deepening of the premium smartphone and AI-ready PC segments in India. As Apple continues to expand its local manufacturing footprint and retail presence, distributors like Redington remain positioned to capture increased volume from upcoming hardware refreshes.

Positive

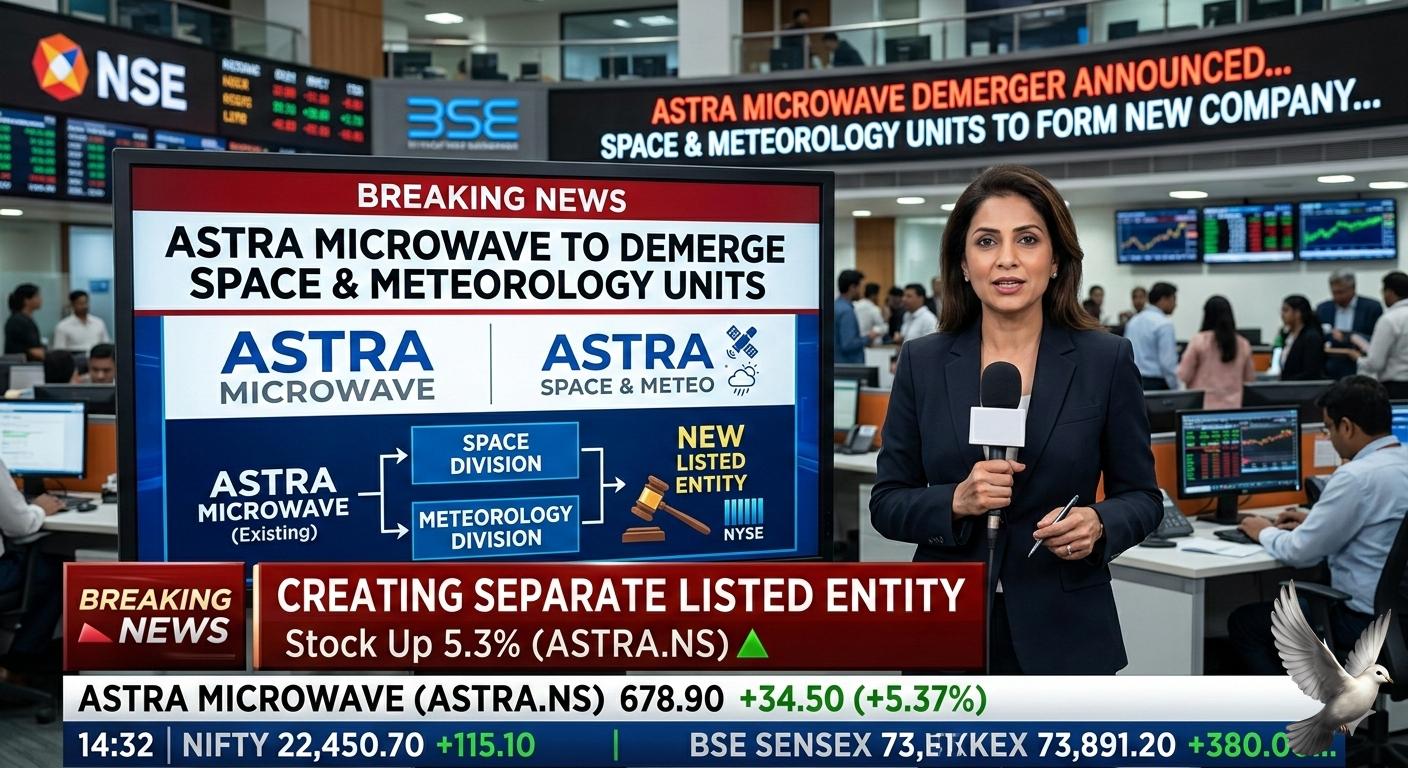

Astra Microwave to Demerge Space and Meteorology Units into Separate Listed Entity

Astra Microwave Products has reached a major corporate milestone with its Board granting in-principle approval for the demerger of its space, meteorology, and hydrology business. This strategic pivot will result in the creation of a new, independently listed entity named **Astra Space Technologies Private Limited (ASTPL)**.

The restructuring is designed to separate the company’s core Defence and Aerospace operations from its rapidly scaling Space and Meteorology segments. Management expects the transition to be completed by **Q1 FY28**.

**Financial Snapshot and Market Context**

Astra Microwave’s market capitalization currently stands at approximately **₹9,419 crore**. As of February 27, 2026, the stock closed near **₹968.60**, maintaining a strong year-on-year growth of over **62%**.

The company recently reported its best-ever quarterly performance for Q3 FY26, with revenue reaching **₹258 crore** and a significant EBITDA margin of **30.9%**. This profitability surge is attributed to a favorable product mix and disciplined execution of its expanding order book.

**The Space and Meteorology Business (ASTPL)**

The new entity, ASTPL, will inherit a legacy of high-performance engineering. Over the past two decades, the space division has executed orders exceeding **₹750 crore** for ISRO, with an additional **₹250 crore** in contracts scheduled for completion by **FY28**.

The Meteorology and Hydrology segment adds further stability, having delivered over **₹330 crore** in contracts to date. This division currently holds an order book of **₹285 crore**. By spinning off these assets, the company aims to provide more granular management focus on capital-intensive satellite and weather radar technologies.

**Strategic Rationale**

The demerger follows a "mirror shareholding" model, ensuring that existing investors receive shares in the new company proportionate to their current holdings. This move is expected to unlock significant shareholder value by:

- Enabling specialized capital allocation for distinct business needs.

- Improving operational efficiency and governance oversight.

- Allowing each entity to pursue sector-specific growth strategies in India’s expanding defense and space ecosystems.

**Looking Ahead**

Astra Microwave continues to hold a robust standalone order book of **₹2,226 crore**. The defense segment remains the primary driver, accounting for roughly **89%** of the total backlog.

With revenue targets set between **₹1,400–₹1,500 crore** for FY27, the company is positioning itself to capitalize on the Indian government’s self-reliance initiatives and the increasing commercialization of the global space sector.

Positive

Indian Rupee Records First Monthly Advance Since April as Traders Evaluate Seasonal Trends

The Indian rupee recorded its first monthly appreciation in nearly a year this February, breaking a downward trend that had persisted since April 2025. The currency strengthened by approximately 1% during the month, climbing from historic lows to trade near the 90.40 level against the U.S. dollar in mid-February.

The primary catalyst for this recovery was the breakthrough announcement of a landmark trade deal between India and the United States. Under the agreement, U.S. tariffs on Indian goods were reduced from 25% to 18%, a move that significantly brightened the outlook for Indian exports. This policy shift effectively removed a major layer of uncertainty that had previously triggered heavy speculative selling of the local unit.

Capital flows also provided a vital cushion. Foreign Portfolio Investors (FPIs) turned into net buyers during the first half of the month, with total net inflows reaching 19,675 crore. A significant portion of this interest was concentrated in debt markets and domestic growth sectors such as capital goods and financials. In a single week ending February 13, net inflows reached 69.34 billion, highlighting a pivot in global investor sentiment toward Indian assets.

Macroeconomic data released in late February added further support to the currency's narrative. India’s GDP growth for the third quarter of fiscal year 2026 reached 7.8% under a newly introduced 2022-23 base year series. While this represented a slight sequential moderation from the previous quarter's 8.4%, it surpassed many market estimates. Additionally, January inflation was contained at 2.75%, remaining well within the central bank's comfort zone.

However, the final days of the month saw some of these gains pared back. On February 27, 2026, the rupee settled at 90.99 against the dollar as profit-taking in the equity markets and renewed geopolitical tensions in the Middle East pressured emerging market currencies. Brent crude oil prices rose to 71.91 per barrel, increasing the dollar demand from importers.

Despite the month-end volatility, the Reserve Bank of India’s strategic interventions near the 91.00 level helped prevent a deeper slide. The month concluded with the rupee positioned significantly higher than its January close, supported by a much-improved trade landscape and a robust domestic growth trajectory.

Positive

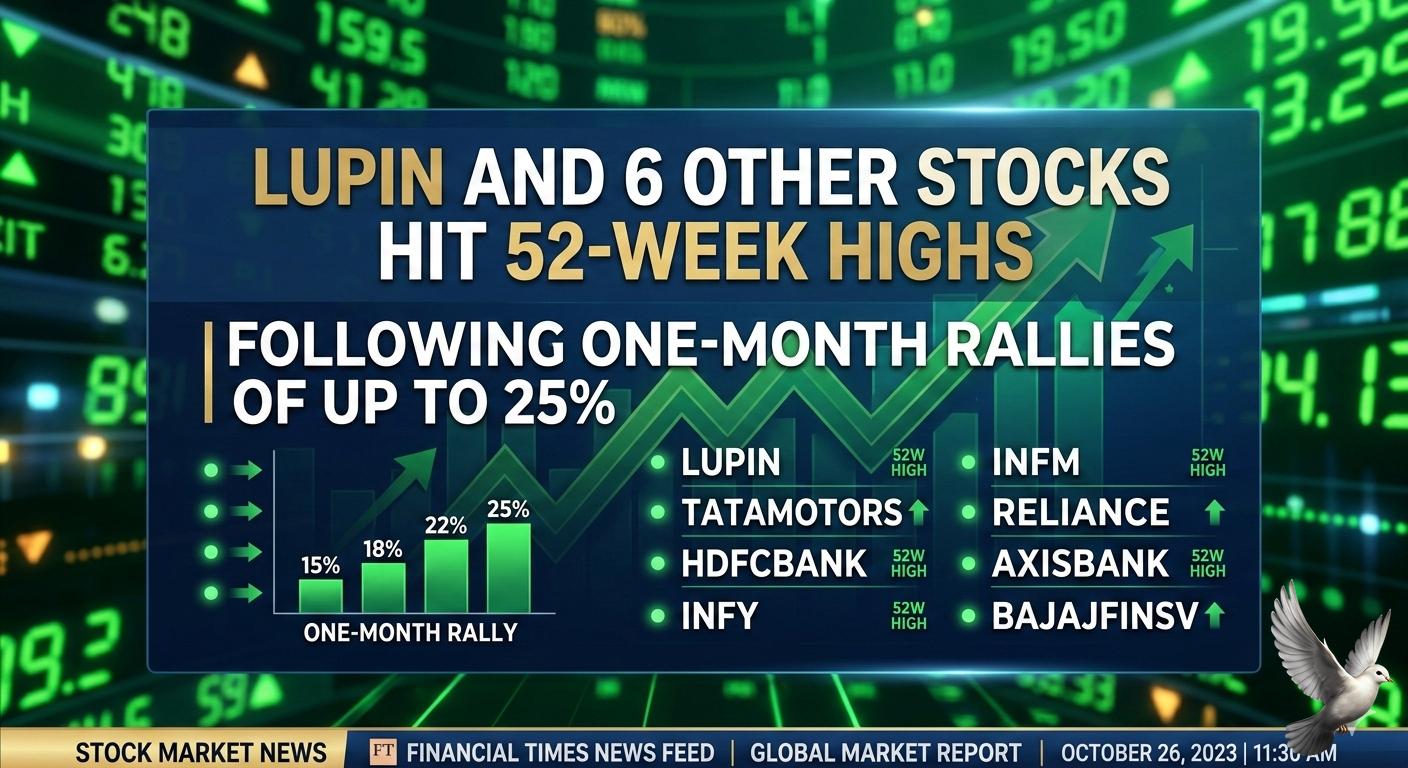

Lupin and 6 Other Stocks Reach 52-Week Highs Following One-Month Rallies of Up to 25%

Global Market Brief: February 27, 2026

Global financial markets are navigating a complex landscape of geopolitical negotiations and shifting economic data. Recent sessions show a distinct divergence between blue-chip stability and high-growth volatility, as investors recalibrate expectations for the remainder of the first quarter.

Equity Market Performance

Wall Street ended its latest session with a mixed profile. The **Dow Jones Industrial Average** managed a slim gain of **0.03%** to close at **49,499.20**. In contrast, the tech-heavy **Nasdaq Composite** saw a sharper decline of **1.2%**, falling to **22,878.38**, while the **S&P 500** retreated **0.5%** to settle at **6,908.86**.

In Asian markets, performance remained fragmented. Tokyo’s **Nikkei 225** rose **0.29%** to **58,753.39**, while South Korea’s **Kospi** tumbled **1.72%**. Indian benchmarks showed resilience but faced pressure, with the **Sensex** holding near **82,248** and the **Nifty 50** hovering around the **25,500** mark.

Commodity Trends and Energy

Energy markets have seen a slight cooling as diplomatic channels remain active. **WTI Crude** eased to **$65.03** per barrel, while **Brent Crude** stayed above the **$70.50** threshold. Despite the immediate dip, analysts maintain a cautious outlook for 2026, with some forecasting an average of **$60.00** per barrel due to a projected supply surplus.

Precious metals are currently in a consolidation phase following a historic rally. Gold futures in New York are trading near **$5,199** per ounce. In domestic markets, **24K Gold** is priced at approximately **₹16,183** per gram, reflecting a minor pullback. Silver has shown significant intraday strength, surging over **3%** to reach **₹2.67 lakh** per kilogram on the back of safe-haven demand.

Inflation and Central Bank Policy

The **European Central Bank** has maintained its deposit facility at **2.00%**, signaling confidence that inflation is converging toward target levels. In India, the **Reserve Bank of India** kept the repo rate unchanged at **5.25%** with a neutral stance.

Economic indicators suggest that global inflation is stabilizing, though base effects from the previous year may cause temporary upticks. The **U.S. Producer Price Index (PPI)** forecast stands at **0.3%**, a figure closely watched as a precursor to consumer pricing trends.

Sector Analysis

The technology sector continues to experience headwinds, with the **Information Technology** sector falling **1.8%** in recent U.S. trading. However, specific pockets of the market, such as **Financials**, gained **1.3%**. In emerging markets, electronics and appliances have seen a reversal in trends, with high-volume trading in local mid-cap leaders indicating a potential floor for recent corrections.

Market volatility, as measured by the **VIX**, increased by **3.9%** to reach **18.63**, suggesting that while panic is absent, caution remains the prevailing sentiment among institutional participants.

Positive

Bharat Biotech Weighs $500 Million Initial Public Offering

Market Brief: Bharat Biotech IPO Outlook

Bharat Biotech International Ltd, the Hyderabad-based pioneer behind India’s indigenous Covid-19 vaccine, is actively exploring an initial public offering (IPO) targeted to raise upwards of **$500 million**.

The move comes as the company seeks to capitalize on its global prominence, having delivered more than **9 billion** vaccine doses worldwide since its inception in **1996**. While the promoter family currently holds **100%** equity, this potential listing would mark a significant transition toward public transparency and market-driven valuation.

Financial Performance & Growth

Recent financial data indicates a strengthening bottom line. The company's revenue rose to **₹1,462.9 crore** in **FY25**, up from **₹1,323.2 crore** the previous year. More impressively, operating profit margins saw a sharp ascent to **28.2%** in **FY25**, compared to just **8.8%** in **FY24**.

This growth is supported by a diversified portfolio. While the oral polio vaccine was historically the primary revenue driver, the company has successfully shifted focus toward higher-volume products like its Typhoid Conjugate (TCV), Rotavirus (RV), and Japanese Encephalitis (JE) vaccines.

Strategic Infrastructure

To bolster future capacity, Bharat Biotech is investing heavily in its Sapigen Biologix facility in Bhubaneswar. The project involves a capital expenditure of **₹200–250 crore** for **FY26**, aimed at creating a large-scale manufacturing hub.

The start of production at this plant is expected to optimize the company's working capital, which saw inventory days spike to **340** in **FY25** due to supply chain build-outs.

Sector Dynamics

The Indian pharmaceutical market is entering **2026** with strong fundamentals, projecting a growth rate between **7.8% and 8.1%**. This momentum is supported by the federal "Biopharma Shakti" initiative, which has earmarked **₹10,000 crore** over the next five years to boost domestic production of biologics and biosimilars.

As a key supplier to the Government of India and UNICEF, Bharat Biotech remains central to institutional procurement, though it continues to navigate the volatility of tender-based pricing and increasing competition in export markets.

IPO Market Context

The primary market for new share sales in India has seen a selective start in **2026**. Investors are currently prioritizing volume-driven growth and sustainable earnings over pandemic-era peaks.

If it proceeds, Bharat Biotech’s **$500 million** offering would serve as a major bellwether for the biotechnology sector, joining a high-profile pipeline that includes major players like Jio Platforms and the National Stock Exchange. Proceeds from the sale are expected to fund further R&D and next-generation vaccine platforms.

Positive

Howard Marks on Investment Strategies Amidst AI Market Growth

Market Brief: AI Investment Landscape

The artificial intelligence sector has reached a critical inflection point where technical capability is no longer in doubt, but market profitability remains a central debate. Billionaire investor **Howard Marks** recently reinforced this sentiment, characterizing AI as a "real" and revolutionary technology capable of reshaping global labor. However, he remains cautious on the investment outlook, noting that current valuations for some startups resemble "lottery tickets" rather than guaranteed returns.

Market Performance and Volatility

February 2026 has been defined by a sharp divergence between record-breaking financial results and cooling investor enthusiasm. **Nvidia**, the industry bellwether, reported a staggering **$68.1 billion** in quarterly revenue—a **73%** year-over-year increase. Despite these historic figures, its stock price fell by over **5.5%** following the announcement, wiping out roughly **$260 billion** in market capitalization as investors questioned the sustainability of massive infrastructure spending.

Broader indices have felt the pressure of this "AI paradox." In early February, the **Nasdaq Composite** saw a pull-back of over **1%** in a single day, while the **S&P 500** continues to hover near the **7,000** mark. This volatility highlights a growing market rotation away from "builders"—the companies providing chips and data centers—toward "users" who can demonstrate clear AI-driven revenue growth.

Infrastructure vs. Monetization

Global spending on AI is projected to exceed **$2.02 trillion** in 2026, a **36%** annual increase. A significant shift is occurring in how this capital is deployed. Expenditure is moving from speculative model training toward **inference**, which focuses on meeting the actual demand for active AI applications.

* **Hyperscaler Capex:** Major tech firms are on track to spend **$527 billion** on capital expenditures this year.

* **Infrastructure Growth:** Software frameworks required to scale autonomous agents are seeing an **83%** growth rate.

* **Economic Impact:** Analysts estimate that AI-related investments contributed roughly **1%** to U.S. GDP growth over the past year.

Strategic Transition to Agentic AI

The market is transitioning from simple generative tools to **Agentic AI**—systems capable of independently executing complex workflows in finance, HR, and legal sectors. While efficiency gains are widespread, the "hard truth" of 2026 is the difficulty of monetization. Companies are moving away from "AI moonshots" to focus on cost minimization and error elimination.

The Investor Dilemma

Howard Marks suggests a balanced approach is mandatory in this environment. While the potential of AI is likely underestimated in the long term, current market prices do not necessarily reflect "bargains." The focus has shifted from whether a company uses AI to how it translates that usage into the bottom line. Success is now measured by **outcome-aligned services** rather than the mere adoption of new tools.

Negative

CA Rudramurthy BV Forecasts Continued Market Weakness and Advises Trader Caution

Indian equity markets concluded a volatile session on February 27, 2026, with benchmark indices suffering sharp declines. The Nifty 50 tumbled **317.90 points**, or **1.25%**, to settle at **25,178.65**.

The BSE Sensex mirrored this weakness, tanking **961.42 points** to end the day at **81,287.19**. This downturn was fueled by a combination of persistent foreign fund outflows and heightened global uncertainty following a lack of progress in international trade and nuclear negotiations.

Market technicals shifted significantly as the Nifty breached its psychological support of **25,300**. This level, which had previously acted as a strong demand zone, now represents an immediate hurdle.

The Bank Nifty index also faced selling pressure, losing its recent momentum. While it remains structurally more resilient than the broader market, it is currently testing critical support near the **60,500** mark.

Foreign Institutional Investors (FIIs) remained aggressive sellers, offloading equities worth **3,465.99 crore** in a single session. Domestic Institutional Investors (DIIs) attempted to cushion the fall by purchasing stocks valued at **5,031.57 crore**, yet this was not enough to prevent a broad-based sell-off.

Sector-specific performance was notably weak in the auto, FMCG, and pharmaceutical spaces. High-profile laggards included Sun Pharma, Bharti Airtel, and Mahindra & Mahindra, which fell by approximately **2%**.

Macroeconomic data released today offered a contrast to the market gloom. India's real GDP growth for the financial year 2025-26 is estimated at **7.6%**, supported by robust manufacturing and service sector performance.

Additionally, retail inflation has remained benign, with the April-December average recorded at a low of **1.7%**. Despite these strong internal fundamentals, external pressures such as rising Brent Crude prices, which jumped **1.26%** to **$71.64** per barrel, continue to weigh on investor sentiment.

The short-term outlook remains cautious. Analysts identify the next major support zone for the Nifty between **25,000** and **24,900**. A failure to hold these levels could invite further corrective pressure. Conversely, the index requires a decisive close above **25,650** to signal a resumption of upward momentum.

Positive

Twelve Large-Cap Stocks Record 50-80% Gains Within One Year

Global Large-Cap Performance Brief: February 2026

The large-cap landscape has shifted into a high-conviction phase as we move through the first quarter of **2026**. While broad market indices show modest gains, a select group of industry leaders is quietly delivering powerful returns between **50% and 80%** over the trailing twelve months.

Market leadership is currently undergoing a structural rotation. The heavy concentration in "Magnificent Seven" stocks that defined recent years is broadening. Investors are now favoring "steady compounders" with resilient cash flows over pure momentum plays.

US Market Momentum

The S&P 500 maintains a bullish trajectory, closing recently near **6,928** points. This represents a year-to-date gain of approximately **8.2%** for the Dow and **12.5%** for the Nasdaq. However, the "easy money" phase has matured, and the market is now rewarding specific execution over general sector exposure.

* **Technology & Infrastructure:** Oracle and Netflix have surged, with gains of **5%** in single sessions, as AI monetization moves from hardware to the application layer.

* **Industrial Strength:** Companies like Caterpillar and Progressive are outperforming without the typical tech-heavy volatility, supported by infrastructure spending and pricing power.

* **Valuation Gap:** The forward P/E ratio for the top mega-caps stands at **28.3x**, while the broader market remains more attractive at **21.8x**.

Emerging Market Resilience

Indian large-caps are showing significant stability despite global volatility. The Nifty 500 delivered a **7%** gain recently, but specific blue-chip leaders are anchored by domestic institutional support and a recovery in rural consumption.

* **Reliance Industries:** Holds a dominant market cap exceeding **₹19,00,000 crore**, acting as a primary stabilizer for regional indices.

* **Banking Sector:** HDFC Bank and ICICI Bank continue to command massive liquidity, with market caps of **₹14,00,000 crore** and **₹10,00,000 crore** respectively.

* **Growth Projections:** India’s GDP is projected at **6.7%** for **2026**, providing a fertile backdrop for large-cap earnings to stabilize even as global rate-cut cycles slow.

Sector Rotation and Risks

A "vicious rotation" is underway as capital exits overcrowded AI trades. Investors are increasing allocations to financials and industrials, which have seen single-day advances of up to **1.4%** even when tech indices retreat.

* **Energy Outperformance:** The energy sector has emerged as a surprise leader in early **2026**, with some constituents up over **55%** on average.

* **Inflation Watch:** Real-time inflation estimates have dipped to **1.55%**, suggesting that while large-caps are sensitive to rates, the downward trend in pricing pressure supports sustained margin expansion.

The current environment defines **2026** not as a crisis year, but as a transition year. Success is no longer guaranteed by buying the "whole shelf" of big tech; it now requires selecting individual "bottles" where earnings growth is backed by actual revenue receipts.