Bearish News

Collection

Crude Oil Drops Below $110 Following Delayed US Strike on Iran

Crude oil prices fell more than 2% during early trade on Tuesday, pulling back from recent highs as investors reacted to potential de-escalation in the Middle East. Market sentiment shifted quickly after the United States announced a postponement of a planned military strike on Iran, explicitly aiming to provide additional time for diplomatic negotiations following appeals from regional leaders. This regulatory freeze on direct military action has provided immediate relief to global supply concerns, reversing the sharp upward momentum built during the previous session. On Monday, international crude oil futures had surged dramatically, with the West Texas Intermediate June contract closing up 3.1% at $108.66 per barrel, and July Brent crude rising 2.6% to reach $112.10 per barrel. The current correction has cooled those immediate price shocks, pulling benchmarks lower. Despite the intraday drop, energy markets remain highly sensitive to physical supply crunches. Global crude and refined inventories have seen a massive reduction of nearly 250 million barrels since regional hostilities escalated, with recent drawdowns dropping at an aggressive pace of roughly 4 million barrels per day. The primary driver for future market directions remains the status of the Strait of Hormuz. Because the waterway acts as a strategic chokepoint handling approximately 20% of global oil and gas production, its effective closure or restricted access keeps massive volumes of energy out of the market, structurally lifting the long-term price floor for crude. Market analysts note that while record-high levels of energy exports from alternative producers have prevented prices from surging toward extreme thresholds like $150, sustained market stabilization relies entirely on concrete breakthroughs in diplomatic negotiations. Until a permanent solution for maritime shipping security is established, crude prices are expected to exhibit high volatility, balancing between immediate geopolitical de-escalation and severe underlying inventory deficits.

Brent crude drops toward $109 per barrel after Trump delays planned strike on Iran

International energy markets experienced a sharp downward correction on Tuesday morning following significant geopolitical developments from Washington. Global benchmark Brent crude fell below **$109** per barrel during early trading, paring more than **2%** from its previous session settlement of **$112.10**. Concurrently, West Texas Intermediate (WTI) futures dropped **1.8%** to trade around **$102.48** per barrel, down from the prior close of **$104.38**. This market shift marks a notable reversal from overnight trading sessions where Brent had spiked to a high of **$112**. The immediate catalyst for the price decline was an announcement from US President Donald Trump stating he would temporarily hold off on a military strike against Iran that had been scheduled for Tuesday. The decision to delay the escalation came after direct appeals from Middle Eastern leaders and regional allies, reviving thin hopes that a diplomatic resolution could prevent a wider conflict. Despite the temporary relief, the broader market remains highly volatile. Energy infrastructure across the Middle East continues to operate under high-risk conditions. Global crude prices have surged more than **50%** since initial military strikes involving the US, Israel, and Iran on February 28, which led to a partial blockade and severe disruption of tanker flows through the Strait of Hormuz. The ongoing maritime bottlenecks continue to strain physical supply buffers. According to recent energy data, global oil inventories fell by an average of **8.5 million** barrels per day over the second quarter, shrinking the available supply cushion in major developed economies. However, severe headwinds on the demand side are keeping a lid on further price run-ups. High fuel costs and international supply blockages are denting consumption. Global oil consumption is currently forecast to contract by **2.4 million** barrels per day year-over-year during the second quarter, leading to a broader projected annual decline of **420,000** barrels per day for the full year. Even with lower global consumption patterns, the structural deficit in the physical market is expected to persist into the latter half of the year. Market analysts continue to warn that any prolonged or permanent closure of the Strait of Hormuz—the world's most critical oil transit chokepoint—will cause severe, compounding shortages for global oil tankers and international product delivery.

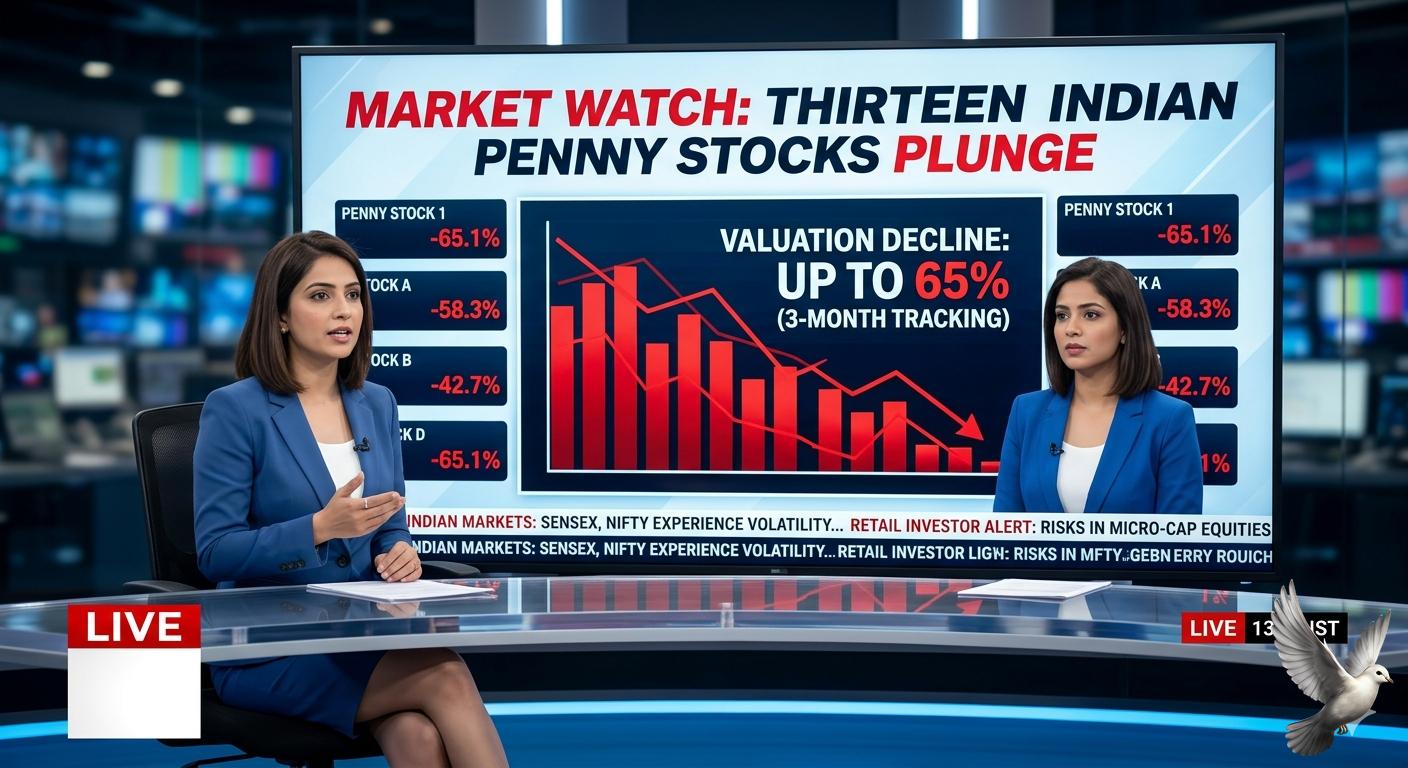

Thirteen Indian Penny Stocks Experience Valuation Declines of Up to 65% Over a Three-Month Tracking Period

Retail participation in the low-priced equity segment has faced a severe structural reality check. A cohort of thirteen highly-traded penny stocks listed on domestic exchanges has experienced sharp valuation corrections, plunging by up to **65%** within a rolling three-month tracking period. This widespread capitulation highlights the escalating risks within micro-cap equities, catching speculative retail traders off guard. The steep losses across these specific counters reflect a broader shift in market liquidity and heightened regulatory scrutiny on low-float stocks. Leading the downward spiral, specialized micro-cap entities in the textile, infrastructure, and digital services sectors saw the most severe wealth erosion. Three prominent counters in this list lost more than **50%** of their market value in ninety days, heavily driven by retail panic selling and the sudden absence of institutional buying support. Market tracking indicates that corporate governance issues, weak quarterly financial fundamentals, and high debt-to-equity ratios triggered the sell-off. As interest rates remain structurally elevated globally, highly leveraged small enterprises are facing severe operational headwinds, directly impacting their equity valuations. This correction coincided with a volatile period for the broader market benchmarks. While the headline BSE Sensex and NSE Nifty hovered near record territories, the broader mid-cap and small-cap indices faced visible profit-booking pressure. Institutional investors have been systematically rotating capital away from high-beta penny counters into defensive large-cap alternatives. Regulatory changes have also played a crucial role in accelerating this downside momentum. Stringent surveillance measures, including enhanced short-term Additional Surveillance Measure frameworks, have limited speculative intraday leverage on low-priced shares, directly drying up trading volumes. Financially overextended retail accounts have borne the brunt of this **65%** drop, with many locked into lower circuit freezes for consecutive trading sessions. Market analysts warn that ultra-low-priced equities often suffer from low liquidity, making it exceedingly difficult for retail participants to exit their positions during a structural downturn. The widespread losses in these thirteen penny stocks serve as a stark reminder of the underlying volatility in the micro-cap ecosystem, where speculative hype often decouples from actual corporate earnings.

Rupee Approaches Record Low as Rising Oil Prices Strain Indian Markets

The Indian financial ecosystem is managing severe macroeconomic headwinds as geopolitical volatility in West Asia drives a sharp depreciation in the domestic currency. Increased risk aversion and escalating energy import bills have pushed the Indian rupee to historic lows against the US dollar. The domestic currency recently breached the psychological threshold of **95.00**, touching an all-time intraday low of **95.96** against the US dollar. This move represents a year-to-date decline of more than **6%**, positioning the rupee as the weakest performing major currency in Asia for the year. A primary driver behind this pressure is the sharp inflation of global energy costs. Brent crude oil futures are trading between **$100 and $110 per barrel**, with the Indian basket averaging **$115 per barrel** in April and hovering near **$106 per barrel** in May. Because India imports approximately **85%** of its crude oil requirements, every **$1** increase per barrel adds an estimated **₹12,000 crore to ₹16,000 crore** to the annual national import bill. The escalating import bill has rapidly expanded the current account deficit, triggering a surge in corporate dollar demand. In response, authorities have deployed defensive measures to protect foreign exchange reserves and absorb the shock. The government implemented a sharp tariff adjustment, raising the import duty on gold and silver from **6% to 15%** to curb non-essential dollar outflows. Voluntary demand-side push strategies are also being leveraged, with economic assessments indicating that a modest **10%** reduction in crude imports could preserve up to **$13.4 billion** in foreign exchange reserves. The Reserve Bank of India has actively intervened in the spot foreign exchange market, utilizing billions of dollars from its **$696.9 billion** foreign exchange reserves buffer to smooth out extreme volatility and prevent an unchecked spiral. The broader equity markets reflect these underlying macroeconomic strains. Broad-based selling pressure has pushed the benchmark NSE Nifty 50 down to **24,176.15**, while the BSE Sensex trades near **74,638.74**. Foreign institutional investors have intensified capital outflows, offloading equities worth **₹1,959.39 crore** in isolated daily sessions, adding further structural pressure to the equity ecosystem. Beyond capital flows, the energy shock presents direct challenges to domestic growth and inflation management. Retail inflation rose to **3.48%** in April, while wholesale inflation scaled a three-and-a-half-year high of **8.3%**, driven by escalating transport, food, and energy inputs. Updated economic projections suggest that a sustained crisis could shave up to **0.6%** off India's baseline GDP growth, potentially moderating the expansion rate to **6.3%** for the current fiscal year.

India's AI Gap Signals Potential End to Market Outperformance

The Indian stock market is navigating a pronounced structural shift as a record volume of foreign capital exits domestic equities. Foreign institutional investors have pulled **$22 billion** out of the market so far this year, already surpassing the previous year's **$19 billion** total outflow. This capital flight marks the sharpest annual foreign selloff in over two decades, reducing foreign equity ownership to a **14-year low of 16%**. Domestic institutional investors have stepped in to stabilize the market, with their ownership rising to a record **17%**, overtaking foreign holders for the first time in more than twenty years. Mutual funds specifically now control **11.4%** of the domestic market capitalisation. Despite this domestic support, the broader indices have faced visible pressure, with the Nifty 50 closing down **2.20%** for the week at **23,643.50**, while the Indian rupee touched a record low of **96.14** against the US dollar. Global fund managers remain underweight on Indian equities by approximately **220 basis points** relative to benchmark allocations. Investors are redirecting capital toward alternative regional markets, driven by concerns over premium valuations and emerging operational challenges within India's tech sector. The benchmark Information Technology index has corrected by roughly **25%** year to date. This pressure stems from fears of structural deflation in traditional IT services, where automated workflows threaten standard hourly billing models. Industry projections indicate traditional revenue streams could face an annual deflation rate of **2% to 3%** over the next few years. Up to **30%** of the legacy services industry is currently deemed exposed to automated delivery shifts, creating a potential baseline revenue risk of **$40 billion**. Despite the immediate compression in effort-based pricing, domestic technology enterprise spending is projected to grow between **6% and 8%** this year, outpacing global peers by over **200 basis points**. Total domestic enterprise IT spending is forecast to reach **$176.3 billion**, with specific infrastructure segments like data centers projected to grow by **20.5%**. Market analysts view the current downturn as a transition phase rather than a permanent breakdown of the corporate services model. The industry expects to eventually capture between **$300 billion and $400 billion** in new expanded market opportunities by the end of the decade as companies move from experimental pilots to full-scale platform modernization.

Oil Prices Up 3% Amid Extended US-Iran Negotiations

Oil prices surged nearly 3% on Friday as energy markets reacted to a high-stakes extension of nuclear negotiations between the United States and Iran. Traders are increasingly concerned that a potential breakdown in diplomacy could trigger immediate supply shocks in the Middle East. WTI crude futures climbed toward $67 per barrel, reaching a seven-month high. Brent crude also saw significant movement, trading around $72.78. These gains were fueled by reports that while Iran described talks in Geneva as progressive, U.S. officials expressed disappointment, signaling a widening gap between the two sides. Geopolitical risk premiums are currently estimated between $4 and $10 per barrel. The market is pricing in the possibility of a disruption to Iran’s 3.3 million barrels per day of production. Concerns are also mounting over the security of the Strait of Hormuz, a critical maritime artery that handles approximately 20% of the world's global oil supply. Regional tensions have escalated further following the U.S. decision to authorize the departure of non-emergency staff and families from Mission Israel. This atmosphere of uncertainty has overshadowed recent data showing a massive 15.9 million barrel build in U.S. crude stocks, which would typically exert downward pressure on prices. Supply dynamics remain complex as OPEC+ prepared for its Sunday meeting. The group is widely expected to maintain its cautious stance, with analysts anticipating a modest production increase of 137,000 barrels per day for April. This comes as Saudi Arabia reportedly nears a three-year high in exports as part of a contingency plan to stabilize the market in the event of regional conflict. For the month of February, oil prices have risen approximately 2.5%, extending a sharp 13.6% rally recorded in January. While long-term forecasts from the IEA and major banks suggest a global supply surplus for 2026, the immediate focus of the market remains fixed on the March 1–6 deadline for a nuclear agreement. Technical indicators show WTI has broken above its 200-day moving average, confirming a reversal of the previous bearish trend. Investors are now watching the $70 mark as the next psychological resistance level for WTI, provided geopolitical frictions remain unresolved.

CA Rudramurthy BV Forecasts Continued Market Weakness and Advises Trader Caution

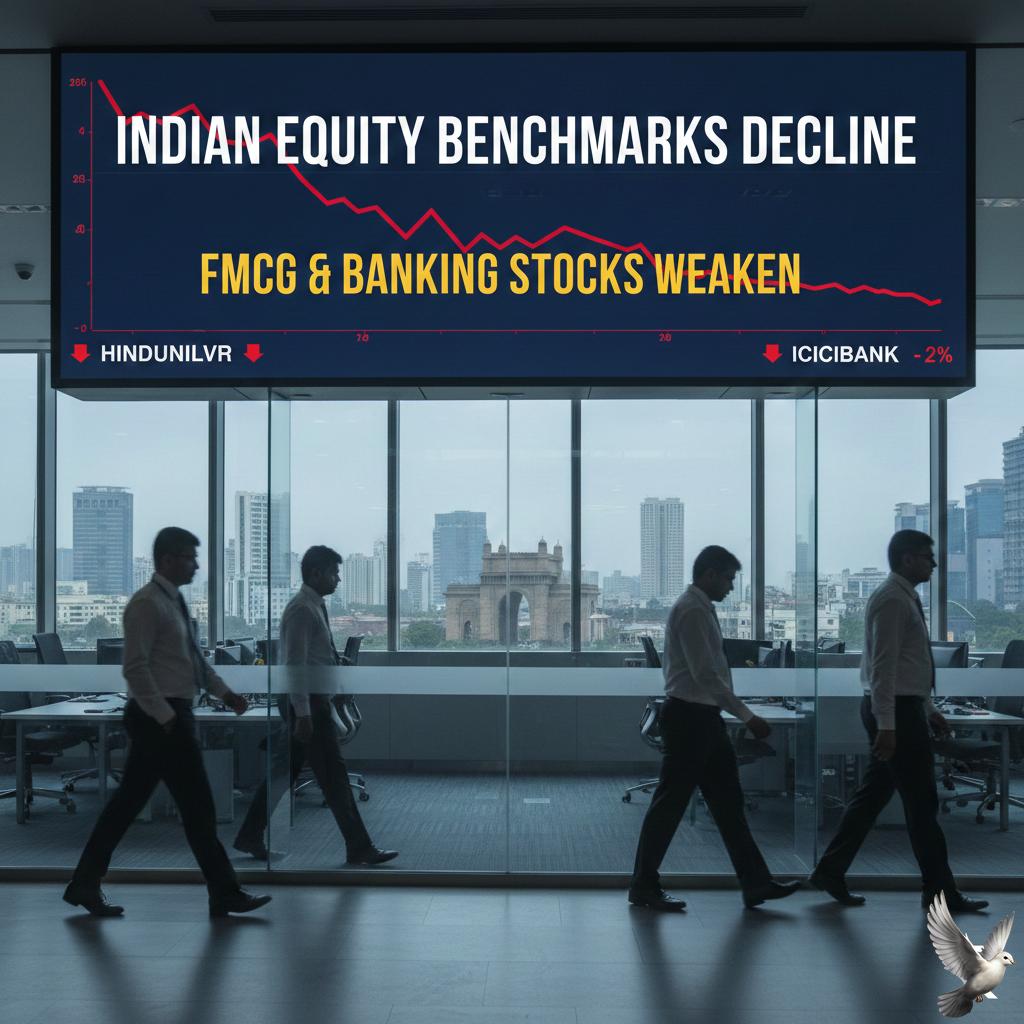

Indian equity markets concluded a volatile session on February 27, 2026, with benchmark indices suffering sharp declines. The Nifty 50 tumbled **317.90 points**, or **1.25%**, to settle at **25,178.65**. The BSE Sensex mirrored this weakness, tanking **961.42 points** to end the day at **81,287.19**. This downturn was fueled by a combination of persistent foreign fund outflows and heightened global uncertainty following a lack of progress in international trade and nuclear negotiations. Market technicals shifted significantly as the Nifty breached its psychological support of **25,300**. This level, which had previously acted as a strong demand zone, now represents an immediate hurdle. The Bank Nifty index also faced selling pressure, losing its recent momentum. While it remains structurally more resilient than the broader market, it is currently testing critical support near the **60,500** mark. Foreign Institutional Investors (FIIs) remained aggressive sellers, offloading equities worth **3,465.99 crore** in a single session. Domestic Institutional Investors (DIIs) attempted to cushion the fall by purchasing stocks valued at **5,031.57 crore**, yet this was not enough to prevent a broad-based sell-off. Sector-specific performance was notably weak in the auto, FMCG, and pharmaceutical spaces. High-profile laggards included Sun Pharma, Bharti Airtel, and Mahindra & Mahindra, which fell by approximately **2%**. Macroeconomic data released today offered a contrast to the market gloom. India's real GDP growth for the financial year 2025-26 is estimated at **7.6%**, supported by robust manufacturing and service sector performance. Additionally, retail inflation has remained benign, with the April-December average recorded at a low of **1.7%**. Despite these strong internal fundamentals, external pressures such as rising Brent Crude prices, which jumped **1.26%** to **$71.64** per barrel, continue to weigh on investor sentiment. The short-term outlook remains cautious. Analysts identify the next major support zone for the Nifty between **25,000** and **24,900**. A failure to hold these levels could invite further corrective pressure. Conversely, the index requires a decisive close above **25,650** to signal a resumption of upward momentum.

Indian Equity Benchmarks Decline Amid Weakness in FMCG and Banking Stocks

Market Brief: Indian Equities & Global Cues Indian benchmark indices faced downward pressure on Friday, **February 27, 2026**, as a combination of domestic sector weakness and cautious global sentiment weighed on investor confidence. Domestic Market Performance The **S&P BSE Sensex** dropped over **250 points** in early trade, hovering near the **81,990** level. Simultaneously, the **Nifty50** slipped approximately **90 points**, testing the critical support zone around **25,400**. Heavyweight selling in the banking and FMCG sectors acted as the primary drag. **HDFC Bank** and **Bharti Airtel** emerged as notable laggards, while consumer staple stocks saw range-bound movement following recent volatility. Sectoral Highlights & IT Resilience In contrast to the broader decline, the **IT sector** showed relative resilience. Despite recent concerns regarding automation and global tech spending, select software majors provided a minor cushion to the indices. The automotive segment saw mixed results, with **Tata Motors** gaining nearly **1%** in early deals. However, the overall market breadth remained tilted toward the bears, reflecting a cautious "stock-picker's" environment. Institutional Flows Foreign Institutional Investors (**FIIs**) returned to a selling bias, offloading equities worth approximately **₹3,465 crore** in the previous session. This outflow follows a brief period of net buying earlier in the month. Domestic Institutional Investors (**DIIs**) continued their role as market stabilizers, recording a net purchase of over **₹5,031 crore**. The persistent "tug of war" between foreign exits and domestic inflows remains a defining theme for Dalal Street. Global Outlook & Commodities Wall Street provided weak cues as the **Nasdaq Composite** and **S&P 500** faced pressure from rising bond yields and geopolitical uncertainties. Asian peers, including the **Hang Seng**, traded lower by nearly **0.9%**, while the **Nikkei 225** managed marginal gains. Energy markets are currently navigating a volatile equilibrium. **Brent crude** prices hovered near **$71 per barrel**, while **WTI** traded around **$65**. Recent diplomatic efforts in Geneva aimed at easing U.S.-Iran tensions have slightly cooled the "war premium," though prices remain elevated compared to late 2025 levels. Higher crude costs continue to pose a lingering risk to India’s inflationary outlook and fiscal deficit.

Ola Electric Shares Decline 84% From Peak to Rs 25 Following Significant Market Correction

Ola Electric shares hit a critical low of **25.13** as of February 27, 2026, marking a staggering **84%** collapse from their post-listing peak of approximately **157**. The stock is now trading significantly below its initial issue price, reflecting a severe erosion of investor confidence. Market capitalization has shriveled to **11,270 crore**, a sharp contrast to its valuation during the 2024 surge. The company’s market share in the electric two-wheeler segment has plummeted to under **6%** in early 2026, down from a dominant **35%** in late 2024. This decline is attributed to a combination of rising competition and persistent quality concerns. Financial performance for the quarter ending December 2025 highlights the deepening crisis. Revenue from operations crashed **55%** year-on-year to **470 crore**, down from **1,045 crore** in the previous year. Quarterly sales volumes also saw a steep drop to approximately **32,000 units**, as legacy players like TVS Motor and Bajaj Auto consolidated their grip on the market. Regulatory pressure has intensified following an administrative warning from SEBI regarding disclosure violations. Additionally, the Central Consumer Protection Authority has scrutinized the firm over more than **100,000** registered consumer complaints related to hardware defects and software glitches. The company is currently executing a "structural reset" to lower its quarterly operating expenses from a peak of **840 crore** to a target of **250 crore**. Despite these cost-cutting measures, major brokerages including Goldman Sachs have downgraded the stock to Neutral, slashing price targets to as low as **26** or even **20** in bearish scenarios. Analysts remain cautious as the firm navigates high cash burn and technical sell-offs. The stock is currently trading below all major moving averages, including the **50-day** and **200-day** lines, signaling a sustained negative market structure. Investors are closely monitoring the upcoming deployment of a **250-member** rapid-response team aimed at clearing massive service backlogs to stabilize the brand's reputation.

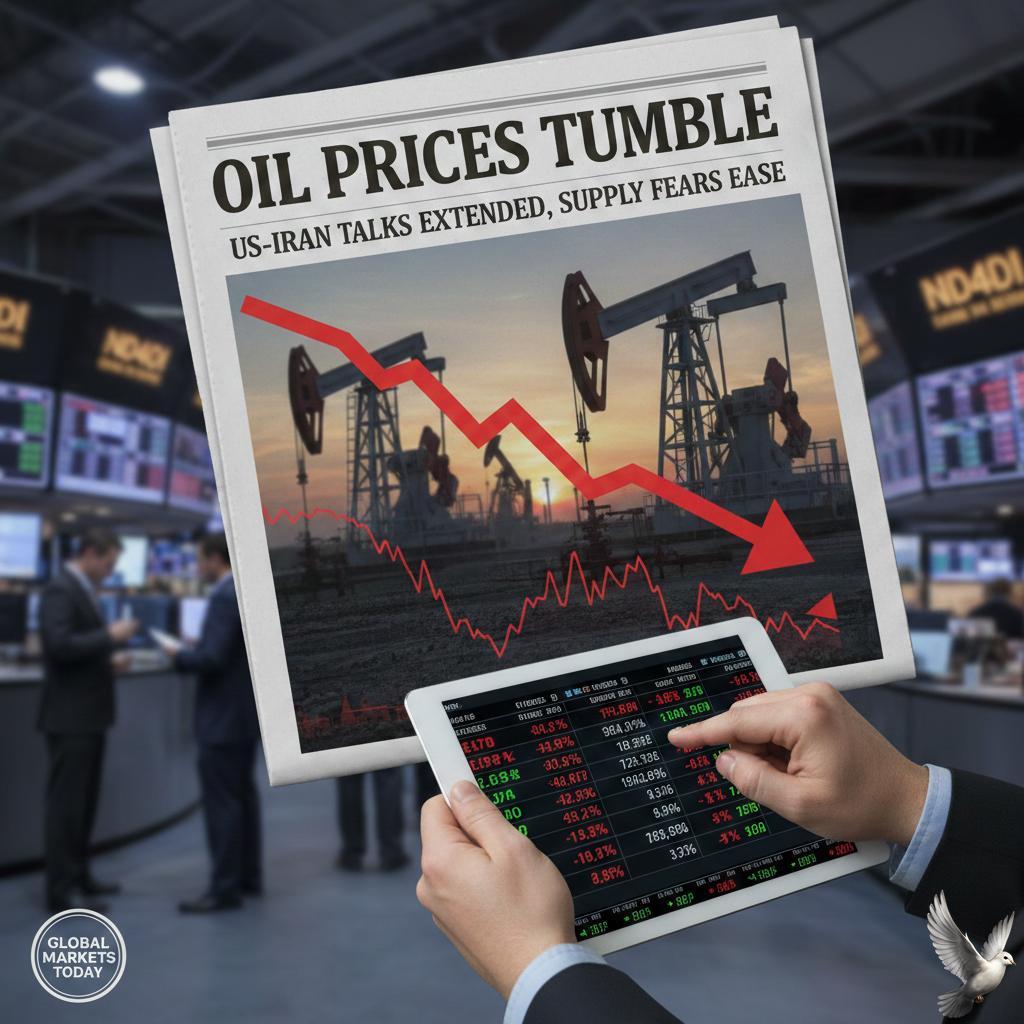

Oil Prices Decline Amid Extension of US-Iran Negotiations

Crude oil prices are moving into the weekend on a downward trajectory, with benchmarks posting weekly losses as high-stakes diplomacy in Geneva alters the risk landscape. WTI crude futures settled near $65.46 per barrel, while Brent crude fluctuated just above the $70.00 mark. These levels represent a weekly decline of approximately 2.2% for WTI and 1.8% for Brent, reversing much of the geopolitical premium added earlier in the month. The primary driver for this cooling sentiment is the extension of nuclear negotiations between the United States and Iran. While American officials expressed some disappointment with the lack of a definitive breakthrough, the agreement to continue technical discussions in Vienna next week has temporarily eased immediate fears of a military escalation. Market participants are closely watching a looming March deadline set by Washington. The situation remains volatile, as Tehran recently stated it would not allow enriched uranium to leave the country—a key sticking point for Western negotiators. Supply dynamics are also weighing on prices. Recent data shows U.S. crude inventories jumped by 16 million barrels last week, the largest increase in three years. This surge in domestic stocks coincides with U.S. production holding steady near record highs of 13.7 million barrels per day. Additionally, output from major exporters is rising. Saudi Arabia’s exports are approaching a three-year peak, and increased flows have been noted from Iraq, Kuwait, and the UAE. This contributed to a broader narrative of a looming global supply glut, with some agencies forecasting a surplus as high as 3.7 million barrels per day for 2026. Focus now shifts to the upcoming OPEC+ meeting this Sunday. The group is widely expected to discuss a modest production hike of 137,000 barrels per day for April. Traders are looking for clarity on whether the alliance will stick to its plan to restore production or maintain current cuts to combat the growing inventory builds. Global demand remains a point of contention among analysts. While the IEA recently lowered its 2026 demand growth forecast to 850,000 barrels per day citing economic uncertainty, other agencies remain more optimistic. Non-OECD economies, led by China and India, are expected to account for nearly all consumption gains this year. For the immediate term, technical-level meetings in Vienna and the Sunday OPEC+ decision will serve as the next major catalysts for price direction. Support for WTI is currently identified in the $62.00 to $63.00 range, while any further breakdown in nuclear talks could quickly reintroduce a risk premium toward the $72.00 resistance level.

SEBI Issues Advisory on Fraudulent Securities Transaction Tax Payment Notices

The Securities and Exchange Board of India (SEBI) and the National Stock Exchange (NSE) have issued an urgent dual-alert following a surge in sophisticated financial scams targeting retail investors. The most critical warning involves the circulation of forged notices demanding immediate payment of Securities Transaction Tax (STT). Fraudsters are now using high-quality forged SEBI letterheads, logos, and seals to demand tax payments under the Finance Act, 2004. These fake documents often cite the SEBI Act, 1992, to threaten legal action if payments are not made. The regulator has explicitly clarified that it never issues notices to individual investors for the collection of STT. Investors must note that STT is an automated levy. It is charged on every buy and sell transaction executed on stock exchanges and is collected directly by brokers at the time of the trade. SEBI does not coordinate with the Reserve Bank of India (RBI) or any other body for the manual collection of this tax from individuals. Beyond tax fraud, SEBI has flagged a rising trend in "account handling" scams. Unregistered individuals are posing as expert fund managers or portfolio providers, promising risk-free or guaranteed profits. These operators typically demand access to private trading credentials and ask for a share of the profits while leaving the investor to bear 100% of any losses. To protect capital, investors are urged to verify the registration status of any entity on the official SEBI website before committing funds. Genuine communications from the regulator will only originate from official domains, and any request for a direct money transfer to a personal or non-official account should be treated as a red flag. The market environment in February 2026 remains volatile, with the Nifty 50 down approximately 2.7% year-to-date as of late February. Amidst this uncertainty, retail participation remains high, with SIP inflows crossing 31,000 crore in recent months. This high level of activity has made the retail segment a primary target for impersonation tactics. Security experts advise investors to stick to authentic trading apps and registered intermediaries. If you receive a suspicious notice, do not engage with the sender or provide sensitive financial data. Official verification of all documents through the SEBI and NSE portals is the only way to ensure the legitimacy of a communication.

Eurozone Bond Yields Hold Near Multi-Month Lows Ahead of Inflation Data

Eurozone government bond yields are stabilizing near multi-month lows as global markets absorb strong corporate earnings and prepare for critical inflation data. German 10-year Bund yields are currently holding steady around **2.71%**, recovering slightly from recent slides to late-November levels. This stabilization reflects a cautious "wait-and-see" approach among investors ahead of preliminary February consumer price index (CPI) reports from Germany, France, and Spain scheduled for Friday. European Central Bank President Christine Lagarde recently signaled that headline inflation is expected to converge to the **2.0%** target in the medium term. Core Eurozone inflation is forecast to ease slightly to **2.2%** year-on-year, while the headline rate is expected to hold firm at **1.7%**. Market sentiment received a significant boost from Nvidia’s latest fiscal results, which saw revenue jump **73%** to **$68.1 billion**. The tech leader’s record data center sales of **$62.3 billion** have bolstered risk appetite across global sectors, temporarily diverting pressure from the sovereign debt market. Currency markets show the Euro holding steady just below the **$1.18** mark. Investors are tracking how currency strength might impact price pressures and influence the ECB's upcoming policy decisions, with the bank currently maintaining key deposit rates at **2.15%**. Broader economic indicators show modest resilience, with Germany’s IFO Business Climate Index rising to **88.6** in February. However, geopolitical tensions and new global trade tariff threats continue to add a layer of complexity to the long-term yield outlook. [Nvidia Earnings: Live Updates and Commentary](https://www.google.com/search?q=https://www.youtube.com/watch%3Fv%3DR9j0EAnE-8Q) This video provides an in-depth look at Nvidia's record-breaking financial performance and its direct impact on global market risk appetite and technology sector trends.

Jane Street Shifts Focus to Crypto Amid Ongoing Market Challenges

Wall Street trading powerhouse Jane Street is currently facing a dual-front legal battle, with high-stakes allegations of market manipulation and insider trading spanning from New York to Mumbai. These developments come as the firm continues to defend its role in some of the most volatile market events of the last several years. In a lawsuit filed on February 23, 2026, the administrator for the Terraform Labs estate accused Jane Street of using "material non-public information" to profit from the 2022 collapse of the TerraUSD (UST) and Luna ecosystem. The collapse originally erased an estimated 40 billion dollars in market value. The legal complaint highlights a critical window on May 7, 2022. Within 10 minutes of Terraform Labs withdrawing 150 million UST from a liquidity pool, a wallet allegedly linked to Jane Street withdrew 85 million UST from that same pool. This move is characterized as a turning point that triggered the final market panic. Jane Street has formally denied the claims, describing them as a "desperate and transparent attempt to extract money." The firm maintains that the catastrophic losses were the direct result of a multibillion-dollar fraud orchestrated by Terraform Labs’ own management. This litigation follows the sentencing of Terraform co-founder Do Kwon, who is currently serving a 15-year prison sentence in the United States. Kwon pleaded guilty to charges of wire fraud and conspiracy after his 2024 extradition. His crimes were described by federal judges as "fraud of an epic generational scale." Simultaneously, Jane Street is embroiled in a significant dispute with the Securities and Exchange Board of India (SEBI). On February 25, 2026, the Securities Appellate Tribunal (SAT) adjourned a hearing regarding a 580 million dollar (4,844 crore rupees) fine and temporary trading ban imposed on the firm. SEBI alleges that Jane Street engaged in a "pump-and-dump" scheme involving the Bank Nifty Index between early 2023 and March 2025. The regulator claims the firm used high-frequency algorithms to push the index up by 1% to 1.3% on derivative expiry dates to capture illicit profits. To resume operations in the Indian market, Jane Street deposited the full 580 million dollar amount into an escrow account. The firm continues to challenge the findings, arguing it was an "index arbitrage" strategy and that it was denied access to critical regulatory documents during the investigation. The broader cryptocurrency market has reacted sharply to these legal pressures. Following the news, market analysts noted a pause in what traders call the "10 a.m. dump"—a pattern of heavy selling often attributed to large algorithmic players. Despite the legal uncertainty, Bitcoin remains volatile, recently testing support levels near 63,000 dollars while attempting to reclaim the 70,000 dollar psychological barrier.

SAT Adjourns Jane Street Hearing to April 17

The Securities Appellate Tribunal (SAT) has adjourned the high-stakes hearing between US-based high-frequency trader Jane Street and the Securities and Exchange Board of India (SEBI). The next session is now scheduled for April 17, 2026. This delay follows a request for additional time to review regulatory responses submitted earlier this year. The dispute stems from a landmark interim order passed in July 2025. SEBI accused Jane Street of a sophisticated market manipulation scheme targeting the Bank Nifty index. The regulator alleged the firm used a two-pronged strategy: buying large quantities of constituent stocks to artificially inflate the index while simultaneously holding massive short positions in the derivatives market. SEBI initially imposed a trading ban and a massive fine of 4,844 crore rupees (approximately 570 million dollars) to disgorge what it termed "unlawful gains." While the US firm maintains that its actions were legitimate index arbitrage, it complied with the directive to deposit the full 4,844 crore rupees into an escrow account. Following this deposit, SEBI lifted the trading ban in late July 2025, though the firm reportedly remains cautious about resuming full operations. The legal battle has now shifted to the tribunal. Jane Street’s appeal challenges the regulator's findings and argues that it was denied access to critical documents used to build the case. The firm claims these materials are essential for its defense. Meanwhile, recent financial reports show Jane Street's India arm saw a six-fold surge in trading gains prior to the regulatory crackdown, reporting net trading profits of nearly 4,700 crore rupees in the 2025 fiscal year. Market observers are closely watching the April 17 hearing. The outcome will likely set a precedent for how high-frequency trading and arbitrage strategies are regulated in India’s rapidly growing derivatives market. For now, the 4,844 crore rupees remain under lien in favor of the regulator as the judicial process continues. [Jane Street vs SEBI SAT Adjournment](https://www.youtube.com/watch?v=udy7zSXEYxQ) This video provides a concise summary of the SAT's decision to adjourn the hearing and the background of the massive 4,844 crore rupee escrow deposit. http://googleusercontent.com/youtube_content/0

RBI to Hold Rs 25,000 Crore Government Securities Switch Auction on March 2

The Reserve Bank of India has scheduled a significant government securities switch auction for March 2, 2026. This operation involves the exchange of short-term debt for longer-dated instruments totaling 25,000 crore. The auction is set to take place between 10:30 AM and 11:30 AM, with settlement finalized by March 4. This move marks the third such operation this month as the central bank intensifies efforts to manage a massive maturity wall. This strategy is designed to alleviate the redemption pressure projected for FY27, a year when the government faces bond repayments worth 5.47 lakh crore. By replacing these upcoming obligations with bonds maturing after FY32, the RBI is effectively stretching the debt profile to more manageable horizons. The current fiscal environment remains demanding. The gross market borrowing for FY27 is budgeted at a record 17.2 lakh crore, an 18% increase compared to the previous year. Net market borrowings are estimated at 11.7 lakh crore. These high figures reflect the government's ongoing funding needs despite a narrowing fiscal deficit target, which has been set at 4.3% of GDP for FY27. Market dynamics have shown some volatility in response to these supply pressures. The 10-year benchmark bond yield recently hovered around the 6.67% to 6.69% range. While domestic inflation remains moderate at 2.75% and systemic liquidity sits in a surplus of over 2 lakh crore, the heavy pipeline of central and state government bond sales continues to keep yields under pressure. To date, the RBI has already conducted successful buybacks and switches worth approximately 84,804 crore in February alone. These proactive measures are critical for maintaining stability in the sovereign debt market as the financial system transitions into a year of record-high issuance and significant repayment obligations. [RBI Market Update](https://www.youtube.com/watch?v=z01RGOV-ZNw) This video provides an expert analysis of the February 2026 debt market outlook, covering the specific borrowing impacts and yield trends discussed in the brief. http://googleusercontent.com/youtube_content/0

JPMorgan CEO Jamie Dimon Cites AI and Operational Risks as Potential Drivers of 2008-Style Financial Crisis

Market Brief: Systemic Fragility and the AI Disruption Current financial conditions are exhibiting growing parallels to the era preceding the **2008 global financial crisis**. Analysts and industry leaders observe that a "rising tide" of liquidity has pushed asset prices to elevated levels, fostering a dangerous sense of complacency across global markets. Traditional risk awareness is being dulled by prolonged periods of high trading volumes and record-breaking stock performance. As of **February 2026**, the **S&P 500** continues to trade near historic highs, even as underlying credit markers begin to signal stress. Credit Market Strain The lending environment is seeing a shift toward riskier behavior. Competitive pressure is driving some institutions to stretch underwriting standards to maintain net interest income. This "chase for yield" mirrors the pre-2008 cycle where leverage was increased to unsustainable levels. Specific stress points are emerging in the private credit and corporate debt sectors. * **Exchange-Traded Funds (ETFs)** now hold approximately **25%** more corporate bonds than US banks. * Total corporate debt outstanding has ballooned to roughly **$16 trillion**. * Broker-dealer holdings have dropped from over **$300 billion** pre-2008 to between **$70 billion and $80 billion** today, significantly reducing market liquidity during potential downturns. The AI Catalyst While the 2008 crisis was rooted in subprime mortgages, the next cyclical downturn may find its catalyst in the technology sector. The enthusiasm surrounding **Artificial Intelligence (AI)** is creating "tectonic shifts" in software and service industries. There is a growing concern that AI disruption could sour the credit cycle as entire industries come under pressure from rapid automation and shifting business models. Recent volatility in software stocks highlights this sensitivity. While AI infrastructure spending currently contributes roughly **1%** to US economic growth, a failure in the "AI boom" could erase the wealth effects currently propping up consumer sentiment. Economic Indicators Global economic data remains mixed, adding to the atmosphere of uncertainty. * **Headline inflation** in key regions like Australia remains stuck at **3.8%**, while European inflation has dipped to **1.7%**. * **Gold** has surged to **$5,017** per ounce, reflecting a flight to safe-haven assets amid geopolitical tensions and market anxiety. * **Brent crude** prices have climbed to **$71.42** a barrel due to supply disruption fears. Sector Outlook The banking sector is bracing for a "sour" credit cycle. High asset prices are no longer viewed as a sign of health but as an increased risk factor. Market participants are being urged to maintain strict underwriting as the probability of borrower defaults rises in sectors previously thought to be stable, such as software and utilities. Vigilance is required as the market navigates this transition from "AI assistance" to "transactional authority," where the speed of technological change may outpace the financial system's ability to absorb the resulting economic shocks.

Oil Prices Stabilize Near Seven-Month Highs Preceding U.S.-Iran Negotiations

Market Brief: Energy Outlook 2026 Crude oil markets are navigating significant volatility as geopolitical risks and shifting inventory data collide. Prices are currently hovering near six-month highs, with **Brent crude** trading around **$71.40** and **West Texas Intermediate (WTI)** positioned at **$66.05**. The primary driver is the intensifying standoff between the U.S. and Iran. Tensions have escalated following a **10-to-15 day ultimatum** from President Trump for Tehran to secure a new nuclear agreement. While military posturing in the Middle East has increased, the market is bracing for a third round of negotiations scheduled for this Thursday, February 26, in Geneva. Supply Risks and Trade Policy Iran remains a pivotal global producer, pumping approximately **3.3 million barrels per day**. Analysts warn that any disruption to the Strait of Hormuz—a chokepoint for **20% of global oil and LNG trade**—could push prices toward **$90** or even triple digits. Adding to the complexity, the White House has signaled plans to increase temporary tariffs from **10% to 15%** on certain trading partners. This trade policy shift creates a ceiling for price rallies, as higher tariffs could dampen global economic growth and long-term oil demand. Inventory and Production Trends U.S. domestic data is currently sending mixed signals. Recent reports from the American Petroleum Institute indicated a substantial build of **11.4 million barrels** in crude stockpiles. This follows a previous week where commercial inventories fell by **9 million barrels**, leaving total stocks at **419.8 million barrels**, which is **5% below** the five-year average. Refineries are operating at **91% capacity**, yet the market remains cautious. While OPEC+ has opted to maintain production pauses through the first quarter of 2026, global supply is still projected to grow by **1.6 million barrels per day** this year. Demand Forecasts The International Energy Agency (IEA) recently revised its 2026 demand growth outlook downward to **849,000 barrels per day**. Total global consumption is expected to reach **104.87 million barrels per day**, with growth almost entirely driven by non-OECD economies, specifically China and India. Investors remain in a holding pattern, balancing a "war premium" of approximately **$4 to $10** per barrel against a projected global surplus. Near-term price action will likely be dictated by the outcome of the Geneva talks and the subsequent EIA inventory data.

IT Stocks Lead Market Decline Amid AI Impact Concerns

The Indian IT sector is currently navigating a period of intense volatility following a strategic shift in the global AI landscape. A recent technical update from the AI firm Anthropic has acted as a catalyst for a broad sell-off, raising fundamental questions about the future of traditional software services and legacy system maintenance. The market reaction was swift and severe. The Nifty IT index plunged by 4.7% in a single session, marking one of its sharpest declines in recent months. This downward pressure saw industry heavyweights like Infosys and HCL Technologies slide between 3% and 5%, while the broader sector witnessed a combined market capitalization erosion of approximately 1.2 trillion rupees. At the center of this turbulence is a blog post from Anthropic detailing the capabilities of its "Claude Code" tool. The tool is designed to automate the modernization of COBOL, a decades-old programming language that still powers roughly 95% of global ATM transactions and critical banking infrastructure. Traditionally, maintaining and updating these legacy systems required massive teams of consultants and years of manual labor—a core revenue stream for many Indian IT firms. Anthropic’s claim that AI can now compress modernization timelines from years to just a few quarters has rattled investor confidence. The fear is that the "managed services" model, which relies on high headcount and billable hours, is facing structural deflation. If AI can autonomously handle code analysis and documentation, the high-margin maintenance contracts that have sustained the sector for decades may rapidly shrink. Global precedents have intensified these concerns. IBM recently experienced its steepest daily decline in 25 years, losing over 30 billion dollars in market value following the Anthropic announcement. As IBM’s mainframe business is deeply intertwined with COBOL systems, the market viewed the AI breakthrough as a direct threat to its consulting and infrastructure moats. Sector analysts have noted that the IT industry’s share of India’s corporate profit pool has already slipped to a three-year low of 9%. With the Nifty IT index down nearly 20% over the past year, the sector is currently the weakest link in the broader market. While many firms are attempting to pivot toward AI-led transformation projects, the transition is proving to be complex and capital-intensive. Looking ahead, the industry faces a structural reset. The focus is shifting from labor-based arbitrage to high-value consulting and AI implementation. However, until companies can demonstrate that they can monetize AI at a scale that offsets the loss of traditional maintenance revenue, the sector is likely to remain under significant pressure. Professional outlooks remain cautious, with some brokerages cutting price targets for major players by as much as 33% as the market adjusts to this new economic reality.

Citrini Founder Attributes Market Selloff to Recent AI Forecast

Market volatility has intensified following the release of a viral macro-analysis titled "The 2028 Global Intelligence Crisis." The report, published by Citrini Research founder James van Geelen, has sparked a significant sell-off across global indexes, driven by a dystopian forecast of the near-term economic landscape. The report details a "deflationary cascade" where rapid AI integration leads to mass white-collar layoffs. It predicts a scenario by June 2028 where the U.S. unemployment rate surges to **10.2%**, rendering traditional human labor obsolete in several sectors. This "intelligence displacement spiral" suggests that as payrolls shrink, consumer spending will soften, forcing companies to adopt even more AI to protect margins, creating a loop with no natural brake. Market reaction was immediate and sharp. On Monday, the **S&P 500** erased early gains to close down more than **1%**, while the Dow Jones Industrial Average fell **1.7%**, losing over **821 points**. The tech-heavy **Nasdaq Composite** declined **1.1%**, finishing at **22,627.27**. Investor anxiety was further reflected in the CBOE Volatility Index (**VIX**), which spiked **10.1%** to reach **21.01**. Software and cybersecurity firms have borne the brunt of the downturn. A major software ETF plummeted more than **4%**, while specific leaders like CrowdStrike and Zscaler saw intraday declines exceeding **10%**. Investors are increasingly wary of "Ghost GDP"—high corporate output that no longer translates into household income or tax revenue. The sell-off is compounded by broader fiscal concerns. The tech sector is already reeling from a **$1 trillion** loss in market value since late January, fueled by massive capital expenditure plans. Hyperscalers are projected to spend over **$600 billion** on AI infrastructure this year alone, a figure that has begun to exhaust investor patience. Adding to the instability, new policy shifts have emerged. Reports of a proposed increase in global tariffs to **15%** have driven a **2%** spike in gold prices, as traders seek safe-haven assets. Gold recently peaked above **$5,150** per ounce amid this heightened geopolitical and economic uncertainty. While some analysts view the recent "catastrophizing" as overdone, the consensus points to a harsh valuation reset. The market is pivoting from "efficiency flexing" to a deeper skepticism regarding the long-term durability of AI-driven revenue, especially as the "intelligence premium" for the global middle class begins to evaporate. [The 2028 Global Intelligence Crisis breakdown](https://www.youtube.com/watch?v=h1Eex37Iays) This video provides an expert analysis of the Citrini report and explains how AI spending fears are currently reshaping global tech valuations. http://googleusercontent.com/youtube_content/0

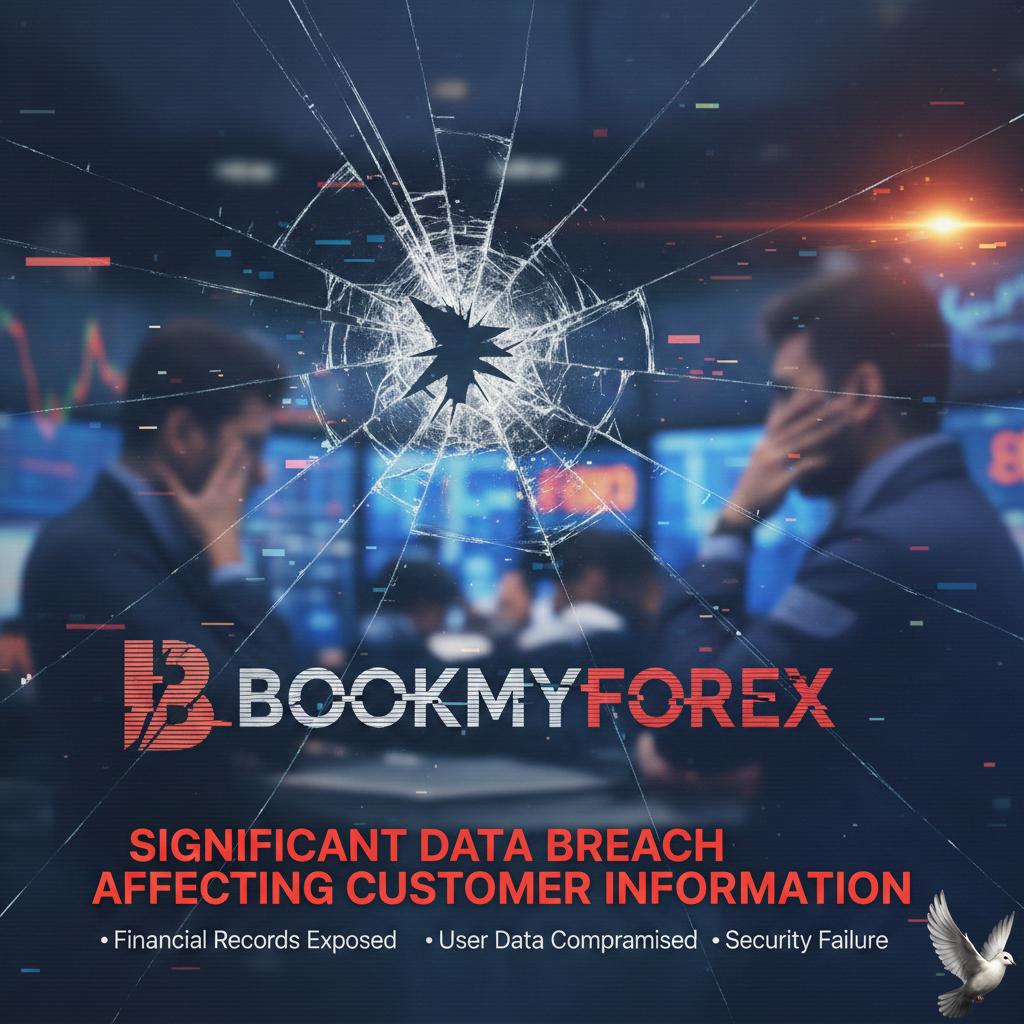

BookMyForex Reports Significant Data Breach Affecting Customer Information

Market Alert: BookMyForex Security Breach A significant data security incident has compromised the **BookMyForex** platform, leading to widespread reports of unauthorized transactions on prepaid forex cards. As of late **February 2026**, thousands of users have reported fraudulent activity, primarily involving international transactions in **USD** and **AED**. Affected customers have noted a surge in debit alerts for transactions they did not authorize. Many of these attempts were successfully processed, while others were declined only after multiple failed security entries. Current reports suggest that the breach has impacted the core card management infrastructure, making immediate mitigation difficult for users. Operational Disruptions The platform's mobile application and customer support channels are currently facing severe outages. Users report being stuck at "Reset App PIN" screens or encountering blank error popups when attempting to access card controls. With the app largely unresponsive, many travelers find themselves unable to lock their cards or modify spending limits while abroad. This has left a significant number of cardholders without access to their primary travel funds, a situation compounded by the high volume of calls overwhelming the company’s support team. Mitigation and Recovery BookMyForex has officially escalated the crisis to its banking partner, **Yes Bank**, to initiate chargeback proceedings. The company is directing users to its web-based card management portal as the primary method for securing accounts. * **Locking Cards:** Users are advised to log in via the website to immediately disable all transaction types. * **Dispute Filing:** Victims are being instructed to email specific dispute desks at both BookMyForex and Yes Bank. * **Insurance Claims:** Most cards issued through the platform include insurance coverage for internet fraud, which may offer a secondary route for fund recovery. Sector Context This incident occurs at a time of heightened digital risk for the Indian fintech sector. Recent industry data indicates that **51%** of senior leaders now cite cybersecurity as the top threat to organizational performance in **2026**. The breach also coincides with recent regulatory shifts. Under the **Union Budget 2026**, Tax Collected at Source (TCS) for foreign remittances was recently adjusted, with education and medical remittances reduced from **5%** to **2%** for amounts exceeding **₹10 lakh**. For those currently affected, the focus remains on securing a formal acknowledgment from the **National Cybercrime Portal** to support pending insurance and chargeback claims. Experts emphasize that until the platform restores full app functionality, manual card locking via the web remains the only reliable safeguard for remaining balances.