Bullish News

Collection

PNGS Reva Diamond Jewellery IPO: Price Band Fixed at ₹367–₹386; Issue to Open February 24

PNGS Reva Diamond Jewellery has officially set the stage for its upcoming public debut, with its Rs 380 crore Initial Public Offering (IPO) scheduled to open for subscription on February 24, 2026. The company has fixed a price band of Rs 367 to Rs 386 per equity share. The issue consists entirely of a fresh issue of approximately 9.8 million shares, with no offer-for-sale component from existing shareholders. The retail investment threshold is set at a minimum lot size of 32 shares, requiring an initial outlay of Rs 12,352 at the upper price band. The bidding process will conclude on February 26, 2026, followed by a tentative listing on the BSE and NSE on March 4, 2026. Proceeds from the offering are earmarked for a significant retail expansion. The company plans to deploy Rs 286.56 crore to establish 15 new stores, further penetrating the western Indian market. Additionally, Rs 35.4 crore is allocated to marketing and promotional activities for its flagship "Reva" brand, with the remaining capital supporting general corporate needs. Financial performance has shown steady growth leading up to the IPO. For the fiscal year ending March 2025, the company reported revenue of Rs 258.18 crore, marking a 30% increase from the Rs 198.85 crore recorded in 2023. Net profit for the same period rose to Rs 59.47 crore, up from Rs 51.75 crore two years prior. As of late 2025, the company maintained 21,866,400 equity shares outstanding on a pre-issue basis. The IPO arrives amid a period of cautious optimism in the broader Indian markets. As of mid-February 2026, the Nifty 50 has been navigating a consolidation phase around the 25,650 to 26,000 levels. While global volatility and high valuations have prompted selective profit-booking, consumption-linked sectors have shown resilience. The Indian gems and jewellery sector continues to benefit from structural shifts. Market valuation for the industry is projected to reach $168.62 billion by 2030, driven by a compound annual growth rate of 8.93%. Recent trade updates, including zero duty on diamond imports and revised tariff frameworks, have bolstered the competitive positioning of domestic players. Investors are closely monitoring the company's regional concentration, as over 95% of its current revenue is generated within Maharashtra. The planned expansion serves as a strategic move to diversify this footprint and capture a larger share of the organized jewellery retail market, which is increasingly favored by Indian consumers for its transparency and certified quality.

Fractal Analytics Projects Growth Through Healthcare and AI Post-IPO Amid Margin Expansion and Robust Cash Flows

FRACTAL ANALYTICS MARKET BRIEF FEBRUARY 16, 2026 Fractal Analytics made its debut on the Indian stock exchanges today, February 16, 2026. The company’s shares listed at **876.00** on the NSE, marking a **3% discount** to its issue price of **900.00**. This listing values the enterprise AI firm at approximately **14,800 crore**. The **2,834 crore** IPO was subscribed **2.66 times** overall. While retail interest was steady, broader market caution regarding high valuations for AI services led to a muted opening. Despite the initial price dip, management remains focused on long-term structural growth driven by the "Fractal Alpha" and "Cogentiq" platforms. Financial Performance and Growth Fractal has demonstrated a significant financial turnaround. After a loss of **54.7 crore** in FY24, the company reported a net profit of **220.6 crore** in FY25. This recovery was fueled by a **26%** year-on-year revenue increase, reaching **2,765 crore**. Operational efficiency is improving as the business shifts from project-based consulting to a platform-led model. * Adjusted EBITDA margins stood near **20%** in recent quarters. * Cash flow from operations reached **500 crore** last year. * Revenue from focus industries grew at a CAGR of **16.8%** between 2023 and 2025. Strategic Sector Expansion Healthcare and Consumer Packaged Goods (CPG) are the primary engines for future earnings. Healthcare is becoming a larger share of the US economy, where Fractal generates over **64%** of its revenue. AI adoption in medical diagnostics and life sciences is expected to grow at a CAGR of **43.9%** through 2034. The company is aggressively scaling its license-based income. By increasing software-led revenue through its "Agentic AI" platform, Fractal aims to decouple growth from headcount, leading to higher gross margins. Market Outlook and AI Spending Global technology spending is showing resilience. Large corporations currently allocate roughly **4.5%** of their revenue to tech, a figure projected to rise toward **6%**. AI’s share of that budget has expanded from **10%** to nearly **33%**. While the emergence of Artificial General Intelligence poses long-term questions for traditional models, Fractal is positioning itself as a "Decision Intelligence" leader. The company currently holds **28 registered patents** and has **38** more in the pipeline, reinforcing its competitive moat in a crowded analytics field. The capital raised from the **1,023 crore** fresh issue is earmarked for R&D, debt repayment, and expanding the "Fractal Alpha" incubator, which houses independent AI startups. Management expects these investments to sustain profitability momentum post-listing.

10 Midcap Stocks with Four Consecutive Quarters of Revenue Growth

NSE Midcap Growth Brief: February 2026 The Indian midcap segment is showing a distinct divide between operational momentum and market valuation. While the Nifty Midcap 100 index recently faced a **0.92%** monthly dip, a select group of ten non-financial firms has defied the trend. These companies achieved consistent sales growth for four consecutive quarters ending December 2025, signaling resilient demand in the energy, consumer tech, and infrastructure sectors. Solar Sector Surge Waaree Energies has emerged as a standout performer in the renewable energy space. The company reported a record-breaking quarterly revenue of **7,565 crore** for the December 2025 period. This represents a massive **118.8%** year-on-year increase. The firm’s operational scale is now hitting critical mass. It achieved a module sales volume of **3.6 GW** in a single quarter, supported by an order book valued at approximately **60,000 crore**. Profit after tax also surged by **118%** to reach **1,107 crore**, reflecting strong pricing power amid India’s green energy transition. Consumer Tech and Logistics In the digital economy, Swiggy demonstrated high-volume growth despite bottom-line pressure. Quarterly revenue jumped **54%** to reach **6,148 crore**. The primary engine for this growth was the quick-commerce arm, Instamart, which saw its revenue climb **74%** to **1,052 crore**. While the company’s net loss widened to **1,065 crore** due to aggressive dark store expansion, its supply chain and distribution segment became a major contributor, generating **2,981 crore**. The focus for investors has shifted toward unit economics as the platform matures. Infrastructure and Healthcare GMR Airports maintained steady topline growth, with sales rising **50.5%** to **3,994 crore** in the December quarter. The Delhi airport alone handled a record **20.8 million** passengers during this period. However, one-time expenses related to labor laws and contract terminations led to a **14%** decline in consolidated net profit, which stood at **174 crore**. In the healthcare space, Narayana Hrudayalaya showcased robust performance. Revenue for the December quarter reached **2,151 crore**, up from **1,335 crore** in the previous year. This growth highlights the sustained demand for specialized medical services and improved operational efficiency across its hospital network. Sectoral Trends at a Glance The broader market is currently rotating away from IT, which has seen a **50,000 crore** decline in mutual fund holdings this month. Investors are increasingly favoring "old economy" sectors and high-growth midcaps with visible order books. * **Nifty Midcap 100 PE Ratio:** Currently at **32.5** * **Top Growth Driver:** Renewable Energy and Quick Commerce * **Key Resistance Level:** Nifty 50 at **26,000** * **Midcap Index Level:** Trading near **59,500** The trend suggests that while the broader midcap index remains volatile, individual companies with strong execution in the manufacturing and service sectors are successfully decoupling from the general market weakness.

Indian Rupee Closes Flat Amid Offsetting Capital Flows

The Indian rupee maintained a narrow range at the start of the week, ending Monday with minimal movement as domestic demand for the dollar was effectively countered by steady foreign inflows. The local unit slipped by a marginal **1 paisa** to settle at **90.67** against the US dollar. This follows a period of consolidation where the currency has hovered near the **90.66** level, reflecting a cautious but stable market environment. Pressure on the rupee has recently stem from significant outflows by Foreign Institutional Investors. In a single recent session, overseas investors offloaded shares worth **Rs 7,395.41 crore**, primarily driven by a sell-off in the information technology sector. External factors remain a primary focus for traders. While the US dollar index has shown periodic strength, global oil prices have seen a slight uptick, adding to the import bill for the world's third-largest oil consumer. The Reserve Bank of India continues to play a stabilizing role. The country's foreign exchange reserves currently stand at **$717.06 billion**, down from a historic peak of **$723.77 billion** earlier this month. Despite this recent dip, the buffer remains robust, providing cover for over **11 months** of imports. Monetary policy signals from the central bank have provided further clarity. The Reserve Bank of India recently maintained the repo rate at **5.25%**, signaling a neutral stance. This decision comes as retail inflation was recorded at **2.75%** for January, comfortably within the bank's target range. Market participants are now looking toward upcoming trade balance figures and global cues for further direction. With the US markets closed for a public holiday, trading volumes remained thin, contributing to the currency's rangebound performance today. The domestic economy's growth outlook remains a supportive factor for the currency. Projections for real GDP growth in the current fiscal year have been adjusted to **7.4%**, bolstered by a new trade agreement with the United States that targets a total trade volume of **$500 billion**.

Puravankara Q3 net profit reaches Rs 58 crore as revenue triples to Rs 1,104 crore

Puravankara Limited has staged a significant financial recovery, reporting a consolidated net profit of 58.34 crore for the third quarter of the 2025-26 fiscal. This performance marks a decisive turnaround from a net loss of 92.64 crore in the same period last year, signaling an end to a string of loss-making quarters. Total consolidated income for the quarter skyrocketed to 1,104.06 crore, representing a 230% increase compared to the previous year. This surge was primarily fueled by robust project execution and a sharp rise in unit handovers, which jumped from 249 units last year to 1,116 units this quarter. The company’s operational efficiency improved notably, with EBITDA margins expanding to 23%, up from 10% in the prior year. Customer collections also reached a record 1,140 crore for the quarter, reflecting a 22% growth that has significantly strengthened the balance sheet and supported cash flow. In the sales arena, the developer achieved a sales value of 1,414 crore during the October-December period. Average price realization grew by 12% to approximately 9,500 per square foot, indicating strong demand for its mid-to-premium offerings across key micro-markets. Puravankara continues to aggressively expand its pipeline, adding over 12.7 million square feet of potential developable area during the first nine months of the fiscal year. This new inventory carries an estimated gross development value of approximately 13,900 crore, concentrated in high-demand zones within Bengaluru and Mumbai. Despite the positive earnings report, the stock experienced a sharp intraday correction on February 16, 2026, dropping over 7% to a low of 239. Market analysts suggest this volatility stems from broader sector-specific pressures and profit-taking after the stock had rallied nearly 8% in the preceding week. The broader Indian residential market is entering a phase of steady consolidation. While average home prices in major cities like Bengaluru and Delhi-NCR are projected to grow by 7% to 8% in 2026, buyers are becoming increasingly selective, prioritizing project completion status and execution quality over speculative gains. Puravankara’s management has emphasized a future focus on calibrated launches and consistent cash flow generation. With a total land bank of 38 million square feet and net debt reduced by 244 crore this quarter, the firm is positioning itself to navigate a more mature and disciplined real estate cycle.

Delhi HC Dismisses Challenge to SEBI's Approval for NSE IPO

Market Brief: NSE IPO Gains Legal Clearance The Delhi High Court has dismissed a writ petition challenging the no-objection certificate issued by SEBI for the National Stock Exchange’s proposed listing. This ruling on **February 16, 2026**, removes a critical legal barrier for the exchange, which has sought to go public since **2016**. The court observed that the petition, filed by a former judicial officer, appeared designed to "interdict" the IPO process. The legal challenge centered on derivative adjustment frameworks, but the dismissal effectively validates the **January 30, 2026** clearance provided by the market regulator. Market Impact and Valuation The National Stock Exchange continues to dominate the Indian financial landscape with a nearly **94%** share in the equity cash market and a **99%** share in equity futures. Current data from the unlisted market shows shares trading near **₹2,130** per unit. This translates to an estimated market capitalization of approximately **₹5.27 lakh crore** (**$63 billion**). The exchange reported a net profit of **₹12,188 crore** for the fiscal year **2025**, representing a **47%** year-on-year increase. Its operational revenue grew by **17%** to reach **₹19,177 crore** in the same period. Strategic Timeline With the legal hurdle cleared, the exchange is expected to accelerate its internal preparations. This includes the formal appointment of merchant bankers and legal advisers to draft the Red Herring Prospectus. Industry analysts anticipate the listing process will take between **8 to 9 months** to conclude. The IPO is structured primarily as an Offer for Sale, allowing existing institutional investors to liquidate portions of their holdings. Benchmarks and Sector Performance The news comes as Indian benchmark indices showed resilience. On **February 16, 2026**, the Nifty 50 closed up by **211 points** at **25,650**, while the Sensex rallied **650 points** to finish at **83,276**. The broader market stability, combined with the clearing of long-standing regulatory "co-location" shadows, positions the exchange for a potential debut in late **2026**. The removal of this litigation risk is viewed as a definitive signal that the exchange has met the governance standards required for public listing after a decade of delays.

Sensex and Nifty Advance to Break Three-Day Losing Streak

The Indian equity markets staged a decisive recovery on February 16, 2026, snapping a multi-day losing streak through a late-session surge. The Nifty 50 climbed 211.65 points, or 0.83%, to settle at 25,682.75. Simultaneously, the 30-share BSE Sensex rebounded by 650.39 points, or 0.79%, finishing the day at 83,277.15. This rally was primarily anchored by the banking and financial sectors, which witnessed strong buying interest. Leading the gains, Power Grid Corporation surged 4%, while HDFC Bank rose approximately 2%. Other significant contributors included Coal India, Axis Bank, and NTPC. In contrast, the IT sector faced its fourth consecutive session of decline due to ongoing concerns over sector-wide shifts, with Tech Mahindra and Infosys among the primary laggards. The broader market reflected a more cautious sentiment. While the Nifty MidCap index gained 0.48%, the SmallCap index ended with a marginal rise of 0.11%. Market breadth remained positive on the Nifty, with 35 stocks advancing against 15 declines. However, regulatory updates weighed heavily on specific players; shares of BSE and Angel One saw sharp declines of up to 10% following a revision in capital market exposure norms. Economic indicators continue to support a "Strong Recovery" phase for the domestic economy. Real GDP growth for the second quarter of the 2025-26 fiscal year was recorded at 8.23%. Manufacturing remains a critical pillar, with Gross Value Added in the sector growing by 9.13% in the same period. This industrial momentum is further bolstered by a low average inflation rate, which has hovered around 1.8% throughout the fiscal year. Global cues remained mixed as Asian markets experienced thin trading volumes during the Lunar New Year holidays. Locally, investors are closely monitoring the Wholesale Price Index (WPI) data and the trade deficit, which reached a record 25 billion dollars in December. Despite these pressures, the domestic investment landscape remains resilient, with Domestic Institutional Investors (DIIs) continuing to provide a cushion against Foreign Institutional Investor (FII) outflows. The commodity market saw profit-booking as gold and silver futures fell by nearly 3% following recent rallies. In the debt market, the 10-year benchmark bond yield remained steady at 6.67%, influenced by movements in U.S. Treasury yields. The current market outlook for 2026 remains constructive, supported by improving fundamentals and valuations that align with long-term averages. While the IT and auto sectors face near-term headwinds, capital goods, pharma, and telecom are emerging as preferred sectors for institutional positioning due to high earnings visibility.

Axis Securities Projects Up to 20% Upside for Shriram Finance, Blue Star, and Two Other Stocks

Market Brief: Momentum Picks for February 2026 Indian equity markets are showing constructive sentiment as the NIFTY 50 aims for the **26,000** psychological milestone. Institutional interest has pivoted toward selective buying, with Foreign Institutional Investors (FIIs) recently turning net buyers. Within this landscape, four specific stocks are currently positioned for potential gains of up to **20%** over the next 3–4 weeks. Shriram Finance: Fundamental Strength Shriram Finance remains a top fundamental conviction pick. As of February 16, 2026, the stock is trading near **1,085**, marking a steady climb from its weekly open of **1,005**. The stock faces immediate technical resistance at **1,100.80**. A decisive close above this level is expected to trigger a sharp breakout toward analysts' average consensus targets of **1,142**. Support is firmly established at **1,017**, providing a cushion for staggered accumulation. Kirloskar Oil Engines: Momentum Leader Kirloskar Oil Engines has emerged as a high-momentum outlier, surging over **17.5%** in the past week alone. This rally was fueled by a robust **27%** surge in quarterly profits and the announcement of a dividend. The stock reached a fresh 52-week high of **1,435** recently and currently trades around **1,390**. With a bullish MACD crossover and a low PEG ratio of **0.87**, the technical setup remains strong. Analysts from major brokerage houses have revised price targets upward, with some aiming as high as **1,540** to **1,665**. Blue Star: Technical Upside Blue Star is displaying resilient price action in the consumer durables segment. The stock is currently priced near **1,972**, maintaining an upward momentum score despite broader market volatility. [Image of a split-system air conditioner unit] Technically, the stock is trading above all its key Simple Moving Averages (SMAs). While short-term oscillators like the RSI are approaching overbought territory at **60.7**, the underlying trend remains bullish. Immediate resistance levels are pegged at **2,006**, with a secondary barrier at **2,269**. Astral Ltd: Breakout Potential Astral has delivered a robust **8.3%** weekly gain, hitting a new 52-week high of **1,624.90** on February 16, 2026. A significant technical milestone was reached with the formation of a **Golden Cross**, where the 50-day moving average surpassed the 200-day average. The stock has outperformed the Sensex by over **13%** on a one-year basis. Current technical indicators, including a Mojo Score of **65**, suggest sustained buying interest. Analysts have set consensus targets near **1,695**, supported by a significant surge in open interest in the derivatives segment. **Market Summary Data** * **Nifty 50 Index:** **25,693** * **Shriram Finance LTP:** **1,085.00** * **Kirloskar Oil LTP:** **1,390.00** * **Blue Star LTP:** **1,972.30** * **Astral Ltd LTP:** **1,624.90**

Arkade Developers Projects Rs 700 Crore Revenue from Mumbai Housing Redevelopment

Arkade Developers Ltd has officially entered a development agreement for a major cluster redevelopment project in Malad West, Mumbai. The venture focuses on the Shree Rani Sati Nagar Co-operative Housing Society and covers a total plot area of approximately 6,553 square metres. The company estimates the Gross Development Value of this project at 700 crore. This move aligns with Arkade’s established footprint in the Mumbai region, where it has already completed 31 projects across 5.5 million square feet. Currently, the firm maintains an active pipeline with over 2 million square feet under construction. Market conditions in Mumbai show a distinct trend toward premiumization. While overall sales volumes in the region saw a marginal decline of 0.47% in the last year, the value of transactions has remained high. Property prices in Mumbai rose by 10.5% in late 2025, driven by a demand-supply mismatch and major infrastructure upgrades like the Coastal Road and Metro expansion. The broader Indian residential market is shifting rapidly. Sales for homes priced above 1 crore grew by 9% in 2025, now making up 28% of the total market. In contrast, the affordable housing segment—properties below 50 lakh—saw its market share drop from 42% to 37% as buyers prioritize lifestyle-led upgrades and larger layouts. Arkade's latest financial results for the third quarter of the 2025-2026 fiscal year reflect these sector-wide shifts. The company reported a consolidated net profit of 40.30 crore, while its revenue from operations stood at 196.73 crore. Despite a year-on-year slide in quarterly profit, the firm maintains a healthy balance sheet with a low net debt-to-equity ratio of 0.04x. The company's total project pipeline is estimated at a valuation of 11,900 crore. This portfolio covers approximately 4 million square feet of saleable carpet area, positioning the developer to capitalize on the sustained demand for high-end residential spaces in Mumbai’s western suburbs. Investors continue to monitor the impact of stable interest rates and government urban redevelopment policies. With average property values in Mumbai now hovering around 8,856 per square foot, the redevelopment of aging housing societies remains a critical revenue driver for established city-based developers.

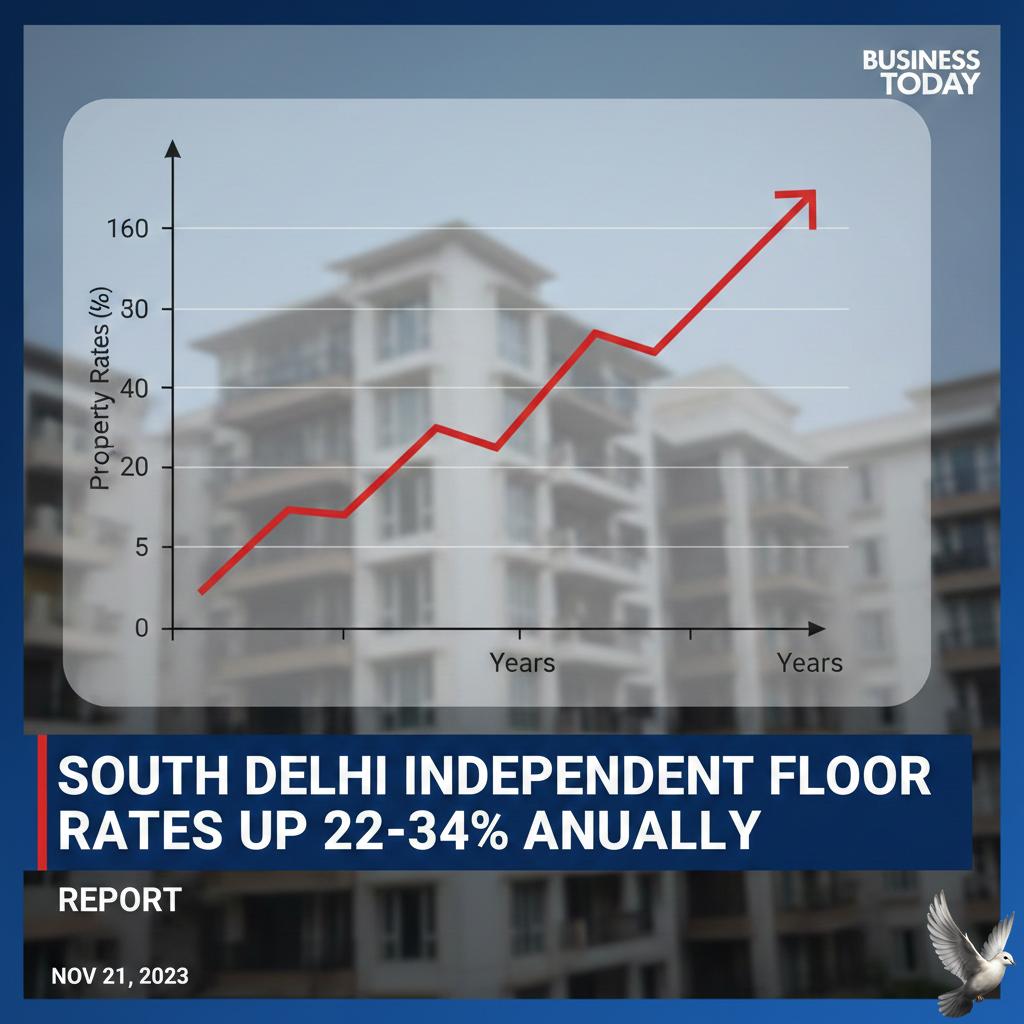

South Delhi Independent Floor Rates Increased 22-34% Annually: Report

South Delhi’s luxury real estate sector continues to outpace the broader national market, fueled by an intense demand-supply mismatch and a wave of High-Net-Worth Individual (HNI) investments. In 2025, independent luxury floors have remained the primary asset of choice for affluent families seeking low-density living and modern amenities. Market data for 2025 reveals that average annual prices for these floors have surged by 22% to 34%. This growth is concentrated in premium micro-markets where land availability is near zero and redevelopment of older bungalows is the only source of new inventory. **Category-A Micro-Markets** Colonies such as Chanakyapuri, Vasant Vihar, Golf Links, and Shanti Niketan are leading the rally with price increases between 25% and 34%. For a standard 2,500 sq. ft. floor in these elite zones, entry prices have climbed from approximately 14.5 crore last year to as high as 25 crore in 2025. Larger units are seeing even steeper valuations; a 6,000 sq. ft. independent floor now commands between 25 crore and 55 crore. **Category-B Micro-Markets** Well-established neighborhoods like Defence Colony, Greater Kailash, and Gulmohar Park have also seen steady appreciation, with property values rising 22% to 26%. A typical 2,500 sq. ft. floor in a Category-B area is now priced between 9 crore and 12.5 crore. Mid-sized luxury floors of 3,200 sq. ft. have seen their valuations move from a baseline of 13.5 crore to nearly 16.5 crore or higher depending on the specific block and road width. **Key Market Drivers** The current momentum is sustained by three critical factors: - Local landowners are increasingly opting for redevelopment to unlock capital and accommodate evolving family needs. - Better utilization of the permissible Floor Space Index (FSI) has allowed for larger, more sophisticated home designs. - A steady migration of wealth from other parts of the National Capital Region into South Delhi, driven by its superior social infrastructure and iconic lifestyle value. While the overall Delhi-NCR housing market showed a more modest growth of roughly 6% in 2025, the luxury independent floor segment remains insulated from broader cooling trends. Limited land supply and a growing preference for floor-wise ownership ensure that pricing remains robust heading into the next fiscal cycle.

German 10-Year Yield Declines Ahead of Key Economic Data

Eurozone sovereign bond yields have hit their lowest levels since early December 2025, continuing a sustained downward trend as market participants pivot toward defensive assets. This shift is driven by cooling inflation and a softening economic outlook across the currency bloc, which now officially includes Bulgaria as of January 2026. The benchmark German 10-year Bund yield has eased to approximately 2.75%, marking its lowest point in over two months. This decline reflects a broader six-day winning streak for European debt, the longest such rally since late 2024. Investors are increasingly seeking the safety of government paper as risk sentiment weakens in the face of stagnant industrial activity. Economic indicators are reinforcing the case for lower yields. Eurozone inflation dropped to 1.7% in January, falling below the European Central Bank’s 2% target. While the ECB held interest rates steady at 2.00% during its February 5 meeting, the undershoot in consumer prices has fueled speculation that the central bank may need to revise its 2026 inflation forecasts downward. The manufacturing sector continues to face headwinds. The latest HCOB Eurozone Manufacturing PMI remains in contraction at 49.5, with German factory orders showing volatility and construction activity slumping to 44.7. While services remain in expansion, the overall recovery appears uneven, keeping the ECB in a "wait-and-see" mode until more definitive data arrives in March. A notable trend in 2026 is the narrowing yield spread between core and peripheral nations. The gap between Italian 10-year yields and German Bunds has tightened to its lowest in nearly two decades, signaling growing investor confidence in the fiscal dynamics of Southern Europe compared to the growth struggles in Germany and France. Traders are now focused on upcoming flash PMI figures and wage growth trackers. These metrics will be critical in determining whether the ECB maintains its current pause or accelerates the timeline for further easing. Currently, money markets are pricing in a cautious path, with only a 30% probability of an additional rate cut before year-end, though a strong euro and falling energy prices could shift these odds. The supply of European government bonds is expected to rise sharply this year, with gross issuance projected to reach 1.4 trillion euros. As the ECB continues its quantitative tightening by reducing its balance sheet, the private market will need to absorb a record volume of net issuance, which may provide a floor for yields despite the disinflationary environment.

European Equities Rise Led by Financial Sector

The STOXX 600 index edged higher on Monday, climbing 0.3% to reach 619.74 points. This movement reflects a steady recovery as the pan-European index maintains its position near record highs. Market sentiment remains resilient, supported by a third consecutive week of gains following a stronger-than-expected earnings season. Financial stocks spearheaded the morning’s performance. Bank and insurance sectors led the rally, with lenders jumping 1.6% and insurance firms gaining 1.0%. Spain’s benchmark, which is heavily weighted toward banks, outperformed most regional peers. This rebound comes after a period of volatility where concerns regarding artificial intelligence disruption and U.S. trade tariffs briefly weighed on traditional business models. Corporate health across Europe appears more robust than previously forecast. Data indicates that approximately 60% of European companies have beaten earnings expectations this quarter, significantly higher than the long-term average of 54%. While overall earnings are still projected to dip by roughly 1.1%, this is a marked improvement from the 4% contraction feared earlier this month. Investors are now shifting focus toward upcoming economic indicators and corporate reports. Fresh data is expected to show Eurozone industrial production grew by 1.3% year-on-year in December. Although this is a slowdown from the 2.5% growth seen in the prior month, it signals continued stability in the manufacturing sector. The remainder of the week will see several high-profile earnings releases. Key reports are due from major players including Airbus, Orange, and BE Semiconductor. These figures will provide further clarity on how European exporters are navigating current trade conditions and the impact of a stronger Euro, which recently touched a four-year high above $1.20. Trading volumes remained lower than usual on Monday due to market holidays in the United States. Despite the thin liquidity, European indices showed broad-based strength. Germany’s DAX rose 0.3%, while the UK’s FTSE 100 and France’s CAC 40 both saw modest gains of 0.2%. The collective focus remains on whether these corporate results can justify the current forward earnings multiple of 15.3, the highest valuation for the index since early 2022.

Indian REITs Distribute ₹2,450 Crore in Q3FY26

India’s Real Estate Investment Trust (REIT) sector has reached a significant milestone in Q3 FY26, demonstrating its resilience and growing appeal as a mainstream investment vehicle. The five publicly listed REITs—Embassy Office Parks, Mindspace Business Parks, Brookfield India, Nexus Select Trust, and the recently listed Knowledge Realty Trust—distributed over 2,450 crore to more than 3.8 lakh unitholders this quarter. The cumulative payouts since the inception of the first REIT in 2019 have now crossed 29,100 crore. This steady flow of capital back to investors highlights the sector's ability to generate consistent income from prime Grade A commercial and retail assets. The total Gross Assets Under Management (AUM) for the sector has climbed to more than 2,50,000 crore as of February 2026. This growth is supported by a massive portfolio of 185 million square feet. Individual performance highlights include Mindspace REIT reporting a 28.7% year-on-year growth in Net Operating Income (NOI) to 671.4 crore, while Brookfield India REIT saw a 464% surge in consolidated net profit to 180.3 crore. Leasing momentum remains high across the board. Embassy REIT recorded 1.1 million square feet of leasing in Q3 alone, while Mindspace achieved 94.5% portfolio occupancy. These figures reflect the strong demand from Global Capability Centres (GCCs) and technology firms for high-quality, managed office spaces. A major recent catalyst for the sector is the Reserve Bank of India’s decision to allow banks to lend directly to REITs. This move is expected to significantly lower borrowing costs and provide these trusts with cheaper capital for refinancing and future acquisitions. Additionally, the government’s plan to launch dedicated REITs for Central Public Sector Enterprise (CPSE) asset recycling is poised to further deepen the market. Market participation is also evolving with the introduction of Small and Medium REITs (SM REITs), allowing for the listing of portfolios valued between 50 crore and 500 crore. This is expected to unlock value in smaller, stabilized assets across Tier-2 and Tier-3 cities. Current market data shows that the REIT market capitalization has crossed 1.6 lakh crore. While the sector currently represents about 19% of India’s listed real estate value, projections suggest the market could grow from 10.4 trillion in 2025 to nearly 19.7 trillion by 2030, driven by urbanization and institutional demand. [Market update on Indian REITs](https://www.youtube.com/watch?v=dQp_G9AGYfI) This video provides additional context on the recent volatility and performance trends within the Indian realty sector during the Q3 FY26 earnings season. http://googleusercontent.com/youtube_content/0

Nifty Eyes 25,350 Support Amid IT Selloff as HDFC Bank and NTPC Show Buy Signals

Indian Market Brief | February 16, 2026 Indian equity benchmarks are navigating a period of heightened volatility as the **Nifty 50** struggles to maintain its footing above key psychological levels. After a sharp 1.30% decline on February 13, the index is currently testing immediate support in the **25,450–25,400** range. The broader market sentiment remains cautious, with the **India VIX** hovering near **13.44**, reflecting moderate but persistent anxiety among traders. Technical indicators show the Nifty trading below its short-term exponential moving averages, signaling a temporary pause in the long-term uptrend. Sector Dynamics The technology sector is under significant duress. The **Nifty IT** index has faced a multi-session sell-off, dropping nearly 8.2% in a single week. This decline is largely attributed to investor concerns over generative AI disruptions and a massive **₹50,000 crore** reduction in mutual fund holdings across top-tier IT stocks. In contrast, the banking and public sectors continue to act as market anchors. The **Nifty PSU Bank** index has outperformed the broader market, delivering returns of approximately 7.8% so far this year. Resilience in this space is supported by strong quarterly earnings and expectations of steady credit growth. Key Stock Highlights **HDFC Bank** remains a focal point for analysts as it shows signs of recovery, recently trading around **₹927**. Market participants are closely watching the **1,005** call option strike for the February expiry as a gauge for near-term bullish sentiment. **NTPC** continues its upward trajectory with a year-to-date return of **10.7%**. The stock recently touched a spot price of **₹369**, benefiting from increased power demand and a strategic focus on the renewable energy transition. Institutional Activity Flows remain divergent. Foreign Institutional Investors (FIIs) have been net sellers in February, offloading equities worth **₹1,374 crore** as of mid-month. This pressure is being counterbalanced by Domestic Institutional Investors (DIIs), who have infused over **₹9,775 crore** this month, driven by robust SIP inflows. Critical Levels For a sustained recovery, the Nifty must decisively reclaim the **25,700–25,800** resistance zone. Failure to hold the **25,400** support could accelerate a correction toward the 200-day EMA near **25,250**, which serves as the primary structural floor.

Gold Market Outlook: Expert Analysis and Five Technical Indicators Suggest Further Downside Risk

Market Brief: Gold Price Consolidation Gold prices on the **Multi Commodity Exchange (MCX)** witnessed a sharp correction, dropping by nearly **Rs 1,800** intraday during recent sessions. This retreat follows a historic rally that saw the metal peak near **Rs 1,80,779** per 10 grams in late January. As of February 16, 2026, the market has entered a phase of quiet consolidation, with prices for **24K gold** hovering around **Rs 1,57,890** per 10 grams. Global and Domestic Indicators The primary driver of the current pullback is a firmer **US Dollar Index**, which has regained strength following hawkish signals from the Federal Reserve. A stronger dollar makes bullion more expensive for international buyers, triggering widespread profit-booking. In the international spot market, gold has retreated from record highs to trade near **$5,020** per ounce. Domestic sentiment remains cautious as technical indicators signal limited immediate upside. While the metal has managed to hold above the psychological floor of **Rs 1,55,000**, the lack of fresh catalysts is keeping the market in a tight range. Key Levels and Strategy Analysts are currently recommending a **sell-on-rise** strategy as the metal faces significant resistance near the **Rs 1,59,400** mark. * **Immediate Support:** Rs 154,400 – Rs 153,150 * **Key Resistance:** Rs 156,800 – Rs 158,200 * **Critical Demand Zone:** Rs 151,900 If gold fails to sustain its current base, a decisive breakdown below **Rs 1,51,900** could open the doors for a deeper correction toward the **Rs 1,45,000** level. Market Outlook The "de-dollarization" narrative that fueled the January surge is facing new headwinds. Reports suggesting a potential shift in **Russian trade policy** toward US Dollar settlements have dampened the aggressive safe-haven bid. Furthermore, the **US January CPI** data, which showed inflation slowing to **2.4%**, has reduced the urgency for immediate interest rate cuts, further supporting the dollar at the expense of non-yielding assets like gold. Despite the current volatility, long-term support remains from central bank diversification and geopolitical tensions in the Middle East. However, for the short term, the market is expected to remain range-bound with a downward bias. Investors are closely monitoring upcoming **US GDP** and **PCE inflation** data for the next directional trigger.

Sebi Proposes ETF Price Band Adjustments and Pre-Open Session Implementation

Market dynamics for Exchange Traded Funds (ETFs) in India are set for a regulatory overhaul as Sebi moves to tighten price discovery and curb volatility. Following a surge in the ETF market—which reached approximately **8.5 trillion INR** in assets by mid-2025—the regulator has issued a consultation paper to address widening gaps between market prices and underlying asset values. Current rules rely on a **T-2 day closing Net Asset Value (NAV)** to set the base price for the trading day. This creates a significant lag, especially during periods of high volatility. To resolve this, Sebi proposes shifting to **T-1 day data**, utilizing either the closing price from the previous session, the average indicative NAV (iNAV) of the last 30 minutes, or the previous day’s closing NAV. The move aims to eliminate manual errors associated with adjusting for corporate actions like dividends and bonuses, which are currently handled manually on outdated data. For investors, the most visible change will be the introduction of dynamic price bands. While most equity and debt ETFs currently operate within a fixed **20%** band, the new framework suggests an initial **10%** limit. This band can be "flexed" up to **20%** following a **15-minute cooling-off period**, with a maximum of two such expansions per day. Commodity ETFs, specifically gold and silver, face even tighter initial controls. Sebi proposes an initial price band of **6%**, which can be expanded in increments of **3%** up to a **20%** limit. This proposal follows extreme volatility in late January 2026, where domestic gold and silver prices saw sharp swings that traditional bands struggled to contain. On February 16, 2026, silver ETFs recorded significant drops of up to **7%** as investors booked profits. To further refine discovery for these global assets, the regulator is weighing a separate **pre-open session** for commodity ETFs. This would allow the market to establish an equilibrium price before the standard trading session begins, aligning domestic prices with international movements that occur outside Indian market hours. Public feedback on these proposals is open until **March 6, 2026**. If implemented, these shifts will bring ETF trading closer to the real-time efficiency of individual stocks, providing a more transparent environment for the **5.2 million** and growing retail ETF portfolios in the country.

Over 11,500 Traders Attend International Outreach Conference 7.0 in Surat

The Indian derivatives landscape reached a significant milestone this February as the Indian Options Conclave (IOC 7.0) in Surat attracted over 11,500 participants from more than 450 cities. The event, themed "Evolve," underscored a structural shift in the market toward disciplined risk management and technology-driven execution. This surge in educational interest coincides with a period of heightened volatility and regulatory transition. As of February 16, 2026, the benchmark Nifty 50 is navigating a sensitive technical zone, trading near 25,471 with immediate support established at the psychological 25,000 mark. Meanwhile, the Bank Nifty remains in a consolidation phase, fluctuating between 59,500 and 60,800. Market dynamics are currently being shaped by the Union Budget 2026 mandates and recent SEBI reforms. Transaction costs for participants have risen following the hike in Securities Transaction Tax (STT) on options premiums to 0.15% and on futures to 0.05%. These measures, combined with the February 1 implementation of 100% upfront premium requirements for option buyers, aim to curb excessive speculation. The profile of the Indian trader is also transforming. Retail investors now hold a record 18.75% of NSE market capitalization, valued at approximately 84 lakh crore. Notably, inclusivity is rising; women now represent 12.2% of registrations at major trading conclaves, while over 60% of new participants are expressing a direct preference for options over cash equity. Institutional behavior reflects a growing divergence. While Foreign Portfolio Investors (FPIs) recorded net outflows exceeding 1.2 lakh crore over the past year, Domestic Institutional Investors (DIIs) continue to provide a stabilizing counter-force. SIP contributions have reached a new peak, averaging over 31,000 crore monthly, ensuring a steady flow of domestic liquidity despite global headwinds. The focus for the 2026 trading year has moved decisively toward capital preservation. Market experts emphasize that with the elimination of expiry-day calendar spread benefits and the introduction of a 2% Extreme Loss Margin (ELM) on short positions, professional-grade tools and psychological discipline are no longer optional. Traders are increasingly adopting multi-leg, defined-risk strategies such as iron condors and bull call spreads to optimize capital under the new margin regime. This evolution reflects a maturing ecosystem where the depth of market knowledge is beginning to match the scale of participation.

**FII and Retail Ownership Increases in Q3 as Selected Smallcap Stocks Deliver Triple-Digit Returns**

Global Market Brief: February 16, 2026 Global financial markets opened the week with a mix of volatility and cautious optimism as investors weighed cooling inflation data against significant technological shifts. Trading volumes remain thin in parts of Asia due to the Lunar New Year holidays, while Wall Street prepares for a week centered on high-stakes corporate earnings. Equities and Sector Performance The broad market narrative is currently dominated by a repricing of the technology sector. After a week of deep cuts driven by fears of artificial intelligence-led disruption, major indices are showing signs of stabilization but remain sensitive. In the United States, the S&P 500 holds near **6,836.17**, while the Nasdaq Composite reflects the tech-heavy anxiety at **22,546.67**. In India, the Nifty 50 is navigating levels around **25,432**, and the Sensex is tracking near **82,500**. Market strategists note a shift in institutional capital away from software-heavy tech and toward sectors with high earnings visibility, such as financials, automobiles, and pharmaceuticals. Small and mid-cap stocks continue to report better-than-expected earnings despite perceived overvaluation. Commodities and Energy Energy and precious metals are reacting to shifting geopolitical tensions and the latest economic indicators. Brent crude is delicately balanced near **$67.74** per barrel, while West Texas Intermediate (WTI) hovers around **$62.90**. Prices are being contained by reports that OPEC+ members may resume gradual output increases starting in April, which could counterbalance supply risks originating from US-Iran tensions. Gold has experienced a brief correction, trading near **$5,020** per ounce. This follows a profit-taking phase after previous rallies. Silver has shown more pronounced volatility, declining to approximately **$2.41 lakh** per kg on local exchanges as it faces pressure from a stronger US dollar. Economic Indicators and AI Impact Global growth for 2026 is projected to remain steady at **3.3%**. A key driver of this outlook is the massive investment in AI infrastructure, with capital expenditure from major tech platforms forecast to hit **$625 billion** this year. In the US, January inflation moderated to **2.4%**, which has strengthened expectations for potential interest rate cuts later in the year. Similarly, India reported a cooling CPI of **2.75%**, providing a resilient backdrop for domestic growth despite some softening in manufacturing surveys. Investors are now focusing on the upcoming release of central bank minutes and earnings from retail giants like Walmart to gauge the health of global consumer spending.

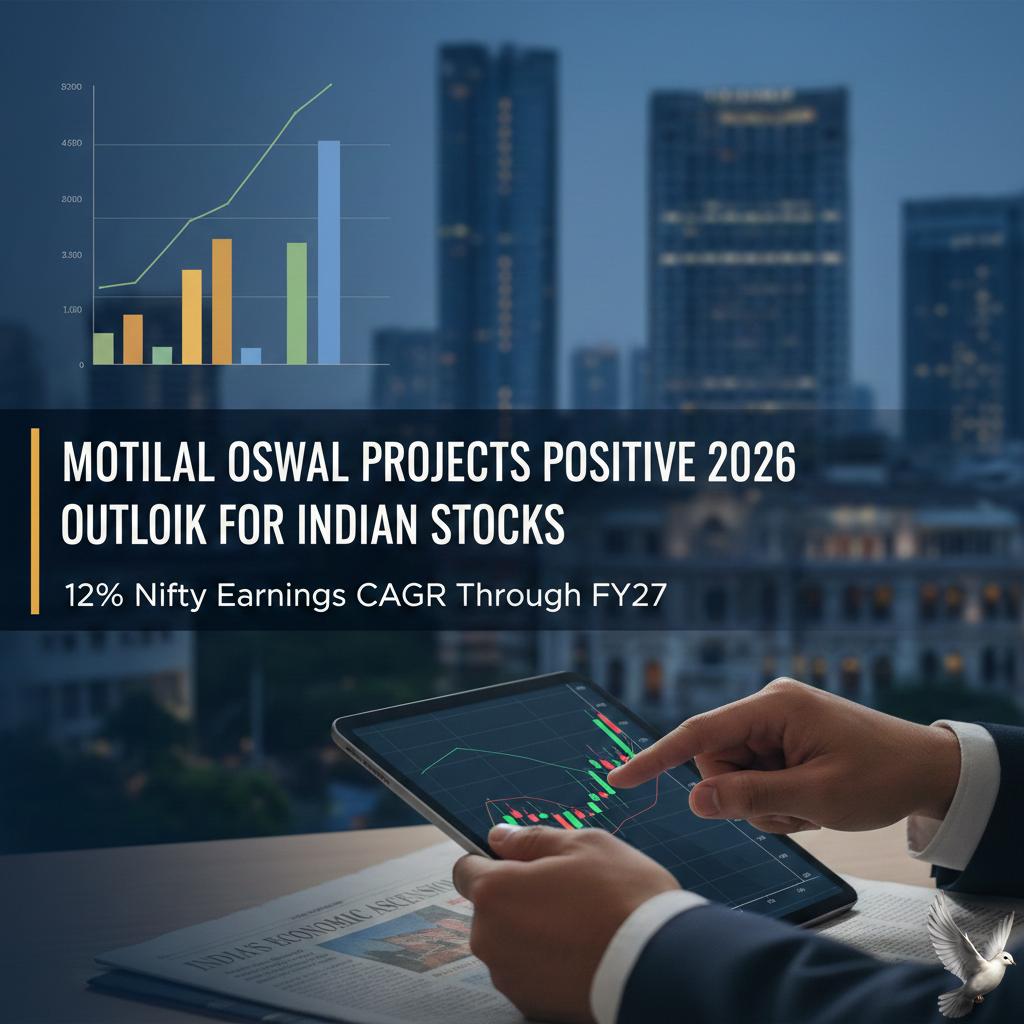

Motilal Oswal Projects Positive 2026 Outlook for Indian Stocks with 12% Nifty Earnings CAGR Through FY27

Market Outlook: India 2026 The Indian equity landscape is undergoing a significant transition in early **2026**. Following a period of consolidation and underperformance throughout **2025**, market sentiment is shifting toward a recovery phase. Benchmark indices are currently demonstrating renewed strength, with the **Nifty 50** trading near the **25,565** mark as of mid-February. Earnings and Valuations Corporate earnings are emerging as the primary catalyst for this turnaround. Projections indicate a Nifty earnings growth recovery to **9%** in **FY26**, with a further acceleration to a **12–14% CAGR** through **FY27**. This follows a stagnant **1%** growth rate recorded in **FY25**. Current valuations are becoming more attractive for long-term positioning. The Nifty's one-year forward price-to-earnings ratio is stabilizing near **21.5x**, which is only slightly above its long-period average. While large-caps offer reasonable valuation comfort, mid-caps and small-caps continue to trade at steeper premiums of **26%** and **50%** respectively, necessitating a more selective approach in the broader market. Institutional Flow Dynamics A structural shift in liquidity is providing a cushion against global volatility. In January **2026**, Foreign Institutional Investors (FIIs) remained net sellers with outflows of approximately **₹25,000 crore**. However, this was more than offset by Domestic Institutional Investors (DIIs), who recorded strong net buying of roughly **₹40,000 crore**. The influence of consistent SIP inflows—now exceeding **₹15,000 crore** monthly—has fundamentally altered the market's resilience. The aggressive selling that once triggered deep corrections is now frequently absorbed by domestic conviction. Macroeconomic Foundation India’s macro fundamentals remain among the strongest in the emerging markets. Real GDP growth for **FY26** is projected at **7.4%**, supported by a significant decline in headline inflation, which averaged **1.7%** in the latter half of **2025**. The **Reserve Bank of India (RBI)** has maintained a supportive stance, with the repo rate adjusted to **5.25%** to foster growth. External buffers are also robust, with foreign exchange reserves standing at approximately **$723 billion**, providing over **11 months** of import cover. Sector Performance and Outlook Banking and financial services are leading the current recovery, supported by steady credit growth and healthy asset quality. The **Bank Nifty** is maintaining levels above **60,500**, acting as a pillar for the broader benchmarks. Manufacturing and technology segments are also gaining momentum. The manufacturing sector is projected to grow by **6.2%** in **FY26**, while the services sector continues to lead overall expansion with a projected growth of **9.1%**. Investors are increasingly rotating into cyclicals and quality large-caps where earnings visibility remains high. The recent India–US trade deal and proposed GST slab rationalizations are expected to provide further tailwinds for export-oriented and consumption sectors throughout the year.

Fortis Healthcare Reports Consistent Growth and Expansion Plans

Fortis Healthcare has maintained a robust growth trajectory, reporting a 19.4% revenue increase in its hospital business for the quarter ended December 31, 2025. This performance was largely supported by a 14% rise in occupied beds and a 10% increase in Average Revenue Per Occupied Bed (ARPOB), which reached 2.56 crore per annum. Despite a 22% decline in consolidated net profit to 197 crore—impacted by a one-time exceptional loss of 45.9 crore related to new labor codes—the company’s operational fundamentals remain strong. The hospital business continues to be the primary growth engine, contributing 1,938 crore to the total consolidated revenue of 2,265 crore. Operating EBITDA margins for the hospital segment expanded to 21.7%, up from 20% in the previous year. Management has set a medium-term target to push hospital EBITDA margins toward the 24-25% range, driven by portfolio optimization and a higher mix of complex surgical procedures in specialties like Oncology and Renal Sciences. Occupancy levels currently stand at 67%, with the company anticipating a ramp-up to 70% within the next 12 months. This growth is being fueled by an aggressive expansion strategy. In January 2026, Fortis acquired the 125-bed People Tree Hospital in Bengaluru for 430 crore, with plans to scale the facility to over 300 beds. This follows the launch of Adayu, a 36-bed mental health facility in Gurugram, and the acquisition of Shrimann Hospital in Jalandhar. The diagnostics arm, Agilus Diagnostics, is also showing recovery with revenue growing 8.3% to 371 crore. Diagnostic margins saw a significant jump to 23.1%, aided by a shift toward higher-value specialized and preventive tests, which now account for 35% and 12% of the segment's revenue respectively. The company has expanded its diagnostic footprint to 4,370 touchpoints as of late 2025. On the stock market, Fortis Healthcare shares were trading around 916.75 on February 16, 2026. While the stock saw a minor intraday dip of 1.2%, it has delivered nearly 50% returns over the past year. Net debt has increased to 2,547 crore to fund recent acquisitions, bringing the net debt-to-EBITDA ratio to 1.24x. Analysts remain generally positive, citing a potential 26% EBITDA CAGR through 2028 as brownfield expansions at flagship facilities like FMRI Gurugram begin to contribute fully.